The week is nearing its close and we open a window at what next week has in store for the markets. On Monday we get the Eurozone’s final consumer confidence figure for September. On Tuesday, we get Japan’s preliminary industrial output rate for August, China’s NBS manufacturing PMI figure for September, the RBA’s interest rate decision, the UK’s GDP rate for Q2, France’s preliminary HICP rate for September, Switzerland’s KOF indicator for September, the Czech Republic’s revised GDP rate for Q2, Germany’s preliminary HICP rate for September, the US JOLTS Job openings figure for August. On Wednesday we get Australia’s final manufacturing PMI figure for September, Japan’s Tankan figures for Q3, the UK’s nationwide house prices rate for September, Germany’s manufacturing PMI figure for September, the UK’s manufacturing PMI figure for September, the Eurozone’s preliminary HICP rate for September, the US ADP employment data for September, the US ISM manufacturing PMI figure for September. On Thursday, we get Australia’s trade data for August , Switzerland’s CPI rate for September, the US weekly initial jobless claims figure, the US Factory orders rate for August. On Friday, we get Japan’s unemployment rate for September, France’s services PMI figure for September and the Zone’s composite PMI figure for September, the US Employment data for September and ending the week is the US ISM non-manufacturing PMI figure for September.

USD – US Employment data next week

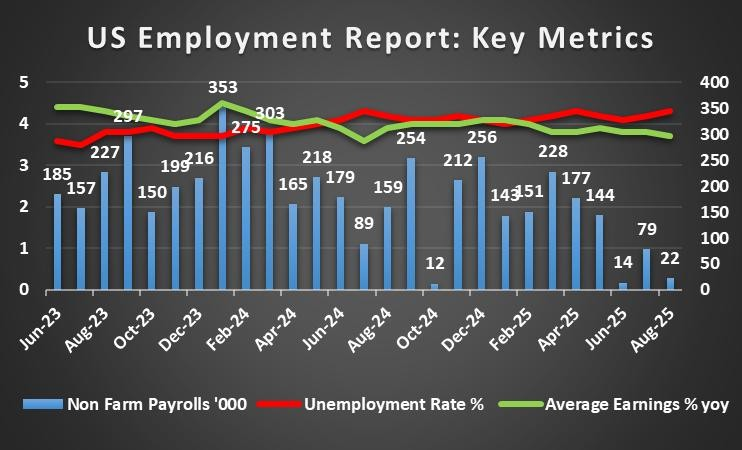

On a fundamental level, we note that President Trump appears to have changed his stance on the Ukraine- Russia war, with him stating on his TruthSocial account that Ukraine could possibly recover all of its territory lost to Russia. In turn, this shift in the President’s view could imply that a peace agreement may be far far away from being materialized. On a macroeconomic level, we would like to point out the release of the US PCE rate which are due to be released later on today. The PCE rate is expected to showcase an acceleration of inflationary pressures in the US economy and could thus provide support for the dollar should such a scenario be materialized. For next week the main event for dollar traders may be the release of the US Employment data for September which are due out next Friday. The current expectations are for the non- farm payrolls figure is expected to improve to 39k from 22k , with the unemployment rate expected to remain steady at 4.3%, it could provide support for the dollar. However, when looking at the bigger picture an NFP figure of 38k is a far cry from the prior readings received earlier on in the year and could still raise worries about the state of the US Employment market. On a monetary level, we would like to note that Fed Chair Powell’s comments earlier on this week tended to dampen the optimism about further rate cuts this year. In particular, Fed Chair Powell had noted that the Fed is in a difficult position in regards to balancing their dual mandate and implied that aggressively easing the interest rate levels prematurely could result in a policy reversal.

Analyst’s opinion (USD)

“This analyst’s opinion last week was that the bank seems concerned about inflation remaining sticky. This view appears to have been validated by Fed Chair Powell’s comments earlier on this week when he discussed his concerns about aggressively easing the bank’s monetary policy. In our view, we wouldn’t be surprised to see another rate cut towards the end of the year purely to aid the Employment market as with the NFP figure expectations next week, the narrative of a loosening labour market does not appear to be going away. However, we would not be surprised to see a weakening of the dollar next Friday post- employment data release unless the NFP figure vastly exceeds the current expectations by economists. ”

GBP – GDP data next week

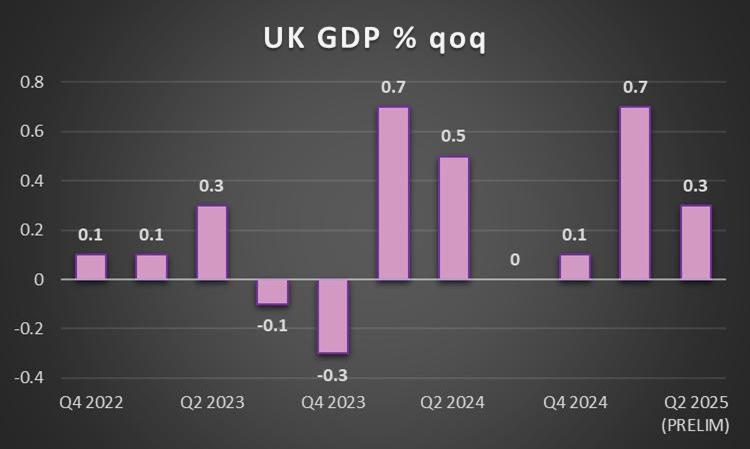

On a fundamental level, we note a recent article that was released yesterday which tended to point that the UK Government may be considering a U-turn on its North Sea stance which could allow for further drilling and exploration to occur. Ironically, increasing oil and natural gas exports could help plug the budget hole that has been plaguing the Labour party since they took over from the Conservatives. On a macroeconomic level, we note that the UK’s preliminary manufacturing and services PMI figures for September tended to disappoint participants. Specifically, the manufacturing sector continued to contract whilst the services sector expanded, albeit at a lower figure than expected. Overall, the financial releases with the exception of the CBI orders figure, tended to disappoint sterling traders and with the economic situation failing to improve, it could weigh on the GBP. For next week pound traders may be interested the nation’s GDP release for Q2 which is expected to showcase signs of a struggling economy and could thus weigh on the pound.On a monetary level, we would like to note the comments by Chief Economist Pill earlier on this week, “It’s always a question of a balance of risks. And you know, I have been on the side of saying maybe the balance of risks are more on the inflationary side than the disinflationary side,” showcasing the bank’s continued concerns over inflation. Therefore, with concerns over inflation remaining high, it may imply that the bank could maintain its restrictive monetary policy approach, which may have provided some support for the sterling.

Analyst’s opinion (GBP)

“The continued policy reversals from the Labour party could lead to internal dissent and could lead to heightened political instability, with challengers potentially emerging to challenge Prime Minister Starmer. Moreover, the worsening of the manufacturing and services sector of the UK economy are worrying and should further financial releases paint a worrying picture for the UK economy it could weigh on the pound”

JPY – Tokyo CPI rates come in lower than expected

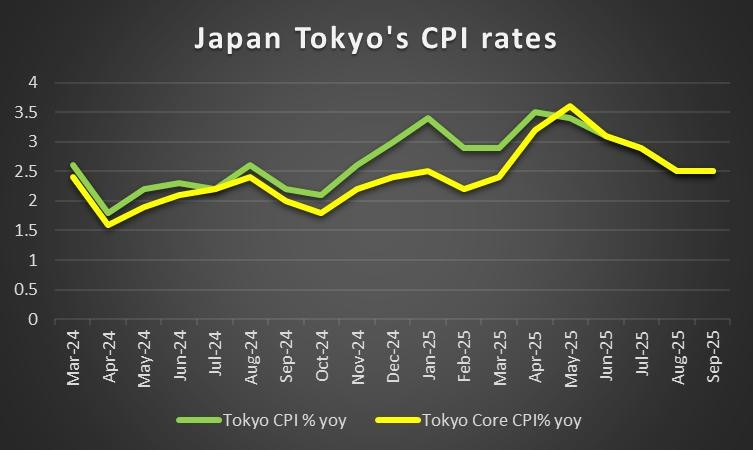

On a macroeconomic level, we would like to note the release of Japan’s preliminary JiBun manufacturing PMI figure for September which came in lower than expected. Specifically the figure came in 48.4 which is lower than the expected figure of 49.5 and thus implied a greater contraction of the manufacturing sector than what was expected by economists. Moreover, of interest was the release of Japan’s Tokyo CPI rates for September which were released earlier on today and failed to showcase the expected acceleration of inflationary pressures in the Japanese economy. In particular, the Core Tokyo CPI rate came in at 2.5% versus 2.8%. Hence both financial releases may have weighed on the JPY, for their own respective reasons. For next week, Yen traders may be looking forward to the release of Japan’s Tankan manufacturing index figures for Q3 which should they showcase an improvement, could in turn increase optimism surrounding the state of the Japanese economy which could provide support for the JPY. On a monetary level, we would like to note the release of BOJ’s July meeting minutes this week, which showcased support for a rate hike from some policymakers. However, considering the minutes were from the July meeting their impact may have been relatively muted. Lastly, the BOJ’s summary of opinions are set to be released net week and could garner some attention from JPY traders.

Analyst’s opinion (JPY)

“The Tokyo CPI rates tend to cast doubt on an immediate rate hike by the BOJ as they failed to showcase the anticipated acceleration of inflationary pressures. In turn we are now slightly concerned for the manufacturing sector of the economy and thus we would not be surprised to see the JPY weakening in the coming week ”

EUR – Inflation data to shake the Zone

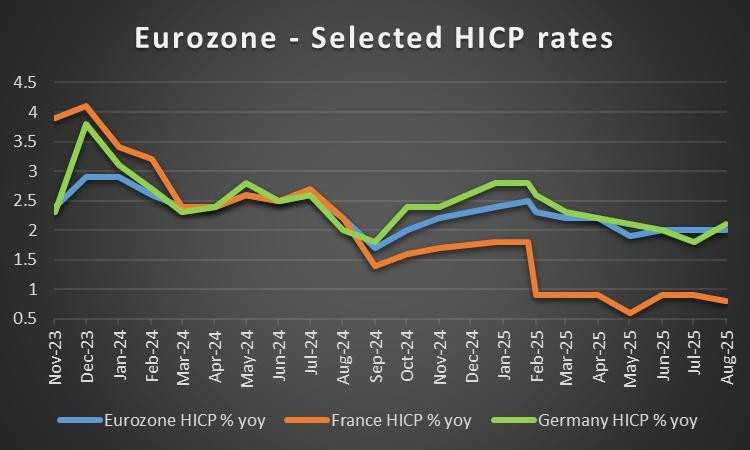

On a fundamental level there is a lot going on for EUR traders. In particular, there are concerns over Russian aggression in the continent and considering that many EU member nations also belong to NATO, fears over a possible escalation between the EU and Russia have risen over the week. On a macroeconomic level we would like to note that there are concerns from our perspective for the two largest economies in the Zone. Specifically, France’s preliminary services PMI figure for September came in lower than expected at 48.9 showcasing a wider contraction of the services industry and for Germany their preliminary manufacturing PMI figure for September which also came in lower than expected at 48.5 thus remaining in contraction territory. The two financial releases tend to paint a concerning picture for the Eurozone and thus could have weighed on the EUR . For next week EUR traders will most certainly be interested in the release of France’s, Germany’s and the Eurozone’s preliminary HICP rates for September which are set to be released. Should the HICP rates showcase an acceleration of inflationary pressures in the Zone it may increase calls for the ECB to prolong their “holding pattern” which in turn could provide support for the EUR. Whereas, should the inflation print showcase easing inflationary pressures in the Zone it may increase calls for a rate cut from the ECB which may then weigh on the common currency. On a monetary policy level, we note the comments made by ECB Stournaras earlier on this week who stated per Bloomberg, “The European Central Bank is probably done lowering borrowing costs, with any further easing needing meaningful changes to the outlook for prices and economic growth” implying that the bank may be done with cutting rates in the near to medium term. Hence, the comments by ECB Stournaras may be perceived as hawkish in nature and may have provided support for the common currency.

Analyst’s opinion (EUR)

“The inflation story of the EU will be dictated next week, but in our view as long as the inflation print remains close to the bank’s 2% inflation target it may not necessarily result in a reaction from ECB policymakers. Hence, we continue to maintain our opinion that the ECB remains in a so called “holding pattern”, yet depending on the HICP releases, we may see a movement in the EUR.

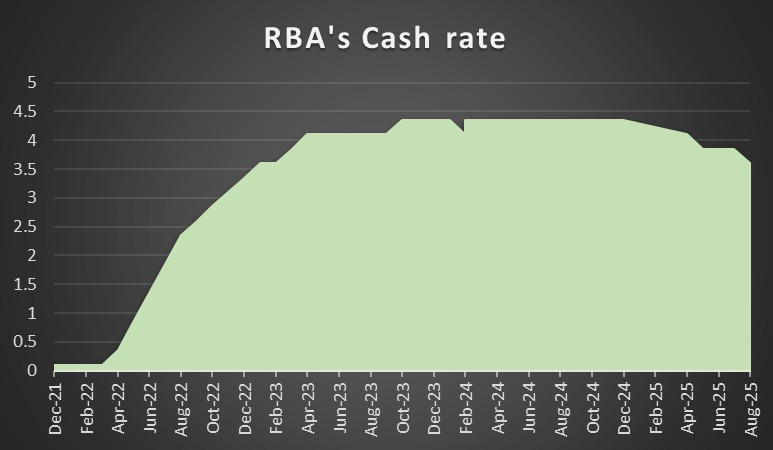

AUD – RBA decision next week

On a fundamental level, Australia has formally recognised the state of Palestine earlier on this week. On a macroeconomic level we would like to note the release of Australia’s CPI rate for the month of August which came in hotter than expected at 3.0% versus 2.9%, implying an acceleration of inflationary pressures in the Australian economy. In turn the hotter- than-expected inflation print may have provided support for the Aussie and may have mitigated the bearish implications on the currency which could have stemmed from the preliminary manufacturing PMI figure for September which came in at 51.6, marking a reduction from the prior month’s figure of 53.0. For next week, Aussie traders may be interested in the release of the nation’s trade data for August, where should the data showcase a trade surplus and an improvement from the prior figure it may aid the Aussie and vice versa. On a monetary policy level, RBA Governor Bullock stated that “Since the August meeting, domestic data have been broadly in line with our expectations or if anything slightly stronger – the Board will discuss this and other developments at our meeting next week” implying that the bank may not be just ready to cut rates again. Hence the comments by the Governor may have been perceived as relatively hawkish in nature and may have aided the Aussie. With that in mind we note that AUD traders may be interested in the RBA’s interest rate decision next week where the majority of market participants are currently anticipating the bank to remain on hold with AUD OIS currently implying 93.78% for such a scenario to occur.

Analyst’s opinion (AUD)

“It is our view that the RBA’s monetary policy stance is at a ‘good’’ place currently and thus we wouldn’t be surprised to see some pushback from policymakers if asked about a possible rate cut in the near future. Moreover, the monthly acceleration of inflation in the economy may dampen hopes that the RBA could cut in their next meeting.”

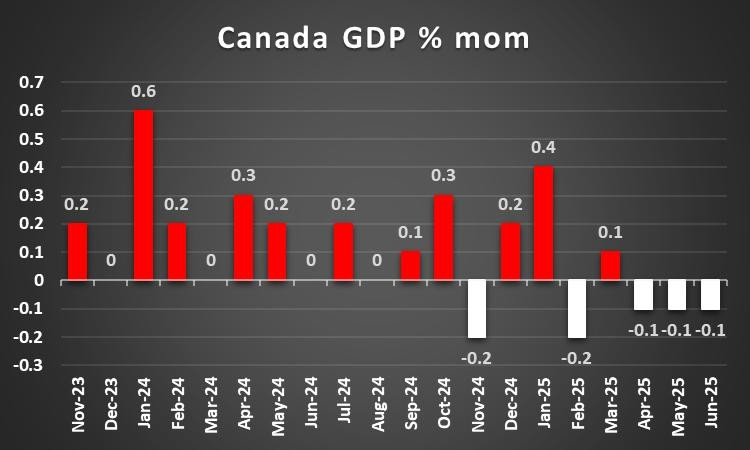

CAD – GDP rates due out today

On a macroeconomic level, we note that Canada’s GDP rate for July which is set to be released today is expected to showcase an improvement i.e economic growth in the economy. Hence, should the aforementioned scenario be materialize it could provide support for the Loonie as the week comes to a close. For next week, it’s set to be a relatively quiet week for Loonie traders with no major financial releases expected from Canada and thus the Loonie’s direction may be dictated by other factors. On a fundamental level, given Canada’s status as an oil-exporting nation, the Loonie may have also benefited as a result of the rise in oil prices this week and may continue to do so should they move higher next week as well. On a monetary level, BoC Governor Macklem, during his speech earlier on this week highlighted the need for Canada to diversify its trade and to essentially reduce its reliance on the US. However, with no clear monetary policy comments having appeared, the comments by the Governor may not have influenced the Loonie.

Analyst’s opinion (CAD)

“The Loonie’s direction may be dictated by other pair’s in the coming week and in particular the dollar considering we have the release of the US Employment data next Friday. From Canada’s perspective, we agree that the nation may need to diversify its trade and to reduce its reliance on the US as a trading partner.”

General Comment

In the coming week we expect the USD to gain more initiative in the FX market considering the upcoming release of the US Employment data. Major US equities markets indexes, such as Dow Jones, S&P 500 and Nasdaq were all in the reds this week. As for gold we note a new all time high was formed. The bullish outlook for the precious metal continues to be tested yet the market sentiment for the time being seems to remain bullish.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.