After a rather volatile week, with USD weakening being probably the main characteristic move in the FX market, we open a window to what next week has in store for the markets. On the monetary front, two events stand out, the first being the release of RBA’s July meeting minutes on Tuesday’s Asian session and the second from Turkey CBT’s interest rate decision on Thursday. Nevertheless, various central bank policymakers are scheduled to make statements and could alter the market’s expectations. As for financial releases we make an early start on Monday with China’s Urban investment, industrial output and retail sales growth rate for June as well as China’s GDP rates for Q2. On Tuesday we get the US retail sales growth rates, Canada’s CPI rates and the US industrial production growth rate all being for June. On Wednesday we note the release of New Zealand’s CPI rates for Q2 and UK’s CPI rates for June. On Thursday we note the release of Japan’s trade data for June, Australia’s employment data for the same month and from the US the weekly initial jobless claims figure, July’s Philly Fed Business index and Eurozone’s preliminary consumer confidence also for July. Finally on Friday we note the release of Japan’s CPI rates for June, UK’s retail sales for the same month and Canada’s retail sales for May.

USD – Greenback weakens as US CPI rates slowdown

The USD is ending the week quite lower against its counterparts. Yet USD’s weakening started at the end of last week as the drop of the NFP figure as reported in the US employment report for June tended to disappoint traders. Yet a cooler look at the data tends to show a mixed picture. Despite the drop, the NFP figure is still at rather healthy levels and the fact that the unemployment rate ticked down to 3.6%, implied that the US employment market remains tight. Furthermore, the average earnings growth rate accelerated, implying that the US employment market may continue to feed inflationary pressures in the US economy. Yet Fed policymakers on Monday tended to ease market worries for the Fed’s hawkish stance, as they implied that two more rate hikes may conclude the Fed’s rate hiking cycle. The final hit for the USD came on Wednesday as the CPI rates slowed down more than expected both at a headline as well as at a core level. The market seems to maintain its expectations for another possible hike by the Fed in its next meeting yet almost fully erased the possibility of a rate hike after that and expects a rate cut in Q12024. Overall, we tend to expect the USD to remain on the backfoot if the market’s expectations for an easing of the Fed’s

GBP – Focus on CPI rates

The pound seems about to end the week stronger against the USD yet is losing ground against the EUR and JPY. Nevertheless, pound traders seem to remain confident possibly also due to the results of the stress tests conducted by BoE regarding the financial stability of the UK. The results showed that UK lenders were well capitalized to go through a possible economic crisis , a scenario that allows practically BoE to maintain its hawkish approach and proceed with more rate hikes in the months to come. Comments by BoE Governor Bailey earlier this week tended to highlight how sticky inflation seems to be in the UK economy, at least stickier than other developed rich economies, yet also stated that expects inflation to come down “markedly” over the next few months. On a macroeconomic level, we note a crack in the tightness of the UK employment market for May as the unemployment rate rose to 4.0% and the employment change figure dropped to 102k. Yet the average earnings growth rate accelerated implying that the UK employment market continued to support inflationary pressures in the UK economy. On the other hand the GDP and manufacturing output growth rates contracted and given BoE’s hawkish intentions our worries for the outlook of the UK economy tend to enhance. Hence we highlight in the coming week the release of the CPI rates for June as well as the retail sales growth rate that may provide a deeper insight to the consumption side of the UK economy.

JPY – Yen strengthening evident

JPY seems about to end the week in the greens against the USD, the EUR and the GBP for a second week in a row in a sign of continued broader strength. On the monetary front, BoJ seems set to keep its ultra-loose monetary policy settings in place for now. It’s characteristic that BoJ Deputy Governor Uchida was reported stating that he does not anticipate rate hikes in the near future. Yet market expectations for some form of monetary policy

tightening in the July meeting are intensifying. Market analysts tend to highlight the possibility of the bank tweaking again its Yield Curve Control policy allowing for its tolerance to Japanese Government Bond (JGB) yields to widen before proceeding with more bond purchases. The rumours were further fuelled by early signs of demand-led inflation, especially in the HORECA sector. Despite this being a plausible scenario, we tend to maintain the view that the bank may prefer to keep its settings unchanged, given that the general inflation level seems to continue to drop in Japan, forcing the bank to maintain a wait-and-see position on where inflation may settle down. Also, we would expect that BoJ may prefer not to widen its tolerance bands on JGB yields, but to erase them all together, should the time come. For the time being though even a stabilisation of market expectations that the end rate is nearing for the Fed but also a number of other central banks, may narrow the interest rate differentials and benefit JPY. On a more fundamental level, we note that JPY’s dual nature as a safe haven may once again affect its course as should market worries ease further we may see JPY experiencing safe haven outflows.

EUR – Fundamentals to continue leading the EUR

The common currency is about to end the week higher against the USD, and GBP yet seems to be losing ground against the JPY. On a macroeconomic level, we highlight our worries for the outlook of the Eurozone. It’s characteristic that Germany’s ZEW indicators for July were worse than expected, implying a more pessimistic outlook and deteriorating conditions on the ground for the largest economy of the area. But also the slowdown of Eurozone’s industrial output growth rate for May was not a good sign. On the other hand, the slowdown of France’s HICP rates for June and the acceleration of Germany’s respective HICP rates was confirmed sending some mixed signals. On the monetary front, the ECB’s hawkish intentions are still present and the market prices-in another rate hike in its July meeting and another one in September. For the time being we note that ECB Governing Council member De Galhau was reported stating that the ECB is nearly finished raising interest rates but will keep them at a “a high plateau, on which we will have to remain for a sufficiently long time to fully transmit all the effects of monetary policy.”. Furthermore, Bank of Portugal Governor Mario Centeno stated that “Inflation is coming down faster than the way up,”. Overall the comments tend to ease market worries for the bank’s hawkish intentions and should they ease further they may weigh on the common currency. Yet we tend to remain a bit worried for Germany’s sticky inflation as it may force Germany’s Bundes Bank to maintain a hawkish stance.

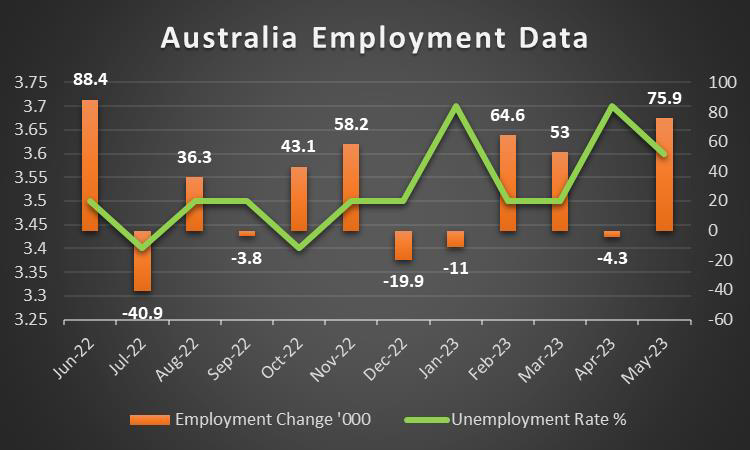

AUD – Employment data eyed

The Aussie repeated last week’s rise against the USD in another steep upward movement. On a more fundamental level, we note that the improvement of the market sentiment tended to help the commodity currency AUD, as it is considered to be more risky. Furthermore, we tend to maintain our worries for the recovery of the Chinese economy. We would note the release of China’s trade data for June. The worrying part is that Chinese exports contracted even further, yet the trade surplus was allowed to rise as imports also fell. Nevertheless, the news imply lower economic activity for China’s economy, which could be stressed even further, yet we expect a bottoming out near the end of the year. For the time being, given the close Sino-Australian economic ties, any indication that the Chinese economic recovery is slowing, may have an adverse effect on AUD. On a monetary policy level, we note for next week the release of RBA’s July meeting minutes which may shed more light in regards to the bank’s intentions. For the time being the market seems to expect another rate hike after a pause in the August meeting. We should also note that RBA Governor Lowe announced that the bank is to cut the number of meetings from next year onwards. It still remains to be seen if Mr. Lowe is to be replaced by someone else at the head of the bank.

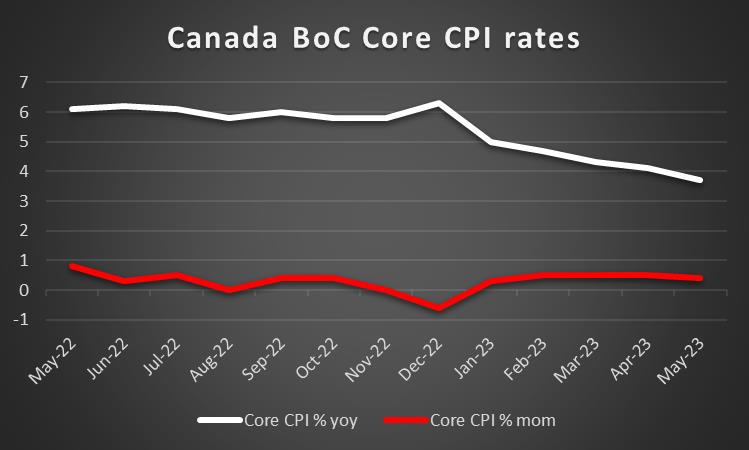

CAD – BoC hikes rates, remains hawkish

The CAD is about to end the week in the greens against the USD, almost fully reversing the losses of the prior two weeks. On the monetary front, we highlight BoC’s interest rate decision on Wednesday. The bank as was expected hiked rates by 25 basis points. Furthermore, in its accompanying statement the bank stated that “accumulation of evidence that excess demand and elevated core inflation are both proving more persistent” and cited it as a reason for the rate hike. It also stated that it will continue to “assess the dynamics of core inflation and the outlook for CPI inflation” in its decision-making process for more rate hikes. It was also characteristic that BoC Governor Macklem verified the stubbornness of underlying inflationary pressures in the Canadian economy in the opening statement of his press conference. That’s why we highlight the release of Canada’s CPI rates for June on Tuesday. On a macro-economic level, we note that Canada’s employment data tended to show a relatively tight employment market, despite the rise of the unemployment rate to 5.4%, as the employment change figure shot up to 59.9k, providing some support for the Loonie. Furthermore, we also note the acceleration of May’s building permits growth rate, despite the overall tightening of BoC’s monetary policy. On a more fundamental level, we also highlight the positive effect a possible additional rise of oil prices may have on the CAD in the coming week, given that Canada is a major oil-producing country.

General Comment

As a closing comment, we expect the USD to relent some of the initiative to other currencies in the FX market, given that the number of high-impact financial releases is to be reduced. Overall we expect volatility to ease in the FX market given also that part of the market’s attention is to be shifted towards stock-markets as the earnings season comes into full swing. For the coming week we note among many companies, the release of the earnings reports of Morgan Stanley and Lockheed Martin on Tuesday, IBM, Goldman Sachs, Tesla and Netflix on Wednesday, Johnson and Johnson on Thursday and AT&T and American Express on Friday. Furthermore, we would like to also make a comment about the interest rate decision of the Turkish Central Bank due out on Thursday. We remind you that the bank had hiked rates in its last meeting, raising them to 15%, yet failed to reach market expectations. The decision triggered another round of weakening for the TRY which had reached as low as 26 Liras per US Dollar before stabilising around that level. We consider the market as maintaining a wait-and-see position ahead of the release. Should the market’s expectations not be fulfilled with another rate hike, we may see the Lira tumbling lower once again. Last but not least we would also note the rise of gold’s price over the past week, which was also triggered by the slowing of the US CPI rates for June and enhanced by the retreat of US yields. Overall the negative correlation of the USD to gold remains present and we expect gold’s price to rise in the coming week should the USD weaken.

如果您对本文有任何常规疑问或意见,请直接发送电子邮件至我们的研究团队,地址为 research_team@ironfx.com

免责声明:

本信息不被视为投资建议或投资推荐, 而是一种营销传播. IronFX 对本信息中引用或超链接的第三方提供的任何数据或信息概不负责.