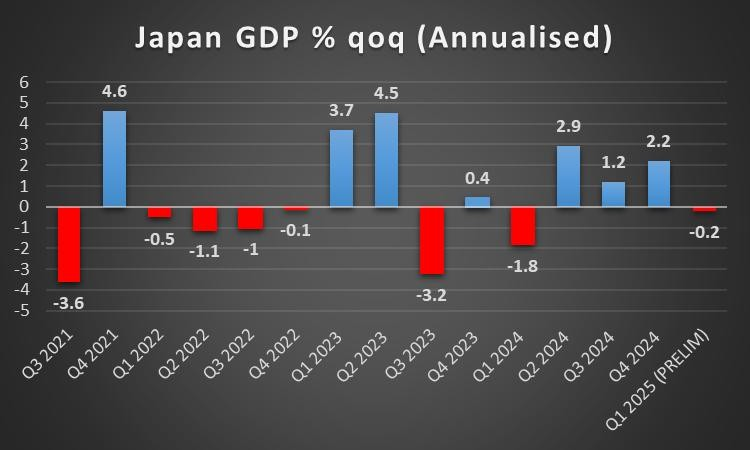

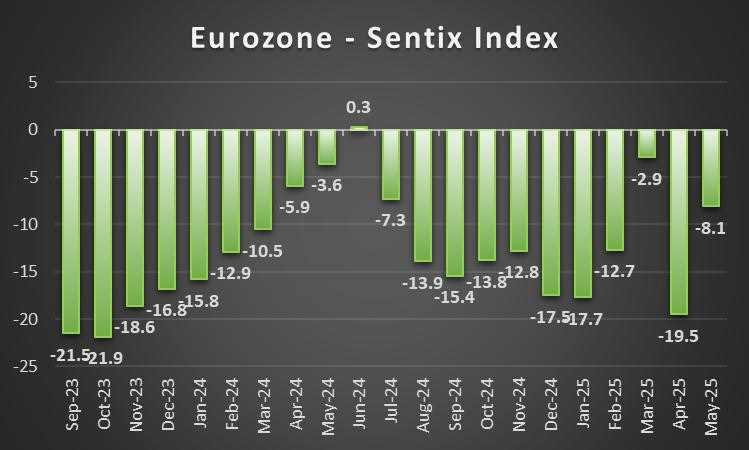

The week is drawing to a close and we open a window at what next week has in store for the markets. On Monday, we make a start with Japan’s revised GDP rates for Q1 , followed by China’s PPI rates for May and CPI rates also for May, followed by the Czech Republic’s unemployment rate for May, the Eurozone’s Sentix index figure for June and China’s trade data for May. On Tuesday, Australia’s consumer sentiment figure for June, the UK’s employment data for April, Sweden’s GDP rate for April, Norway’s CPI for May and the Czech Republic’s final CPI rates for May. On Wednesday we get Japan’s corporate good prices rate for May and the US CPI rates for May as well. On Thursday we note the UK’s GDP rates for April, industrial and manufacturing outputs both for April, followed by the US weekly initial jobless claims figure and the US PPI machine manufacturing rate for May. On Friday we get Japan’s revised industrial output rate for April, followed by Germany’s final HICP rate , Sweden’s CPI rate and France’s final HICP rate all for May, followed by the Zone’s industrial production rate for April and ending off the week is the US’s preliminary UoM consumer sentiment figure for June.

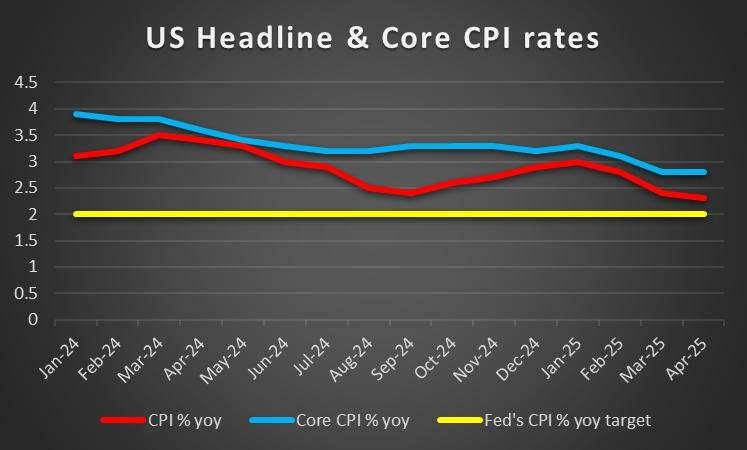

USD – US CPI rates due out next week

On a fundamental level, White House press Secretary Leavitt stated earlier on this week that a phone call between President Trump and Chinese President Xi Jinping has taken place this Thursday, following a lack of progress in trade talks between the two nations. In turn the possibility of progress being made in regards to trade between the US and China may alleviate market worries about the state of the global economy.

On a monetary level, Chicago Fed President Goolsbee’s implied earlier on this week that the uncertainty as a result of the Trump administration’s tariffs may make the banks path forward more difficult, as seen by his comment that “with the uncertainty, I can’t express that with too much confidence because who knows” when talking about the possibility of interest rates moving lower should the economy looks like it did before the Trump administration. In turn this could be perceived as hawkish in nature, should other policymakers showcase their concern which could aid the greenback

On a macroeconomic level we note that the US Employment data for May is set to be released later on today and thus the narrative surrounding the US economy may easily change as the week comes to a close. Therefore, let’s focus on what next week has in store for dollar traders, specifically the US CPI rates for May. Despite the Core PCE rates being the Fed’s favourite tool for measuring inflationary pressures, the CPI rates also play a significant role in gauging inflation in the economy. Therefore, should the CPI rates showcase an acceleration of inflationary pressures in the US economy it may aid the greenback and vice versa.

Analyst’s opinion (USD)

“The CPI rates is something we are eagerly awaiting to see, considering the political and economic situation in the US with Trump imposing a 50% tariff on steel and aluminium which went into effect this week and the constant criticism of Fed Chair Powell the dollar may maintain is control over other currencies. In our view, we wouldn’t be surprised to see an uptick in inflation in the US which in turn could aid the dollar in the upcoming week. ”

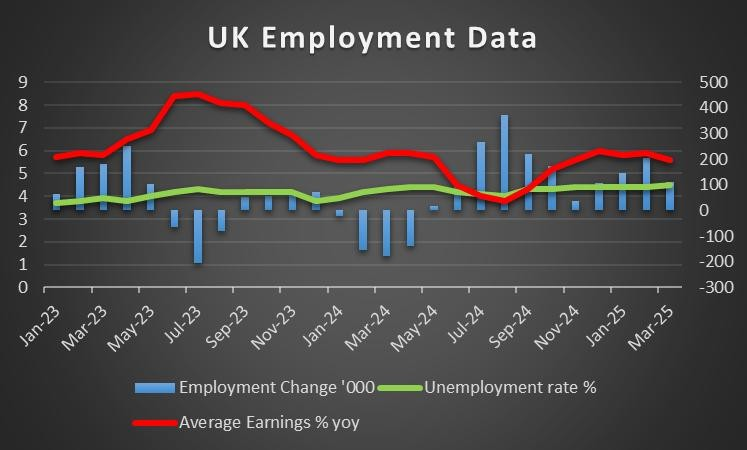

GBP – UK GDP rates and Employment data due out next week

We make a start for pound traders by noting that on a macroeconomic level, the UK’s GDP rates are set to be released next week and may garner attention from pound traders. Moreover, the UK’s employment data is set to be released as well,which could further amplify interest in the pound. Starting with the employment data, should the financial releases and in particular the unemployment rate showcase a loosening labour market it may weigh on the pound. Whereas should the data showcase a resilient labour market, it may aid the sterling. Secondly the release of the UK’s GDP rates for April later on in the week may also garner attention. Should they showcase an expansion of the UK economy it may aid the GBP and vice versa.

On a monetary level, BoE Governor Bailey stated earlier on this week per Reuters that he would be sticking with a “gradual and carefull” approach to cutting interest rates. The Governor’s comments showcase the heightened volatility created in the financial markets and thus his cautious approach may be perceived as hawkish in nature, which could aid the sterling.

On a fundamental level, the UK appears to have been spared from the increased 50% increase in steel and aluminium tariffs. Thus, the apparent friendly terms in regards to trade between the US and the UK, may have aided the UK Equities markets as well as the British pound.

Analyst’s opinion (GBP)

“The UK being sparred from the increased steel and aluminium tariffs is a positive sign for the UK Equities markets. However, we are interest in the unemployment rate for April being release and whether it showcases an increase or a reduction in the unemployment rate.”

JPY – Japan’s GDP rates for Q1 due out next week

On a macro level we note that Japan’s revised GDP rate for Q1 are set to be released on Monday and thus may be of interest for Yen traders. In particular, the prior rate showcased a contraction of economic growth in the Japanese economy and thus should the financial releases on Monday showcase an expansion of economic growth, it may aid the Yen. However, should the revised GDP rates showcase a contraction of economic growth it could instead weigh on the JPY.

On a monetary level , BOJ Governor Ueda’s concern over the ongoing tariff policies, with the Governor stating that “Recent tariff policies will exert downward pressure on Japan’s economy through several different channels”, showcasing a potential hesitancy from the Governor to continue on the bank’s rate hiking path in spite of his comment that “Japan’s economy can withstand such downward pressure”. Thus the Governor’s comments could potentially weigh on the JPY as it may imply that the bank may withhold from raising interest rates in the near future.

Analyst’s opinion (JPY)

“In our view the BOJ appears willing to continue on their rate hiking path, yet the global economic developments appear to be hindering such ambitions. In particular the comments by BOJ Ueda in our view showcase the worries that the trade wars may negatively impact the Japanese economy. Hence we would not be surprised to see a relatively dovish rhetoric emerging from policymakers”

EUR – ECB cuts by 25 basis points as expected

On a monetary level, we note that the ECB has cut interest rates as was widely expected by market participants. The bank cut rates by 25 basis points and in its accompanying statement, noted that “Inflation is currently at around the Governing Council’s 2% medium- term target” and that “trade tensions in April would have a tightening impact on financing conditions have eased” implying that the concern on the impact from trade policies stemming from the US may be easing and could thus facilitate the bank’s monetary easing path. Overall, the comments by the bank could be perceived as dovish in nature and could thus weigh on the EUR.

On a macro level we note the release of the preliminary CPI rates for May which were released this week showcased easing inflationary pressures in the Zone. In turn the lower-than-expected inflation print may have weighed on the common currency. Other than, we had Germany’s manufacturing PMI figure and France’s services PMI figure both for the month of May. Germany’s manufacturing PMI figure came in lower than expected showcasing a continued contraction of the nation’s manufacturing sector, which may have weighed on the EUR. The negative implications however may have been countered slightly by France’s services PMI figure coming in higher than expected. Overall, both financial releases show that Germany’s manufacturing sector and France’s services sector still remain in contraction territory and thus overall may be of some concern for EUR traders.

Analyst’s opinion (EUR)

“We are not surprised from the Zone’s interest rate cut. Yet in contrast to the ECB’s policymakers, we are still concerned over the US’s tariff agenda and how it may shape the global economy. We concur that concerns have eased but it does not necessarily mean that the Eurozone is in the clear”

AUD – RBA still concerned over tariffs

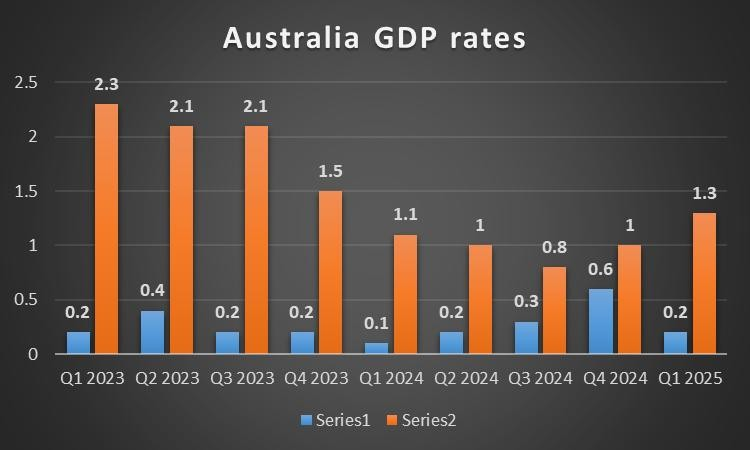

On a macroeconomic level, we note the release of Australia’s GDP rate for Q1 this Wednesday. The nation’s GDP rate both on a qoq and yoy level came in lower than expected at 0.2% and 1.3% respectively. The lower-than-expected GDP showcased that the Australian economy expanded at a slower rate than what was expected by economists. In turn this may be of concern for the Australian economy which in turn may have weighed on the Aussie.

On a monetary level we note that the RBA’s May meeting minutes were released this week as well and tended to provide insight into the banks inner deliberations. In the bank’s minutes it was stated that “at the time of the meeting tariffs were still well above previous levels and future tariff decisions remained highly unpredictable” showcasing the banks concern over Trump’s tariff ambitions and the dynamic nature of the trade talks that have been occurring. In turn this may raise concern for policymakers as to how the global economy may be impacted and thus a more moderate approach of gathering more information may be a more desirable path moving forward.

On a fundamental level, we note the upcoming financial releases from China and in particular their trade data for May which is set to be released on Monday. Should the Chinese exports increase, it may imply that demand for Chinese goods is increasing, which in turn may translate into an increase in demand for Australian raw materials.

Analyst’s opinion (AUD)

“The key issue for AUD traders may be the ongoing talks between President Trump and President Xi Jinping given Australia’s close ties to both nations. Should the trade negotiations showcase signs of improvement, it may be perceived as a positive for the Aussie. In our opinion, China may be willing to work with the US but may require some concessions from the US.

CAD – BoC remains on hold as expected

On a monetary level, the Bank of Canda kept interest rates steady at 2.75% as was widely expected by market participants. In it’s accompanying statement the bank stated that “The trade conflict initiated by the United States remains the biggest headwind facing the Canadian economy” showcasing their continued concerns over the US’s trade ambitions and even noted that “It is still too soon to see the direct effects of retaliatory tariffs in consumer price data”. Overall it appears that the bank is still concerned over the impact of the US’s tariffs on its global trading partners and thus may adopt a wait and see approach which in turn may be perceived as hawkish in nature.

On a macroeconomic level, we note that Canada’s Ivey PMI figure for May was released on Thursday and came in better than expected at 48.9 versus 48.3, showcasing a slight improvement. However the main event of the week which is Canada’s employment data for May has yet to be released at the time of this report and is due out today. Therefore, should the data showcase a resilient labour market it could aid the Loonie and vice versa.

Analyst’s opinion (CAD)

“We are not surprised by the comments made by the Bank of Canada, as we have repeatedly mentioned in this week ahead that the US’s tariff ambitions in spite of them ‘easing’ are still a major source of concern for central banks around the world. In our view the comments made by the BoC showcase their concern and thus we would not be surprised to see the bank remaining on hold in the near future until the proverbial dust settles from the US’s tariff ambitions”

General Comment

As a closing comment we would note our expectations for the influence of the USD in the FX market to maintained given that the release of the US CPI rates in the upcoming week, as well as the ongoing trade narrative between the US and China. As for US stockmarkets all major indexes such as the Dow Jones, NASDAQ and S&P 500 appear to be on track to end in the greens for a second week in a row. As for gold’s price it appears to be moving higher as the week comes to a close and thus will be interesting to monitor in the coming week.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.