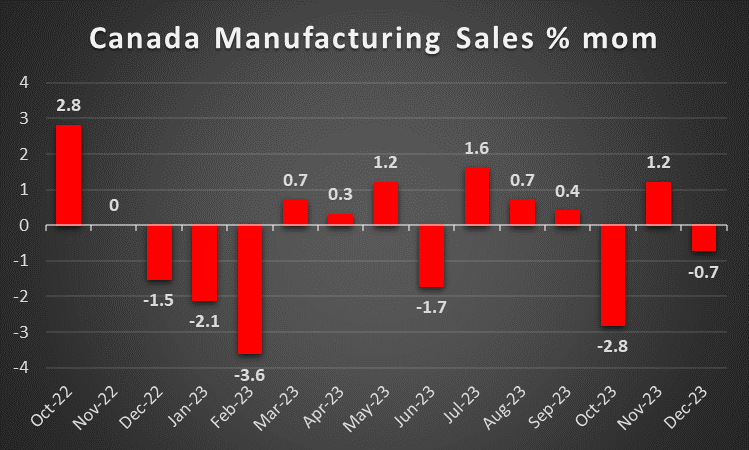

The week is about to draw to a close and we open a window at what next week has in store for the markets. In terms of financial releases, we make a start on a slow Monday, with Japan’s annualized GDP rate for Q4, Norway’s and the Czech Republic’s CPI rates both for the month of February. On Tuesday, we get Japan’s corporate goods prices rate for February, Australia’s Business conditions and confidence figures for February as well, followed by the UK’s ILO employment data for January and ending the day is the US CPI rates for February. On Wednesday, we note the UK’s preliminary GDP rate on a mom level and manufacturing output rate both for January and the Eurozone’s industrial production rate also for January. On Thursday, we note Sweden’s CPI rate for February, the US weekly initial jobless claims figure, PPI Final demand rate, and retail sales rate both for February and Canada’s manufacturing sales rate for January. Lastly, on Friday we get the US Industrial production rate for February and the US preliminary University of Michigan sentiment figure for March.

USD – US February CPI rates in focus

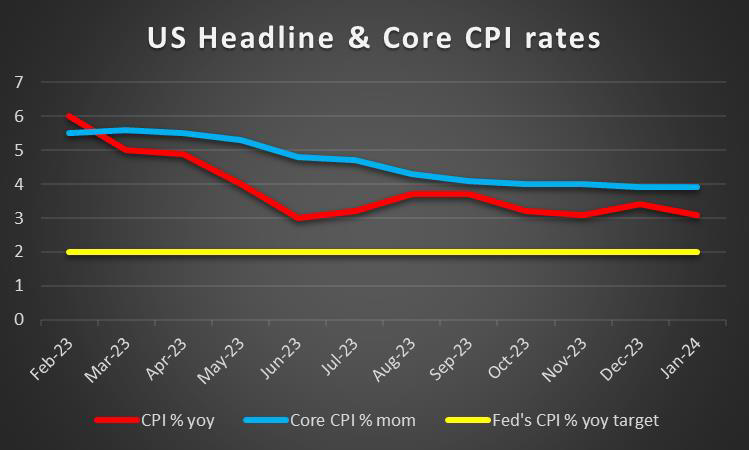

The USD is about to end the week lower against the EUR, JPY, and the pound in a sign of general weakness. On a fundamental level, highlight the recent news regarding Commercial Real estate loans, which appear to be causing concern amongst economists regarding the resilience of US regional banks. Should we see a repeat of the mini-banking crisis that occurred last March, it could have dire consequences for the US economy, yet for now such a scenario appears to be far far away. On a political level, we note that the markets may be preparing for a Trump versus Biden rematch in November, following the dropping out of Niki Hailey on Thursday. On a monetary level, we note that our concerns about inflationary pressures remaining entrenched in the US economy seem to have been re-iterated by Fed Chair Powell during his testimony to Congress on Wednesday. In particular, Fed Chair Powell stated that even though “Inflation has eased notably over the past year”, the bank remains concerned that “reducing policy restraint too soon or too much could result in a reversal of progress we have seen in inflation”. The comments seem to echo the points made by Atlanta Fed President Bostic on Monday that “it is premature to claim victory in the fight against inflation”. However, Fed Chair Powell did confirm that should the economy continue on its current trajectory “it will likely be appropriate to begin dialing back policy restraint at some point this year”, which appears to have overpowered the hawkish rhetoric of keeping interest rates higher for longer this year, and thus weighing on the dollar. Nonetheless, we tend to agree with Fed Chair Powell that it may be prudent to cut rates this year when the time is appropriate, yet the timing of these cuts may not be in line with current market expectations that the Fed may begin cutting in June and thus may support the dollar further down the line. On a macroeconomic level, we note the abnormal amount of mixed signals being sent by financial releases this week. Starting with the S&P Services PMI figure for February, which implied an expansion of economic activity in the services industry at a greater pace than what was expected, which was then contradicted by the ISM Non-Manufacturing PMI figure which came in lower than expected, implying an expansion but at a slower pace. Furthermore, during the week, the ADP Non-Farm Payrolls figure for February came in lower than expected, implying a loosening labor market, yet the JOLTs Job Openings figure for January exceeded expectations implying that demand for labor is on the rise. As such despite the two financial releases providing figures for two different months, their release during this week may have canceled out each other’s potential impact on the dollar. Nonetheless, the stage is set for the US Employment data for February which is due to be released later today and could shake the markets. For next week we highlight the US CPI rates and should they slow down as expected or come in even lower it could allow the Fed to adopt a more dovish stance, thus weighing on the dollar and vice versa. Moreover, we would like to highlight the US Retail sales for February which is expected to increase, potentially moderating the possible negative implications of the CPI rate. Lastly, we would like to point out the University of Michigan’s Preliminary consumer confidence figure for March, due to be released on Friday.

GBP – GDP rate next week

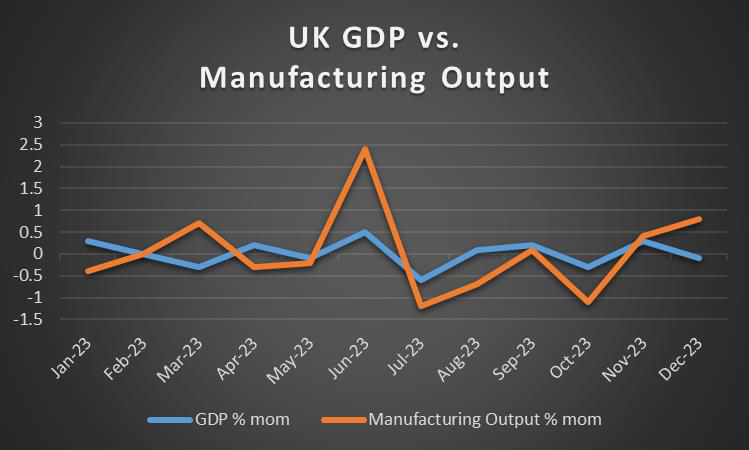

The pound seems about to end the week relatively unchanged against the EUR and JPY yet stronger against the USD. On a macroeconomic level, this week was slightly more interesting for pound traders in terms of financial releases stemming from the UK. The UK’s Services PMI figures for February came in lower than expected, implying that despite the continued expansion in the service industry, it appears to be slowing down, an issue further highlighted by the release of the Construction PMI figure for February. Despite the Construction PMI figure coming in higher than expected, it still implies that the construction sector is contracting and may be worth monitoring in the future. Lastly, the Halifax House price rate for February increased at a decreasing rate, yet proved to be immaterial in influencing the direction of the pound. Overall, it appears that the markets have widely ignored the financial releases stemming from the UK and may have instead ceded control of the GBP’s direction to the fundamentals. In particular, the government’s annual budget deliverance to parliament by Finance Minister Jeremy Hunt on Wednesday, which saw a 2p cut in national insurance contributions by employers which may have aided the pound from a symbolical standpoint, yet in the grander scheme of things it may prove insignificant to the current economic situation. As such, we turn to what next week has in store for pound traders, starting with the UK’s employment data for January. Should the employment data imply an easing labor market, it could weigh on the pound. Thus, should the data showcase the aforementioned scenario, we may see pressures being exerted on the BoE to ease its monetary policy which in turn could weigh on the pound as well and vice versa. Furthermore, the country’s GDP rate for January is also expected to be released on Wednesday, where should it be implied that the UK economic activity is contradicting even further, it could weigh on the pound. Whereas, should it return to expansion, it could support GBP. We would not be surprised to see the UK flirt with recession territory, as the financial releases this week tended to paint a concerning outlook for the UK economy and thus we would maintain a bearish outlook for the GBP in the upcoming week on a macroeconomic level.

JPY – The hike debate is on!

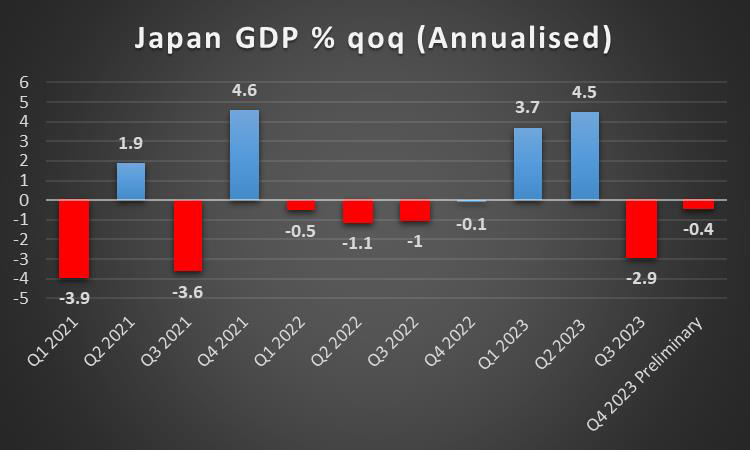

JPY seems about to end the week in the greens against the USD, slightly stronger against the EUR and relatively unchanged against the GBP. We note that on a macroeconomic level, Japan’s Tokyo CPI rate for February which was released on Tuesday, appeared to confirm last week’s BOJ Core CPI rates regarding the persistence of inflationary pressures in the Japanese economy. Furthermore, we highlight two financial releases from Japan this week, with the Service PMI figure for February coming in higher than preliminary estimated, implying an expansion in the Japanese service industry wider than initially thought, thus increasing optimism for the economy’s services sector resilience. Furthermore, the average cash earnings rate on a yoy basis accelerated to 2.0%, which was higher than expected and appears to be in line with the BOJ’s ambitions of an increase in real wages before potentially abandoning its ultra-loose monetary policy. As such on a monetary level, with the bank’s inflation target now seemingly in sight and an apparent increase in real wages also now in play, the rhetoric surrounding the BOJ’s potential exit from its decades-long ultra-loose monetary policy, appears to be intensifying amongst policymakers. In particular, BOJ Governor Ueda stated according to some sources that “the likelihood of achieving 2% inflation is rising” and that it is “possible to exit stimulus while aiming for 2% inflation target”, thus further aiding the narrative that the bank is preparing to abandon its ultra-loose monetary policy, which appears to be aiding the Yen’s ascent. Therefore, our opinion that was expressed in last week’s report appears to be slowly coming to fruition, that “to be convinced that the bank is prepared to normalize its monetary policy during its April meeting, we would require a series of BOJ policymakers to release a series of statements spread throughout March” implying that the bank is preparing to normalize its monetary policy and is sending out hints via a series of smaller communications to market participants. This could be supported based on comments that were made by BOJ policymaker Nakagawa on Thursday that she will “assess and discuss policy tools at the upcoming meeting”, which aids our aforementioned hypothesis and in turn, could support the Yen. Lastly, the next hurdle for Yen traders may be Japan’s revised GDP rate for Q4 on a yoy basis which is due to be released on Monday. Should the GDP rate come in higher than expected, implying economic growth, it could provide some leeway for the BOJ to adopt a more hawkish tone, thus supporting the JPY. Whereas, should it come in lower than expected thus implying a further dive into recession territory, we may see the BOJ’s rhetoric softening and the JPY weakening as a result. Other than that, Yen traders may also keep an eye out for Japan’s corporate goods price rate for February, which is due to be released. However, we believe that its release may be overshadowed by the GDP rate on Monday, as it may dominate next week’s news airtime.

EUR – ECB remains on hold as was expected

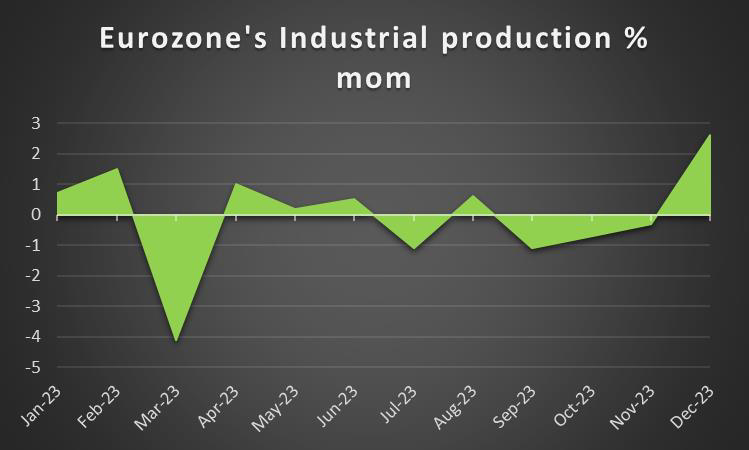

The EUR seems to be on track to end the week in the greens against the dollar, yet lower against the pound and rather stable against the Yen. On a fundamental level, we note that European Parliament President Von der Leyen has won the backing of the European People’s Party group which is the largest party in the EU parliament, to serve for a second term as President of the commission. On a macroeconomic level, we note that the PMI figures for Germany, France and the Eurozone as a whole were better than expected for the month of February, implying that economic activity appears to be picking up, which seems to have supported the EUR following their release. Yet, with the exception of the Eurozone’s Services PMI figure, the PMI figures are still in contraction territory, as such from a more macro perspective, should they deteriorate further it could weigh on the EUR. Also macroeconomically we note the release of the Eurozone’s Q4 final GDP rate, highlighting the difficulties the Eurozone economy faces to grow. On a monetary level, the ECB remained on hold as was widely expected, yet in the bank’s accompanying statement, ECB Staff revised down their Core inflation expectations to 2.6% for 2024, 2.1% for 2025 and 2.0% by 2026, scoring a win for the ECB’s doves. The revisions appear to have weighed on the EUR as the case for the ECB to maintain its hawkish stance appears to have been weakened. Furthermore, during the post-decision press conference, ECB President Lagarde had to clarify to a press member that she “did not say there was no rush” when referring to cutting interest rates. The unscripted moment may infer that the ECB has been a recipient of pressures to cut rates and as such could weigh on the EUR, should ECB officials adopt a more dovish tone. However, at the time of the comment, the markets appeared to have glossed over that possibility as the common currency continued on its ascent.

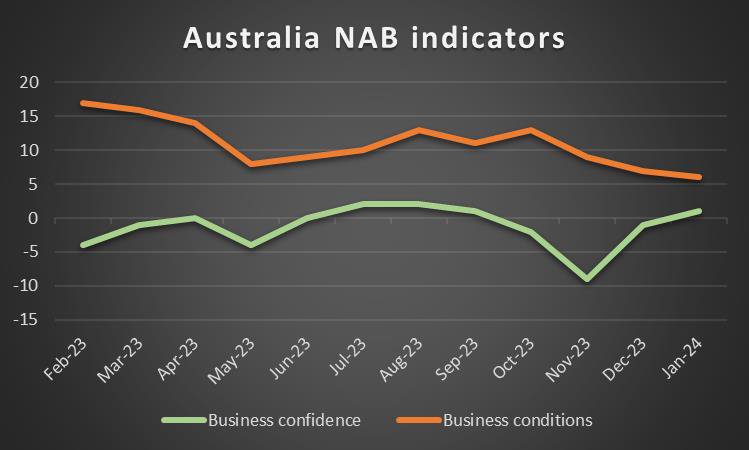

AUD – Business figures next week

AUD is about to end the week higher against the USD, recouping with interest last week’s loses. On a fundamental level, we note that the Aussie’s commodity currency nature tends to make it sensitive to market sentiment. The Aussie may prove particularly sensitive to developments in China given their close economic ties. Hence we note on a political level, that China’s annual National Peoples Conference took place earlier on this week, breaking a tradition of the “two sessions” meeting, with the scrapping of the premier’s press conference. The event was seen as a way to see China’s number 2 in an unscripted environment. Moving on to a macro-economic level, Australia’s GDP rate for Q4 on an annualized basis came in higher than expected, implying a wider than anticipated expansion in economic activity in Australia, which in itself appears to have supported the Aussie. Furthermore, given Australia’s close economic ties with China, the Chinese trade data for February vastly exceeded expectations, implying that the Chinese economy may be recovering and is expanding. In turn, an apparent expansion in China’s economy could lead to increased demand for raw materials from Australia, which may further support the Aussie on a long-term basis. However, not all was positive this week, as China’s Caixin services PMI figure came in lower than expected, although the 0.4 difference may prove to be insignificant in the grander scheme of things thus having no material impact on the CNY and AUD. Lastly, next week’s highlights for Aussie traders may be the Business Conditions and Business confidence figures both for the month of February on Tuesday, yet they may have a minimal impact on the Aussie, as other economies may have more impactful financial releases in the upcoming week.

CAD – BoC remains on hold

The Loonie is about to end its 9-week losing streak against the USD with a bang. On a fundamental level, we note the sensitivity of the CAD to the market sentiment as a commodity currency. The positive correlation of the CAD with oil prices appears to have diverged once again despite Canada’s status as a major oil-producing economy. Oil prices this week tended to move lower following reports that oil supply may be exceeding demand, yet the invitation for the Loonie to turn it down a notch appears to have been lost in the mail. The divergence between the two remains a point of interest and in our opinion may warrant closer attention should it continue as it is irregular. Nonetheless, on a macroeconomic level, Canada’s trade balance figure for January exceeded expectations by coming in at 0.50B versus the expected figure of -0.10B. Furthermore, the building permits rate on a mom basis for January, came in at a shocking 13.5% which is much greater than the expected rate of 4.6%. Following the release, the FX markets appear to have reacted

positively to the news, with the Loonie strengthening against the dollar. Lastly, we would like to note that Canada’s employment data for February, is due to be released later on this afternoon. The employment data is expected to imply a loosening labour market, with the employment change figure expected to decrease to 21.1k and the unemployment rate expected by economists to tick up to 5.8%. In such a scenario, we may see the Loonie weakening slightly as the week comes to a close. On the other hand, should the data send mixed signals or showcase a tight labor market, the Loonie might potentially gain as the week comes to a close. On a monetary level, we highlight BOC’s interest rate decision in which the bank remained on hold, as was widely expected. In the bank’s accompanying statement, it was said that the “Governing Council wants to see further and sustained easing in core inflation”, implying that the bank may not be preparing to cut interest rates just yet, as it may require some ‘convincing’ from financial releases. Furthermore, BoC Governor Macklem during the QA session following the monetary policy decision stated that “if we look beyond shelter, we’re seeing underlying inflation persist”, which could be interpreted as an unwillingness by the bank to cut rates anytime soon. As such, the bank’s accompanying statement in addition to BoC Governor Macklem’s comments may have been perceived as hawkish in nature by market participants, which in turn appears to have provided support for the Loonie.

General Comment

Overall, in the coming week in the FX market, we expect some volatility, as high-impact financial releases are still being released. On the other hand, US stock markets appear to be ending the week in the reds. Nonetheless, we highlight that the release of the US employment data later on today, could easily change their current trajectory. Also, note that the earnings season seems to be over and may continue next month. Furthermore, gold formed new all-time highs during the week. Moreover, the continued decline of US yields tended to support the non-interest-bearing precious metal’s price.

如果您对本文有任何常规疑问或意见,请直接发送电子邮件至我们的研究团队,地址为 research_team@ironfx.com

免责声明:

本信息不被视为投资建议或投资推荐, 而是一种营销传播. IronFX 对本信息中引用或超链接的第三方提供的任何数据或信息概不负责.