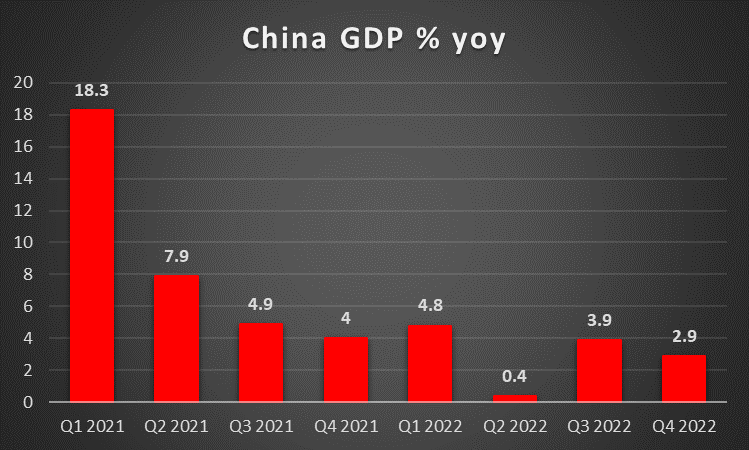

Market worries of a recession appear to be making a comeback this week and with inflationary pressures remaining high we take a look at what next week has in store for the markets. On the monetary front, we note a relatively busy week from monetary policymakers, with Fed policymakers Williams and Mester speaking on Thursday followed by Bostic and Harker on Friday and finishing of the week we have ECB De Guindos on Friday as well. On a more fundamental note, we note the release of the RBA April meeting minutes on Tuesday. As for financial releases, we make a start on a quiet Monday the NY Fed Manufacturing survey. On Tuesday, during the Asian session, we note the release of China’s Industrial Output for March and Q1 GDP rate and in the European session, the UK employment data, Eurozone’s trade balance for February, Germany’s ZEW indicators for April and during the American session we note the release of the US Housing Start figure and the Canadian CPI Print all for March. On Wednesday, during the Asian session, we make a start with Japan’s Tankan N-mfg Indx for April and in the European session, we have the UK’s CPI print followed by the Final HICP rate for the Eurozone all for March and during the American session we have Canada’s Producer Prices for March. On Thursday, during the Asian session, we make a start with New Zealand’s CPI print for Q1 followed by Japan’s trade balance for March and during the European session we have Germany’s Producer Prices rates, France’s Mfg Business Climate all for March and finishing off during the American session we have the US weekly Jobless claims, the Philly Fed Business Index and the Eurozone’s Preliminary Consumer confidence both for the month of April. Lastly, on a very busy Friday, we begin during the Asian session with the Australian Judo Bank Preliminary PMI figures, the UK’s GfK consumer confidence both for April followed by Japan’s CPI print for March, during the European session we have the UK’s Retail sales for March followed by France’s, Germany’s, the Eurozone’s and UK’s Preliminary PMI figures all for April. During the American session, we note Canada’s retail sales for February followed by the US Preliminary Composite PMI figures for April.

USD – Recession worries re-ignited.

The USD is about to end the week in the reds against its counterparts for the seventh week in a row. On a fundamental note, we note that market worries of a recession have heightened as the FOMC March meeting minutes clearly stated that the Fed anticipates a mild recession to occur. Despite stronger than anticipated US employment data last Friday, the release of the US CPI rates came in lower than anticipated which translated into a weaker greenback thus evaporating the gains made on Friday’s session. On a monetary note, this week, we had three Fed FOMC voting members with public engagements, with Minneapolis Fed President Kashkari and Philadelphia Fed President Harker both re-iterating hawkish comments made by their colleagues last week, fueled speculation of a rate hike in the next FOMC meeting. However, Chicago Fed President Goolsbee reminded traders that not all members are on the same page, stating “Given how uncertainty abounds about

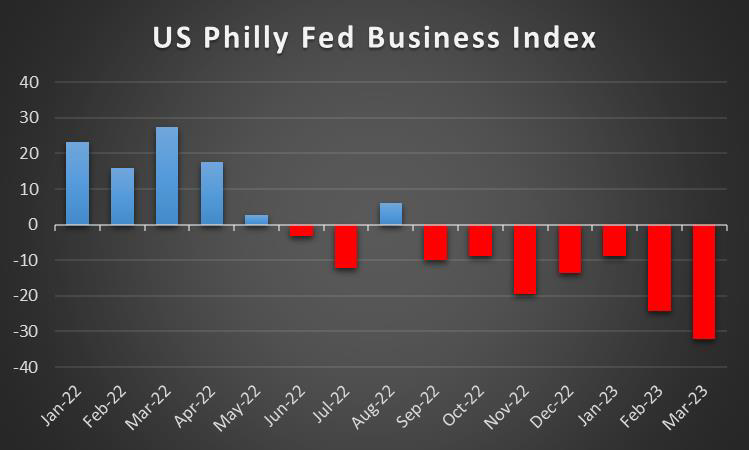

where these financial headwinds are going, I think we need to be cautious”. As such, despite the vote to hike being unanimous, the growing dovish sentiment as seen by the FOMC meetings may play a key role in the FOMC May meeting. On a macroeconomic level, we note the release of the S&P Mfg PMI for the US next week in addition to the Philly Fed Business index as this may verify the expectations of a slowdown by the Fed and the IMF which may further weaken the dollar. On the other hand, should the data provide a contradictory outlook we may see the greenback strengthening as the Fed is itching for data to support a further rate hike.

GBP – Traders await CPI print.

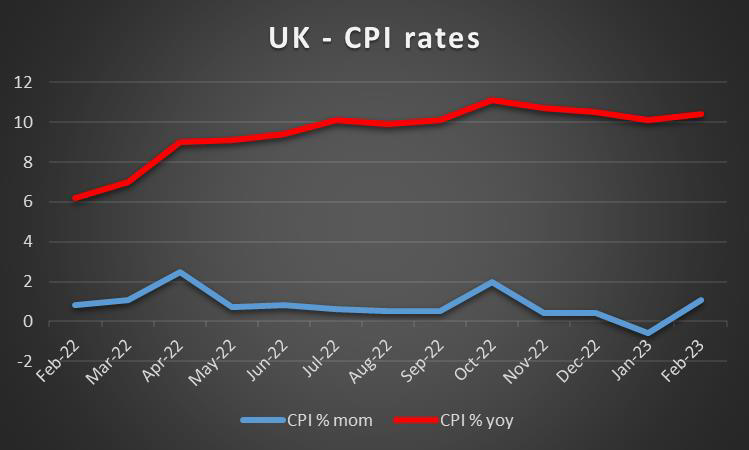

The pound is about to end the week stronger than the dollar and the Yen, yet weaker than the euro. On a fundamental note, we highlight the fact that during the IMF meetings this week, the British economy was predicted to be the worst-performing out of the G7, with a predicted decline in Real GDP by -0.3% in 2023. As such the pound ending the week in the greens against the dollar and the yen may not be a sign of pound strength but dollar and Yen weakness. On a monetary level, we highlight BoE Bailey’s speech on Wednesday in which he stated that “Today I do not believe we face a systemic banking crisis.”. In combination with his opinion during the same speech that QT is implemented “gradually, and not in stressed times”, may imply that Bailey is willing to continue with hiking rates further during the BoE’s May 13th Meeting. Furthermore, the replacement of MPC Tenreyro with Megan Greene may cause a change in power within the MPC hence providing support for the pound if Greene’s comments are perceived as hawkish, given that Tenreyro’s comments seemed to lean on the dovish side. On a macroeconomic level, we note the release of the UK’s CPI print, Gfk consumer confidence, retail sales and preliminary manufacturing & services figures which may validate the IMF’s hypothesis of a decline in the British economy. Hence if this is validated, we may see the pound weakening as the MPC may decide to hold or cut rates in order to prevent the economy from entering a recession.

JPY – Yen faces safe haven outflows

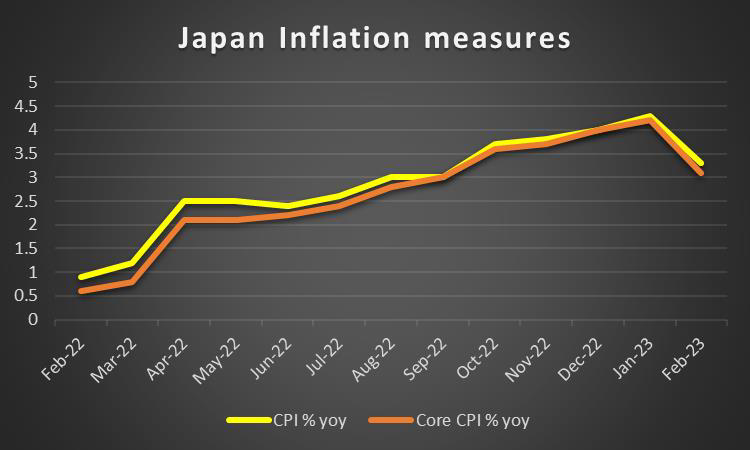

The JPY is about to end the week in the reds against the common currency and the pound, but stronger than the greenback. implying that the JPY has shown a general sign of weakness as market worries of a prolonged banking crisis have eased. BoJ’s Governor Ueda formally took over as head of the Bank of Japan on Sunday, taking the reins from Mr.Kuroda. During his first meeting as head of the bank, Governor Ueda re-iterated the need to stick to the ultra-loose monetary policy stating according to FT that “In light of the current economic, price and financial conditions, it is appropriate to maintain the yield curve control for now”. Analysts had previously anticipated some sort of indication by Ueda that the BoJ would be gradually phasing out the YCC used by his predecessor for over a decade, thus weakening the JPY. On a macro level, we note the release of Japan’s PPI this week and it was indicative of some sort of inflationary pressure are still visible in the economy as the rate had risen for March on a month on month basis. However, traders will most likely be anticipating the release of Japan’s Reuters Tankan Non-Mfg Idx on Wednesday and Japan’s trade data on Thursday, while we highlight the release of the CPI rates next Friday. If the CPI print comes in lower than anticipated, then we may see the JPY weakening as the pressure on BoJ may ease, and vice versa.

EUR – Market worries ease.

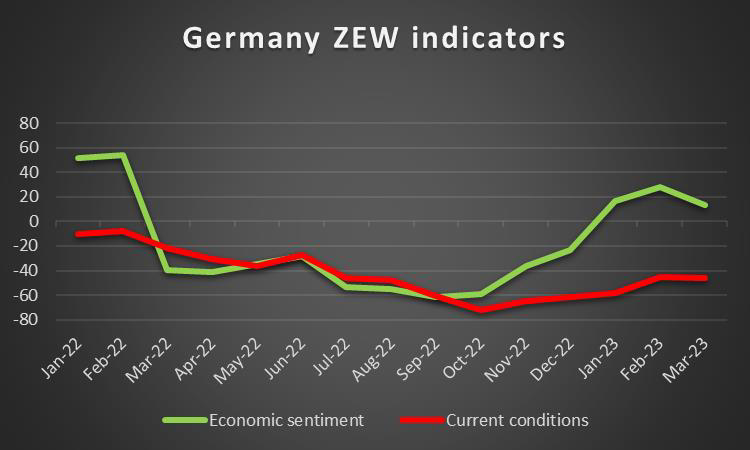

The common currency saw strengthening across the board this week and is about to finish in the greens against the dollar, JPY and the pound. On a fundamental note, we acknowledge the fact that the French protests are continuing as Macron’s deeply unpopular government faces staunch opposition hence potentially weakening one of Europe’s largest economies, which in turn may affect the EUR in the long run. On a monetary front, we highlight the speeches by ECB policymakers De Guindos and Holzman whose rhetoric appeared to be hawkish yet slightly different. For example, ECB Vice President De Guindos on Wednesday stated that “Underlying inflation is proving to be much stickier” and Holzmann on Monday “I would not rule them (rate hikes) out but I would also not say that they will necessarily come either”. Both comments provided support for the common currency, as they strengthen the case for further interest rate hikes. However, it may provide some insight as to the perceived terminal rate, as ECB’s Holzmann prior to the mini-banking crisis had called for three more rate hikes of 50 basis points according to Reuters. The comments made on Wednesday are contradictory to this, as a slither of doubt can be sensed. Hence if the rhetoric from Holzmann changes to slightly dovish then we may see a weakening of the common currency. On a macro outlook, we note Germany’s declining CPI rates as a sign that the eurozone is seeing an easing in inflationary pressures, as being one of the largest economies in the Eurozone, Germany’s data has a significant impact on the common currency in general. EUR traders may find further support next week in the event that Eurozone’s, France’s and Germany’s Preliminary PMI figures for April improve as that would imply an improvement in economic activity for the area. Also, we note Germany’s ZEW Economic sentiments, as we also note Germany’s PPI rates and Eurozone’s final HICP rates for March. In the event of continued inflationary pressures the ECB could continue with its rate hikes, hence overall providing support for the common currency.

AUD – AUD in the clear?

The Aussie appears to have strengthened against the USD as this week draws to a close. On a fundamental note, we give emphasis to the deterioration in the US-Sino relationship which could potentially negatively affect the Aussie in the long run. Considering the recent developments following Taiwan’s President Tsai Ing-Weng meeting with House Speaker McCarthy last Wednesday, which provoked China to announce military drills around the island over the past weekend. The developments sparked renewed fears of tensions between the world’s biggest superpowers may negatively affect the AUD, given the reliance of Australia on China and the US. On a monetary note, RBA’s Deputy Governor Bullock speaking on Wednesday revealed that the RBA was considering a rate pause before the SVB collapse according to Bloomberg, which may have weakened the AUD. However, Bullock stated that “There is trouble brewing in the rental accommodation market and that has implications for inflation” as such implying that there is still a possibility that the pausing of rate hikes is temporary. On a macroeconomic level, we highlight the fact that the Australian labor market remains tight following this week’s release of employment data. We can deduce that despite the change in employment decreasing, it did so by only a fraction of what was anticipated by market analysts, spiking mass support in the Aussie. Furthermore heading into next week’s financial releases with the Judo Bank Mfg and Composite PMI figures in addition to the Composite Leading Idx rate, traders may be anticipating the data to further support the strengthening of the Australian economy, hence providing support for the AUD.

CAD – BoC holds interest rates steady.

CAD – BoC holds interest rates steady.

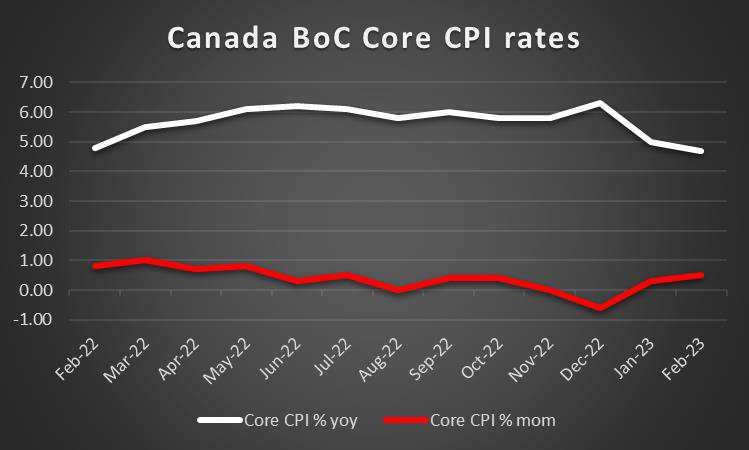

The Loonie strengthened against the dollar for the week. Fundamentally we note the continued support in the Canadian economy as a result of OPEC+ oil production outputs continues to support the CAD, given that Canada is a major oil exporter. On a macroeconomic level, we note the statements made by US Energy Secretary Jennifer Granholm on Wednesday, were according to Reuters the US is considering the possibility to refill their strategic petroleum reserves. In the event that the US decides to refill it’s SPR then we could see an increase in the price of oil as demand increases. Note that the current rise of oil prices is in addition to banking sector worries subsiding regarding Toronto-Dominion bank and have set the CAD on an upwards trajectory. On a monetary level, as was anticipated the BoC on Wednesday did not raise interest rates, hence we could attribute partial strengthening in the CAD to the comments made in the forward guidance of the bank stated that “getting inflation the rest of the way back to 2% could prove to be more difficult”. Implying that the BoC may hold interest rates at current levels but it may be too soon to start cutting due to the perceived long-term difficulties of bringing down inflation. Furthermore traders await the CPI rate due out on Tuesday as it will provide helpful insight as to the inflationary pressures in the Canadian economy. Should they decrease as expected we may see the CAD weakening as BoC’s position to remain on hold may solidify and on the other hand if the CPI print is higher than predicted then we may see the CAD strengthening as a case might be made for further hikes to resume.

General Comment

As a closing comment, following IMF’s grim outlook on the world economy as the Spring meetings began this week, we highlight the increasing risk of market volatility as fears of a recession have resurfaced. Following the Fed minutes revealed that the FOMC expects a mild recession to occur, we may see the USD continue to decline over other currencies as traders await Preliminary US financial releases onwards. In the equities market, the market sentiment seems to have improved following the weakening of the greenback. With Earnings releases due, we make a start on Friday with JPMorgan(#JPM),Wells Fargo(#WFC) and Citigroup(#C). On Tuesday we await the earnings release of Johnson&Johnson(#JJ) followed by Bank of America(#BAC), Lockheed Martin(#LockheedMT) and GoldmanSachs(#GS). On Wednesday we begin with Tesla’s (#TSLA), Morgan Stanley (#MS), IBM (#IBM), Rio Tinto ADR (#RIO), Travelers (#TRV) and Alcoa(#AA). Thursday we anticipate earnings by BHP Group (#BLT), Phillip Morris(#PhilMorris), AT&T(#T), American Express(#AXP) and lastly Xerox(#Xerox). Also, the weakening of the USD may provide a cautionary tale to gold traders to be on alert for any possible spikes in the precious metal’s price. Gold continued its ascent higher this week capitalizing on USD weakness displaying once again their negative correlation.

如果您对本文有任何常规疑问或意见,请直接发送电子邮件至我们的研究团队,地址为 research_team@ironfx.com

免责声明:

本信息不被视为投资建议或投资推荐, 而是一种营销传播. IronFX 对本信息中引用或超链接的第三方提供的任何数据或信息概不负责.