Market worries for a possible global economic slowdown seem to have intensified in the past week maybe with the US economy being more in the market’s focus. Overall, volatility seemed to remain low and we now open the window to see what the coming week has in store for the markets. On the monetary front, we note from Sweden, Riksbank’s interest rate decision on Thursday. On Wednesday though we also note that Fed Chairman Jerome Powell, ECB President Christine Lagarde and BoE Governor Andrew Bailey are scheduled

to speak at the ECB Forum on Central Banking and could create volatility in the markets. Also other policymakers from around the world are scheduled to speak during the week and could sway the market’s opinion. As for financial releases we make a start on Monday with the US durable goods orders for May and on Tuesday we note the release of Germany’s forward looking GfK Consumer Sentiment for July and the US consumer confidence for June. On Wednesday we note the release of Australia’s retail sales growth rate for May, Eurozone’s business climate for June and the highlight is the release of the final US GDP rate for Q1. On a packed Thursday we get Japan’s preliminary industrial output growth rate for May, China’s NBS manufacturing PMI figure for June, UK’s final GDP rate for Q1, UK’s Nationwide house prices for June, France’s and Germany’s preliminary HICP rate for June, Switzerland’s KOF indicator also for June, Canadas’ GDP rate for April and from the US the weekly initial jobless claims figure as well as the consumption rate for May. On Friday, we get from Japan Q2’s Tankan indexes and Tokyo’s CPI rates, Chinas’ Caixin manufacturing PMI, Eurozone’s preliminary HICP rate and in the American session, from the US the ISM manufacturing PMI figure, all of the releases being for June.

USD– Recession worries intensify

The USD Index seems about to end the week near the same levels it begun on Monday, with some slight losses yet with little volatility. Even Fed Chairman Powell’s testimony before the US Congress was unable to provide support for the greenback. The Fed Chairman largely stuck to the script, providing nothing new which could surprise the markets. Overall Powell reaffirmed the bank’s decisiveness to curb inflationary pressures in the US economy by tightening its monetary policy but was not able to exclude the possibility of a recession. Yet the bank’s path to avoid a recession for the US economy may prove to be a difficult one, given the rate hikes which are on the Fed’s agenda for the coming months. Market worries for a recession in the US economy in the near term are wide and its characteristic that a number of economists and investors are warning that a recession is now more likely than not. That’s why we highlight the release of the final US GDP rate for Q1 on Wednesday. The rate is allready in the negatives according to the preliminary releases at -1.5% and is indicative for the contraction the US economy has suffered in Q1. Before that though, on Monday we note the release of the US durable orders growth rate for May and on Tuesday we note the release of the US consumer confidence indicator for June. On Thursday we get the Fed’s favourite inflation measure, the Core PCE price index and the consumption rate, with both releases being for May as well as the weekly initial jobless claims figure. Finally on Friday’s American session we note the release of the US ISM manufacturing PMI figure for June.

GBP – GDP rates in focus

The pound seems to have remained rather stable against the USD, the EUR and the JPY for the current week. On a macroeconomical level, besides the worries for the shrinking of the UK economy as evidenced by the GDP rates for the months of March and April, we also highlight the release of CPI rates for May which showed that inflationary pressures in the UK economy remain high, as the headline rate ticked up reaching 9.1% yoy. It should be noted that the core CPI rate slowed down though, which would imply that the rise of prices was fuelled by a jump in prices of food and energy. Also we note that the headline rate slowed down on a month on month level, which could imply a relative stabilisation of prices at rather high levels though. Thus we may see stagflation actually looming over the UK economy in the coming months. At the same time we note that BoE had hiked rates in its last meeting in the past week, yet only by 25 basis points which may prove to be insufficient to avert inflationary pressures being ingrained in the UK economy. An additional worry was mentioned by BoE rate setter Catherine Mann, which stated that the weak pound could be a source of imported inflation and that the bank may have to proceed with a faster tightening of its monetary policy. It should be noted that inflation is expected by BoE to remain in the area of 9-10% yoy initially and accelerate to 11% yoy in October. Hence, we highlight the final GPD rates for Q1 on Thursday, which mind you at the preliminary release were at 0.8% qoq and we also note the release of UK’s nationwide house prices for June on the same day.

JPY – Reaching 24 year low levels

JPY is about to end the week slightly stronger against the USD after reaching a new 24 year low level, but remains also relatively stable against the EUR and the GBP. BoJ’s monetary policy tends to weigh on the Japanese currency especially if set in contrast with other central banks that have started or are about to tighten their policies. The bank in its latest interest rate decision last Friday, kept rates unchanged at -0.10% and had mentioned in the accompanying statemnet that “The Bank will purchase a necessary amount of japanese government bonds (JGBs) without setting an upper limit

so that 10-year JGB yields will remain at around zero percent”. Yet the bank’s decisiveness to defend its ultra loose monetary policy and the 0.25% cap for the 10 year government bond of Japan, in order to provide support the Japanese economy, does not pass without criticism. It’s characteristic that a Japanese Government official was reported by Reuters, stating that BoJ’s policy creates a “negative spiral” for the Yen which in turn highlights the need for the bank to tweak its yield cap policy. It should be mentioned though that Japan’s CPI rates remained rather stable for May if compared to April, which may ease somewhat the pressure on BoJ. On a more fundamental level, we note that JPY’s dual nature, as a national currency and a safe haven could be enhanced in the coming week and should the general level of uncertainty in the international markets rise, we may see the Yen getting some support and vice versa. As for financial releases we make a start with the release of the preliminary industrial output growth rate for May on Thursday. On Friday we note the release of Tokyo’s CPI rates for June and highlight the release of the Tankan indexes for Q2.

EUR – Preliminary HICP rates eyed

The common currency is about to end the week with some slight gains against the USD and remains relatively stable against the pound and JPY. On a monetary level ECB’s intentions to hike rates in July by 25 basis points seem to have been reaffirmed in the past few days, yet the width of the September rate hike remains to be seen. Comments made by ECB chief strategist Philip Lane were characteristic as he was reported stating that”I think it’s enough to say that the size of the September increment will reflect our ongoing or evolving assessment, rather than revisit the size of the increment in July,”. At the same time ECB President Lagarde defended the bank’s antifragmentation policy for Eurozone members borrowing costs as she was reported stating “You have to kill it in the bud,”. It should be noted though that our worries for the economic outlook of the Eurozone are still present and actually were enhanced after the preliminary release of the PMI figures for June. It was characteristic that the figures for France and Germany, the two key economies of the zone, but for also the Eurozone as a whole, dropped beyond expectations, implying a wider slowdown of the expansion of economic activity across member states and sectors for the current month. In the coming week we highlight the release of the preliminary HICP rates for June of Germany and France on Thursday and for the Eurozone as a whole on Friday. Should the rates accelerate further, we may see the common currency getting some support, as the pressure on the ECB to tighten its monetary policy more decisively would rise further. Also we would like to note the release of Germany’s forward looking GfK consumer sentiment for July on Tuesday, Eurozone’s Business climate indicator for June on Wednesday as well as Germany’s and the Eurozones’ unemployment rates for June and May respectively on Thursday.

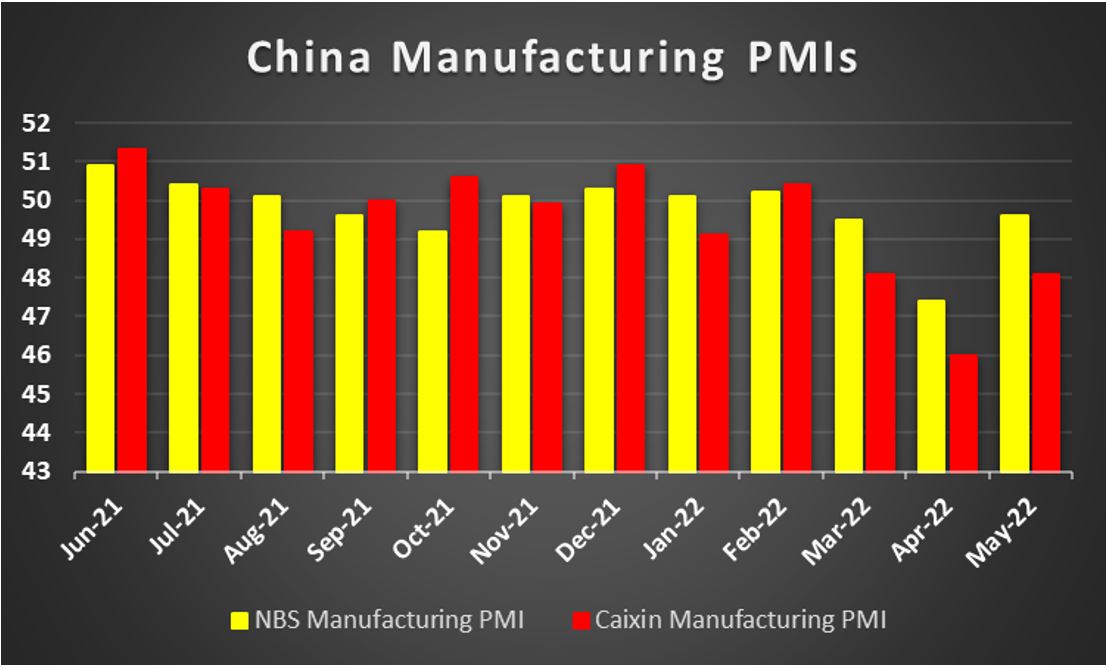

AUD – Chinese data to move the Aussie

AUD is about to end the week at the same levels against the USD as the week begun. On a monetary level it seems that RBA Governor Philip Lowe may have been able to provide some support for the Aussie during Tuesday’s Asian session as he stated that the bank would be considering the possibility of a 50 basis points rate hike in its July meeting. Also the release of the bank’s June meeting minutes showed that “the Australian economy had significant underlying momentum and inflationary pressures were pronounced” while

“members also agreed that further steps would need to be taken to normalise monetary conditions in Australia over the months ahead” which reaffirmed the bank’s hawkish intentions. Yet on a fundamental level as a commodity currency, market worries are intense for a possible global economic slowdown. Keeping this in mind we tend to focus on China as the Australian economy is closely linked to the Chinese economy. Hence, we highlight the release of Chinas’ NBS and Caixin manufacturing PMI figures for June on Thursday and Friday respectively. The indicators’ readings were below the cut-off point of 50 in May, implying a shrinking of economic activity in the crucial manufacturing sector of China and should the readings drop further we may see the Aussie weakening as such results could imply also a shrinking of order books for Australian exporters of raw materials to China. Also on a domestic level we would note the release of Australia’s retail sales growth rate for May due out on Wednesday. Overall, should the market sentiment for the outlook of the global economy turn even more sour, we may see the Aussie weakening further, given its sensitivity as a commodity currency.

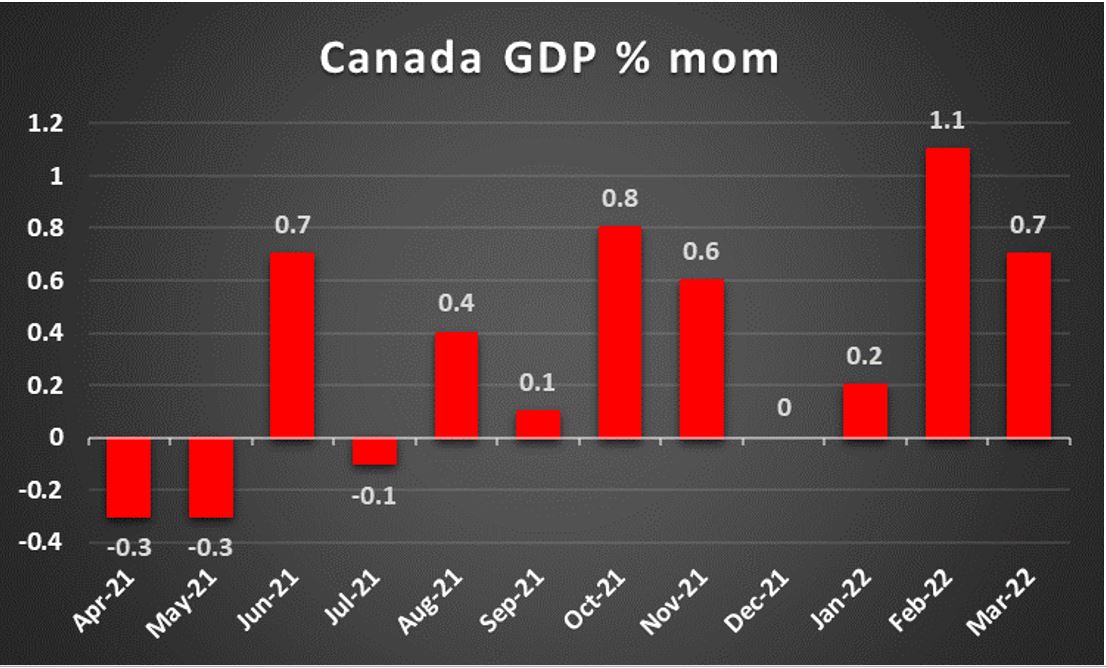

CAD- GDP rates and oil prices to watch out for

The CAD seems about to end the week stronger against the USD after two consecutive weeks of losing ground. It should be noted that on a macroeconomic level, the retail sales of Canada for April accelerated more than expected, providing some support for the Loonie. Also we note that Canada’s CPI rates for May accelerated beyond expectations both at a core as well as an overall level, on a month on month and on a year on year level. The acceleration increased the pressure on Bank of Canada to act more decisively in

regards to the tightening of its monetary policy and to steepen its rate hike path. It’s characteristic that Bank of Canada Deputy Governor Carolyn Rogers stated on Wednesday that inflation in Canada was too high and had not yet peaked, adding “it’s keeping us up at night”. On the other hand though CAD bulls may have calmed somewhat in the past days as oil prices continued to drop substantially with WTI prices at some point dropping below $103 per barrel. The extensive market worries for a possible recession and the

possible adverse effect on the demand side of the oil market practically victimised oil prices. Given that Canada is a major oil producing economy, its’ understandable that a possible further drop of oil prices could also have an adverse effect on the Loonie as well. Also the nature of the CAD as a commodity currency tends to make it sensitive also the global economic outlook. As for financial releases in the coming week, we highlight the release of April’s GDP rate on Thursday and should the rate slow down we may see the CAD slipping at the prospect of a slower growth for Canada’s economy.

General Comment

As a closure, we would like to note that we expect the USD to regain some of the initiative over other currencies, given the accelerating frequency and increased gravity of US financial releases in the coming week, probably also seeing some increased volatility. On the other hand, certain currencies may come under increased volatility and move independently at certain points in the coming week. For example, the common currency at the release of Germany’s , France’s and the Eurozone’s preliminary HICP rates for June. We would like to make a small comment though also for Riksbank’s interest rate decision on Thursday. The bank is expected to hike rates by 25 basis points raising the interest rate from 0.25% to 0.50%. It’s characteristic that SEK OIS imply that the market has fully priced in the rate hike hence it may take more than a simple rate hike for the SEK to get some substantial support. Should the bank actually hike rates as expected and also issue a statement with a rather hawkish tone, we may see the Krona strengthening. It should be noted that CPI rates for May took the markets by surprise as they accelerated beyond market’s expectations, thus increasing the pressure on the bank to tighten its monetary policy. On the other hand we must note that

Sweden’s GDP rate for Q1 on a quarter on quarter level dropped into the negatives which may be advising some caution. As a sidenote for the bank we would also like to mention that Erik Thedeen has been

appointed as the new governor for Riksbank yet is to assume office from January 1st which provides a substantial amount of time. On the equities front, we would note the rise of the main indexes of the US stockmarkets for the week, as they were trying to recover some of the lost ground. On the other hand it should be mentioned that gold’s price tended to present low volatility, maybe also reflecting USD’s lack of activity. Overall though we maintain the view for the precious metal’s negative corelation with the USD, which could be in display once again in the coming week.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.