As the week draws to a close we open a window at what next week has in store for the markets. On Monday we note the release of the preliminary PMI figures for June of Australia, Japan, France, Germany and the Euro Zone as a whole, the UK and the US. On Tuesday we get Japan’s chain store sales for May, Germany’s Ifo indicators for June, UK’s CBI industrial orders for June and Canada’s CPI rates for May. On Wednesday, we note the release of New Zealand’s trade data for May, Japan’s BoJ is to release the summary of opinions for its last meeting, Australia’s CPI rates for May and from the Czech Republic CNB’s interest rate decision. On Thursday, we get Germany’s GfK consumer Sentiment for July, UK’s CBI distributive trades for June, the US durable goods orders for May, the final US GDP rate for Q1 and the weekly initial jobless claims figure. On Friday, we get from Japan, Tokyo’s CPI rates for June, France’s preliminary HICP rate also for June, the Czech Republic’s revised GDP rate for Q1, Euro Zone’s economic sentiment for June, Canada’s GDP rate for April, the US consumption rate for May, we highlight the release of the US PCE rates for May and finally note the final University of Michigan Consumer Sentiment for June.

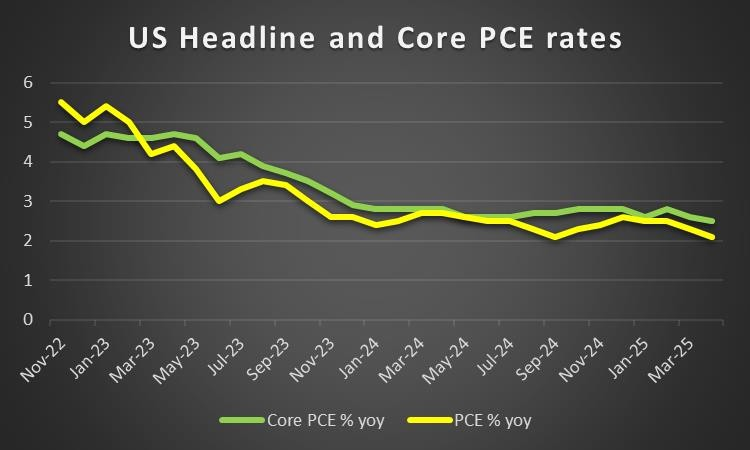

USD – May’s PCE rates in focus

On a monetary level, we note the Fed’s interest rate decision last Wednesday. The Fed remained on hold as was widely expected yesterday. The bank mentioned the solid pace of economic activity expansion, the tightness of the US employment market and that inflation remains somewhat elevated in its accompanying statement. All the comments tend to point towards a delay in any further easing of the bank’s monetary policy yet in the bank’s projections the new dot plot implies Fed policymakers’ expectations for two more rate cuts until the end of the year which seems to be in line with the market’s expectations. Should we see Fed policymakers proceeding in the coming week with hawkish comments contradicting the market’s expectations we may see the USD getting some support.

On a macroeconomic level, we highlight the release of the US PCE rates for May next Friday. Should we see the rates accelerating implying persisting inflationary pressures in the US economy, the release could provide support for the USD as the Fed’s doubts for easing its monetary policy could be enhanced. On the contrary in the case of easing inflationary pressures in the US economy, we may see the USD slipping as it could enhance market expectations for the Fed to expedite its rate cutting path.

On a fundamental level, we see the ongoing political unrest in the US but also on an international level, given US President Trump’s erratic behaviour. Further uncertainty could weigh on the USD and we tend to maintain our worries for a possible involvement of the US in the Israel -Iran war. We also note the substantial resistance to a possible US involvement in the war, even within the Republican party or MAGA supporters, which may be the main reason behind US President Trump’s hesitation.

Analyst’s opinion (USD)

“In the coming week, we highlight the release of the US PCE rates for May and a possible acceleration could provide support for the USD and vice versa. On a monetary level, any hawkish comments by Fed policymakers could also provide some support for the USD.”

GBP – Fundamentals to lead

We make a start by noting on a monetary level that BoE decided to remain on hold at 4.25% yesterday as was widely expected, thus with little effect on the pound’s direction. However the bank also hinted at future rate cuts. BoE Governor Andrew Bailey stated after the release that interest rates are to remain on a gradual downward path yet at the same time stressed the uncertainty on a global level, and highlighted worries for the UK employment market. In the coming week, we have a number of BoE policymakers that are scheduled to make statements, including BoE Governor Bailey on Tuesday and should we see a dovish tone prevailing, implying that more rate cuts are in the pipeline, we may see the statements weighing on the pound.

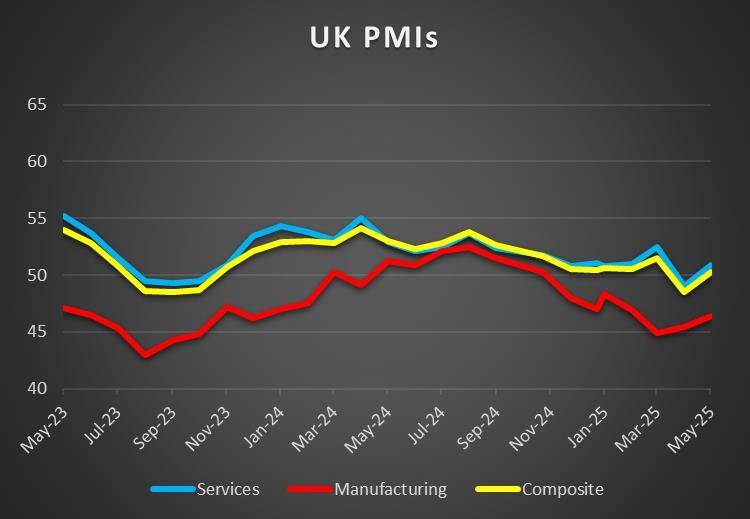

On a macroeconomic level, we note the slowdown of the CPI rates on a headline and core level, yet we still view the CPI rates as being at still relatively high level. In the coming week, we highlight the release of the preliminary PMI figures for June with special focus on the services sector. A rise of the PMI indicator’s reading could imply a faster expansion of economic activity in the critical UK services sector thus supporting the sterling.

On a fundamental level, we note that US President Trump has signed off a deal which lifts some of the US-UK trade barriers. The news were on the positive side, yet in our opinion it still is too little for the UK economy. Also on a fundamental level, we maintain our worries for the possible involvement of the UK in Israel -Iran conflict, especially given the UK air base in Cyprus, which may have a possibly bearish effect on the pound.

Analyst’s opinion (GBP)

“We tend to place more weight on fundamentals for pound traders in the coming week, with special interest on BoE’s intentions, given the few high impact financial releases expected in the coming week. Should possibly a dovish tone emerge from BoE policymakers, it could weigh on the pound ”

JPY – JPY’s safe haven qualities may come in handy

On a monetary level, we note that on Tuesday’s Asian session BoJ remained on hold at 0.5% as was widely expected, yet there is a relative cautiousness on behalf of the bank to proceed with further normalisation of its monetary policy. In its accompanying statement the bank noticed some weakness in the recovery of the Japanese economy, which may be adding pressure on the bank to extend the pause of its rate hiking path. The bank also highlighted the risks in the outlook of the Japanese economy such as the possible impact of the US tariffs on trade. In reflection of the above worries the bank announced a slower tapering of its QE program which could be perceived as dovish. In the coming week, we note the release of the BoJ summary of opinions for the June meeting and should further doubts about a more hawkish path emerge, we may see the JPY retreating.

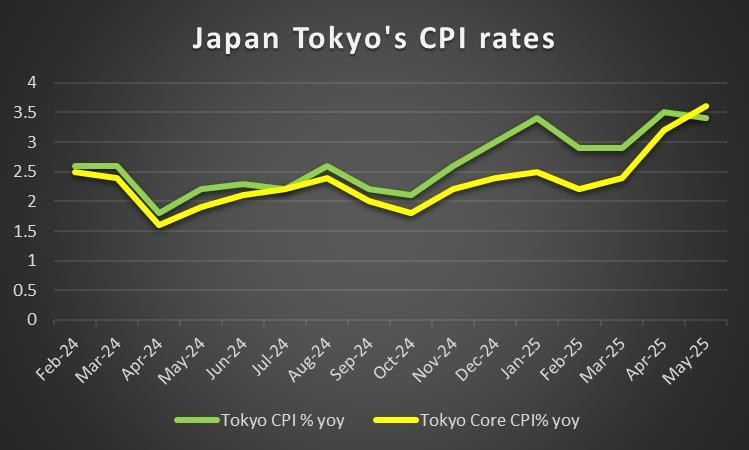

On a macroeconomic level, we note the release of Japan’s CPI rates for May in today’s Asian session, and also note the release of Tokyo’s CPI rates for June next Friday. An acceleration of the rates could act as a preview for the nationwide CPI rates given the density of the megacity’s population. As for economic activity we note the release of the preliminary June PMI figures with special interest on the manufacturing sector. Should the indicator’s reading rise above 50, implying a halt in the contraction of economic activity for the sector and some expansion of economic activity we may see the JPY getting some support.

On a fundamental level we note JPY safe haven qualities in the international markets. Should we see further escalation of geopolitical tensions on an international level, with special interest being on Iran-Israel conflict, we may see the JPY getting some support and vice versa.

Analyst’s opinion (JPY)

“We expect JPY to be primarily moved from BoJ’s intentions in the coming week. Also the Japanese currency’s safe haven qualities may prove to be another factor affecting JPY’s direction. Possible escalation of geopolitical tensions with special focus being on the Iran-Israel conflict could create support for the Japanese currency while a possible easing of market worries the opposite. ”

EUR – June’s preliminary PMI figure to move the EUR

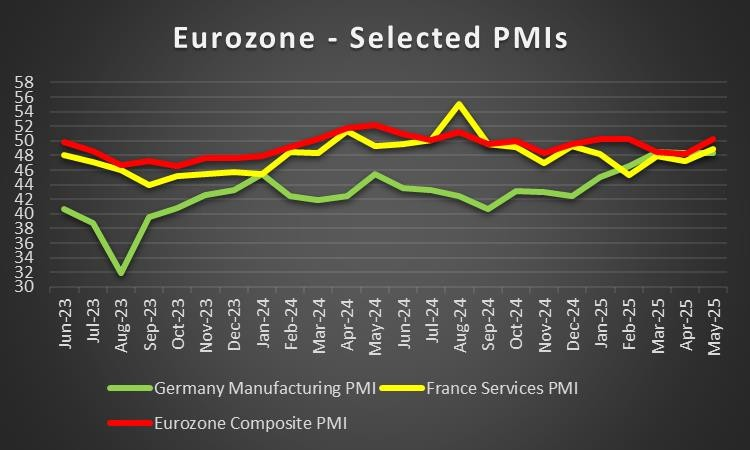

On a macro level we note the verification of the easing of inflationary pressures on a Euro Zone level for May, which may be adding pressure on the ECB to ease its monetary policy further. Also we note the increased optimism for Germany’s economic outlook and improvement of the conditions on the ground of the German economy as described by the ZEW indicators. In the coming week, we highlight the release of June’s preliminary PMI figures with special focus being on Germany’s manufacturing sector. Should we see the indicators’ readings improve further we may see the EUR getting some support, especially should the readings exceed market expectations.

On a monetary level, we note the market’s expectations for the ECB remained relatively unchanged since our last report, with the market expecting one rate cut more to come until the end of the year. The dovish inclination of the bank was underscored by ECB policymaker and France’s central Bank Governor De Galhau statement that the banks next move is more likely to be towards a rate cut than a rate hike. Should we see more ECB policymakers delivering more dovish comments in the coming week, we may see them weighing on the EUR. ECB President Lagarde is scheduled to speak next Thursday, yet we expect no comments on monetary policy.

On a fundamental level we note in the coming week the EU-Canada summit in Brussels. We expect the summit to highlight the close EU-Canadian trade ties especially in the light of the US trade tariffs, which could provide some support for the EUR and the CAD. Also any escalation in the tensions currently characterising the EU-US trade relationships could weigh on the common currency and vice versa. Other fundamental issues that could affect the common currency would be the Israel -Iran conflict, the Russian-Ukrainian war with both conflicts possibly weighing on the EUR should they escalate.

Analyst’s opinion (EUR)

“We note the release of the preliminary PMI figures for June of Germany, France and the Euro Zone as a whole, as a possible market mover for EUR pairs and an improvement of the indicators’ reading could provide some support for the EUR. On the bearish side for the single currency, we note any possible dovish statements by ECB policymakers. ”

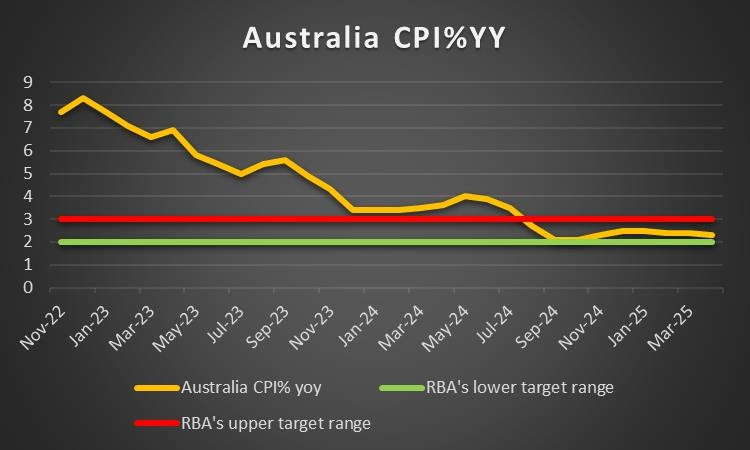

AUD – Australia’s May CPI rates the next big test for the Aussie

On a macro level, we note the release of Australia’s May employment data which came in weaker than expected. On the one hand the unemployment rate remained at 4.1% as expected, yet on the other, the employment change figure took the markets by surprise as it dived into the negatives. The weaker than expected data may have added more pressure on RBA to expedite the easing of the monetary policy. The next big test on a macroeconomic level for the Aussie, is expected to be the release of Australia’s May CPI rates next Wednesday. If rates slow down implying further easing of inflationary pressures we expect the pressure on RBA to cut rates to intensify, thus weighing on the Aussie.

On a monetary level, we note that the market’s expectations for RBA to deliver three more rate cuts until the end of the year, as expressed in the our last report, remain unchanged. Hence the dovish inclination of the market remains, which could be weighing on the Aussie especially if the dovish expectations are enhanced by a possible easing of inflationary pressures or any possible dovish statements by RBA policymakers.

On a fundamental level, we highlight the market’s perception for the Aussie as a riskier asset as any intensification of market worries for geopolitical tensions could turn the market more cautious thus weighing on the AUD. Furthermore we note that the mixed Chinese financial data for May seem to have left Aussie traders unimpressed. Given the close Sino-Australian ties, any signs of a possible slowdown of economic activity in China could weigh on the Aussie.

Analyst’s opinion (AUD)

“In the coming week we expect Aussie traders to focus on the release of the CPI rates for May and a possible slow down could weigh on AUD. Furthermore should the market sentiment turn more cautious given the geopolitical tensions, we may see AUD retreating.”

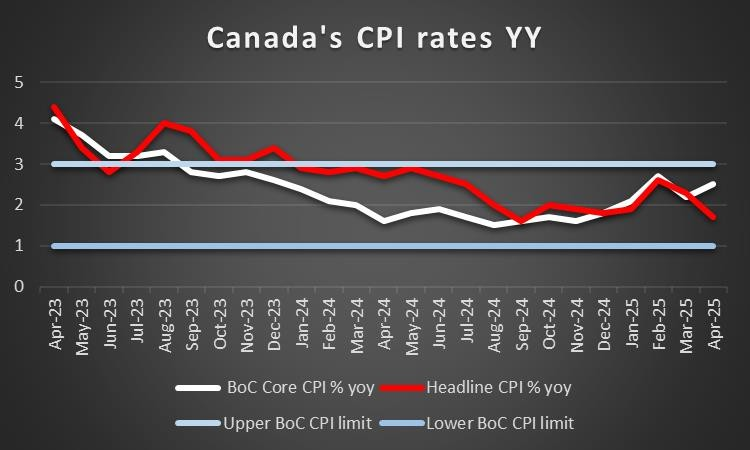

CAD – May’s CPI rates to move the Loonie

On a macroeconomic level, we had a rather easy going week for Loonie traders, yet Canada’s PPI rates for May and retail sales for April are still to be released and could alter the Loonie’s direction. In the coming week, we highlight on a macroeconomic level, the release of Canada’s CPI rates for May on Tuesday. Should the rates slow down implying further easing of inflationary pressures in the Canadian economy, the release may add more pressure on the BoC to restart its rate cutting path, thus weighing on the CAD.

On a monetary level, we note BoC Governor Macklem’s comments that inflationary pressures may be greater than expected, especially at a core level. He also highlighted the uncertainty caused by the tensions in the US-Canadian trade relationships, with any increased costs from US tariffs and/or Canadian counter-tariffs being expected to be passed on to consumer prices. Overall BoC Governor Macklem’s comments tended to tilt towards the hawkish side. Should we see more BoC policymakers expressing such hawkish views the Loonie may get some support as the market may have to ease its current expectations for the bank to deliver a rate cut in the October meeting.

On a fundamental level, we note the rise of oil prices as a possible factor that could provide some support for the Loonie, given Canada’s status as a major oil producer. Especially a possible closure of he Hormuz straits by Iran could be a decisive factorbehind an increase of oil prices. We also note that a possible improvement of the EU-Canadian trade relationships could provide some support for the Loonie ,yet CAD traders have fixated their gaze on the US-Canadian trade relationships. We note that Canada’s PM Mark Carney stated that new tariffs are to be imposed in the coming weeks in order for Canadian industries being protected from unfair trading practices and overcapacity. Should we see tensions in the US-Canadian trade relationships intensify we may see them weighing on the Loonie.

Analyst’s opinion (CAD)

“We expect Loonie traders in the coming week to focus on the release of Canada’s CPI rates for May and a possible slowdown of the rates could weigh on the Loonie. On a monetary level, any hawkish comments by BoC policymakers could support the Loonie, while on a fundamental level, any intensification of the tensions in the US-Canadian trading relationships could weigh on the CAD.”

General Comment

As a closing comment we note that the risk arising from the Israeli-Iranian conflict cannot be understated. The conflict seems to still be at an escalating stage and the scenario of the US and/or other powers getting involved, could weigh substantially on markets. On the other hand, Israel no longer seems to be seeking merely the halting of Iran’s nuclear program, but also a regime change in Iran. On the other hand Iran seems to be prepared to face the Isreali attack. The war tends to evolve to a war of air superiority and ammunition attrition but also attrition on a psychological level within the population of the two countries. In any case we highlight the possibility of further escalation that could weigh on riskier assets while at the same time support safe havens such as gold, while any signs of cooling say for example any willingness by Iran to enter negotiations about its nuclear program may ease market worries somewhat and allow for some support for riskier assets to emerge.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.