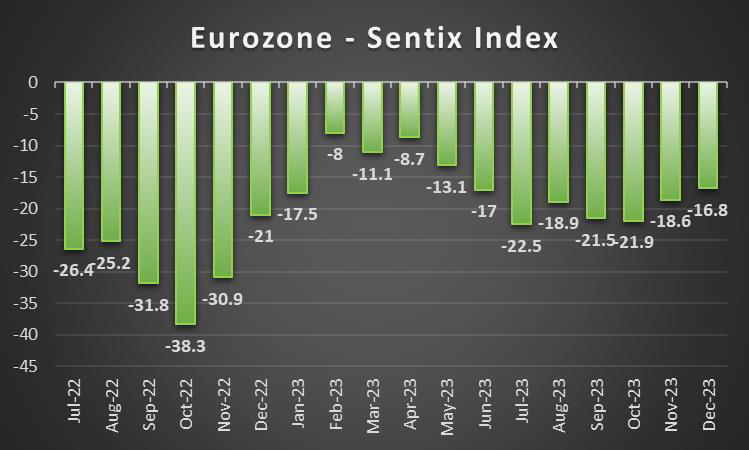

As the week draws to a close, markets are gradually waking up from the holiday season. We note the high number of financial releases in the next week. Making a start on Monday, with the release of Germany’s industrial orders rate for November, Switzerland’s CPI rate for December and the Eurozone’s Sentix index figure for January. On Tuesday, we note Japan’s Tokyo Core CPI rates for December, Australia’s retail sales rate and Germany’s industrial production rate both for November and lastly Canada’s Trade balance figure for November. On a quiet Wednesday, we note Australia’s CPI rate for November and Norway’s CPI rate for December. On Thursday, we note Australia’s trade balance figure for November, followed by the Czech Republic’s and the US CPI rates both for the month of December and closing off the day is the US weekly initial jobless claims figure. Finally, on a busy Friday, we note China’s PPI and CPI rates and trade balance figure all for the month of December, followed by the UK’s Preliminary GDP rate, Industrial output rate and Manufacturing output growth rates all for the month of November, France’s Final HICP rates and the US PPI rates both for December.

USD – FOMC indicates rate cuts are on the menu

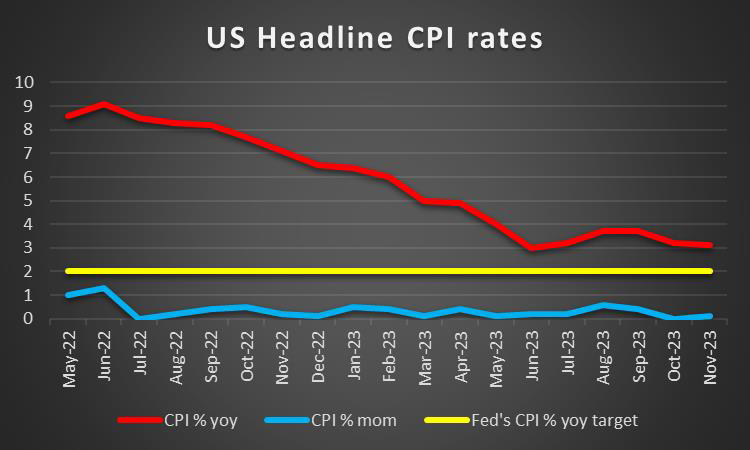

The USD seems about to end the week in the greens, ending its 3-week losing streak. On a monetary level, we note that FOMC’s December meeting minutes which were released during yesterday’s American session, tended to verify that the bank has likely reached its terminal rate and that rate cuts are on the “menu” for this year. Yet, market participants who may have been hoping for a validation of the current market expectations of 6 rate cuts this year, beginning in March, may be somewhat disappointed, as several policymakers implied that the current level of interest rates may need to stay for a longer time period, a view we tend to agree with. As such, we may see support for the dollar, should the Fed follow through on its intentions. On a macroeconomic level, we note the release of the ISM Manufacturing PMI figure for December on Wednesday, which implied a narrowing in the contraction of economic activity for the US manufacturing sector, which may have aided to the dollar’s ascent. Yet market participants may be more interested in the release of the US Employment data later on today, where should it be implied that the labor market remains tight, we may see the dollar gaining and vice versa. We place a heavy emphasis on this financial release, given that it will be the first major release for the new year and could have a significant impact on the greenback. Looking at next week, dollar traders may be interested in next week’s CPI rates for December, where should it be implied that inflationary pressures are easing further, it could weigh on the dollar as it would allow market expectations for the Fed’s actions to solidify. Lastly, we also note the PPI rates for December, which are to gauge inflationary pressures at a producer’s level.

GBP – GDP rate for November due out next week

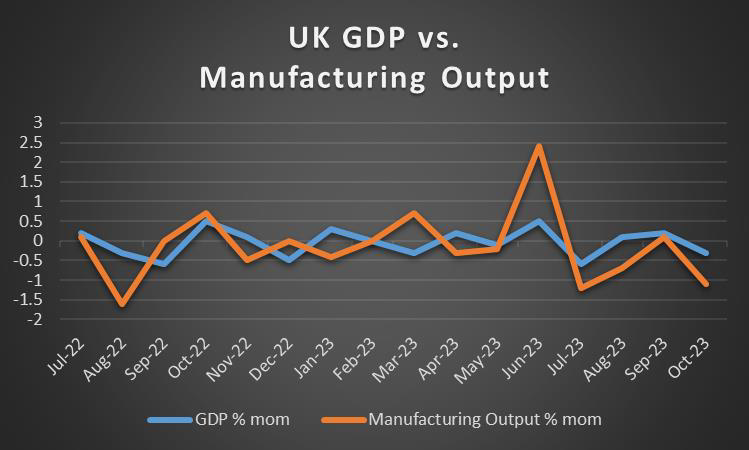

The pound is about to end the week lower against the EUR, and the US dollar, yet stronger against the JPY. On a monetary level, we note the relatively quiet week from BoE policymakers and as such pound traders may be more interested in financial releases stemming from the UK. In particular, the S&P Manufacturing PMI figure for December tended to highlight the potentially dire situation of the sector yet market worries tend to be balanced by the increased economic activity of the services sector. Nevertheless, we maintain our concerns for the UK economy heading in 2024 and as such, pound traders may be interested in next week’s financial releases, where the UK’s preliminary GDP rate for November is due to be released on Friday. Should the GDP rate imply that the UK economy has continued contracting, we may see the pound weakening and vice versa.

JPY – Difficult start for Japan

JPY is about to end the week in the reds against the dollar, EUR and the pound in a sign of broader weakness. On a monetary level, we note that BOJ Governor Ueda appears to have signaled clearly the bank’s willingness to abandon their decades-long monetary policy “if the virtuous cycle between wages and prices intensifies and the likelihood of achieving the price stability target of 2 percent in a sustainable and stable manner rises sufficiently”, which may have provided support for the Yen. However, we note the

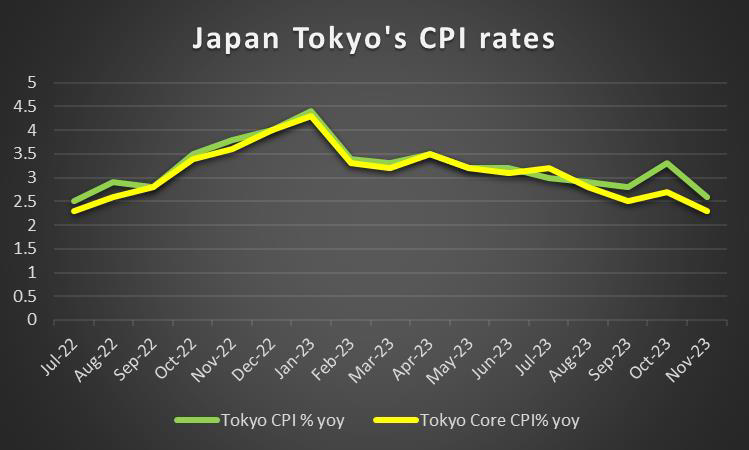

Earthquake that hit Japan on New Year’s day may be having a monetary impact as well. The earthquake that struck Japan which measured a 7.6 magnitude on the Richter scale, may place higher barriers for the bank to change their monetary policy stance, as the economy may not be able to withstand such a large change under such circumstances. As such, the bank may delay any potential change in its monetary policy decision, which could weaken the Yen. On a macroeconomic level, we note Japan’s Tokyo Core CPI rate for December which is due to be released next Tuesday. Should the Core CPI rate imply that inflationary pressures are persisting in the Japanese economy, the need to abandon the bank’s ultra-loose monetary policy may be enhanced, thus potentially supporting the Yen and vice versa.

EUR – EU treads on the edge of recession

The common currency is about to end the week in the reds against the USD and GBP but higher than the Yen. On a monetary level, we note the relatively quiet front from ECB policymakers and as such our attention turns to the financial releases stemming from the Euro area this week. In particular, we begin with the Manufacturing PMI figures for December for the Euro Area as a whole, France and Germany, which all came in better than expected earlier on this week. The better-than-expected PMI figures may have provided some relief for the EUR, yet we should still note that despite the narrowing contraction of the Manufacturing sector, it is still in contraction territory and the better-than-expected figures were just barely higher. As such, despite the PMI release, it may be concerning for Eurozone’s economy that the two largest countries in the bloc, continue to experience a contraction in their manufacturing activity as it could heighten fears for a potential recession in the bloc. Therefore, from a macro perspective we may see the EUR weakening, should the recession fears intensify. Moreover, despite December’s lower-than-expected Preliminary HICP rates for France and Germany on a mom level, they are still higher than the last readings, implying entrenched inflationary pressures in the bloc. Hence should ECB policymakers maintain the call to maintain rates at their current levels for a longer period we may see the EUR getting some support.

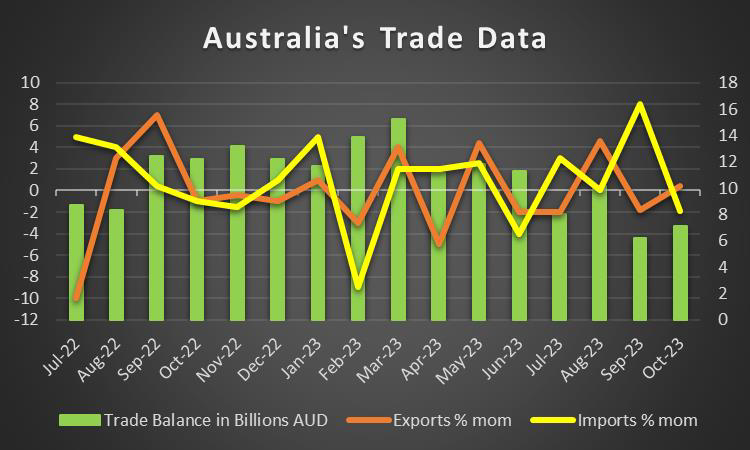

AUD – Worries for China

AUD is about to end the first week of 2024 in the reds against the USD. On a monetary front, we note that RBA’s interest rate decision that was due to occur on the 2nd of January appears to have been pushed back to the 6th of February. On a macroeconomic level, we note the release of Australia’s Manufacturing and services PMI figures both for December, which both came in lower than expected, implying a wider contraction of economic activity in both the manufacturing and services industry. The lower-than-expected releases may have weighed on the Aussie during the week. On an economic level, we turn our attention to China, which released its NBS and Caixin Manufacturing PMI figures for December, which continue to contradict one another and as such may have led to increased volatility in the Aussie given their close economic ties. On a fundamental level, we note the increasing tensions between the island of Taiwan and China, which could lead to increased volatility in the region and could weigh on the Aussie in the near future.

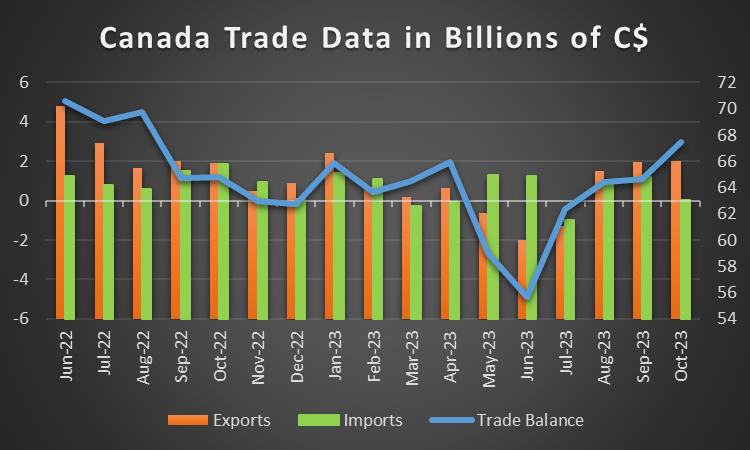

CAD – Canada’s trade balance for November due out next week

The Loonie is about to end the week against the USD in the reds. On a fundamental level, we note that oil prices over the week are on track to end the week slightly higher. As such, should oil prices continue their upward trajectory, we may see the higher oil prices providing support for the Loonie, given Canada’s status as a major oil producer. Moreover, with the continued tensions in the Middle East and in particular Iran, the Red Sea closing and Libya, we may see oil prices remaining slightly elevated over the next week. On a macroeconomic level, we note Canada’s employment data which is due to be released later on today during the American session, which is expected by economists to highlight a loosening labour market and as such could weigh on the Loonie. Yet Canada’s Ivey PMI figure is expected to increase, which may imply an expanding manufacturing industry for Canada and as such could provide some comfort for CAD traders. Lastly, Loonie traders may be interested in Canada’s trade balance for November next Tuesday, where should it come in higher than expected, it may provide support for the CAD and vice versa.

General Comment

Overall we expect market activity in the coming week to intensify, as we kickstart the new year with key financial releases. In regards to US stock markets, we saw the bears taking control over the markets, with all three major indexes seemingly on track to end the first trading week of the year in the reds. In the coming week, we may see market interest start shifting towards US stock markets as the

earnings season begins, with big banks such as JP Morgan (#JPM), Bank of America (#BAC), Wells Fargo (#WFC) and Citigroup (#C) making their releases. We also note that the US bond yields in particular the 5-Year and 10-Year moving higher this week. It should be noted that the rise of US yields may have weighed on gold’s price as did the strengthening of the USD, given their negative correlation. Lastly, we note that volatility appears to be picking up in the Middle East with Iran having faced a terrorist attack and protests hindering the production of Libya’s largest oil field, which may lead to elevated oil prices. Moreover, the heightened risks of attack by Houthi rebels in the Red Sea appear to have intensified and as such, hindering passage through one of the world’s most vital trade arteries could have an impact on the global economy. Lastly, tensions between Taiwan and China appear to be escalating and as such we are keeping a close eye on the developments, as they could upset the delicate stability in the region.

Se tiver alguma dúvida ou comentários sobre este artigo, solicitamos que envie um email diretamente para a nossa equipa de Research através do research_team@ironfx.com

Isenção de responsabilidade:

Esta informação não é considerada como aconselhamento ou recomendação ao investimento, mas apenas como comunicação de marketing. O IronFX não é responsável por quaisquer dados ou pela informação fornecida por terceiros aqui mencionados, ou com links diretos, nesta comunicação.