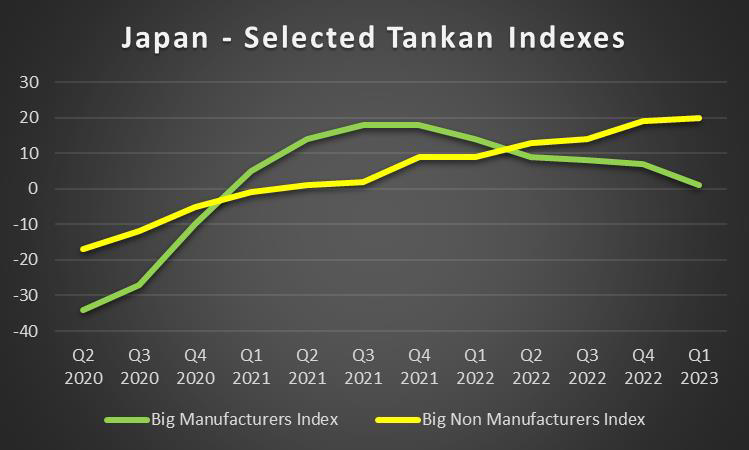

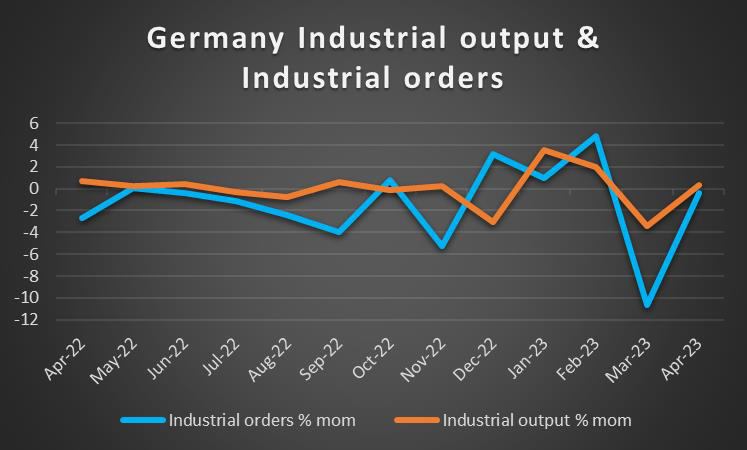

The week is drawing to a close with market worries for a possible global economic slowdown being intense, given the hawkish stance of a number of central banks. In the coming week, we note on a monetary policy level two events. The first is to be on Tuesday as RBA is to release its interest rate decision and the second on Wednesday as the Fed is to release the minutes of its June meeting. As for financial releases we note on Monday the release from Japan of the Tankan indexes for Q2, Australia’s building approvals for May, China’s Caixin Manufacturing PMI for June, Switzerland’s CPI rates for June and the US ISM manufacturing PMI for the same month. After a rather easy-going Tuesday, we note on Wednesday the release of Turkey’s CPI rates for June and the US factory orders for May. On Thursday we get Australia’s trade data for May, Germany’s industrial orders for the same month, the US weekly initial jobless claims figure, Canada’s trade data for May and the US ISM non-manufacturing PMI figure for June. Finally, on Friday get Germany’s industrial output for May, UK’s Halifax House prices for June, Sweden’s and Norway’s GDP rates for May and we highlight the US employment data for June as well as Canada’s employment data for the same month.

USD – US employment data and Fed’s minutes eyed

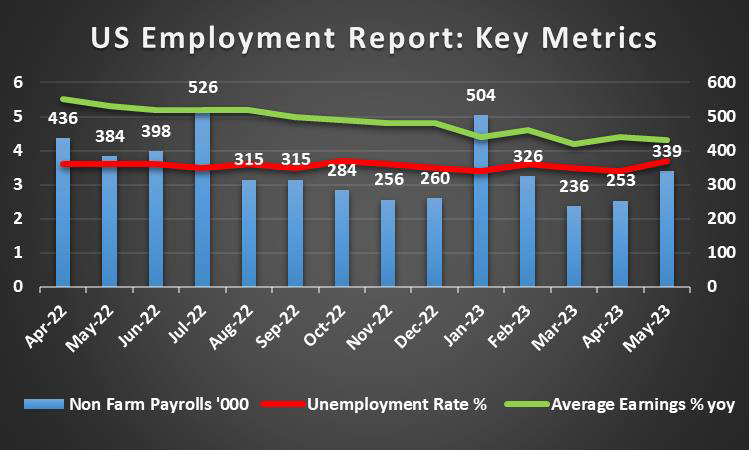

The USD is about to end the week higher against its counterparts. Despite the Fed remaining on hold in its last meeting we note that the bank maintains its hawkishness. It’s characteristic that Fed Chairman Powell in his speech at ECB’s annual forum in Sintra Portugal, doubled down on the bank’s hawkish stance as he did not exclude the possibility of back-to-back rate hikes while also stating that “If you look at the data over the last quarter, what you see is stronger than expected growth, a tighter than expected labor market and higher than expected inflation … That tells us that although policy is restrictive, it may not be restrictive enough and it has not been restrictive for long enough”. On the other hand, better-than-expected data from the US showed that consumer sentiment for June is more optimistic than expected, while at the same time, the number of new home sales for May was higher than expected, both pointing towards a more robust US economy and an appetite for more spending. At the same the acceleration of the US GDP rate for Q1, tended to imply that the possibility of a recession in the US economy may be avoidable. Yet exactly these readings, among others, may also imply that consumption could continue to feed inflationary pressures in the US economy, prompting the Fed to continue with its monetary policy tightening. In the coming week, we expect the release of the Fed June meeting minutes to shed more light on the bank’s intentions and should the document maintain the bank’s hawkishness we may see the USD getting some support. The crown though of financial data next week is expected to be the release of June’s employment data. The forecasts currently seem to be a bit mixed as the NFP figure is expected to drop, the unemployment rate to remain unchanged and the average earnings growth rate to accelerate. Overall a disappointment from a possible drop of the NFP figure could weaken the greenback, yet should the actual rates and figures meet their respective forecasts, the US employment market seems to remain tight, thus allowing the Fed to continue its monetary policy tightening.

GBP – BoE maintains its hawkishness

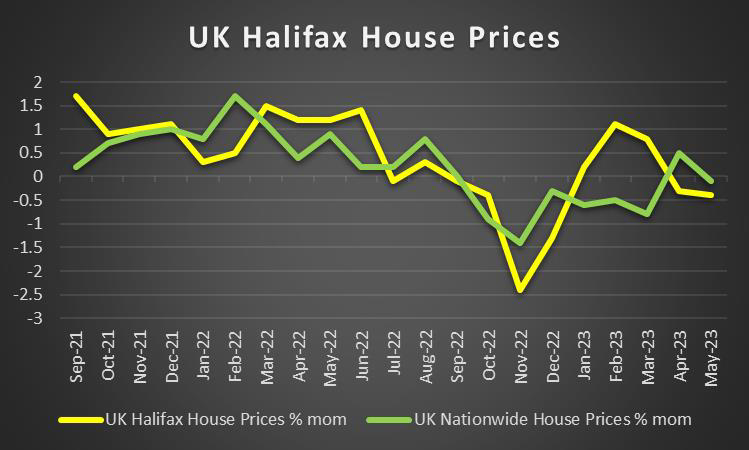

The pound is losing ground against the USD and EUR while it remains rather stable against the JPY, not exactly a sign of sterling’s strength. On a more fundamental level, we note the readiness of the UK Government to nationalize, even on a temporary basis, the large and highly indebted utility company Thames Water. Mind you that may not be the only UK water company in trouble. Such a development may burden the already strained fiscal policy of the UK Government. On a monetary level, we note that BoE seems to be maintaining its hawkishness and preparing for another rate hike. BoE Governor Bailey from Sintra, Portugal signaled that the bank is ready to keep rates at high levels, may we add even higher levels, for a prolonged period given the persistent inflationary pressures and the tight UK employment market. Please note that BoE Governor Bailey dismissed the idea that the UK employment market remains tight as a result of Brexit and instead suggested that it’s a response to the passing of the coronavirus crisis. Overall we expect the bank to remain hawkish which in turn may support the pound in the coming week somewhat. On a macroeconomic level, we note that the CBI distributive trades remained little changed in the negatives, showing a pessimistic outlook for UK retailers. Furthermore the wider contraction of the Nationwide House prices for June, was another possible symptom of BoE’s monetary policy tightening. Also, the GDP rate for Q1 remained in the positives, yet at anemic levels and given BoE’s hawkish intentions we may start seeing a recession on the horizon for the UK economy.

JPY – BoJ remains dovish

JPY is losing ground against the USD and EUR and seems to remain relatively stable against the pound as the week draws to a close, in a sign of wider weakness. Given the recent hawkish comments from ECB, FED and BoE officials on the one hand and the BoJ leaning on the dovish side on the other, we highlight the divergence of monetary policy outlooks which tends to weigh on the Japanese currency. The bank seems to remain dovish and ready to keep its ultra-loose monetary policy settings in place. It’s characteristic that BoJ Governor Ueda, stated while being at ECB’s forum that the underlying inflation is still below the bank’s 2% implying that there is good reason for BoJ’s dovish stance. Furthermore, we note that BoJ hit a new high in JGB holdings as the bank keeps pumping and may intensify bearish tendencies for JPY. Overall we note on a fundamental level that JPY is expected to continue weakening given that interest rate differentials widen as mentioned before, carry trade is also a threat and inflation seems to be easing, thus cementing BoJ’s stance, while the trade balance remains in the negatives, implying that more wealth is exiting the Japanese economy from the country’s international trading activities. On the other hand, JPY may get some support should the Japanese government come to the rescue of the Yen, given that Japan’s Finance Minister Suzuki declined to rule out the possibility of a market intervention. Furthermore, JPY may start getting its appeal back as a safe haven instrument should tensions in the global political scene and/or market uncertainty be on the rise again.

EUR – ECB locks in next rate hike

The common currency is gaining ground against the USD, JPY and GBP in a sign of broader strength for the common currency. ECB’s hawkish rhetoric seems to have contributed to that end. The bank sharpened its hawkishness at its annual forum in Sintra, Portugal over the past few days. ECB President Christine Lagarde cited the inflation tormenting the Zone as too high, while also implying that more rate hikes could be expected as she mentioned that “It is unlikely that in the near future, the central bank will be able to state with full confidence that the peak rates have been reached,”. Furthermore, we note that ECB Vice President De Guindos left the possibility for a rate hike in the September meeting open, while the market prices in a 25 basis points rate hike by the bank in its next meeting in July and another one in the September meeting. It’s understandable that the bank may keep rates at high levels for a prolonged period of time. As for the dynamics within the ECB, we expect Germany’s BuBa President Nagel to push harder for more rate hikes, given that the HICP rate seems to have accelerated in Germany for the current month despite slowing down everywhere else in the Eurozone, which in turn may deepen the rift between hawks and the rest in the ECB. On a macro level, the situation is not rosy. It should be noted that the economic outlook for the German Economy seems to become more pessimistic in June while also the conditions on the ground are deteriorating and should such indications multiply we may see EUR slipping.

AUD – RBA’s interest rate decision in focus

AUD’s weakening against the USD, from last week seems to continue, yet at lesser intensity. Nevertheless, the fundamentals are still providing headwinds for AUD given the market worries for a possible economic slowdown on a global level and at the same time AUD’s second nature as a commodity currency, which is also considered more risky. Furthermore, we note that China’s economic recovery is still not convincing, given that the NBS manufacturing PMI figure remained below the reading of 50, despite improving, implying another contraction of economic activity that may not bode well with Australian exporters of raw materials. At the same time, we note that inflation seems to have eased in Australia for May considerably. A development that may also allow RBA to dampen its hawkishness in its next interest rate decision, due out on Tuesday. For the time being, we note that AUD OIS imply a probability for the bank to remain on hold at 4.1% of 62.78%. It’s understandable as the minutes of the last interest rate decision, showed that the bank was ready to remain on hold at its last meeting and the decision to hike rates was taken with a “fine balance”, as we mentioned in a prior report. Given also the slowdown of the CPI rate we may see the bank pausing its rate-hiking path. Yet the market for the time being seems to expect another rate hike in the bank’s August meeting. Hence should also Governor Lowe’s accompanying statement, lean less on the hawkish side and also underscore that the bank is to remain data dependent implying more uncertainty, we may see the Aussie weakening as the market’s expectations may be contradicted.

CAD – Canada’s employment data eyed

The CAD is about to end the week in the reds against the USD, ending a winning streak of four weeks. On a macroeconomic level, we note that Canada’s CPI rates for May slowed down both on a core and headline level. The release may have been the main factor weakening the Loonie as the slow-down has supported the case for BoC to remain on hold. For the time being though the market seems to marginally price in the possibility of another rate hike in its July meeting and stand pat for the remainder of the year. Yet at this point, we have to note the worries for the Canadian housing market and mortgages. Overall should the markets maintain and intensify their expectations for another rate hike we may see the CAD getting some support. On a more fundamental level and given that Canada is a major oil-producing economy, we note the slight rise of oil prices for the week, which if continued and extended in the coming week may provide some support for the CAD as well. It should be noted that oil prices got unexpected support on Wednesday as the

EIA weekly US oil inventories figure dropped by 9.604 million barrels, substantially more than last week’s drawdown and than what the market expected. The release highlighted the US oil market’s tightness thus pushing oil prices higher. On the other hand, we note market worries for the demand side of the commodity may have clipped oil price’s gains. Should oil prices continue to rise, we may see the CAD getting some support. Last but not least, we would like to express our continuous worries regarding the wildfires in Canada as another ecological catastrophe is taking place.

General Comment

As a closing comment, we expect the USD to regain some of the initiative in the FX market over other currencies given that the number of high-impact releases stemming from the US seems to increase, with the US employment report for June on Friday being the highlight. Nevertheless, there are still instances that may allow other currencies to get under the spotlight and form their own course. As for US stockmarkets, we note the rise of Nasdaq, Dow Jones and S&P 500 as the week is about to end, implying an improved market sentiment US stockmarkets seem to have gotten a boost from improved market data. Should the market sentiment be improved in the coming week, we may see US equities getting some support. Furthermore, we note the steepening of the inversion of US yields highlighting the short-term risk the US economy is currently facing. A continuation of the rise of US yields may at the same time have a negative effect on gold’s price, given that the precious metal is not bearing interest, thus bonds may be more appealing. Also a possible strengthening of the USD could weigh on gold’s price further and vice versa.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.