WTI appears to be ending the week, near last week’s closing figure, with markets appearing uncertain as to the commodity’s next direction. Oil traders continue to grapple with conflicting fundamentals of tensions in the Red Sea, OPEC’s oil demand expectations and the deteriorating stability in the Middle East which continues to threaten one of the most vital oil arteries in the world. In this report we aim to shed light on the catalysts driving WTI’s price, assess its future outlook and conclude with a technical analysis.

Oil: Overview Report

OPEC’s first report for 2024

OPEC’s monthly report was released yesterday, in which the oil cartel announced its projections for the oil market outlook for 2025. According to their projections, global demand is expected to “grow by a robust 1.8 million bpd”, which implies that demand for oil will remain elevated. Moreover, the group projects that a “shift to more accommodative monetary policies is expected 2H24”, implying that monetary policy may begin to ease in the second half of the year.

As such, the report could potentially be perceived as optimistic for the oil markets and thus could provide support for oil prices from a more macro perspective. Yet, should the cartel’s expectations of easing monetary policy by the second half of 2024 not materialize, we could see downward pressures on oil prices being exerted.

Crude oil inventories and Baker Hughes point to a reduction in demand

On another note, the US crude oil inventories pointed to a decrease in oil demand during the past week, with the API weekly crude oil inventories figure reporting on Wednesday, that crude oil inventories in the US increased by 0.483M barrels, which is much higher than the expected drawdown of -2.400M barrels. As such traders may be interested in the release of the EIA weekly crude oil inventories figure which is due to be released later on today.

Should it validate the API figure of an increase in oil inventories, implying a reduction in demand, we may see oil prices being weighed down and vice versa. On another note, the Baker Hughes oil rig count which was released last Friday, indicated that demand for oil may be declining, as the count dropped back down the 500 figure, by coming in at a total of 499, which could weigh on oil prices in the long term. Therefore, should the Baker Hughes oil rig count, decline further, implying a further reduction in demand, it could weigh on prices. Whereas, should they begin to increase, thus implying increasing demand, prices could find newfound support and potentially move higher.

No end in sight for Red Sea tensions

Despite the USA’s and UK’s attempts to deter the Houthi Rebels in Yemen from continuing their hostilities against shipping vessels, the group does not appear to have heeded the warnings in the form of bombs and airstrikes. According to Bloomberg, three commercial ships this week have been struck by drones fired by Houthi Rebels in the south of Yemen.

As such, the continued tensions and military escalation could further prolong the resumption of trade via the Suez Canal and could continue providing support for oil prices, as the supply chain of oil continues to be shrouded in uncertainty. However, in our opinion, the markets appear to be relatively unfazed by developments in Yemen and as such, any material impact on the oil markets would have to be as a result of a significant military escalation, or the resumption of trade via the Suez Canal.

Pakistan-Iran

As if the world didn’t have enough military conflicts, Pakistan and Iran appear to be ready to go at it with each other. Iran on Monday fired missiles into Pakistan territory, claiming to have been targeting the militant group of Jaish al-Aldi, with Islamabad responding by firing their own missile strikes into Iran. Given, Iran’s status as an oil producer and that the nation’s territorial waters coincide with the remaining trade route of oil from the Middle East into the international markets, a potential disruption of that area as well, could cause irreparable damage.

Therefore, should the two nations continue in their tit-for-tat approach, it could lead to higher oil prices, as the viability of the world’s crucial oil artery is once again placed under a cloud of uncertainty. Yet, for now, the impact appears to be minimal but is something worth looking out for in the coming week.

Oil: Technical Analysis

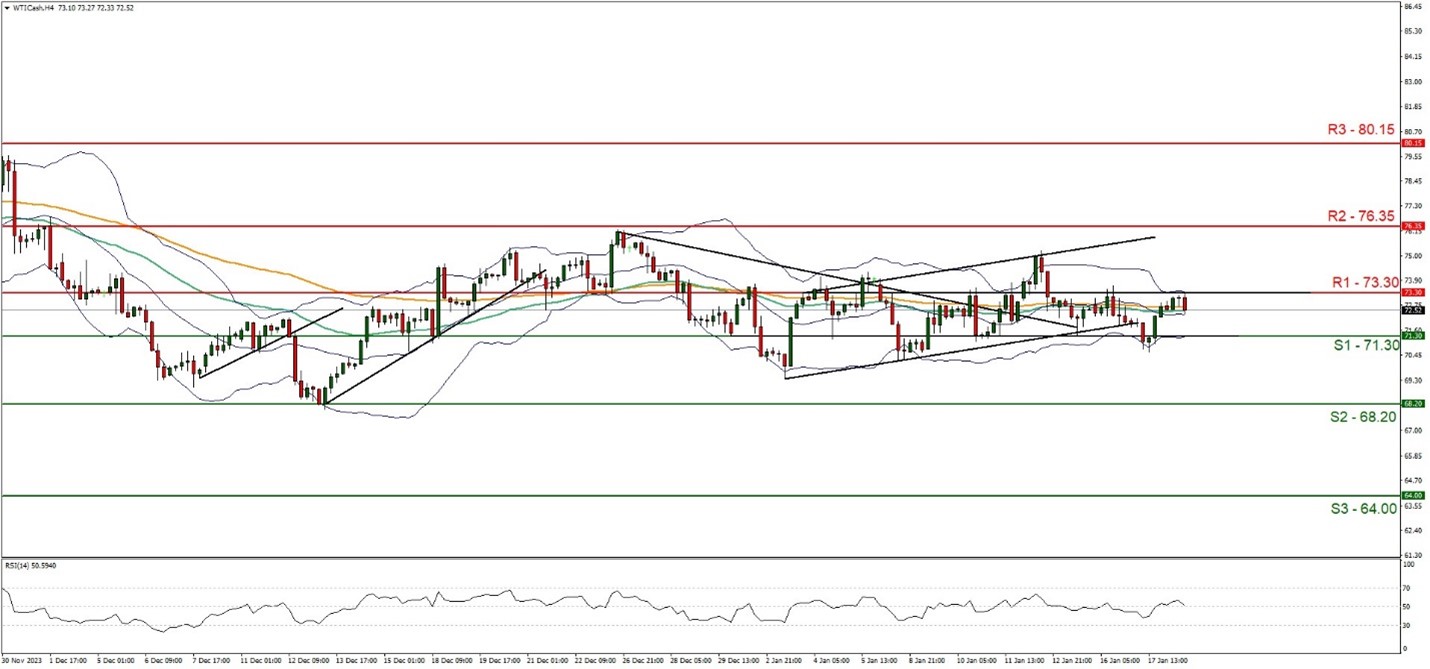

WTI Cash H4

Looking at WTICash 4-hour chart we observe the price action appears to remain relatively unchanged since the beginning of this week. We maintain a neutral bias for the commodity and supporting our case is the RSI indicator below our chart which currently registers a figure of 50, implying a neutral market sentiment. For our sideways bias to be maintained, we would like to see oil remaining confined between the 71.30 (S1) support level and the 73.30 (R1) resistance line.

Yet, we should note that the distance between our S1 and R1 levels, is fairly narrow and as such could easily be broken. Nonetheless, for a bullish outlook, we would like to see a clear break above the 73.30 (R1) resistance line, with the next possible target for the bulls being the 76.35 (R2) resistance level. Lastly, for a bearish outlook, we would like to see a clear break below the 71.30 (S1) support level, with the next potential target for the bears being the 68.20 (S2) support line.

免责声明:

This information is not considered investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced or hyperlinked, in this communication.