As the week draws to a close, we open a window to what next week has in store for the markets. On the monetary front, we note the release of RBA’s interest rate decision on Tuesday and BoC’s interest rate decision on Wednesday. As for financial releases, we note on Monday, the Eurozone’s Sentix figure for December and the US Factory orders rate for October. On Tuesday, we get Japan’s Tokyo CPI rates and the US ISM Non-Manufacturing PMI figure, all for the month of November and the US Jolts job openings figure for October. On Wednesday, we make a start with Australia’s GDP rate for Q3, Germany’s Industrial orders rate for October, the US ADP National employment figure for November and Canada’s trade balance figure for October. On Thursday, we note Australia’s trade balance figure for October, China’s trade balance for November, Germany’s industrial production rate for October, the UK’s Halifax house prices figure for November followed by the Eurozone’s Revised GDP rate for Q3 and ending of the day is the US weekly Initial jobless claims figure. Lastly, on a heavyweight Friday, we note Japan’s revised GDP rate for Q3, and the US employment report for the month of November and finishing of the week is the US University of Michigan Preliminary Sentiment figure for December.

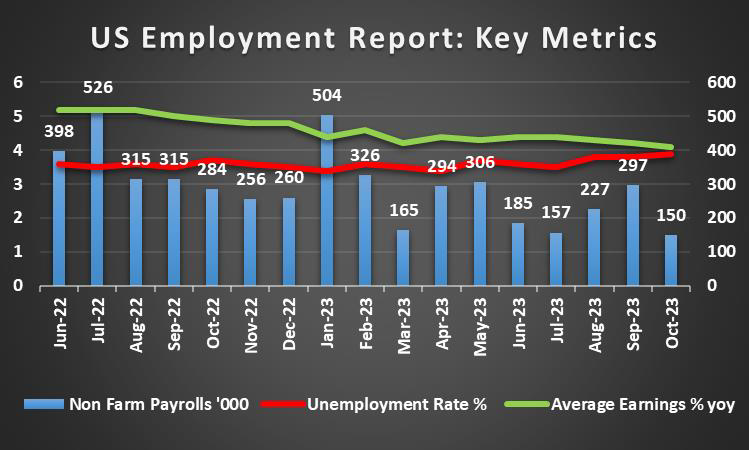

USD – US Employment data next week

The USD tended to remain relatively unchanged against its counterparts for the week. On a monetary level, we note the release of the Fed’s Beige Book. The book states that economic activity has slowed since the previous report, with six districts noting slight declines in activity. The report also indicated when referring to the labour market that “several Districts continued to describe labour markets as tight “, which could lead to persistent inflationary pressures in the US economy. However, Fed Governor Waller stated that he is “increasingly confident that policy is currently well positioned to slow the economy and get inflation back to 2 percent”. The comments made by the Governor could be perceived as predominantly dovish, which could send mixed signals to market participants, as the contradicting views with the Beige book, appear to be cancelling each other out. On a macroeconomic level, we note the acceleration in the 2nd estimate of the US GDP rate for Q3 which came in better than expected at 5.2%. The acceleration of the US’s GDP rate may have provided support for the dollar, yet it appears that the predominant market expectation that the Fed is done raising interest rates, seems to have muted its impact on the greenback. As such, traders may be turning their attention to next week’s financial releases from the US, with the US Employment data for November, the JOLTS Job openings figure for October and the ISM Non-Manufacturing PMI figure for November, which may allow the dollar to take the initiative after seemingly having ceded some control over its direction to other currencies this week.

GBP – Fundamentals to continue leading the way

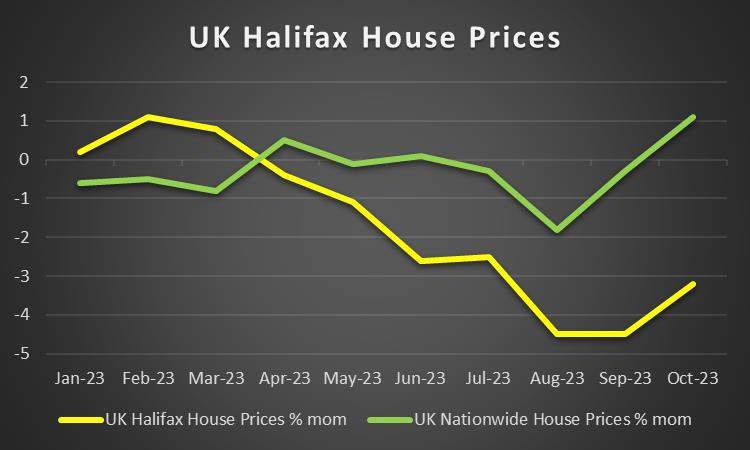

The pound is about to end the week higher against the USD and the EUR yet relatively unchanged against the JPY. On a fundamental level, we note the diplomatic episode between Prime Minister Sunak and Greek Prime Minister Mitsotakis, in which PM Sunak is accused of snubbing the Greek PM by cancelling their meeting at the last minute, following a row over the Parthenon Marbles. The snubbing is not expected to have a financial impact, yet on a political level, it could worsen the Conservative’s polling numbers which are already 20 points behind the Labour party. On a monetary level, we note that BoE Governor Bailey re-iterated his comments made last week for market participants not to expect inflation to fall quickly, as he stated on Wednesday that the bank would do “what it takes” in order to reduce inflation to 2%. Hence, should the Governor’s comments be re-iterated by other central bank officials, we may see some support for the pound. On a macroeconomic level, we note a relatively quiet week from the UK in terms of financial releases, and next week appears to be also relatively quiet for the UK with the exception of the UK’s Halifax house prices figure for November, which is due to be released on Thursday. As such, we expect the pound’s direction to be dictated by fundamentals.

JPY – Tokyo Core CPI rate due out next week

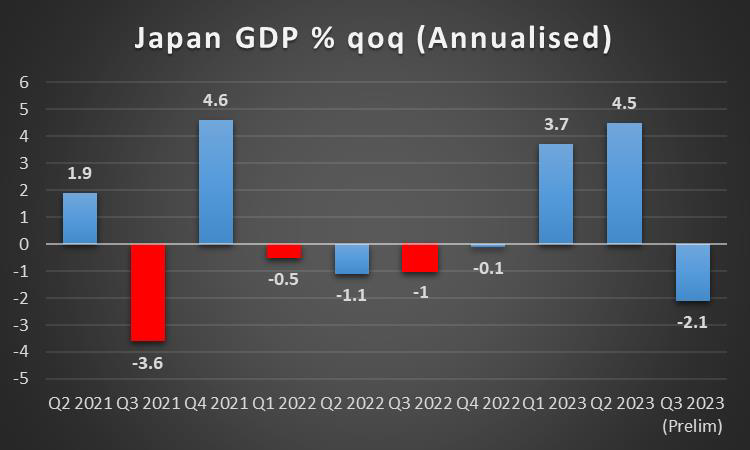

JPY is about to end the week stronger against the USD and the EUR and relatively unchanged against the pound. On a monetary level, we note the comments made by BOJ Board member Nakamura who stated on Thursday “We haven’t reached a stage where we can say with conviction that sustained, stable achievement of 2% inflation accompanied by wage growth is in sight”, implying that the bank’s current monetary policy may not be working yet. As such the board member’s comments could have weighed on JPY as it would imply a continuance of the current ultra-loose monetary policy settings. Furthermore, it should be noted that the board member also stated that the bank “Must patiently maintain current monetary easing for the time being”. Nevertheless, we tend to stick to our comments last week, that we may see the market’s expectations being enhanced for the bank to proceed with its first rate hike which is expected in Spring next year. Moreover, any comments by BoJ policymakers supporting the idea of a policy normalisation may support the JPY in the coming week. On a fundamental level, we continue to highlight the JPY’s dual nature as a safe haven and a national currency, with heightened tensions in the Middle East or even in South America, potentially providing some support for the yen, whilst easing tensions could weaken it. On a macroeconomic level, the deceleration of the BOJ’s Core CPI rates which were released on Tuesday and came in lower than expected, seem to cast some doubt over last week’s acceleration of Japan’s CPI rates for October. The lower than expected, BoJ Core CPI rates, tend to imply that the bank may not normalize its monetary policy for now, which could weigh on the Yen. On the other hand, Yen traders may be looking towards next week’s Tokyo CPI rates for November which are due to be released on Tuesday and Japan’s Revised GDP rate for Q3 on Friday, which could provide some indication in regards to the direction of the Japanese economy. A higher-than-expected CPI rate for Tokyo, in conjunction with a higher-than-expected GDP rate, could provide support for the Yen and vice versa.

EUR – Revised GDP rate for Q3 due out next week

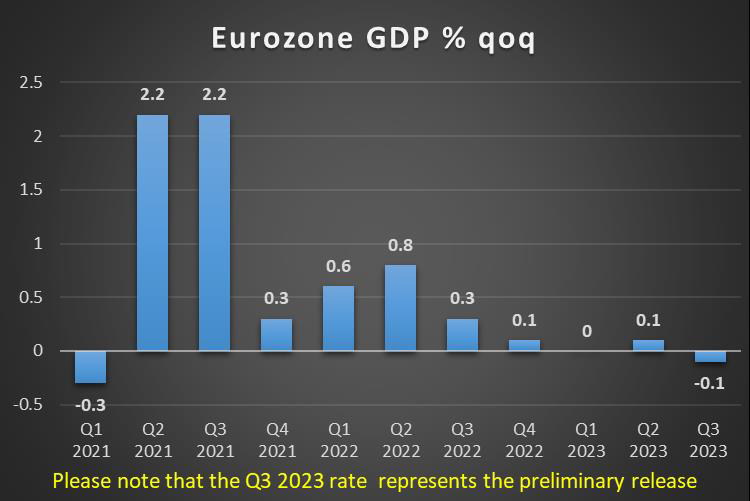

The common currency is about to end the week in the reds against the USD, JPY and GBP, in a sign of general weakness. On a political level, we note the continued rift among Europeans about immigration, which appears to be tantalizing the Eurozone on a political level, as riots in Spain and Ireland continue. For the time being, we continue to expect no major market reaction on the issue. On a monetary level, we note the comments made by ECB President Lagarde on Monday, that “we expect the weakening of inflationary pressures to continue, even though headline inflation may rise again slightly in the coming months”, implying that overall, inflationary pressures in the Eurozone appear to be easing, and as such further rate hikes by the ECB may not be warranted, which could weigh on the EUR. However, she did also state that the medium-term outlook for inflation remains surrounded by considerable uncertainty, which could be interpreted, as a nod that the bank may have not reached its terminal rate, which could support the EUR, should other policymakers further re-iterate her comments. On a macroeconomic level France’s, Germany’s and the Eurozone as a whole released their Preliminary HICP rates, which all came in lower than expected. In addition, the final GDP rates for France came in lower than expected, implying weaker economic activity, which may have aided to the common currency’s descent during the week. The apparent of easing inflationary pressures, in addition to lower economic activity in one of the largest economies in Europe, appear to be fuelling market expectations that the ECB may start cutting rates earlier than expected thus adding additional bearish pressure on EUR. In the coming week, we note the Eurozone’s revised GDP rate for Q3, which we anticipate coming in as expected if not lower, based on this week’s financial releases. In such a scenario, we may see the EUR weakening further.

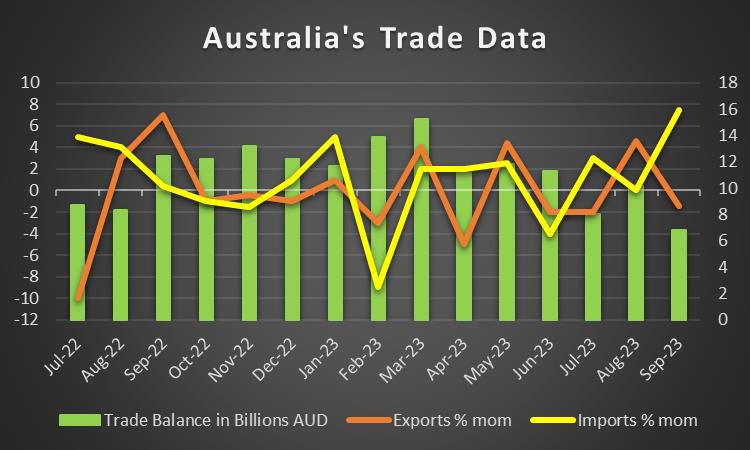

AUD – RBA interest rate decision in sight

AUD is about to end the week slightly higher against the USD for the third week in a row. On a monetary level, we note that RBA’s interest decision is due out next week with AUD OIS currently implying a 95.78% probability for the bank to remain on hold at 4.35%. In the event that the bank remains on hold, we may see the Aussie weakening, should the bank’s accompanying statement indicate that the bank is done with hiking. On the other hand, should the accompanying statement indicate that the bank may have hawkish intentions, we may see the Aussie gaining, yet we do not anticipate such an event to occur for the time being. On a macroeconomic level, we note that Australia’s preliminary retail sales rate for October, came in lower than expected, which could further dampen expectations of a hawkish pause by the RBA and as such, traders may be also interested in the GDP rate for Q3 which is due to be released on Wednesday and the country’s trade balance figure for October which is due to be released on Thursday. We should also note the release of China’s NBS and Caixin Manufacturing PMI figures for November, which sent mixed signals maintaining our worries for China’s manufacturing industry. The continued troubles for China’s economic recovery could weigh further on the Aussie given the close economic ties between the two nations. As such, traders may be also interested in China’s November trade data and specifically the import growth rate.

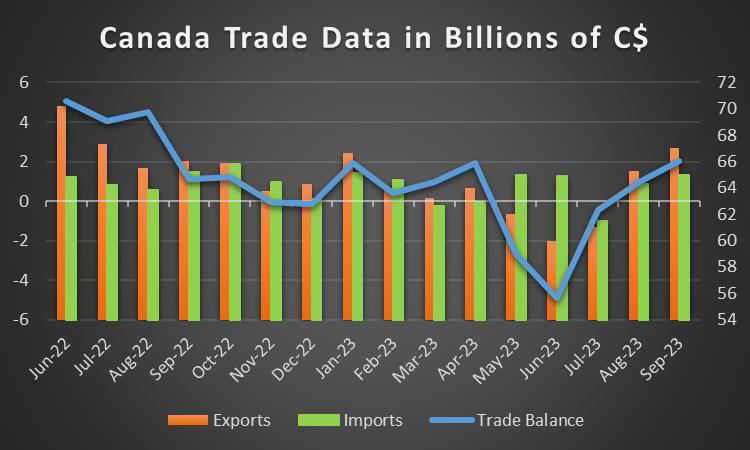

CAD – BoC interest rate decision due next week

The Loonie is about to end for a third week in a stronger against the USD. On a monetary level, we note that the BoC is due to announce its interest rate decision next Wednesday, with CAD OIS currently implying a 85.32% probability for the bank to remain on hold. In the event that the bank remains on hold which appears to be the predominant market expectation, we may see the Loonie weakening against its counterparts, should central bank officials imply that rate cuts may be just around the corner, as the market is anticipating a rate cut in March 2024. Any indication that this may occur earlier, could weigh on the Loonie, yet we should note that in the event of a hawkish pause, we may see the Loonie gaining, as it may imply that the market’s expectations will be contradicted. On a fundamental level, the rising oil prices over the past week appears to be aiding the Loonie, given the nation’s status as an oil producer, thus higher oil prices may be attributed to the Loonie’s strengthening. In terms of financial releases this week, we note that Canada’s GDP rates came in lower than expected and characteristically the yoy rate contracted by -1.1%. The release did not seem to have a material impact on the CAD as it continued strengthening against the USD. We should note that Canada’s employment data has not been released at the time of this report, and should the data indicate that the employment market remains tight we may see the CAD getting some support. Lastly, in terms of financial releases for next week, we note Canada’s trade balance figure for October and their Ivey PMI figure for November which are both expected to be released on Wednesday.

General Comment

In the coming week, we expect the FX market to increase in volatility given the high number of high-impact financial releases stemming from the US. We highlight especially the release of the US Employment data as the predominant financial release for the week, which could greatly impact the major pairs. As for US equities markets, we note that the earnings release season appears to have ended for the major companies, with the S&P500 and NASDAQ 100 remaining relatively unchanged since the start of the week and with only the DOW JONES 30, making gains as the week nears its end. Overall we expect the US equities markets to continue being driven by fundamentals and may focus also on the Fed’s intentions yet the US employment report for November may have ripple effects on the US equities markets. As for gold, we note that the precious metal jumped almost to the 2050 key psychological figure, yet may be due a market correction to lower ground next week, as the bullish momentum appears to be waning. The drop of US yields over the week may have also provided some support to the shiny metal and should they continue in their current direction, we may see a transfer of flows from the interest-bearing US bonds towards the precious metal.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.