The week is drawing to a close and we open a window at what next week has in store for the markets. On Monday, we not no major financial releases. On Tuesday we get Germany’s Gfk consumer sentiment figure for June, France’s preliminary HICP rate for May, the Eurozone’s Business climate and final consumer confidence figures for May, followed by the UK’s CBI figure for May and the US durable goods orders rate for April and consumer confidence figure for May. On Wednesday we get Australia’s CPI rate for April, New Zealand’s interest rate decision, France’s final GDP rate for Q1. On Thursday we note Australia’s capital expenditure rate for Q1 and the US GDP rate for Q1 and weekly initial jobless claims figure, whilst ending the day is Canada’s current account figure for Q1. On Friday, we note Japan’s Tokyo CPI rates for May, Japan’s preliminary industrial output rate for April, Australia’s retail sales rate for April, Sweden’s final GDP rate for Q1, Switzerland’s KOF indicator figure for May, the Czech Republic’s final GDP rate for Q1, Germany’s preliminary HICP rate for May, the US Core PCE rates for April, Canada’s GDP rate for Q1 and ending the week is the University of Michigan final figure for May.

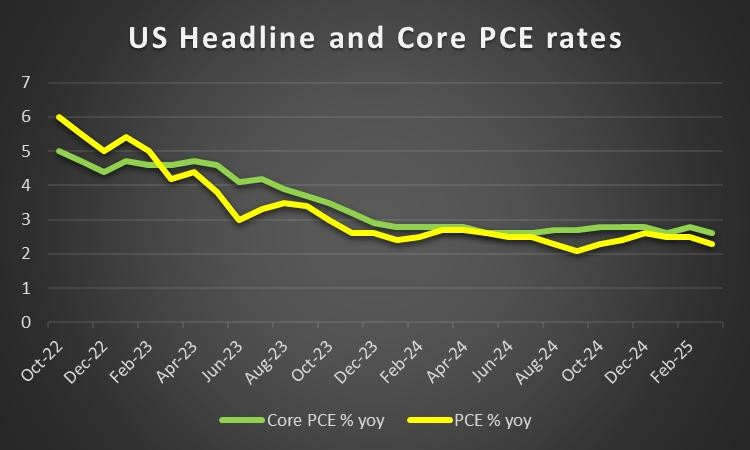

USD – US Core PCE rates due out next week

On a fundamental level the President tax and spending bill has passed the US House of Representatives and is now on its weigh to the Senate where it faces another challenge before being set into law. The administration’s tax and spending bill has raised some concerns over the long term

On a monetary level, Fed Board Governor Wallers comments yesterday could be perceived as dovish in nature, with the Governor stating that “Then we’re in a good position at the Fed to kind of move with rate cuts through the second half of the year” if tariffs are brought down closer to 10%. Thus the Governor is implying that the bank may cut rates in the second half in the year, which in turn could weigh on the greenback

On a macroeconomic level we note that the release of the US Core PCE rates for April which are the Fed’s favourite tool for measuring inflationary pressures in the US economy. Thus should the rates showcase an acceleration of inflationary pressures in the US economy, it could increase pressure on the Fed to remain on hold for a prolonged period of time, which in turn may aid the dollar. On the flip side should the Core PCE rates showcase easing inflationary pressures in the economy it may have the opposite effect and thus could weigh on the USD.

Analyst’s opinion (USD)

“The release of the US PCE rates brings attention back to the dollar in the coming week. Moreover, with trade tensions far from over, the announcements from the US could influence the markets next week. ”

GBP – UK CPI rates come in hotter than expected

We make a start for pound traders by noting that on a macroeconomic level, the UK’s CPI rates for April which were released on Wednesday came in hotter than expected both on a core and on a headline level. The hotter than expected inflation print showcased an acceleration of inflationary pressures in the UK economy, which may increase pressure on the BoE to withhold from cutting interest rates further and thus may have aided the pound.

On a monetary level, the hotter than expected inflation print may have raised some concern amongst BoE policymakers, with BoE Chief Economist Pill stating prior to the release of the UK’s inflation print that the bank may have started cutting rates “slightly to early” last year. Thus, we would not be surprised to see BoE policymakers adopting a slightly more cautionary tone which may be perceived as hawkish in nature and could thus aid the pound.

On a fundamental level, the announcement that the EU and the UK have agreed to a new post Brexit reset trade deal, may be perceived as a positive for EU-UK relations and may pave the way forward for more fruitful trade negotiations with the EU. Thus, the positive developments may aid the UK Equities markets.

Analyst’s opinion (GBP)

“Overall the persistent inflationary pressures in the UK economy may increase pressure on the bank to ease on their dovish monetary policy stance, which in turn could aid the pound”

JPY – Japan’s CPI rates come in hotter than expected

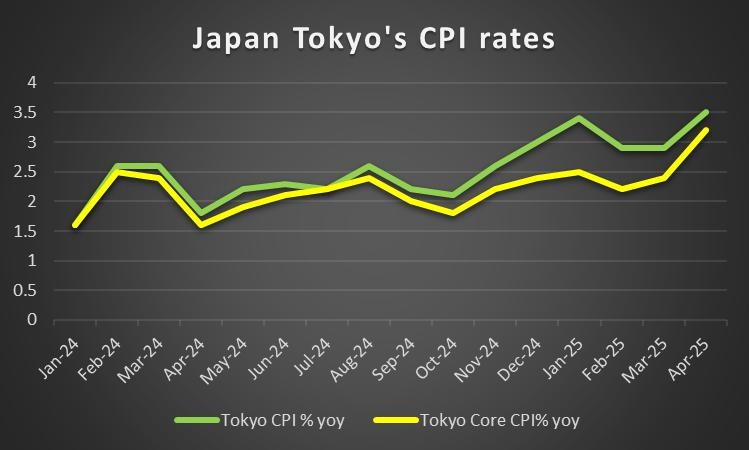

On a macro level we note that Japan’s CPI rates for April were released earlier on today. The nation’s inflation print came in hotter than expected on a core level, at 3.5% versus 3.4%. The hotter than expected inflation print may increase pressure on the bank to resume on its rate hiking path in order to combat the acceleration of inflationary pressures in the economy. In turn this may aid the JPY. For next week, traders may be looking forward to the release of the Tokyo CPI rates for May. Despite the release being for the month of May, it still provides valuable information into the inflation picture in Japan and thus should the Tokyo CPI rates showcase an acceleration of inflationary pressures, it may amplify calls for a BOJ rate hike which may aid the Yen. On the other hand, should the CPI rates showcase easing inflationary pressures it may have the opposite effect which may weigh on the JPY.

On a monetary level , BOJ Governor Ueda has refrained from hinting at action over the recent surge in the Japanese Bond-Yields which reached record highs. Per Bloomberg the Governor stated that “I want to refrain from commenting on specifics on short-term moves in bond yields” but he will “keep watching them closely”. Nonetheless, policymakers may also be looking forward to next week’s Tokyo CPI rates which we previously mentioned

Analyst’s opinion (JPY)

“Inflation remains elevated in the Japanese economy and thus attention turns to the Tokyo CPI rates next Friday”

EUR – ECB June rate cut?

On a monetary level, we highlight the comments made by ECB policymaker Stournaras who stated that he sees a June rate cut and then the bank remaining on pause. The comment by ECB member Stournaras that he sees a June rate cut, is dovish in nature and may weigh on the EUR. However, the implications that the bank may remain on hold in their following meeting and possibly remain on hold for a period of time, may be perceived as hawkish in nature and could overshadow the dovish remarks and could provide support for the EUR as the week comes to a close. Lastly, the announcement today that the US may be imposing a 50% tariff on EU exports to the US, may raise worries for the ECB and may further increase pressure on the bank to adopt a more cautionary monetary policy approach.

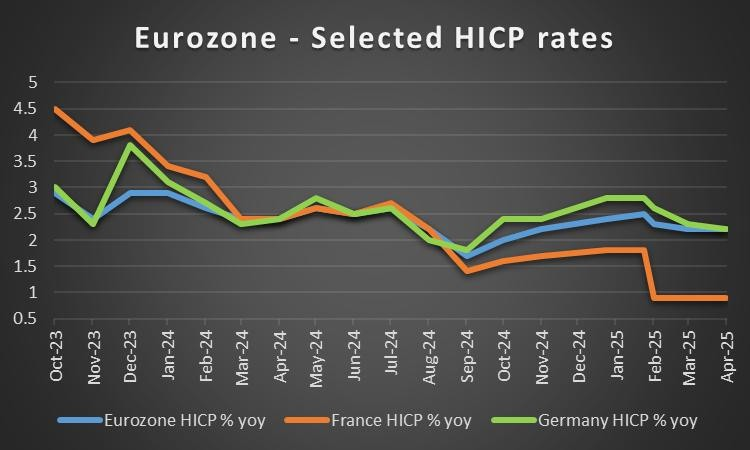

On a macro level we note the release of the preliminary PMI figures for May with a special interest being placed on Germany’s manufacturing sector figure which despite showcasing some improvement from 48.4 to 48.8, it still remains in contraction territory. Moreover, France’s preliminary services PMI figure showcased a wider contraction than what was expected and lastly, the Euro Zone’s Composite PMI figure entered contraction territory implying a reduction of economic activity across sectors in the area and thus all three combined may have weighed on the EUR. Yet the confirmation of the expected acceleration in inflation for the Zone for the month of April and the better-than-expected German GDP rates for Q1, may have masked over the aforementioned PMI figures and taken the stage, which may have overall provided support for the EUR when taking everything into account. Lastly, the release of Germany’s and France’s preliminary HICP rates for May next week are set to be crucial considering the ongoing trade war between the EU and the US as well as the shaky economic outlook for the Zone.

Analyst’s opinion (EUR)

“The announcement that the US may be imposing a 50% tariff on EU exports to the US starting next month, showcases how volatile the trade situation still is. Moreover, in spite of Germany’s better than expected GDP rate which was released today, the PMI figures for France, Germany and the Zone are still a concern especially when we take into account the confirmation of the acceleration of inflationary pressures in the Zone from a yoy perspective on a core level. ”

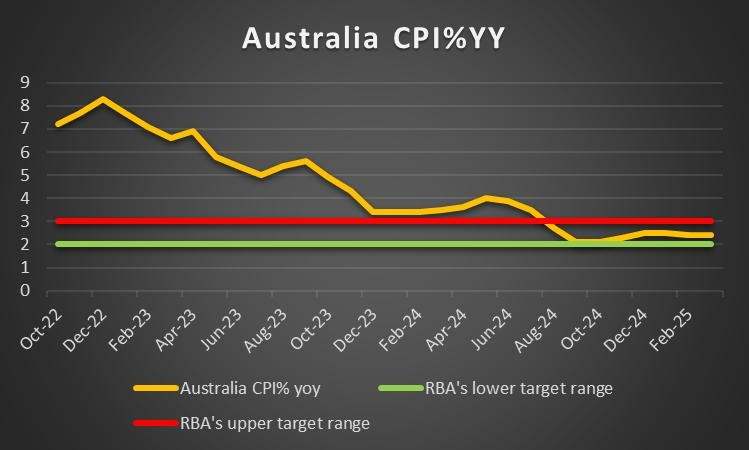

AUD – RBA cuts rates as expected

On a macroeconomic level, we note the release of Australia’s CPI rates for April next Wednesday the 28th of May which may garner attention from Aussie traders. The release of the CPI rates could influence the Aussie’s direction, considering the importance of the inflation print. Should the CPI rates showcase an acceleration of inflationary pressures in Australia, it may aid the Australian dollar and vice versa.

The bank in its accompanying statement noted that “Inflation is in the target band and upside risks appear to have diminished” and seems to be cautiously ready to deliver more rate cuts in the coming months, depending on the developments of inflation and the labour market. The release weighed on the Aussie and any dovish comments by RBA policymakers could renew bearish tendencies for AUD.

On a fundamental level, we note that the improvement of the market sentiment created by the US- Sino trade ongoing trade talks, which may have provided some support for the AUD given their close economic ties with China. Specifically, the high levels talks between the US and China since their Geneva meeting.

Analyst’s opinion (AUD)

“The key issue for AUD may be the release of Australia’s CPI rates for April next Wednesday. Should the CPI rates showcase an acceleration of inflationary pressures in the Australian economy it could aid the Aussie.”

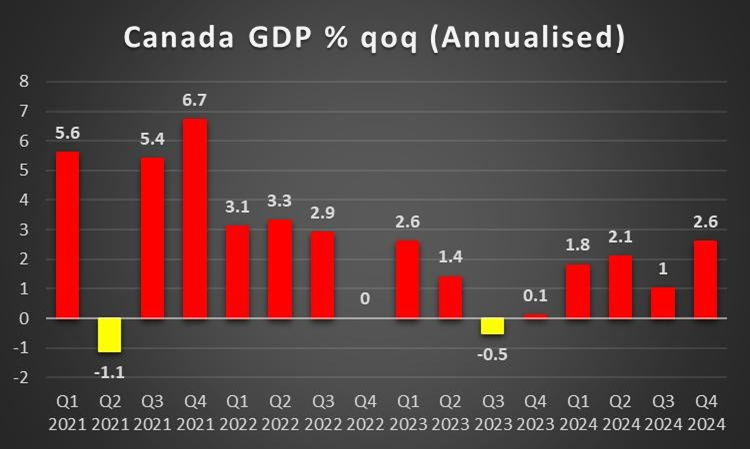

CAD – Canada’s CPI rates come in hotter than expected

On a monetary level, BoC Governor Tiff Macklem stated that “I expect the second quarter will be quite a bit weaker”. It appears that the bank still remains concerned over the implications of the US’s trade policy as it may blurr the nations future economic outlook. In turn the Governor’s comments may be perceived as hawkish in nature, which could aid the Loonie.

On a macroeconomic level, we note that Canada’s CPI rates for April which were released on Tuesday came in hotter than expected on a core and headline level. Specifically the Core CPI rate on a year-on-year basis accelerated to 2.5% versus the prior rate of 2.2% and the headline rate cmae in hotter than expected at 1.7% versus 1.6% yet was still lower than the prior months rate of 2.3% Overall the implications of the Core CPI rate acceleration may have aided the Loonie. For next week, Loonie traders may be interested in the release

Analyst’s opinion (CAD)

“We remain vigilant for the CAD given the release of the nation’s GDP rate for Q1 being released next Friday. Moreover, the Core CPI rates for the nation which were released earlier on this week, may increase pressure on CAD policymakers to adopt a more cautionary tone which may aid the Loonie”

General Comment

As a closing comment we would note our expectations for the influence of the USD in the FX market to increase given that the number of high impact financial releases and monetary policy events stemming from the US is to increase, as well as the ongoing tariff rhetoric. As for US stockmarkets the situation remains volatile. As for gold’s price it appears to be moving higher as the week comes to a close and thus will be interesting to monitor in the coming week

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.