The week is coming to an end and we open a window at what next week has in store for the markets. On Monday we make a start with the release of China’s trade data for December, albeit the timing of the release is a bit tentative and continue with UK’s manufacturing output for November and the Czech Republic’s CPI rate for December. On Tuesday, we get Japan’s current account balance for November and the US PPI rates for December. On Wednesday we get from Japan the Tankan indexes for January, UK’s and Sweden’s CPI rate for December and in the American session we highlight the release of the US CPI Rates for the same month, while we also note the release of the NY Fed manufacturing index for January and Canada’s manufacturing sales for November. On the monetary front, Sweden’s Riksbank Governor Thedeen speaks and the Fed is scheduled to release its Beige book. On Thursday we get Japan’s corporate goods prices for December, Australia’s employment data for December, UK’s GDP rate for November, Canada’s number of house starts for December and from the US the weekly initial jobless claims figure, January’s Philly Fed Business index and December’s retail sales. On Friday we get from China Decembers’ industrial output and Q4’s GDP rate, UK’s retail sales for December, Eurozone’s final HICP rate for December and the US industrial production for December.

USD – US December CPI rates to shake the markets

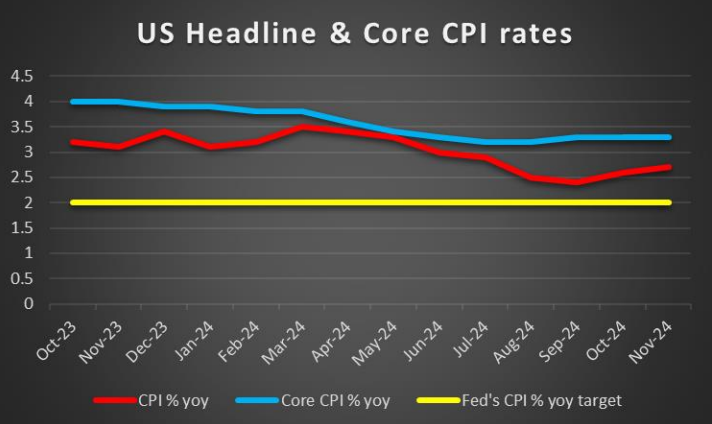

Before we start, we note that the US employment report for the past month has still to be released and could alter the greenback’s direction. We note that the release of the ISM non-manufacturing PMI figure for December, showing a faster expansion of economic activity in the US services sector and thus providing some support for the USD. On a macroeconomic level, we also highlight the release of the US CPI Rates for December on Wednesday and a possible acceleration of the rates could provide some support for the USD. A possible resilience of inflationary pressures in the US economy may enhance the Fed’s hesitation to cut rates. On a monetary level, we note the release of the Fed’s December meeting minutes in which the bank’s worries for the possible inflationary effect from Trump proposed policies such as tariffs on imports from various countries and immigration policies and we see the release as hawkish and supportive for the USD. Finally on a deeper fundamental level, the uncertainty surrounding Trump assuming office, tends also to provide support for the USD in the form of safe haven inflows.

GBP – Elon Musk plots to overthrow the UK Government

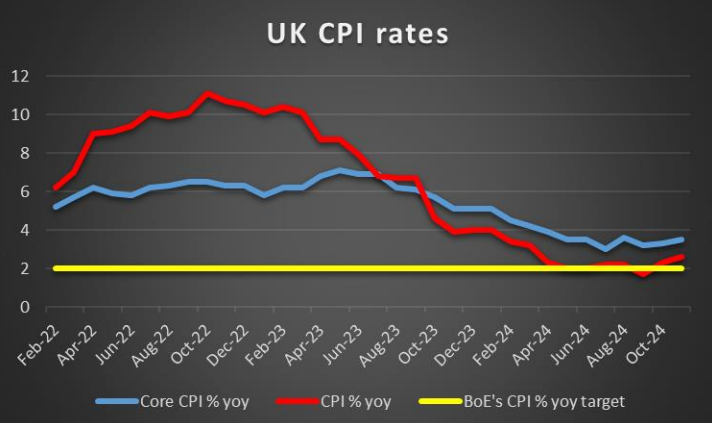

On a fundamental level, the Financial Times article about Musk plotting to overthrow the UK Government before the next General elections made an international sensation. It seems that the Musk is favouring the far right party REFORM to get into power in the UK and overall the political turbulence may weigh on the pound. Furthermore we also highlight the rise off UK Government borrowing costs as gilt yields are on the rise. The rise of Gilt yields may be another indication for the pessimistic opinions in the market about the UK economic outlook. The issue is expected to lead to even less spending in the fiscal policy and could weigh on the sterling. On a monetary level, we highlight the market’s expectations for BoE to proceed with a rate cut in its next meeting and see it as weighing on the pound. The macroeconomic outlook may expedite any loosening of the bank’s monetary policy until Q2 25. Hence we highlight the UK financial releases next week which concern inflation, growth, demand and manufacturing activity in the UK economy. Especially the release of December’s CPI and November’s GDP rates are to be closely watched by pound traders and should they accelerate the pound may get some support as the release may contradict market expectations and could force pound traders to reposition themselves.

JPY – JPY dangerously low

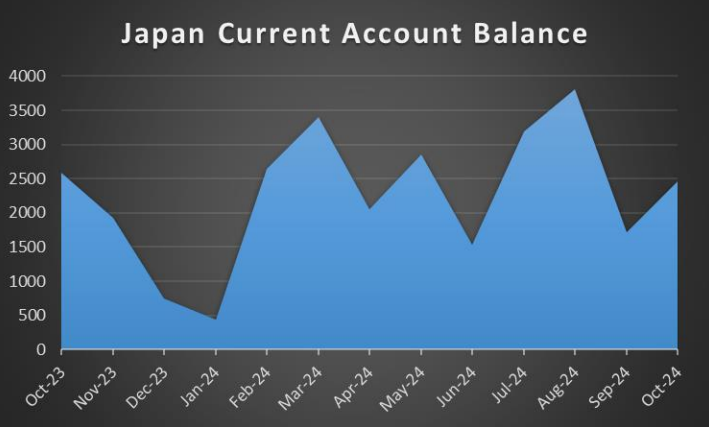

JPY has eased its decline, yet remains at dangerously low levels against the USD. The weakening of the JPY may continue to feed carry trade selling positions for the JPY, thus deepening the negative spiral. Hence we issue a warning for a possible market intervention to the Yen’s rescue by the Bank of Japan, as the Japanese currency has entered the zone at which such interventions took place in the past year. Please note that a market intervention could also take the form of statements by BoJ officials. On a monetary level, the failure of the Bank of Japan to raise its interest rates in an effort to normalise its monetary policy may have enhanced bearish tendencies for the JPY. For the time being the market seems to expect BoJ to remain on hold in the January meeting and proceed with a rate hike in the March meeting. Any statements enhancing the market sentiment for a possible delay of a potential rate hike may provide weigh on JPY. Also please note that on a fundamental level the safe haven qualities of the JPY should not be underestimated, thus should we see uncertainty rising in the international markets, JPY could be getting some support. On a macroeconomic level, in the coming week, we note the release of Japan’s PPI rate of December for inflation, January’s Tankan indexes for economic activity and November’s current account balance.

EUR – Political uncertainty, easing monetary policy and economic outlook all point downwards

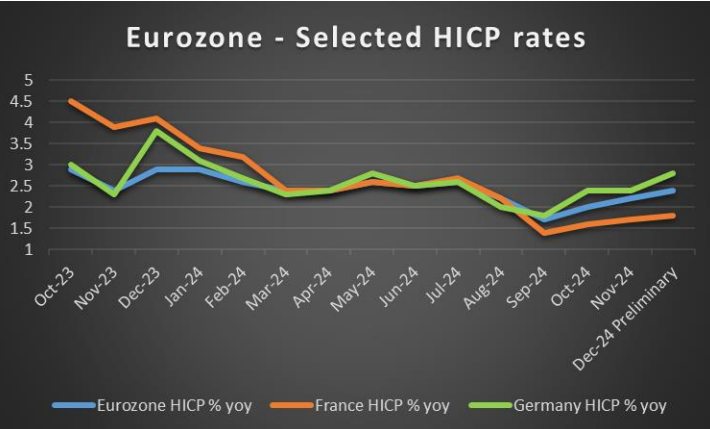

Fundamentally, we note the wide uncertainty on a political level given the weak government in France and the looming elections in Germany. The load for the EUR became even greater as US President elect Donald Trump, expressed his willingness for the US to buy Greenland from Denmark and has not excluded the possibility of a military intervention to that end. France and Germany reacted to Trump’s intentions and the whole issue sends shockwaves in the Euro Zone. Also we note Elon Musk’s intervention in the German elections in favor of the far right AfD, which also created controversy within Germany. Also the intentions of Trump to impose tariffs on EU products exported to the US, tend to weigh on the EUR. On a monetary level, the market’s expectations for the ECB to continue cutting rates at an even faster pace potentially, also tend to weaken the common currency. On a macroeconomic level despite the acceleration of Germany’s industrial output growth rate for November, providing possibly some comfort, the outlook remains rather bleak, with expectations for the Eurozone to suffer a continuous contraction of economic activity, especially in the manufacturing sector which could weaken the EUR. Please note that given the low number of high impact financial releases from the Euro Zone, maybe with the exception of the final HICP rate of the Euro Zone for December, we expect fundamentals to lead the single currency in the coming week.

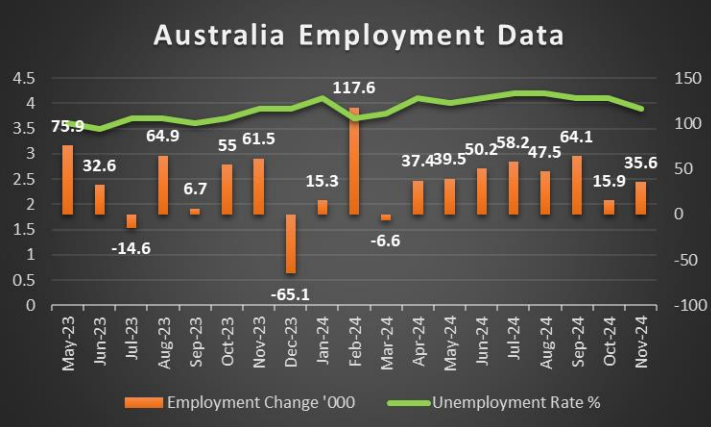

AUD – December’s employment data to rock the Aussie

On a macroeconomic level we note the release of the Australian employment data for November next Thursday. Should the employment data show a tighter Australian employment market, we may see the Aussie getting some support as it may cause the RBA to turn more hawkish. Please note that on Wednesday, we got the November CPI rates which showed an acceleration and may have allready turned RBA more hawkish. On the other hand, on a monetary level, we note the market’s expectations for the bank to cut rates in its next meeting in February, which could be weighing on the Aussie. On a fundamental level, we note the influence of developments in China have on the Aussie, given the close Sino-Australian trading ties. The stalling of inflationary pressures in the Chinese economy was a signal of weak demand. Please note that in the coming week, on Tuesday, we get China’s December trade data and Aussie traders’ focus is expected to be on the imports growth rate. Furthermore, we note the release of China’s industrial output for December and the GDP rate for Q4. Should the GDP rate show an acceleration beyond 5% we may see the Aussie getting some support as it would imply that the Chinese economy has reached its target for growth of 5% by the end of the year and thus support the Aussie.

CAD – PM Trudeau resigned, elections ahead

We make a start for the Loonie by noting that the Canadian employment data for December are still to be released as these lines are written and could alter the mood for the CAD. On a fundamental level, the whispered resignation of Canadian PM Trudeau past week, ahead of the October elections, was realised on Tuesday and dominated Loonie fundamentals. The Liberal Party has now to elect a new leader, yet the New Democratic Party that has supported the Trudeau Government, is expected to withdraw its backing thus leading the country to elections. The conservative party is expected to win, according to opinion polls as it leads currently by a two digit difference. The prospect of a conservative government seemed to support the Looney as the Conservative party is considered as a more business friendly political power in Canada. Also on a fundamentals level, we note that oil prices slightly rose over the past week yet remain for the time being unconvincing for their bullish tendencies and thus remain also unable to provide support for the Loonie. On the flip side on a monetary level market’s expectations for a dovish Bank of Canada, tend to weigh on the CAD. We note the lack of high impact financial releases in the coming week stemming for Canada, thus we expect fundamentals to lead the Canadian Dollar in the days to come.

General Comment

Overall we expect the dominance of the USD over the FX market to continue in the coming week, given the gravity and frequency of US financial releases but also the gravity of US fundamentals with US President-elect Trump and the Fed leading the way. As for US stockmarkets, we expect market interest to increase in the coming week as we start with the earnings season. Major US banks such as JPMorgan (#JPM), Wells Fargo & Co (#WFC), Goldman Sachs (#GS) and Citigroup (#C) are to release their earnings reports on Wednesday and on Thursday we note the earnings releases of Bank of America (#BAC) and Morgan Stanley (#MS). The importance of the releases relies also in that the earnings reports show not only how well each bank performed over the past quarter, but are also a barometer for the US financial sector as a whole and may set the market mood for earnings reports to come. So should we see the earnings reports being better than estimates, we may see the market sentiment getting a lift and major US equities indexes being in the greens. As for gold, we note that its price rises despite the strengthening of the USD and the rise of US bond yields and thus the negative corelation of the USD with gold seems to have been interrupted. Overall we see the case for further advances of the precious metal’s price, yet currently it still remains fragile. Also lets not underestimate the possible ripple effects of the release of the US employment report for December and the US CPI rates for the same month on US stockmarkets and gold’s price.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.