This week, crude prices started recovering from their steep fall, suffered in the first couple sessions of 2023 and pared most of their weekly losses, as improved sentiment alongside prospects for a rebound in energy consumption from China’s reopening sustained WTI’s ascend. Paradoxically, grim forecasts by the World Bank for the global economy and unexpected buildups in both EIA and API crude oil inventories appeared to have minimal impact of WTI prices. Regardless, energy traders will be paying attention to the US inflation report later due out later today which is expected to cool and could validate their assessment for an extension of crude prices to the upside. In this report we aim to shed light on the catalysts driving WTI’s price, assess its future outlook and conclude with a technical analysis.

Prospects for a rebound in energy consumption lift WTI

WTI prices found support from revamped hopes for a strong comeback from China, which appears committed at shedding away its strict zero covid policy and return to normalization. The prospects for increased demand for crude has been the major driver behind the recent jump of oil prices, yet analysts caution that the reopening plans may be impeded as surging covid cases pile up across major Chinese cities. More recently, the World Health Organization expressed concerns related to data gathering practices from Chinese authorities regarding infections, deeming them plain “unreliable”. Moreover, oil traders do not seem to be fazed by the recent comments from IMF and the World Bank, which more or less delivered a strikingly similar message. Both organizations forecast that the global economy will face serious hurdles in 2023 as economic activity stemming from the world’s strongest powerhouses, the US , Europe and China, is expected to slowdown considerably. The IMF placed particular emphasis on China’s growth projections and warned that “for the next couple of months, it would be tough for China, and the impact on Chinese growth would be negative” and highlighted that surging infection cases across the country are expected to hurt the economy, impacting growth on the domestic as well as on the international level. Despite the comments, traders’ short-term outlook for crude appears to broadcast bullish undertones for the time being.

Crude oil inventories data record huge buildups

Evidently this week, we observed a deviation from underlying fundamental catalysts of WTI và its prices, as in theory we would have expected oil prices to ease, since data from both API và EIA agencies reported incredulous buildups in their inventories over the past week. More specifically, on Tuesday the weekly API crude oil inventories figure pointed to an oversized buildup of 14.8 million barrels in stocks and similarly, yesterday EIA’s weekly oil inventories recorded an even larger a buildup of almost 19 million barrels of crude for the same period. The results suggest weakening demand for crude which should have translated into weakness for WTI prices. The EIA’s reported figure of 19 million barrels, ranks as the third largest weekly buildup ever recorded. A possible explanation for the unexpected reaction could be that market participants are placing more weight on the prospects for China’s reopening, cancelling out in a way the expected negative reaction from crude stock buildups.

Key US inflation data incoming

Tomorrow, the energy traders will be sitting at the edge of their seats awaiting patiently for the release of the December’s CPI print which is expected to provide an update on the inflationary problem in the US. According to estimates, the December’s year on year CPI rate is expected to decelerate to 6.5% from the last month’s 7.1%. Furthermore, the year-on-year Core CPI rate, which excludes volatile food and energy prices, also for the same month, is set to ease to 5.7% from the 6.0% recorded in the previous month. Should the actual rates meet the expectations, that would imply that inflationary pressures are abiding and may ultimately incentivize the Fed to slow down the pace of its interest rates hikes. The prospect for smaller hikes to come may therefore drive the dollar lower and could as a result boost oil demand, as it makes crude cheaper for buyers holding other currencies.

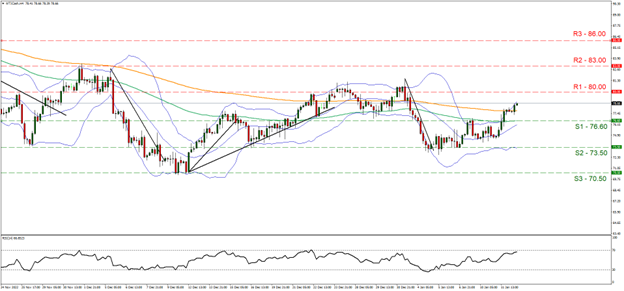

Phân tích kỹ thuật

WTI Cash H4

Looking at WTICash 4-hour chart we observe oil prices finding a floor around the $74 per barrel during last week, which laid the ground for the subsequent rise and break of the previous 76.60 resistance level now turned (S1) support. We hold a bullish outlook bias for crude prices and supporting our case is the RSI indicator below our 4-hour chart which currently registers a value of 67, highlighting the positive sentiment surrounding the commodity. Adding to our case, is the break above the upper bound of the Bollinger band, signaling that the bulls are in control. We have to note nonetheless, that the results of the US CPI print due out later today, can influence the price action significantly. Should the bulls reign, we may see the break above the 80.00 (R1) resistance level and the price action moving higher, closer to the 83.00 (R2) resistance barrier. Should on the other hand the bears take over, we may see the price action fall below the 76.60 (S1) support level and move decisively lower, towards the 73.50 (S2) support base.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced or hyperlinked, in this communication.