Despite volatility seemingly subsiding this week, markets may not be out of the woods just yet and we take a look at what next week has in store for the markets. On the monetary front, we note a relatively quiet week from monetary policymakers, given the public holidays as Christian easter is upon us, while on a more fundamental level, we note the IMF and World Bank 2023 spring meetings commencing on Monday. We note the release of Canada’s BoC interest rate decision on Wednesday, while on the same day, we also highlight the release of the Fed’s March meeting minutes. As for financial releases, we make a start on Monday with Japan’s Current Account figure for February. On Tuesday, China’s CPI and PPI rates for March. On Wednesday, we note the release of Japan’s Machinery Orders and Corporation Goods Prices and the US inflation metrics, all for the month of March. On a busy Thursday, we anticipate Australia’s Employment data, followed by China’s trade data and in the European session, Germany’s Final HICP rate, all being for March followed by UK’s GDP and Manufacturing output growth rates for February, the Czech Republic’s CPI rates for March, Eurozone’s Industrial Production for February and lastly the weekly US Initial Jobless claims figure and the PPI rates for March. Finally, on Friday, we have New Zealand’s Manufacturing PMI, Sweden’s CPI and France’s Final HICP rate all for March, and at the finishing of the day we have Canada’s Manufacturing Sales for February and the US Industrial Production for March the preliminary University of Michigan Consumer Sentiment for April.

USD – Traders to set their targets on CPI rates next Wednesday

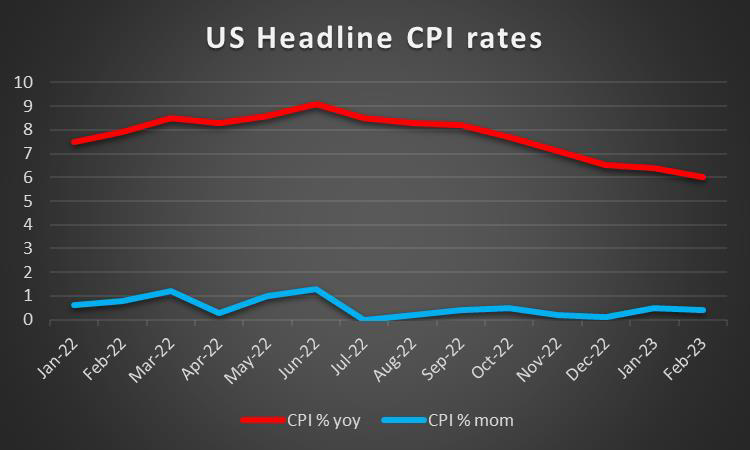

The USD is about to end the week in the reds against its counterparts. On a fundamental level, we note the market worries of a recession as the impact of high-interest rates appears to be making their presence felt on US economic data. It’s characteristic that the ISM manufacturing PMI figure for March dropped to new record post-pandemic lows, while the non-manufacturing PMI figure also indicated a slowdown of expansion of economic activity. But also employment data, the JOLTS job opening for February, the ADP National employment figure for March and the initial jobless claims figure, were disappointing. Please note though that March’s US employment report with its NFP figure is still to be released as these lines are written and may alter the greenback’s direction. In the coming week, we highlight the release of the US CPI rates for the past month, as inflation is the main determinant regarding the Fed’s monetary policy outlook. A possible easing of inflationary pressures may weaken the USD as it may ease the market worries about the Fed’s intentions. On the demand side of the US economy, we note the release of March’s retail sales and the preliminary UOM consumer sentiment for April. The situation remains fragile though as traders tread carefully through the murky waters. In an unexpected revelation, JP Morgan Chase CEO James Dimon stated that the Fed stress-testing system was “inadequate and never incorporated interest rates at higher levels” which fuelled the hunt by US lawmakers to maintain their siege of the Federal Reserve. Despite attempts by officials and central bank policymakers to calm investors, some key industry players may still believe that the banking industry is still fragile and will require a delicate touch to prevent further fallout. On a monetary policy level, we note that Fed policymakers such as Cleveland Fed President Mester and Fed Board Governor Cook sounded hawkish. We highlight the release of the Fed’s March meeting minutes, exactly to see how deep the bank’s hawkishness is. Should the document actually maintain a confident, hawkish tone, implying more monetary policy tightening, we may see the greenback getting some support.

GBP – BoE’s Pill lifts the pound on his shoulders

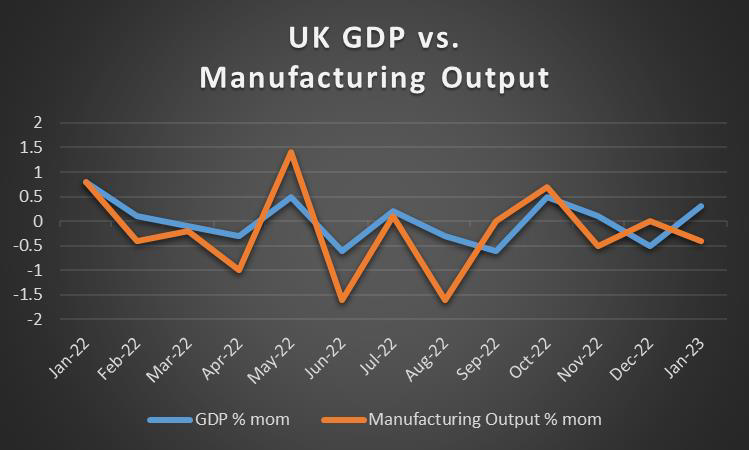

GBP is about to end the week slightly lower against the JPY and higher against the dollar while remaining relatively stable against the common currency. On a fundamental note, we highlight that out of the major economies, the UK appears to be more financially stable allowing for the sterling to counteract the dollar heavyweight. On a monetary level, BoE Governor Pill’s speech on Tuesday was hawkish as he stated “if there were to be evidence of more persistent [inflationary] pressures, then further tightening in monetary policy would be required”, potentially indicating the intentions of BoE when they are meeting on the 11th of May, as the current level of inflation is “unacceptably high” (as Pill also stated), following the acceleration of the CPI rates for February, a tone that could provide support for the sterling. However, should other BoE officials such as MPC Member Tenreyro, present a more dovish outlook, as was seen during her speech on Tuesday where she said “the MPC will need to take into account the resulting extra tightening in credit conditions when choosing a Bank Rate path”, we may see the pound slipping. On a macroeconomic level, we note the UK’s Manufacturing PMI for March which verified that the UK manufacturing sector’s economic activity contracted even further since February and might be experiencing the lagging impacts of persistently tightening monetary policy. On the flip side, any further monetary policy easing may boost economic growth, hence we intend to monitor closely, besides BoE officials’ statements, also any key financial releases stemming from the UK especially the GDP rate for February on Thursday.

JPY – Yen sits atop a see-saw with market worries on one hand and economic data on the other

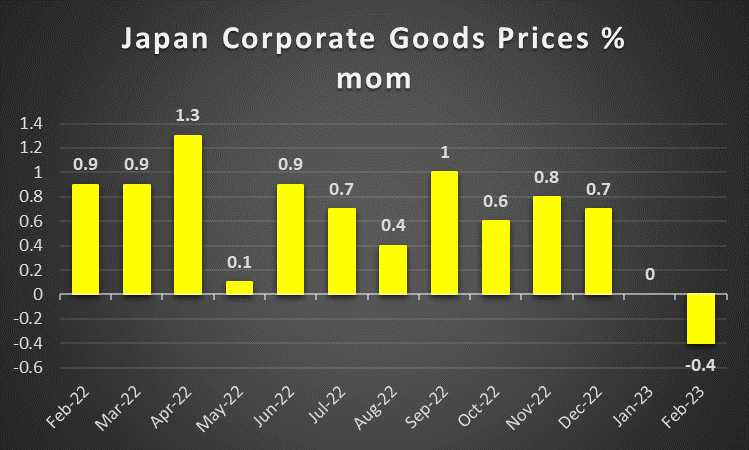

JPY is about to end the week slightly stronger than last week’s closing price against the greenback, common currency and the pound, indicating that the JPY has shown a general sign of strengthening as market sentiment remains indecisive. Overall, inflows are enjoyed by the Yen during times of unrest in the markets, as it is considered a safe haven. On a monetary policy level, we note the changing of the guard in BoJ as Kazuo Ueda will formally take over as Governor on Sunday could indicate new policies for the BOJ thus potentially indicating that the years of ultra-loose monetary settings could be gradually phased out thus potentially supporting the JPY. We note that in the event that Governor Ueda indicates a willingness to move away from the central bank’s bond yield control policy may provide some insight into the next BoJ meeting on the 28th of April. Thus following from last week the possibility of less frequent BOJ JGB purchases, may allow for the Japanese Yen to strengthen. On a fundamental level, we note JPY’s dual nature as a safe haven instrument and a national currency and the possibility of further tensions supporting it, while a further easing of market worries may weaken it. Furthermore, we note the agreement signed between Japan and Russia in regards to purchasing oil above the price cap imposed by the US, may have been a result of no alternative options, as other options for the supply of the badly needed oil, may have resulted in the possibility of a slowdown in the Japanese economy. On a macroeconomic level, we note that Japan’s Tankan Manufacturing index was reduced for Q1 which may support a slowdown of economic activity in Japan’s key manufacturing sector. As for the coming week, we note the importance of next week’s Corporation Goods Prices for March and Machinery orders for February as they provide further insight into the Japanese economy and should the data be favourable we may see JPY gaining somewhat.

EUR – Light at the end of the tunnel?

The common currency was on the rise against the USD, but appeared to weaken against the GBP for the week. On a monetary level, EUR traders’ expectations that the ECB has some leeway if they choose to proceed with further monetary policy tightening tended to rise, yet the lower-than-predicted PPI rates for February may be a subtle reminder that easing inflationary pressures. It should be noted that last week’s CPI rates release showed that HICP rates are still above the bank’s target, despite a slowdown, refuelling the hawkish rhetoric of ECB President Lagarde who stated that underlying inflation remains “significantly too high”. Overall, on a macro level, traders may anticipate the release of the Eurozone’s Industrial Production figure for February for a more complete outlook on the Eurozone economy as the situation remains volatile after the confirmation of the contraction of economic activity for March, in the manufacturing sector of Germany and Eurozone’s as a whole. On a fundamental level, the continued social upheaval in France with workers’ unions announcing that strikes will continue and last week’s strikes in Germany may slow down growth and thus may weaken the common currency. Also, we note the absence of new developments in the recent shake-up of Deutsche Bank thus it may appear that market worries seem to have been alleviated, potentially resulting in support for the common currency. Yet the situation may change at any time and requires continuous monitoring.

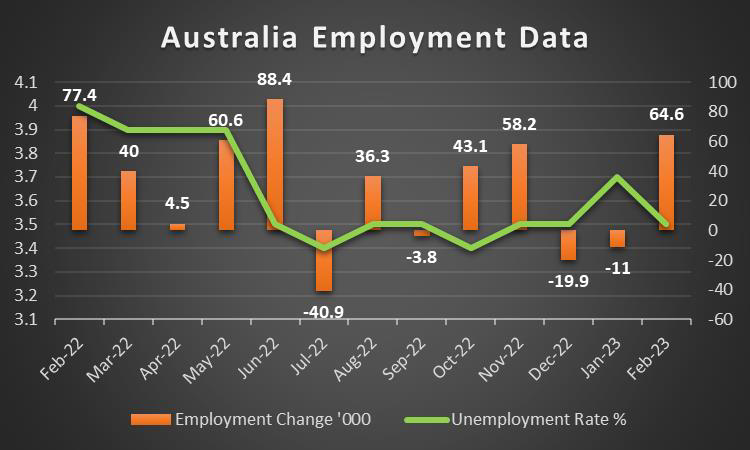

AUD – RBA holds the interest rate ship steady

AUD seems to have slightly weakened against the USD since last week’s closing price, as the week draws to a close. On a monetary level, we note RBA’s decision on Tuesday to hold rates at their current levels as was widely anticipated. We note the justification released that the decision was made in order to allow for the RBA to assess the impact of past increases. However the most significant element of Governor Lowe’s accompanying statement may have been that “inflation has peaked in Australia”, thus may indicate that interest rates may have reached or are nearing their terminal level. This could potentially weaken the Aussie against its counterparts as we may see the RBA remaining on hold as stated in last week’s outlook. On a macro level, we note the release of Australia’s employment data next week, and should the release show a tight Australian employment market we may see the Aussie gaining. On a more fundamental level, a possible continued deterioration of the US-Sino relationship may weaken the Aussie, given the close Sino-Australian economic ties. Especially considering the recent statement by Australia’s Prime Minister Albanese who according to Reuters stated that he has yet to receive an invitation to visit China. On a macro level, we note the release of China’s inflation metrics for March next week, yet we also highlight the release of China’s trade data for the same month and especially the import growth rate which may potentially be signaling fewer exports of raw materials from Australia to China if it slows down, which in turn may weaken the Aussie. Overall, we view the release of March’s employment data next week to be the main driver for the Aussie, yet we note that on a fundamental level, the Aussie as a commodity currency remains quite sensitive to the market sentiment. An improvement of the market sentiment could provide support for AUD and vice versa.

CAD – BoC’s interest rate decision in the limelight

The CAD seems to have remained relatively unchanged against the USD for the week. It should be noted that Canada’s Manufacturing sales for February are set to be released next week. On a macroeconomic level, we highlight the slashing of the trade surplus for February in comparison to January, while on the flip side, we had better-than-expected Employment data for the past month. On the monetary front, we highlight BoC’s interest rate decision next Wednesday. The bank is widely expected to remain on hold at 4.50% and characteristically CAD OIS imply a probability of 86% for such a scenario to materialise at the time. We expect market attention to turn to the accompanying statement and should any forward guidance included in it sound uncertain or even dovish, we may see the CAD slipping. On a more fundamental level, we note that WTI’s price seems to have skyrocketed during the week following the announcement by OPEC+ to cut production by 1.16 million barrels per day. As such should the bullish tendencies for the commodity’s price be maintained, the CAD may experience inflows given that Canada is a major oil-producing country. Furthermore, on a fundamental level, we should note as a negative development, the fact that Toronto-Dominion Bank, during the week became the largest shorted bank globally which may weaken the CAD if negative reports continue to reel in, given its size as the second largest bank in Canada. Such a development could undermine the financial stability of the country thus such rumours may weaken the Loonie on a fundamental level, as the stakes are high.

General Comment

As a closing comment, following IMF’s grim outlook on Thursday that the global economy is set for years of weak growth according to the Financial Times, we may see the market starting to shake, potentially increasing the risk of market volatility. Following the OPEC+ surprise decision to cut oil production, we may

see an increase in inflationary pressures as energy costs increase thus potentially making the job of central banks to combat inflation much harder. In a more general sense, we may see the USD continue to maintain the initiative over other currencies as major US financial releases are present from Wednesday onwards. In the equities market, the market sentiment seems to have worsened following the disappointing US economic activity and employment data potentially worrying traders of further economic downturn or even a recession. Also, the decline of US yields may provide a cautionary tale to gold traders to be on alert for any possible spikes in the precious metals’ price. The negative correlation of the gold’s price with the USD was greatly visible from space this week with major changes seen in both trading instruments. With the weakening of the USD, we saw gold board a Rocketship to the moon, as US economic data came in lower than expected. It should be noted, that the spike above the psychological threshold of US$2000 per ounce once again, could be indicative that the mentality of traders may be shifting, thus we may see the bulls continue their reign over the precious if US economic data next week continues to be indicative of an economic downturn in the US economy thus may weaken the greenback.

Se tiver alguma dúvida ou comentários sobre este artigo, solicitamos que envie um email diretamente para a nossa equipa de Research através do research_team@ironfx.com

Isenção de responsabilidade:

Esta informação não é considerada como aconselhamento ou recomendação ao investimento, mas apenas como comunicação de marketing. O IronFX não é responsável por quaisquer dados ou pela informação fornecida por terceiros aqui mencionados, ou com links diretos, nesta comunicação.