The week is drawing to a close, yet as these lines are written, the US and Canadian employment data for February are still to be released and could alter the market’s mood, depending on the actual rates and figures to be released. Hence we have look at what next week’s calendar has in store for the markets. On Monday, we get Japan’s current account balance, Germany’s industrial output and Sweden’s GDP, all being for January, while from Norway we get February’s CPI rates. On Tuesday we get Japan’s revised GDP rate for Q4, Australia’s NAB business conditions and confidence for February, the Czech Republic’s CPI rates also for February, and the US JOLTS job openings figure for January. On Wednesday we get Japan’s PPI rates for February, we highlight the release of the US CPI rates for February and we get also from Canada, BoC’s interest rate decision. On Thursday we get Euro Zone’s industrial output for January, the US weekly initial jobless claims figure, the US PPI rates for February and Canada’s building permits for January. Finaly on Friday, we get UK’s GDP and manufacturing output rates for January and from the US the preliminary University of Michigan Consumer Confidence for March.

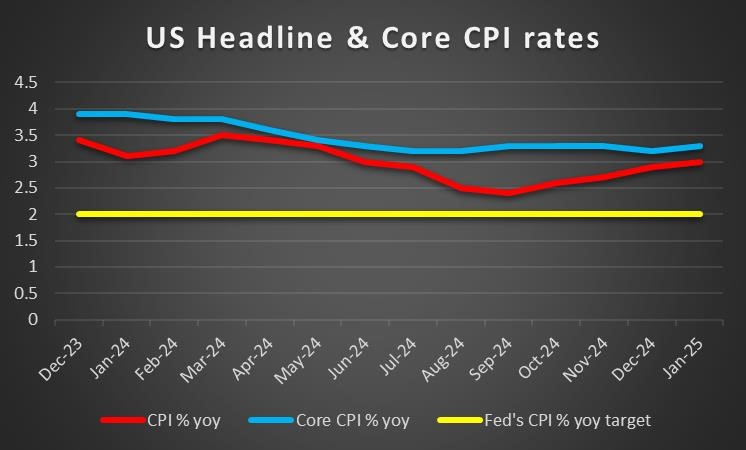

USD – February’s US CPI rates in the epicenter

The USD has reversed last week’s gains and is currently marking the biggest weekly loss since November 2022, yet the US employment report is still to be released as these lines are written and its release could alter the greenback’s path either way depending on the actual rates and figures. On a macroeconomic level, we note the market worries for the outlook of the US. The Atlanta GDP rate currently predicts a steep contraction of the US economy in the first quarter of the year of up to 2.4%. Overall, the outlook for the US economy tends to be increasingly pessimistic or at best, worries are growing, which in turn weigh on the USD.

On a monetary level, the Fed’s doubts for easing its monetary policy tend to remain. It’s characteristic how Fed policymakers are warning for inflationary pressures and cite US President Trump’s tariffs as the main factor. Currently the market seems to expect the bank to deliver another two rate cuts, one in May and one in October. Should the market’s dovish expectations ease further, we may see USD’s losses being clipped and after the release of the February’s employment report in today’s American session, we set the release of the US CPI rates for February next Wednesday, as the next big test for the USD. Should the rates show a persistence of inflationary pressures by failing to slow down or even accelerating we may see the USD getting some support and vice versa.

On a fundamental level, US President Trump’s tariffs are coming and going. It’s characteristic that tariffs of 25% on Canadian and Mexican products entering the US were applied early this week, only to be postponed for auto-parts for another month, on Thursday. Furthermore, additional 10% tariffs were applied on Chinese products. The application of tariffs and possible retaliatory action by targeted countries, enhances the uncertainty of the US, but also the global economic outlook. Hence do not rest assured that the US is finished with tariffs, by applying them on Canadian, Mexican and Chinese products. Economies such as the Euro Zone and Japan are next on the list enhancing uncertainty further. Overall any hardening of the Trump’s stance on the issue could support the USD as safe haven inflows may roll in while any easing could weigh on the greenback.

Analyst’s opinion (USD)

“Overall we see the case for the weakening of the USD to be maintained in the coming week, as market worries for the US economy outlook are intense. Yet a possible more hawkish stance by the Fed and/or a hardening stance on behalf of Trump for imposing tariffs could provide substantial support for the USD.”

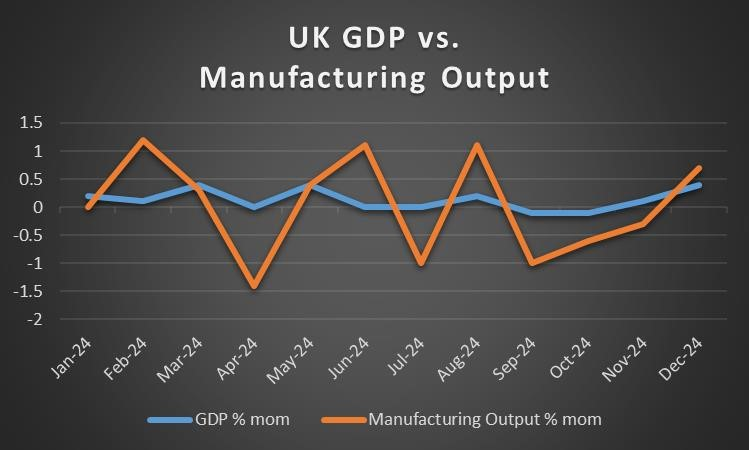

GBP – January’s GDP rate at the end of next week

On a monetary level, BoE seems to maintain its dovish orientation, yet may be easing a bit. The bank seems to be worrying about the possible negative effects the US tariffs on various countries, may have on the growth of the UK economy and BoE Governor Bailey’s comments were characteristic. For the time being we note the market’s expectations for the bank to cut rates two more times until the end of the year. No statements by BoE officials are on the calendar for the next week, yet should the market’s dovish expectations intensify, they may weigh on the GBP.

On a fundamental level, UK seems to be escaping Trump’s tariff intentions for now, given that international transactions between the UK and the US are balanced, which could be considered as a positive for the pound. Also we note the UK Government’s involvement in the future of Ukraine, yet that seems to be for the time being not market related.

On a macro-economic level, we note that final PMI figures for February verified the contraction of economic activity for the manufacturing sector and the expansion for the services sector. A negative surprise may have been, the drop of the construction sector’s PMI figure. In the coming week we highlight the release of the UK GDP rate for January on Friday amidst other financial data. Should the rate accelerate from December’s 0.4% mom we may see the GBP getting some support, as it would imply that the UK economy grew at a faster pace.

Analyst’s opinion (GBP)

“No major factor seems to be in support for the pound given BoE’s dovishness. Yet the market’s interest for January’s GDP rates could readjust the focus of pound traders’ attention on financial data as next week will be drawing to a close. ”

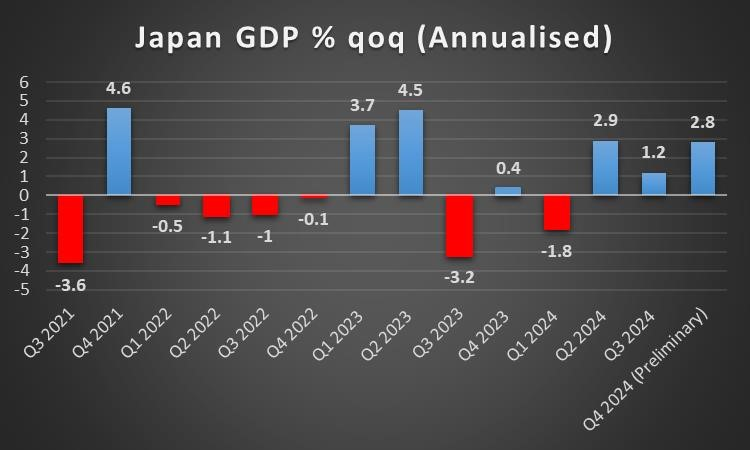

JPY – Revised GDP rate for Q4 amidst slew of financial data

The week passed rather unnoticed on a macroeconomic level for JPY traders, maybe with the exception of February’s final PMI figures. In the coming week, we get a number of financial data amidst which we note the release of the revised GDP rate for Q4, as the revised figure tends to differ from the preliminary release. A possible acceleration of the rate could provide some support for the JPY especially if the acceleration is substantial as the market may have to readjust its expectations for the macro-economic outlook of Japan.

As for JPY’s direction we highlight BoJ’s intentions as a major factor. For the time being the market expects the bank to proceed with another rate hike, possibly in the July meeting. Yet we see the case for the bank’s intentions to possibly exceed the market’s hawkish expectations. In any case BoJ Deputy Governor Uchida kept hopes alive for another rate hike to come, albeit downplayed the possibility of a rate hike in the coming meeting, in two weeks-time. Overall, we expect that should market expectations for further tightening of the bank’s monetary policy be enhanced, JPY could get additional support.

On a fundamental level, we note JPY’s safe haven qualities as a possible factor for its direction. A possible enhancing of the market’s uncertainty could provide support for the JPY and vice versa. Another issue that tended to pass under the radar over the week, was Trump’s innuendo for a “weak Yen”, implying that Japan is keeping the value of its currency artificially low. The overall issue awakened the possibility of the US imposing tariffs on Japanese products entering the US. Should such the possibility be enhanced in the coming week, we may see it weighing on the JPY.

Analyst’s opinion (JPY)

“We tend to highlight BoJ’s intentions as a key determinant of JPY’s direction and any hints for further tightening of BoJ’s monetary policy could aid the Japanese currency. Also a possible wide acceleration of Japan’s revised GDP rate for Q4 24, could provide some support for JPY ”

EUR – Germany’s fiscal bazooka

The common currency strengthened across the board for the week, with the USD being maybe the main victim. On a fundamental level, we note that the easing of market worries for the US to impose tariffs on European products may have been one of the factors supporting the EUR. We tend to disagree and expect the US to actually impose tariffs on European products, a scenario that may weigh on the single currency. Also on a fundamental level the enhanced market expectations for increased fiscal spending by the German government tended to support the EUR. The total investment could amount to some €1 trillion over the next years, and is targeting defence and infrastructure. Yet the issue may hit a halt as the German Government may have to alter or even eliminate the constitutional clause limiting its budget deficit. Should we see market expectations for an expansionary fiscal policy being enhanced, EUR could get additional support.

On a monetary level, as expected, ECB delivered a 25 basis points rate cut. In the accompanying statement the bank stated that monetary policy is becoming meaningfully less restrictive while it reiterated its determination to ensure that inflation stabilises sustainably at its 2% medium-term target. Despite the bank’s rates continuing to have a downward direction, we may be witnessing a slight shift towards a less aggressive dovish tone, which may ease market expectations for more rate cuts to come. Should such signals increasingly emerge in the coming week, we may see the market repositioning itself and thus providing some support for EUR.

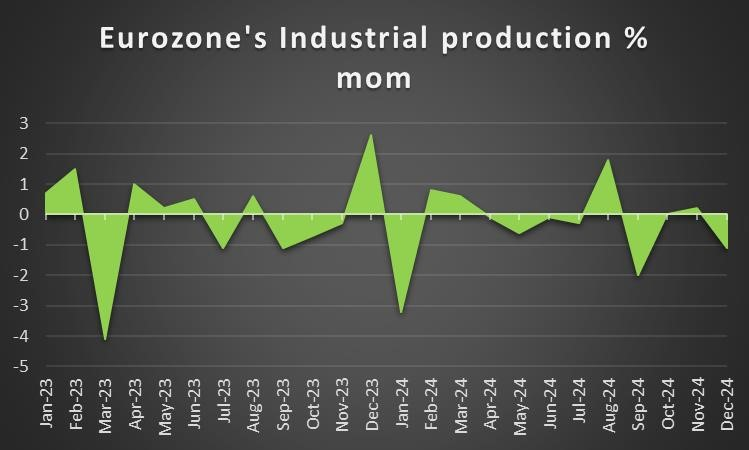

On a macroeconomic level we note the easing of demand in the Euro Zone for January as reported by the slowdown of the retail sales growth rate yet the highlight may have been the release of the preliminary HICP rate for February of the Euro Zone, implying that the disinflation process is ongoing yet at a possibly slower pace than expected. As for economic activity the revised GDP rate verified the anemic growth of the area’s economy for Q4 24, while Germany’s industrial orders growth rate for January showed a substantial contraction and both indicators tend to enhance the worries for growth in the Euro Zone. Overall the macro economics tend to weigh on the common currency and we do not expect that to change in the coming week, maybe one exception could come from Euro Zone’s Sentix index for March on Monday.

Analyst’s opinion (EUR)

“Overall we tend to highlight two issues for EUR traders in the coming week, the first being Trump’s tariffs and the second Germany’s expansionary fiscal policy plans., which tend to be opposing forces for the EUR. Should the market’s worries for US tariffs being applied on EU products intensify, we may see them weighing on the EUR, while should Germany’s fiscal “Bazooka” come stronger into play, we may see the EUR getting some support”

AUD – Fundamentals to lead

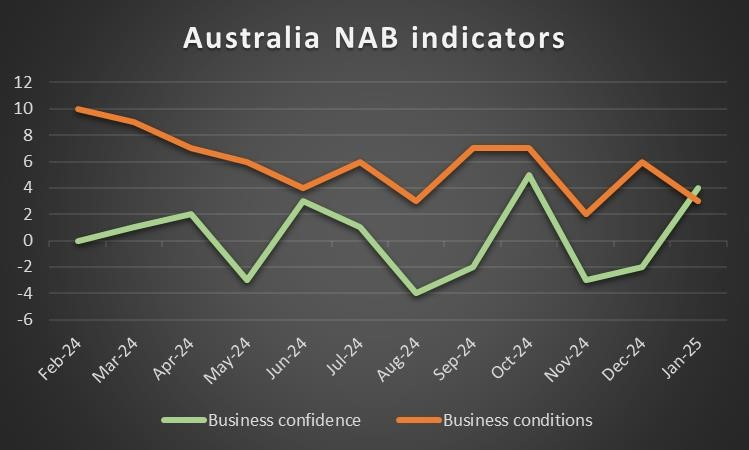

• On a monetary level, we note the release of RBA’s last meeting minutes, last Tuesday. In the bank’s minutes it was stated that “Members agreed that their decision at this meeting did not commit them to further reductions in the cash rate target at subsequent meetings”, implying that the bank may remain on hold in their next monetary policy meeting. Furthermore, it was also stated that the return of inflation to the bank’s inflation target zone, whilst preserving the labor market was not yet assured. Overall the bank’s minutes could be interpreted as predominantly hawkish in nature, and should such signals multiply in the coming week, we may see the Aussie getting some support.

On a macroeconomic level, we highlight the wider than expected acceleration of the GDP rate for Q4 25, implying that the Australian economy grew at a faster pace than expected. But also the widening of Australia’s trade surplus in January, the acceleration of the retail sales growth rate for January and of the building approvals growth rate for the same month were positive signs. In the coming week, given the lower number of Australian high impact financial releases in the calendar, we expect Aussie traders to focus mostly on fundamentals.

Fundamentally the Aussie could get some support should the market sentiment improve given the perception of AUD being a riskier asset due to its commodity nature. The close Sino-Australian ties also force Aussie traders to keep an eye out for developments in China. In the past few days there were some mixed signals as on the one hand economic activity in China’s manufacturing sector improved, as per the Caixin Mfg PMI figure for February, which was a positive while the slowdown of China’s import growth rate for the same month may spell trouble for Australian exports of raw materials.

Analyst’s opinion (AUD)

“Overall, given the low number of high impact financial releases from Australia in the coming week, we expect Aussie traders to focus on fundamentals. Any improvement of the market sentiment could aid AUD, while any intensification of the US-Sino trade war could weigh on the Aussie”

CAD – BoC to cut rates further?

On a fundamental level, we cannot downplay the importance of the US tariffs on Canadian products which are coming and going. Should tensions in the US-Canadian relationships intensify we may see them weighing on the Loonie. Also the drop of oil prices over the past few days does not pose well for the CAD. On a political level, we note that Canada’s PM Justin Trudeau is stepping down and the Liberal party is to elect its new leader on Sunday. Headlines highlight former central banker Carney and former finance mnister Freeland as possible successors. Maybe the most impressive development after Trudeau stepped down was that the Liberal party was able to recover in opinion polling. It seems that Trump’s tarifs and foreign policy created a rally around the flag effect in Canadian politics, while the stepping down of Trudeau as such and the prospect of a new leader in the Liberal party allowed for estranged liberals to return to the party. The new Liberal leader is to be the new PM of Canada and lead the country to the October elections.

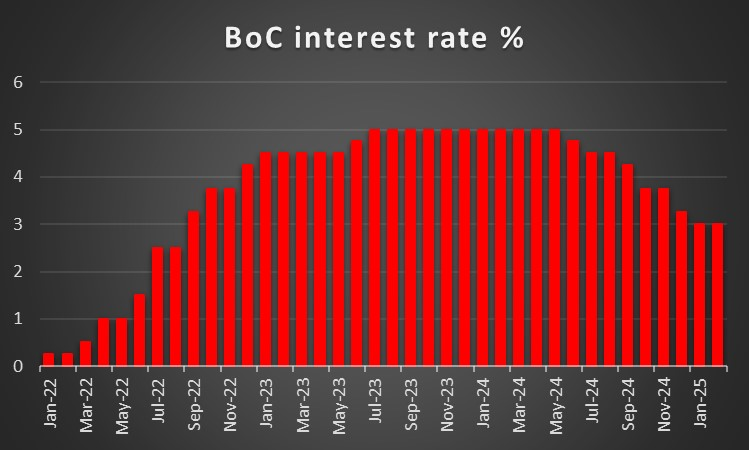

On a monetary level, we highlight the release of BoC’s interest rate decision next Wednesday. The market seems to expect the bank to deliver a 25 basis points rate cut, lowering rates to 2.75%. Currently CAD OIS imply a probability of almost 70% for such a scenario to materialise, while the rest imply that the bank could also remain onhold. The market also seems to expect the bank to continue cutting rates further, with the next rate cut possibly being in the June meeting. Hence should the bank cut rates as expected, it could weigh a bit, yet we expect market focus to shift to the bank’s forward guidnace and should BoC maintain a dovish tone, it could weigh on the CAD. On the flip side should the bank issue a forward guidance which will be more hawkish, the event could turn to be a hawkish rate cut which could provide support for the Loonie.

On a macrolevel we highlight the releae of Canada’s February employment data which is to be released in today’s American session and a possible loosening of the Canadian employment market could weigh on the Loonie as it may enhance the dovish expectatiosn of the market for the BoC next week and vice versa. We also note the drop of the manufacturing PMI figure for February below 50, implying a contraction of economic activity for the sector and was considered a negative signal, yet on the flip side, Canada’s trade surplus widened beyond expectations for January, providing a more positive tone. In the comign week, we have no major financial releases from Canada, thus attention may be shifted away from macroeconomics.

Analyst’s opinion (CAD)

“Overall for Loonie traders we highlight three issues, the first being the release of February’s employment data on a macro level and a looser Canadian employment market could weigh on the CAD. Second and on a fundamental level we note the US/Canadian trade relationships and Trump’s tariffs, where any escalation of frictions could weigh on the CAD, while thirdly and on a monetary level, BoC’s interest rate decision could rock the Loonie. A possibly more dovish BoC could weigh substantially on the Canadian currency ”

General Comment

As a closing comment, we expect the USD to maintain the initiative in the FX market in the coming week given the gravity of the release of the US inflation data. Moreover, we remain vigilant for new unexpected announcements by US President Trump which could create mayhem in the markets. As for US Equities markets we note the wide drops of all three major equity indexes in the US, namely the Dow Jones, S&P 500 and Nasdaq. Fundamentals such as the market worries for the US economic outlook and the uncertainty caused the US administration’s trade war tends to feed equity bears. As for gold’s price, the upward motion seems to have been halted as if gold bulls are taking a break. Increased uncertainty could renew the bullish tendencies and bring the precious metal’s price to new record high levels.