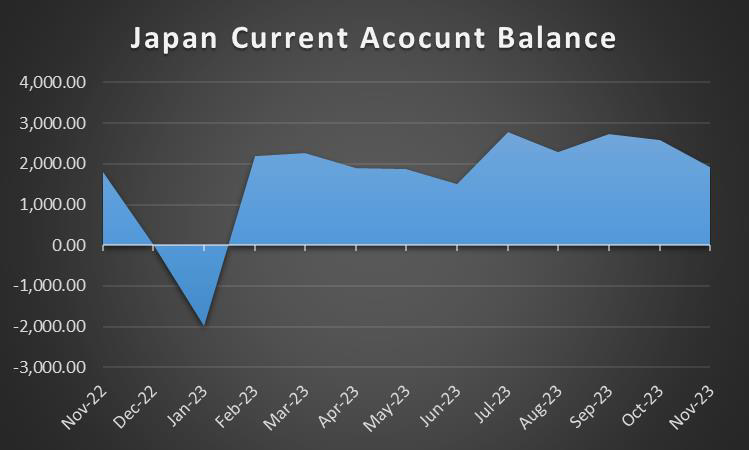

The week is slowly drawing to a close, yet the US employment report for January is still to be released and could alter the current picture of the markets. Yet for the coming week, on the monetary front, we note RBA’s interest rate decision, during Tuesday’s Asian session, while we also note from the Czech Republic, CNB’s interest rate decision, and a number of policymakers from various central banks, which are scheduled to speak during the week. As for financial releases, we note on Monday the release of Turkey’s CPI rates for January, Eurozone’s final Composite PMI figure for the same month and Eurozone’s Sentix index for February and from the US the ISM non-manufacturing PMI figure for January. On Tuesday we get Germany’s industrial orders for December, UK’s Construction PMI figure for January and New Zealand’s Q4 employment data while on Wednesday we start with Germany’s industrial output for December, Halifax House Prices for January and Canada’s trade data for December. On Thursday we get Japan’s current account balance for December, China’s inflation metrics for January and from the US the weekly initial jobless claims figure while on Friday we note the release of Norway’s CPI rates and Canada’s employment data, both being for January.

USD – USD loses ground

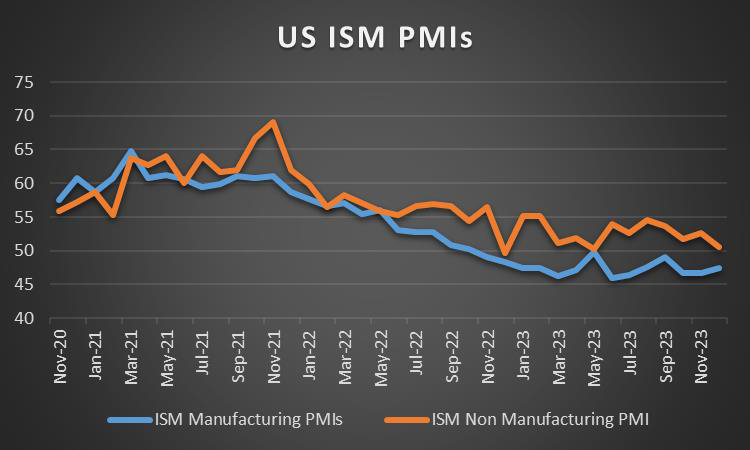

The USD is about to end the week in the reds against its counterparts, yet the US employment report is still to be released and may change that picture just before the week’s end. On the monetary front, we note that the Fed remained on hold as was widely expected, failing to excite the markets either way. In its accompanying statement, the bank seems to be taking its time regarding the possibility of any rate cuts. Fed Chairman Powell in his press conference stated that March is not a base scenario for rate cuts. Please note that the market had already shifted before the release, expecting the first rate cut in May. We tend to be even less dovish and suspect that the bank may start cutting rates in the summer, a scenario that if materialized could keep USD supported on a monetary level. On a fundamental level, the unofficial pre-election period is ongoing, with Trump having the advantage, at least in the Republican party. In the international political arena, the drone attack on a US base in the Middle East, by an Iranian-backed organisation, leaving three dead and more wounded, seems to be changing the game. President Biden was pressured to respond and such a response could escalate tensions in the area even further. On a macroeconomic level, we note the improvement in consumer sentiment for January and highlight the release of the ISM manufacturing PMI figure for January. The indicator’s reading remained below 50, implying another contraction of economic activity for the sector, yet the reading rose beyond expectations sending an optimistic message.

GBP – BoE remains hesitant to signal rate cuts

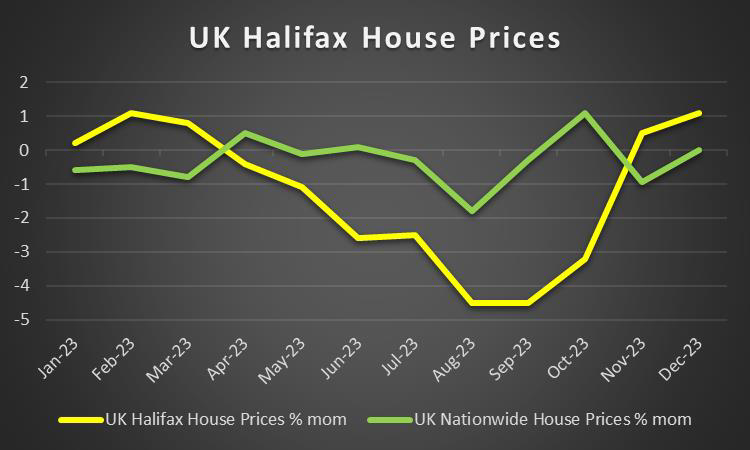

The pound is about to end the week relatively stronger against the USD and the EUR, yet weaker against the JPY. On a monetary level, BoE remained on hold as was widely expected, keeping rates unchanged at 5¼%. The bank in its accompanying statement, seemed prepared to keep a restrictive financial environment for a prolonged period in order to bring inflation down and it also seems to be targeting inflation from the services sector. Also, it’s interesting how the power balance within the bank changes, strengthening the extremes, as we have a first vote in favor of a rate cut while in favor of a rate hike, the votes are now two. In his press conference, BoE Governor Bailey highlighted that the bank is not at a point to discuss possible rate cuts yet, underscoring the bank’s hawkish tone. The release tended to provide some support for the pound and we expect the pound to remain supported on a monetary level. On a macroeconomic level, we note the acceleration of the nationwide house price growth rate for January, in an indication of wider demand for the housing sector. On the other hand, the final manufacturing PMI figure came in lower if compared to the preliminary release implying that the contraction in economic activity for the month in the sector was actually wider than initially estimated.

JPY – Safe haven flows to move the JPY

JPY is about to end the week higher against the USD,GBP and EUR, in a sign of wider strength. On a monetary level, we note the release of BoJ’s summary of opinions for the January meeting. The document tended to highlight the possibility of a continuance of monetary easing under yield curve control, as a sustainable and stable achievement of the price stability target has not yet come in sight. The release tended to contradict market expectations for a possible

normalisation of the bank’s ultra-loose monetary policy. Yet we have to note that there are a number of policymakers still pushing for an alteration of the direction of the bank’s monetary policy. On a macroeconomic level, we note the acceleration of the preliminary industrial output for December yet also mention that the rate failed to meet the market’s expectations. On the demand side of the Japanese economy, we note the beyond-the-market expectations, slowdown of the retail sales growth rate for the same month. So, the past week tended to dim the picture of Japan on a macroeconomic level. On a fundamental level, we note JPY’s dual nature as a national currency and a safe haven for the international markets. The latter may have been a key factor behind the strengthening of the JPY, as market worries for regional banks in the US in conjunction with a drop of US yields may have produced inflows for the Japanese currency. Should market worries intensify in the coming week we may see JPY gaining more ground and vice versa.

EUR – Eurozone’s inflationary pressures ease

The common currency is about to end the week stronger against the USD, lower against the JPY and relatively weaker against the GBP. On a fundamental level, we note the political turmoil troubling the EU, especially farmers in Belgium, France and Germany, who are protesting against increasing costs and the new green policy. Some of the measures announced by the EU Commission, including a limiting of imports of Ukrainian agricultural products and an easing of some green rules, may prove to be insufficient for an appeasement of European farmers. Overall should the situation be maintained or even escalate we may see it weighing on the common currency in the coming week. On a macroeconomic level, we note that inflationary pressures in January eased somewhat, intensifying the expectations that December’s acceleration, may have been temporary. Furthermore and despite the economic locomotive of the Eurozone, Germany, remaining in a recession for Q423, according to the preliminary release, the Eurozone as such avoided such a scenario for now, as the GDP rate for the Eurozone as a whole, ticked up. Nevertheless, we expect growth to deteriorate in the first half of the year due to the restrictive monetary policy of the ECB, and the prospect of a recession seems to be looming over the Eurozone. For the time being, we maintain the view that the ECB is to delay any rate cuts and it’s characteristic that ECB President Lagarde declined to give a timeline for interest rate cuts, as reported by Bloomberg and continued to state that “we are not there yet” regarding the inflation target.

AUD – RBA’s interest rate decision ahead

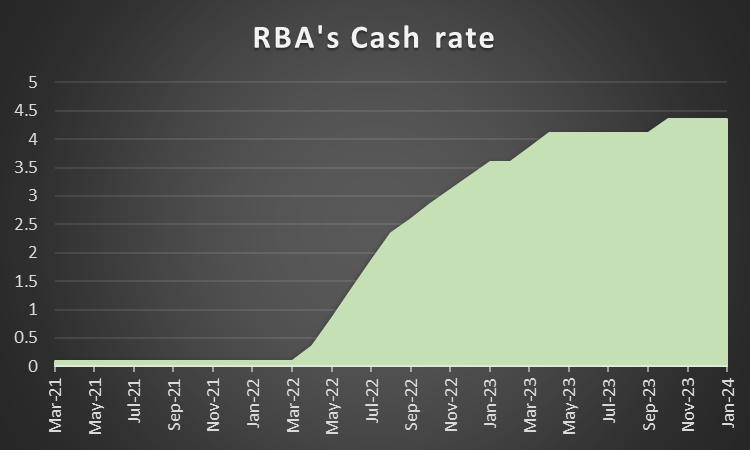

AUD is about to end the week in the greens against the USD. On a macroeconomic level, we note the wide contraction of the building approvals growth rate for December and we highlight the easing of inflationary pressures for Q4. On the monetary front, we note the release of RBAs’ interest rate decision on Tuesday’s Asian session. The bank is widely expected to remain on hold keeping interests at 4.35% and currently, AUD OIS imply a probability of 94.1% for such a scenario to materialise. Hence, we tend to expect market focus to be on the bank’s accompanying statement. We would expect the bank to maintain a hawkish stance implying a continuance of the restrictive financial environment in Australia. Yet the easing of inflationary pressures in Q4, may moderate the bank’s stance and if so, could weaken the Aussie. On the other hand, the CPI rate remains above the bank’s inflation target range of 2-3%, which may force the bank to remain strict in its hawkishness and such a scenario may support AUD. On a fundamental level, we note the close Sino-Australian economic ties and China’s NBS and Caixin manufacturing PMI figures for January are not exactly encouraging as Chinese factories seem to be struggling to keep economic activity afloat. Further signals of a failure of the Chinese economy to recover may weigh on the Aussie. Furthermore, we note the market’s perception as a riskier asset and should the market sentiment turn more cautious, we may see it weighing on the Aussie.

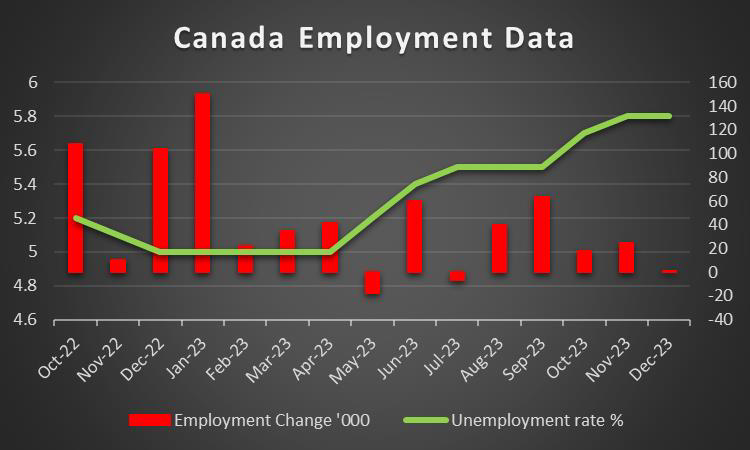

CAD – Employment data in focus

The Loonie is about to end the week, stronger against the USD, breaking a 5-week losing streak. On a macroeconomic level, we note that the manufacturing PMI figure for January rose, remained below the reading of 50, yet nevertheless, the release provided support for the Looney. Furthermore, we note the acceleration of the GPD rate for November, beyond the market’s expectations, which improved the outlook for the Canadian economy. Yet the release also tended to ease the pressure on BoC to proceed with extensive rate cuts within the year. We note that the market currently, tends to expect the bank to proceed with four rate cuts within the year, while inflation is nearing the bank’s target at a headline level. In the coming week, we highlight the planned speeches of BoC Governor Tiff Macklem on Monday and Tuesday. Should a possible hawkish tone in BoC Governor Macklem’s speeches emerge, we may see the CAD getting some support. On a fundamental level, we note the path of oil prices, given their positive correlation with the Looney. We tend to see the case for the fundamentals of the oil market to weigh on oil prices and in such a case we may see them weighing also on the CAD. Furthermore, we note that the CAD as a commodity currency is sensitive to the market sentiment and a possible cautious market sentiment, could also weigh on the CAD and vice versa.

General Comment

Overall, we expect volatility in the FX market to ease given that the frequency and gravity of financial releases is expected to ease as well. We also tend to expect the USD to relent some of the initiative to other currencies, allowing them to set their course more independently over the coming week. As for US equities markets, we note that the earnings period is still ongoing and could still attract investors. In the coming week we note the release of the earnings reports on Monday of McDonald’s (#MCD) and Caterpillar (#CAT), on Tuesday of Ford Motor (#F), Spotify Tech (#SPOT) and Snap (#SNAP), on Wednesday Alibaba (#BABA), Walt Disney (#DIS), Uber Tech (#UBER) and PayPal (#PYPL), on Thursday Philip Morris (#PM) and on Friday PepsiCo’s (#PEP). As for gold, we note the strengthening of its price, which is in line with the weakening of the USD, given the negative correlation of the two trading instruments. Furthermore, we note that the drop in US yields polished the shiny metal further, as bond investors may have turned their attention towards gold as a safe haven instrument. Should we see the greenback losing further ground in the coming week, we may see gold’s price rising further.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.