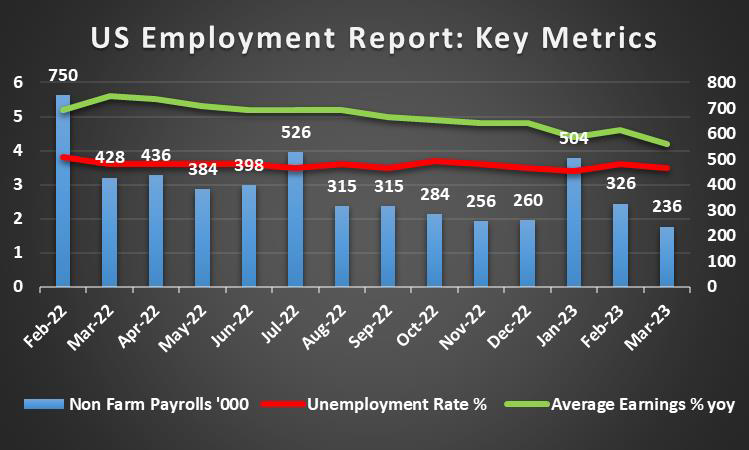

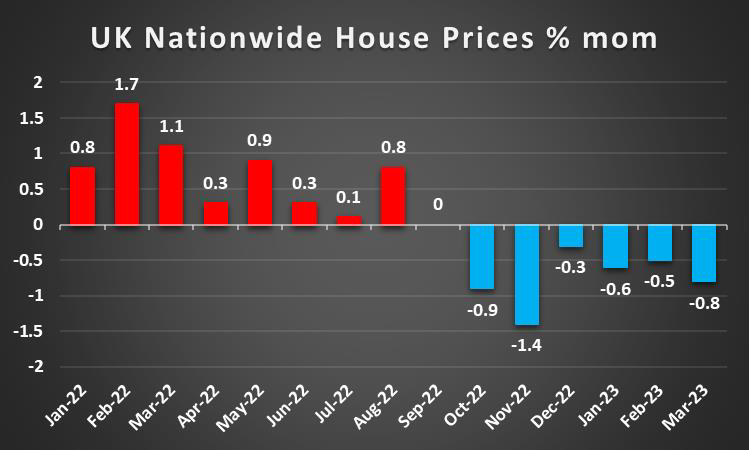

Market worries of a recession have continued into this week and with consumer sentiments further deteriorating, we look at what next week has in store for the markets. On the monetary front, we note a relatively quiet period in regard to monetary policymakers, as the Fed continues its blackout period before its Wednesday meeting. On a more fundamental note, we note the release of the RBA’s interest rate decision on Monday, followed by the Fed’s and the Czech Republic’s interest rate decisions on Wednesday and finally the ECB’s and Norway’s interest rate decisions on Thursday. As for financial releases, we make a start on a quiet Monday with Canada’s Manufacturing PMI and the US ISM Manufacturing PMI figures for April. On Tuesday, during the European session we note the UK’s Nationwide House Price on a MoM basis and the Czech Republic’s Preliminary GDP rate on a YoY basis and the Eurozone’s Preliminary HICP YoY rate all for the month of April and during the American session the release of the US Factory Orders rate for March. On Wednesday, during the European, we make a start with Turkey’s CPI rate for April and in American session, we have the US ISM Non-Manufacturing PMI figure for April. On Thursday, we make a start during the Asian session with New Zealand’s HLFS Unemployment rate for Q1, Australia’s Trade Balance figure for March and China’s Caixin Manufacturing PMI figure for April and in the European session we note the UK Final services PMI figure and during American session, we highlight the US Weekly Initial Jobless Claims and Canada’s Trade Balance for March. Lastly, on an important Friday, we begin during the European session with Switzerland’s CPI rate on a YoY basis and during the American session, we note key release of the US Employment data for April.

USD – US economy in shambles

The USD is about to end the week in the greens against its counterparts despite spending the majority of the week in the reds. On a fundamental note, we note that the U.S House of Representatives passed a bill to increase the debt ceiling with the bill now being sent to the Senate where it is expected to fail. Despite the expectation of the bill failing to pass the Senate, the greenback could find support as the progress being made may alleviate fears of the U.S defaulting on its debt. On a monetary note, we highlight Fed Governor Cook who stated during her speech last Friday, “there is evidence that the path back to our low and stable inflation goal could be long and is likely to be uneven and bumpy”. This may suggest that the Fed still has a long way to go with interest rates, implying higher rates in order to reach the Fed’s 2% inflation target. We highlight the Fed’s interest rate decision on Wednesday and the bank is expected to hike rates by 25 basis points, with Fed Fund Futures implying an 90.2% percent probability for such a scenario to materialize. Should also the accompanying statements reaffirm the bank’s intentions for further tightening and to keep rates at a high level for a prolonged period, we may see the greenback gaining, whereas should the bank seem to have hesitations and imply that the interest rate is nearing its peak, we may see the USD losing ground. On a macroeconomic level, we note the release of the US Preliminary GDP rate for Q1, implying a worse-than-expected slowdown in economic growth for the U.S with the actual figure coming in at 1.1% yoy. The verification of a slowdown in the U.S economy has aided to the weakness of the greenback, as the US economy may be unable to withstand further rate hikes.

GBP – Pound inches closer to 10-month highs

The pound is about to end the week stronger against the Yen, and slightly stronger against the Euro and the dollar. On a fundamental note, we highlight the fact that the UK’s anti-trust regulator blocked Microsoft’s $69 billion deal to acquire Activision, may have negatively impacted the business sentiment in the UK. Following British chip giant Arm, stating last month that they would be pursuing a US-only listing, the blocking of Microsoft’s acquisition has dealt another blow to the UK’s hopes to attract businesses. On a monetary level, we highlight BoE Chief Economist Pill’s comments on Tuesday, where during a US podcast, he stated that “Somehow in the UK, someone needs to accept that they’re worse off and stop trying to maintain their real spending power by bidding up prices”, implying that part of the blame for high inflation stems from workers’ high pay. This statement could be interpreted that the BoE will continue increasing rates in the future, unless unemployment increases or wages decrease, hence providing some form of temporary support for the pound. On a macroeconomic level, we note the release of the UK’s Retail sales rate which contracted even more than expected for March, indicative of a reduction in consumer spending in the UK economy, as the data indicates a negative outlook. This may place additional pressure on the BoE to ease its aggressive rate hike policy, despite high inflationary pressures on the economy thus weakening the pound. On the flip side though, more UK retailers seem to be expecting higher revenue for April. Furthermore, traders may be anticipating the UK’s Nationwide house prices due to be released next Tuesday as an indication of the consumers purchasing power ability for housing, indicating the cumulative effect of BoE’s tightening in the real estate sector as well, with a higher-than-expected figure providing support for the pound and vice versa.

JPY – BoJ keeps monetary policy stance unchanged, yet YCC tweaks may be due

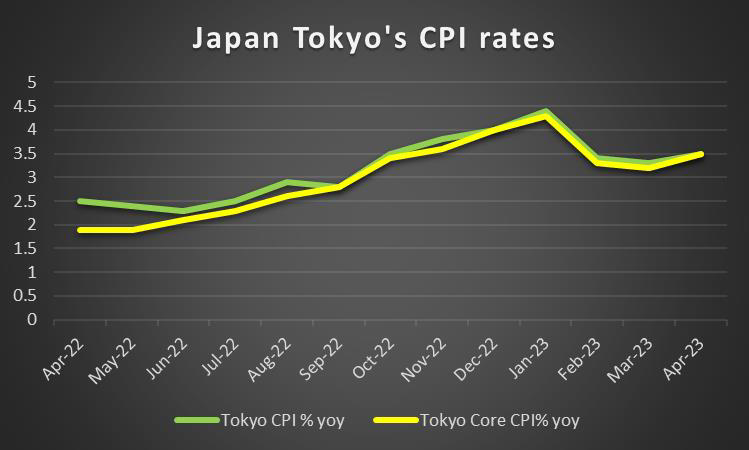

The JPY is about to end the week significantly weaker against its counterparts after the dovish decision by the BoJ. BoJ Governor Ueda following today’s decision to maintain interest rates at current levels, left the Yen once again negatively predisposed for further deterioration, as the interest rate differentials with other central banks continue to widen. In the banks forward guidance statement the following phrase that “short- and long-term policy interest rates to remain at their present or lower levels”, which was included last time the BoJ met under Kuroda, has since been removed, implying that the BoJ may be willing to drop the YCC policy entirely, which was implemented by Mr Ueda’s predecessor Haruhiko Kuroda. The forward guidance is indicative of a shift in the BoJ’s decade-long easing policy, as they enter a new era under the leadership of Governor Ueda. Therefore, by potentially abandoning the ultra-loose monetary policy stance, we may see the JPY gain against its counterparts in anticipation of “tougher” monetary policy. On a macro level, we note the release of Tokyo’s CPI rate, earlier today, exceeded expectations and accelerated to the 3.5% level, the highest in over 40 years placing more pressure on the BoJ to alter its stance in order to protect consumers from excessive purchasing power deterioration. On the contrary the Preliminary Industrial production output and Retail sales rates for March ticked upwards , indicative of a relatively resilient Japanese economy which may provide support for the BoJ to maintain it’s YCC policy for now.

EUR – EUR traders brace for ECB interest rate deciscion impact

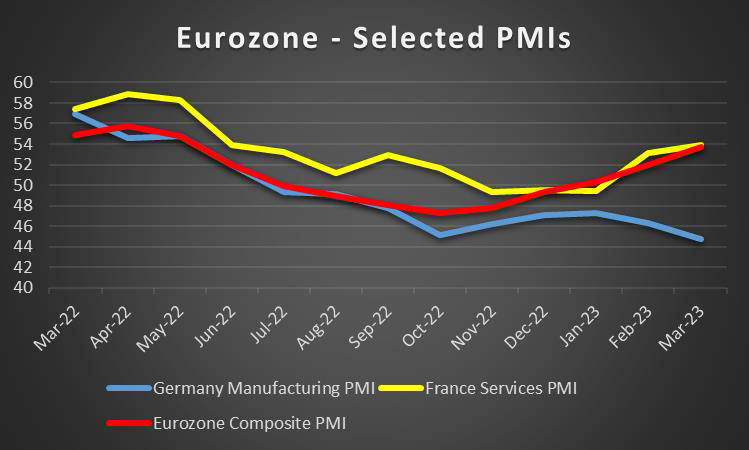

The common currency is on track to end the week flat against the pound and the dollar, however it appears it will end the week stronger against the JPY. Fundamentally, we note Deutsche Bank reporting positive earnings for the 11th quarter in a row and as one of Europe’s largest banks, sends signals of resiliency and boosts confidence in the EU banking sector, thus providing support for the common currency as optimism in EU’s economy improves. On a monetary front, we highlight the statements by ECB’s policymakers De Guindos and Panetta, whose rhetoric appeared to mirror remarks made last week by ECB Chief Economist Lane and ECB policymaker Schnabel. Both comments re-iterated the possibility for further interest rate hikes, as we head into next week’s interest rate decision on Thursday. However, we note that despite the hawkish remarks, the EUR has not significantly gained against its counterparts, as traders prepare for a potential re-evaluation of the ECB’s monetary policy during today’s Eurogroup meetings. Lastly should the ECB’s forward guidance statement contain language that may indicate further interest rate hikes by the ECB, we may see the common currency strengthening, whereas should the statement provide an indication of pausing interest rates or in the extreme scenario cutting interest rates, we may see the EUR weakening. On a macro outlook, we note the Eurozone’s and Germany’s preliminary GDP rates for Q1, which highlight a deterioration in economic activity across the euro area. As the economic sentiment declines, signaling that the eurozone is seeing a deteriorating economic outlook, the euro is expected to face significant hurdles in its short to medium horizon. Furthermore, France’s preliminary HICP rate came in hotter than expected and the market now awaits in anticipation for Germany’s preliminary HICP rate for the same period to either validate or disprove whether inflationary pressures in the eurozone move in unison. EUR traders may find some guidance before next week’s interest rate decision as the Eurozone’s preliminary CPI rate will be released on Tuesday. Should the CPI rate tick upwards, it may imply inflationary pressures persisting in the Eurozone thus providing support for the EUR as the ECB may decide to increase rates in order to curb inflation. However, should the CPI rate tick downwards it could weaken the EUR as it may lead to the ECB re-evaluating its posture before acting.

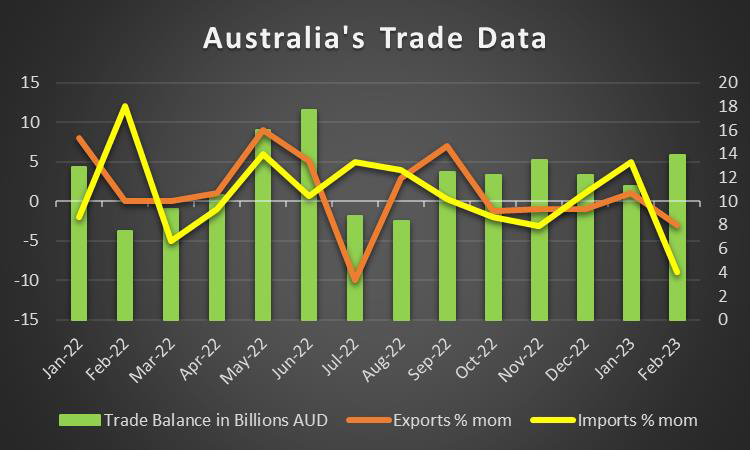

AUD – AUD traders await RBA Interest rate descicion

The Aussie lost significant ground against the USD this week, due to signs of Inflation easing from it’s 33-year highs. On a fundamental note, we give emphasis to the brewing confrontation in the Pacific theatre as the US-Sino relationship deteriorates, potentially impacting the Aussie negatively in the long run. Considering the recent statements by US Treasury Secretary Yellen that China is adopting a confrontational posture against the US, it may fuel tensions between the world’s biggest superpowers, which may negatively affect the AUD due to the heavy reliance by the Australian economy on the demand for its exports by China. On a monetary level, we note the landmark review by the RBA which sets to remove the bank’s ability to dictate cash rate policy and will instead hand the responsibility over to a new independent board of monetary policy experts. Part of the reform includes the removal of the Government’s ability to veto monetary policy, thus truly granting the bank independence. Also, the impact of inflation may no longer have precedence over the employment market in RBA’s considerations. In the long run this may provide support for the Aussie, yet we note that the changes will come into effect in July 2024, with no immediate impact in sight. On a macroeconomic level, we highlight release of the CPI rates for Q1, indicative of continued inflationary pressures in the Australian economy which was also supported during today’s PPI rates for Q1 , coming in higher than expected. Therefore, as we head into next week’s interest rate decision the Aussie may continue facing pressure, as AUD OIS implies an 88.9% probability that the Bank will remain on hold. Should the bank also solidify the markets’ expectations for a pausing of its interest rate hiking path we may see AUD slipping further, as traders await the NBS and Caixin PMI manufacturing figures for April. Given Australia’s heavy dependence on the Chinese economy to import its goods, a resilient Chinese manufacturing complex could provide support for the Aussie as it could translate into increased demand for Australian goods.

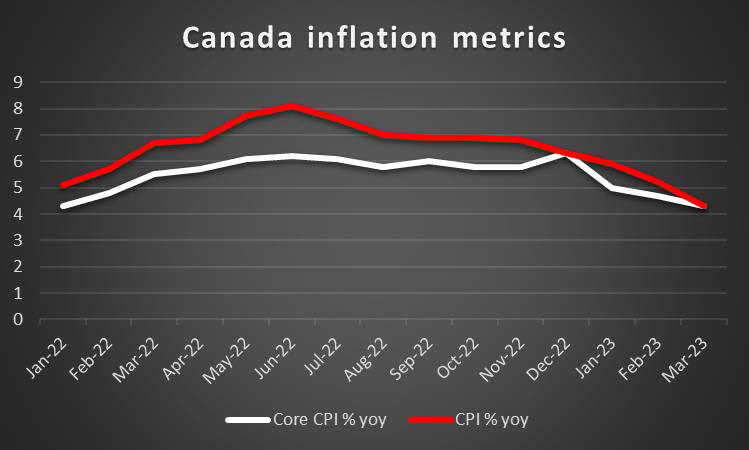

CAD – Loonie may see hikes in the future

The Loonie weakened against the dollar for the week, reverting to levels seen at the start of the month. Fundamentally we note that a third of Canada’s federal workers are still on strike since last Wednesday, as wage negotiations appear to have reached a stalemate. This may further weaken confidence in the Canadian economy, and as a result if the strikes persist, they may further weaken the CAD. On a monetary tone, the BoC deliberations for the April 12th monetary policy decision, were released on Wednesday. The statement highlighted that the Canadian labour market remains tight, in addition to wage growth remaining within the 4% to 5% range, aiding to the persistent inflationary pressures within the economy. Most importantly were the deliberations on whether to hold or hike interest rates, validating our hypothesis that the bank’s decision to maintain current interest rate levels was temporary in order to facilitate further data gathering. On a macroeconomic level, we note the expectations for a higher-than-expected GDP rate today, which if realized could provide support for the CAD as it would showcase an acceleration of the growth of the Canadian economy in February. We expect CAD to also be driven by financial releases next week with the highlights being on Canada’s trade data for March and especially April’s employment data on Friday. Lastly, we note that WTI erased all gains made by the OPEC+ cut at the start of the month, following Russia’s statement that they see no need for further oil output cuts.

General Comment

As a closing comment, following heightened recession fears, the US equities sector the US economy appears to be losing steam as renewed banking fears have undermined a relatively resilient equities earnings season from high-profile companies, highlighting the jittery sentiment amongst traders, amidst the Fed’s interest rate decision backdrop next week. Hence, we continue to highlight that stockmarket traders will have to navigate between the release of earnings reports, the fed’s interest rate decision, the US employment report for April and the market worries for a possible recession in the US economy next week. We note some worries though for companies not meeting the market’s expectations, such as UBS and GSK. When it comes to next weeks earnings we note on Tuesday Pfizer(#PFE), Starbucks(#SBUX) and Ford (#F). On Wednesday we note Airbus (#Airbus), BNP Paribas (#BNP Paribas) and Lloyds Banking Group (#LLOY). Lastly on Thursday, we anticipate Apple (#APPL), Moderna (#Moderna), AIG (#AIG) releases. Finally, we note that the relative stabilisation of the USD has been reflected in the shiny metals price as gold traders appear indecisive about the precious direction. The uncertainty in US yields may have also been reflected on gold’s price as the relative stabilisation in US yields may be a further indication of an undecisive market.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.