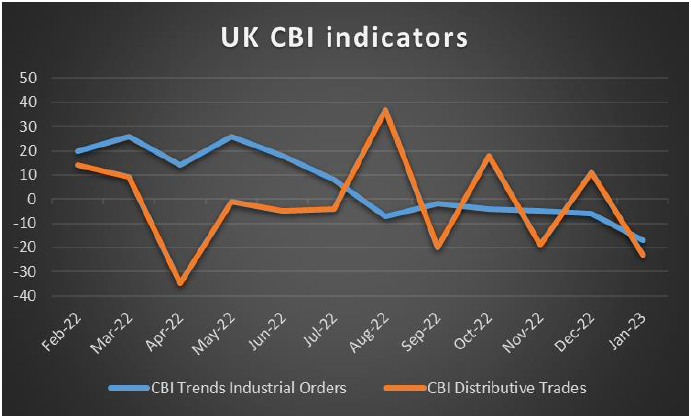

The week is about to end and was full of surprises, yet we open a window at what next week has in store for the markets. On the monetary front, the release of the Fed’s last meeting minutes on Wednesday, are expected to gather substantial interest from traders, while we also note the release of RBA’s February meeting minutes on Tuesday and from Turkey CBT’s interest rate decision on Thursday. As for financial releases we make a start on Monday with Sweden’s CPI rates for January and Eurozone’s preliminary consumer confidence indicator for February. On Tuesday we highlight the release of the preliminary PMI figures of Australia, France, Germany, the Eurozone as a whole, the UK and the US while we also note the release of Germany’s ZEW indicators for February and we highlight Canada’s CPI rates for January, while we also note the release of New Zealand’s trade data for the same month. On Wednesday we note the release of Australia’s wage price index for Q4, and from Germany, we get the Ifo indicators and the preliminary HICP rate, both being for February. On Thursday we note the release of Australia’s capital expenditure growth rate for Q4, UK’s CBI distributive trades indicator for February, Canada’s business barometer for February, the US weekly initial jobless claims figure and highlight the second release of the US GDP rate for Q4. Finally on Friday, we highlight Japan’s CPI rates for January and also note the release of Germany’s forward looking GfK consumer sentiment for March, UK’s CBI trends for industrial orders for February and from the US the consumption rate for January, the Core PCE Price index for the same month and February’s final University of Michigan consumer sentiment indicator.

USD – Fed’s minutes to catch traders’ attention

The USD is about to end the week higher for a fourth week in a row against its counterparts. We highlight that Fed policymakers seem to remain hawkish and Dallas Fed President Logan, Philadelphia Fed President Harker, as well as New York Fed President Williams, made comments showcasing the Fed’s willingness to hike rates further and keep rates at a high level, practically diminishing market hopes for a possible rate cut within the year. We also note that the acceleration of the retail sales growth rate beyond market expectations for January and the fact that inflation rates tended to remain elevated, for the same month, seem to highlight the persistence of inflationary pressures in the US economy. Such rates in conjunction with the stellar employment data for the past month allow if not force the Fed to maintain its hawkishness and embolden the scenario that the terminal interest rate of the bank may be higher than the market’s expectations. Overall, we expect monetary policy fundamentals to play a key role in USD’s direction next week and highlight the release of the Fed’s last meeting minutes. The document once released is expected to be scrutinized by analysts for further clues about the banks’ intentions and we expect a hawkish tone to characterize it. Should that be the case and should also Fed officials maintain a hawkish tone in the statements next week we may see the USD advancing higher.

GBP – Fundamentals to take over

The pound seems to be edging lower for the week against the USD and the EUR but not JPY. In the past few days, the pound’s direction may have been influenced by financial data. We note the release of UK employment data for December, which were viewed as being quite strong, given that the employment change figure rose beyond expectations reaching 74k, while the unemployment rate remained unchanged at 3.7%. Both indicators showcased the tightness of the UK employment market, yet we have to note that the average earnings growth rate slowed down beyond expectations, allowing for the assumption that inflationary pressures in the UK economy are feeding less for wages. Yet that’s understandable given that the headline and core CPI rates for January on a year-on-year level slowed down more than expected, with a drop in petrol and energy prices being possibly responsible. Yet also the PPI rates for January slowed down more than expected, being in line with the relative CPI rates. Overall the release allows for some optimism that BoE’s hawkishness may be allowed to ease by policymakers. Overall we expect in the coming week fundamentals to get into the driver’s seat for the pound’s direction, as the number of high-impact financial releases is reduced.

JPY – CPI rates at the end of the week

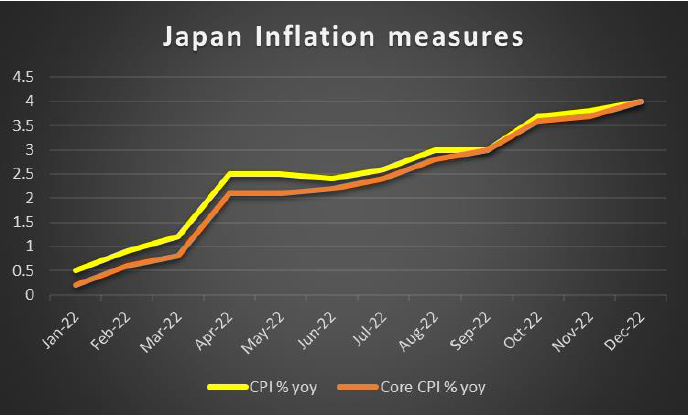

JPY is about to end the week weaker against the USD, EUR and GBP in a sign of a broader weakness. On a macroeconomic level, we note that the machinery orders growth rate got out of the negatives and accelerated, implying that Japanese businesses had the confidence to invest more in the Japanese economy. On the other hand, though we are worried that the trade deficit widened and the export growth rate slowed down, with trade data implying that the country suffered more from its international trading activities. On a monetary level, we note that the Japanese Government on Tuesday nominated Mr. Kazuo Ueda as the next Governor of the Bank of Japan. For the time being, we reiterate that we do not expect any radical overhaul of the bank’s ultra-loose monetary policy, at least not in the current year, some tweaks though are quite possible. Yet we do expect that an exit strategy will start to be drafted and may ultimately lead the bank to its first rate hike. For the time being, we may see the new BoJ Governor maintaining a neutral position and we do consider him more of a centrist. At this point, we would also like to note the appointments of Mr. Shinichi Uchida, a BoJ veteran, who is to provide a detailed knowledge of the easing program so far, as well as Mr. Ryozo Himino, a former Chief Financial regulator with international ties, as Deputy Governors. As for financial releases, we highlight the release of Japan’s CPI rates for January (Headline and Core) on Friday. Both rates are expected to accelerate further and reach 4.0%yoy and if so, add more pressure on BoJ to tweak its dovish monetary policy settings further.

EUR – Preliminary PMI figures to move the common currency

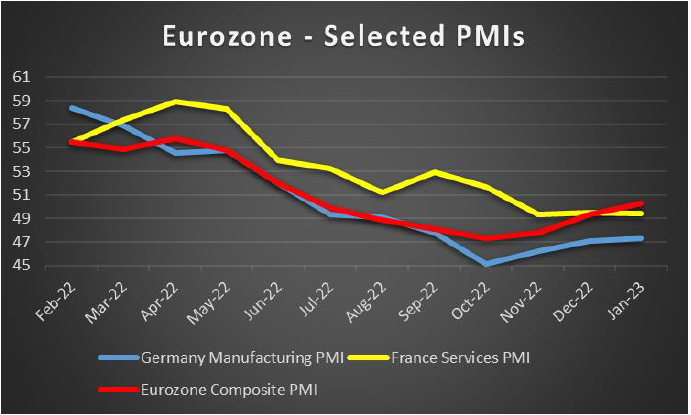

The EUR seems to end the week lower against the USD, yet is gaining against the GBP and JPY. On a macroeconomic level, we note that the second estimate of the GDP rate for Q4 reaffirmed the slowdown from Q1, which is worrying as the economy continues to slide lower, also due to ECB monetary policy tightening. Yet ECB President Christine Lagarde reiterated the bank’s intentions to keep hiking rates in order to tame inflationary pressures in the zone. At this point, we would like to note that Ms. Lagarde singled out wage growth as a potential source of durable inflation. So, overall the hawkish stance of the bank is to remain and could provide some support for the common currency on a monetary level, given its intentions for another 50 basis points rate hike in the March meeting. In the coming week, we highlight the release of the preliminary PMI figures for February, with forecasts for the Zone as a whole implying some improvement in economic activity, as even the contraction expected in the manufacturing sector is to become more narrow. Also, Germany’s ZEW, GfK and Ifo indicators are forecasted to improve which could also provide some support for the EUR, if actually so.

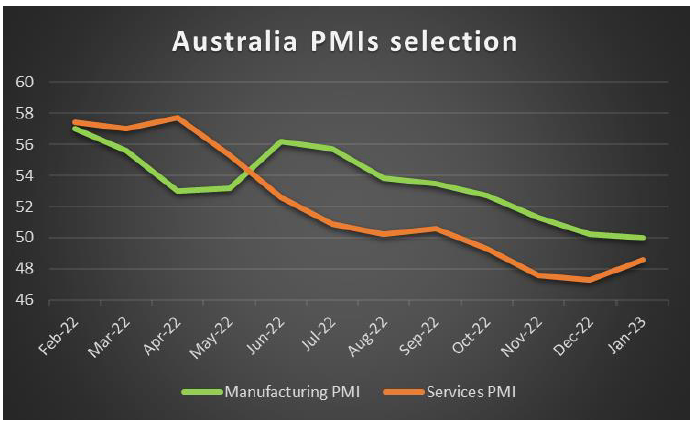

AUD – RBA’s hawkishness to be maintained, for now

The Aussie is about to edge a bit lower against the USD for the week. On a macroeconomic level, we note the release of Australia’s employment data for January. The employment change figure improved, yet failed to get out of the negatives reaching merely -11.5k a far cry lower from the market’s expectations of +20k, while the unemployment rate rose to 3.7%. The release pushed the Aussie lower against the USD, as it highlighted some easing of the tightness of the Australian employment market, which in turn could create some worries in RBA for its monetary policy tightening path. We remind our readers that the bank in its last interest rate decision, had proceeded with a 25 basis points rate hike and warned for more to come. It should be noted that RBA Governor Lowe maintained a hawkish stance before Australian lawmakers in line with the latest interest rate decision. Yet there seems to be increasing political pressure and criticism for RBA’s Governor and the bank’s hawkish stance, which Mr. Lowe for the time being seems to defy. At this point, we note that the release of RBA’s last meeting minutes on Tuesday’s Asian session and Aussie traders and analysts are expected to keep a close eye on the release. We expect the bank’s hawkishness to be maintained and in such a scenario we may see AUD getting some support.

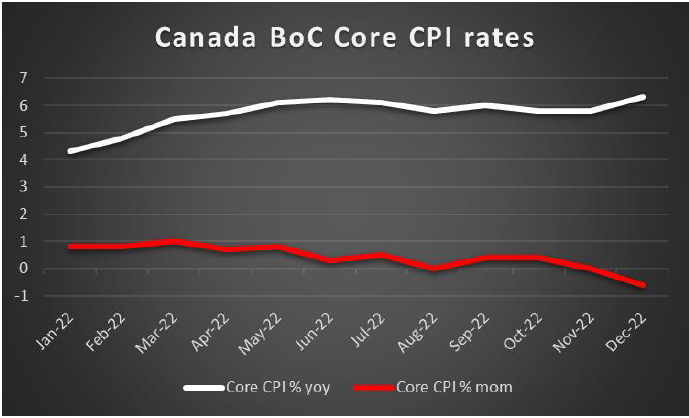

CAD – CPI rates under close watch

The Loonie is about to end the week lower against the USD. We note that on a macroeconomic level, Canada’s employment data for January were better than what the market expected. It was characteristic that the employment change figure, despite being expected to correct lower rose even further reaching a stellar 150k forcing the unemployment rate to remain unchanged at the low levels of 5.0%. The release could be interpreted as a green light for the BoC to maintain its hawkishness. It’s characteristic that BoC Governor Tiff Macklem was reported stating that “The Canadian economy remains overheated and clearly in excess demand, and this continues to put upward pressure on many domestic prices,” before Canadian lawmakers. The statement seemed to leave the possibility of the bank increasing interest rates further on the table. Yet in the coming week, we highlight the release of Canada’s CPI rates which may prove to be one of the main factors behind BoC’s monetary policy. Should the rates accelerate further we may see BoC’s determination to tighten monetary policy further solidifying, and thus could provide some support for the CAD. On a more fundamental level, we note that WTI’s price seems to be edging lower for the week, which may have also contributed to the Loonie’s weakening, given that Canada is a major oil-producing country.

General Comment

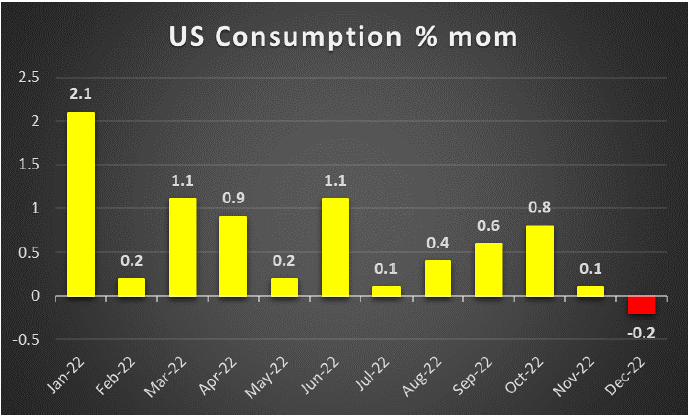

In the big picture and as a closing comment, we see the case for the USD to maintain its dominance over other currencies to the same degree as last week, as the gravity yet not the frequency of US financial releases is to continue and we highlight to that end the release of the Fed’s last meeting minutes on Wednesday and the release of the second estimate of the US GDP rate for Q4. Nevertheless, we note that there are still times at which other currencies may steal the spotlight from the greenback and take the initiative. At this point, we would also like to make a small comment on the movement of US stock markets. US stock markets seem about to end their week by sending mixed signals, maybe with Nasdaq gaining slightly while the Dow Jones, S&P 500 and Nasdaq are slightly lower, yet overall all three indexes do not seem able to get out of their current sideways motion. In the coming week we see the case for the Fed’s intentions regarding its monetary policy to continue to play a key role in their direction, and should the market mood improve further and a more risk-oriented market sentiment surfaces, we may see US stock markets gaining further. Also, the earnings season is still on and we would note the release of the earnings reports of Walmart and Home Depot on Tuesday, of Nvidia on Wednesday and Alibaba and Booking on Thursday. As for gold’s price, we note that the negative correlation with the USD was on display once again, as the strengthening of the USD tended to weaken the shiny metal’s price. We expect that relation to be maintained in the coming week as well and would also like to note that the rise of US yields over the past few days may have also contributed to the weakening of the Gold’s price.

Se tiver alguma dúvida ou comentários sobre este artigo, solicitamos que envie um email diretamente para a nossa equipa de Research através do research_team@ironfx.com

Isenção de responsabilidade:

Esta informação não é considerada como aconselhamento ou recomendação ao investimento, mas apenas como comunicação de marketing. O IronFX não é responsável por quaisquer dados ou pela informação fornecida por terceiros aqui mencionados, ou com links diretos, nesta comunicação.