US stock markets are set to extend their losing streak today, after the delivery of hawkish statements from various Fed speakers that boosted the greenback and investors maintain their risk-on approach in a tumultuous global economic scene. In this report we aim to present the recent fundamental news releases that impacted the fall of the US stock markets, look ahead at the upcoming events that could affect their performance and conclude with a technical analysis.

Fed’s decision causes stock market selloff

As inflationary pressures continue to whiplash global markets, pushing central banks to press on with aggressive rate hikes, investors grow anxious as worries for economic slowdown and the prospect of recessions across the board loom over markets. The greenback continues to reign supreme in the foreign exchange market, attracting heavy inflows, while the US stock markets record significant losses, tumbling lower, reaching levels once seen before in 2020. Dollar dominance has been retained after Fed’s interest rate decision, which as widely anticipated, hiked interest rates by another 75 basis points, marking its third consecutive jumbo rate hike since June’s meeting. In its accompanying statement the central bank explicitly reiterated its pledge at bringing down inflation towards the 2% target level and in the revised dot plot graph the committee’s plans shifted towards raising interest rates higher and for a prolonged period of time, eyeing a ceiling of 5% in mid-2023, as the threat of inflationary pressures becoming deeply entrenched in the economy are significantly worrisome. Fed Chair Powell’s speech following the decision carried a clear and concise hawkish tone and warned of “pain” ahead for the economy as the central bank attempts to cool demand. Particularly striking, was the Fed Chair Powell’s inability to assess the probability of the US economy falling into a recession, raised concerns across the markets and had a detrimental effect on the US equity markets. Furthermore, the concerns were also reflected across the bond markets, where the US 10-year yield was on the rise, highlighting market worries, and the 2-year yield soared to new highs indicating that the market anticipates the recession to hit the US sooner rather than later. At the same time, we must note that the inversion of the yield curve continues, highlighting that the short-term risk is estimated by the market as high, actually higher than the long-term risk for the US economy to enter a recession.

Fed speakers to shake equities further

During this week a series of FOMC members are scheduled to deliver speeches and the market tunes in for clues. On Monday, Cleveland Fed President Mester stated that the “U.S. central bank needs to keep policy restrictive for some time, and if there is an error to be made, better that the Fed do too much than to do too little”, reiterating in a sense, the Committee’s unanimous consensus. A similar message was delivered by Chicago Fed President Evans, in favor for raising interest rates further, stating that “my viewpoint is roughly in line with the median assessment”, giving or at least maintaining for the time being, credibility in the central banks’ actions. Today we note the scheduled speeches by Saint Louis Fed President Bullard, Fed Governor Bowman, Atlanta Fed President Bostic and Richmond Fed President Barkin and should the hawkish rhetoric by the policy makers be maintained, we may see the dollar gain additional support and in contrast the US stock markets plunge lower as investors may opt for a risk on approach amidst the chaos.

To conclude, as the dollar continues to climb higher, supported by widespread fears of economic recessions across the world, the systematic weakening of other major economies’ currencies, persistent inflation and the prospect of high interest rates for prolonged periods of time, we hold the view that US stock markets are to remain in negative territory and continue to experience waves of outflows, as opportunities for further business development and profitability become scarcer.

Технический анализ

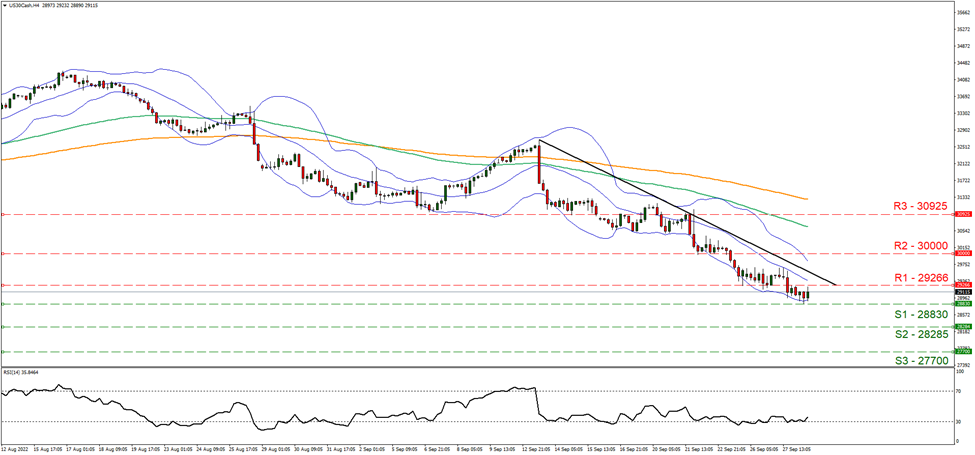

US 30 Cash, 4-Hour Chart

Support: 28830 (S1), 28285 (S2), 27700 (S3)

Resistance: 29266 (R1), 30000 (R2), 30925 (R3)

Looking at the 4-hour chart of Dow Jones we note observe its downward trajectory as indicated by the descending trendline initiated on the 13th of September and the price action reaching levels once seen before in 2020. We hold a bearish outlook bias for the continuation of the index’s price action moving to lower ground and supporting our case is the RSI indicator below our 4 hour chart which currently registers a value of 35 highlighting the persistent negative sentiment around the equity index. Should the bears continue to reign over we may see the break below the 28830 (S1) support base and a move near the 28285 (S2) support level. Should the bulls take over and for us to change our assessment we would require seeing the clear break above the 29266 (R1) resistance level, the definitive break above the descending trendline and the price action moving close to the 30000 (S2) resistance barrier.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.