The week is drawing to a close, and as usual, we open the door to see what next week has in store for the markets. Starting on Monday, we note China’s urban investment rate, industrial output and retail sales rate followed by the US retail sales rate all for the month of February. On Tuesday, we note Germany’s ZEW economic sentiment figure for March, Canada’s CPI rates and the US industrial production rate all for February and ending the day with New Zealand’s current account figure for Q4. On Wednesday we note the BOJ’s interest rate decision, Japan’s machinery orders rate for January and trade balance figure for February, followed by the Zone’s final HICP rate for February, the highlight of the week which if the Fed’s interest rate decision and New Zealand’s GDP rate for Q4. On Thursday, we get Australia’s employment data for February, China’s loan prime rate , the UK’s employment data for January, the SNB’s, Riskbank’s and the BoE’s interest rate decisions followed by the US weekly initial jobless claims figure, the US Philly Fed Business index for March, Canada’s producer prices rate for February and New Zealand’s trade balance figure for February. On Friday we note Japan’s CPI rates for February, Canada’s retail sales rate for January and the Zone’s preliminary consumer confidence figure for March.

USD – Fed decision week

On a monetary level, the Fed’s interest rate decision is set to occur on Wednesday. Economists are currently anticipating the Fed to remain on hold, with FFF implying a 97% probability for such a scenario to materialize. Thus, our attention turns to the bank’s accompanying statement in addition to Fed Chair Powell’s press conference following the bank’s decision. Specifically, the possible remarks and comments in regards to the US’s ongoing trade wars and the Fed’s outlook on the economy as a result of the tariffs. In turn should the Fed imply that they may cut rates before June which is the current expectation, then it could weigh on the dollar. On the other hand, should the Fed imply that the risks to inflation have increased due to the trade wars and thus imply that the Fed may remain on hold for a prolonged period then it may aid the dollar.

• On a fundamental level, US President Trump’s tariffs are resulting in retaliatory measures from the affected nations. Specifically, Canada announced C$29.8 bln in retaliatory tariffs on the United States on Wednesday in response to U.S. President Donald Trump’s steel and aluminum tariffs with the EU also announcing that it has launched the process to impose additional countermeasures on the US, which will target roughly €18 billion worth of goods. The EU’s actions have sparked the ire of the US President with Trump announcing that if the tariffs are not revoked immediately the US will retaliate. The imposition of tariffs and trade wars appears to have enhanced the uncertainty of the global economic outlook.

Analyst’s opinion (USD)

“The Fed’s decision is crucial. The Fed remaining on hold is all but priced into the markets and thus heightened volatility may occur during Powel’s presser and the Fed’s accompanying statement. The CPI rates for February may have showcased easing inflationary pressures but the ongoing trade wars risk reversing that progress. Hence, we would not be surprised to see the Fed pushing back against any commitment to cutting rates in the near future. On the other hand the unemployment rate ticked upwards from 4.0% to 4.1% which is also a concern for the Fed. Nonetheless, the main issue is still the tariffs, it’s an ever changing landscape with tariffs being imposed and reverted on a day-to-day basis at this point”

GBP – BoE decision to occur next week

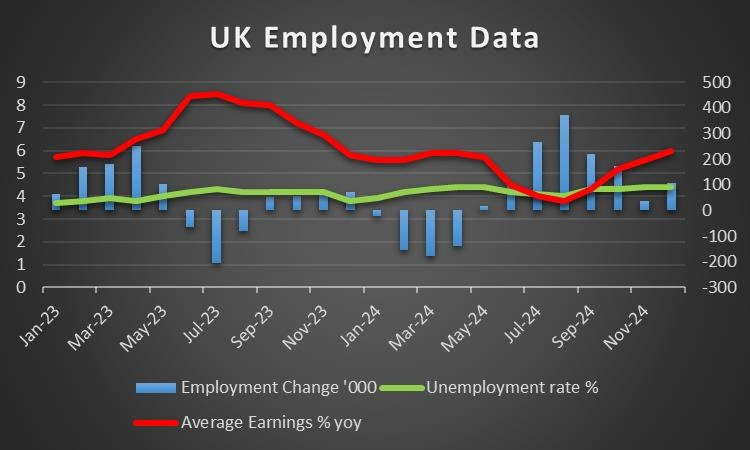

On a monetary level, the BoE’s interest rate decision is set to occur on Thursday. The majority of market participants are currently anticipating the bank to remain on hold with GBP OIS currently implying a 91.4% probability for such a scenario to materialize. Therefore, we would turn our attention to the bank’s accompanying statement in order to gain greater insight into the bank’s forward guidance. Specifically, should the bank imply that they may cute rates in their next meeting as is currently implied by GBP OIS, it may weigh on the pound. However, should they indicate that they may wish to remain on hold it could instead aid the GBP.

• On a macro-economic level, we note that the UK’s employment data for January is set to be released on Thursday which tends to coincide with the BoE’s decision. Therefore, the release of the UK’s employment data could play a role in the direction of the pound prior to the decision. Hence, should the employment data showcase a loosening labour market, it could weigh on the sterling. However, should the employment data showcase a resilient labour market, it could instead aid the pound.

Analyst’s opinion (GBP)

“The UK may suddenly find itself in trouble given that the tariffs imposed by the US also impact the UK’s steel exports to the US. Therefore, the picture for the UK’s economy remains muddy for the time being. In other news, of interest is of course the BoE’s decision where the bank is expected to remain on hold. In our view, we wouldn’t be surprised to see a nod from policymakers for a possible rate cut in their next meeting ”

JPY – BOJ decision on Wednesday

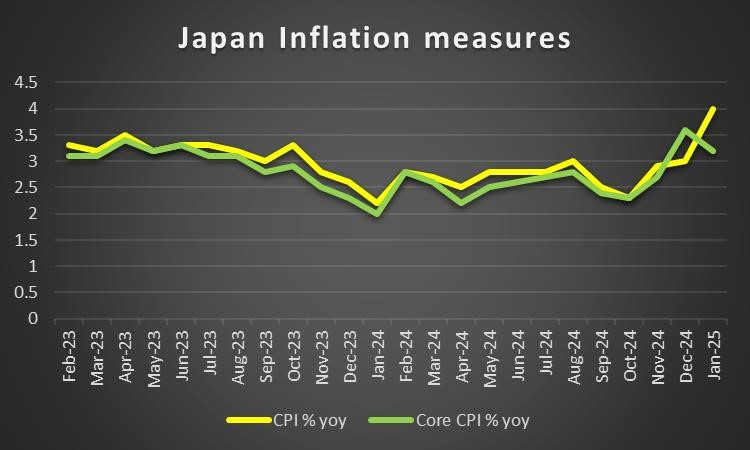

On a macroeconomic level, of interest this week was Japan’s GDP rate on a quarter-on-quarter basis for Q4 which was released on Tuesday. The GDP rates may have disappointed Yen traders as they came in lower than expected at 0.6% versus 0.7% yet when compared to the prior quarter’s rate of 0.3% it is still a welcome improvement. For next week we would like to note the release of Japan’s CPI rates for February, which are set to be released on Friday. Should the CPI rates showcase an acceleration of inflationary pressures it may aid the Yen, as pressure may mount on the BOJ to hike rates in their next meeting. On the other hand, should the CPI rates remain steady or showcase easing inflationary pressures, then it could weigh on the JPY as the bank may remain on hold for a prolonged period of time.

That being said, on a monetary level the highlight for Yen traders might be the BOJ’s interest rate decision on Wednesday in which the bank is widely expected by economists to remain on hold at 0.5%. In particular, JPY OIS currently implies a 91.6% probability for such a scenario to materialize. Hence, we would also turn our attention to the bank’s accompanying statement for clues into as to how the bank may proceed in the future. In particular, we would like to point out that the bank is expected to remain on hold up until their July meeting, where JPY OIS currently implies a 42.6% probability for the bank to hike rates by 25 basis points. That being said, whether or not the bank hikes rates or not is currently a coin flip per JPY OIS with a 40.1% probability being attributed to the bank remaining on hold. Therefore, should the bank’s accompanying statement imply that the bank may hike in the near future it could aid the JPY and vice versa.

Analyst’s opinion (JPY)

“We tend to highlight BoJ’s decision as the main event for Yen traders in the coming week. We wouldn’t be surprised to see the bank remaining on hold. However, the CPI rates which are due out on Friday could easily change the picture. ”

EUR – EU retaliates against the US

The EU has announced that it has launched the process to impose additional countermeasures on the US, which will target roughly €26 billion worth of goods. According to the Commission’s press release “in response to new US tariffs affecting more than €18 billion of EU exports, the Commission is putting forward a package of new countermeasures on US exports. They will come into force by mid- April, following consultation of Member States and stakeholders.” Moreover, Comission President Ursula Von Der Leyen stated that “The countermeasures we take today are strong but proportionate” and that the EU in the meantime “will always remain open to negotiation”. The ongoing trade war may be of concern to the growth narrative in the EU, yet it appears that they are willing to negotiate. However, despite the tariffs being relatively proportional in nature, President Trump on Thursday threatened the EU with a 200% tariff on alcohol products. In conclusion, the trade war may be only just beginning and thus could have severe consequences both for the EU and the US down the line.

On a monetary level, ECB President Lagarde’s comments earlier on this week may have aided the common currency. Specifically ECB President Lagarde warned that the trade war involving the US “might feed into inflation more directly and increase volatility” and that the ECB “cannot provide certainty” in regards to the way forward. The comments made by ECB President Lagarde may imply that the bank could be preparing for a period of high volatility with potential fluctuations in inflation in the Zone. In turn, this may further imply that the bank could adopt a wait and see approach and thus could cut rates further down the line. Such a scenario may have aided the EUR, yet should financial releases stemming from the Zone imply that the economic situation may be taking a turn for the worse, it could force their hand.

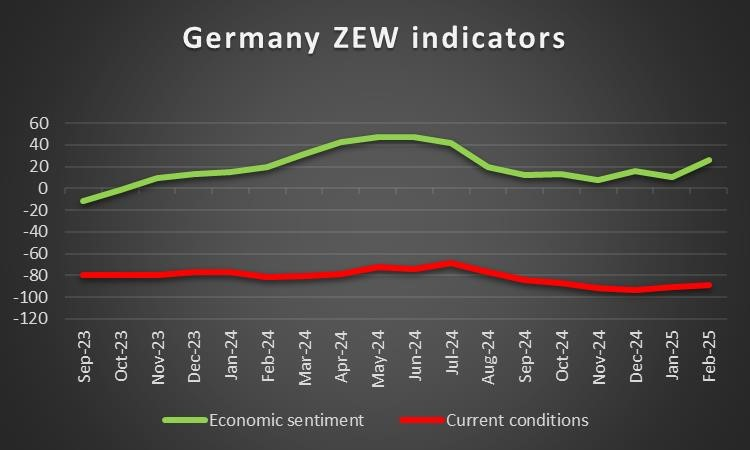

On a macroeconomic level we note that Germany’s ZEW economic sentiment figure for March is due out Tuesday. The financial release is considered to be a barometer for consumer spending in Germany and thus the financial release may be crucial and could influence the EUR’s direction. Therefore should we see an improvement in the figure, it may imply consumer confidence in the economy has increased and could thus result into increased consumer spending which may aid the EUR. On the other hand a figure lower than the prior reading of 26, may imply that consumer confidence has decreased and may thus imply a reduction in consumer spending which in turn could weigh on the EUR.

Analyst’s opinion (EUR)

“EUR traders may be kept on the edge of their seats, as the EU Commission gears up for their trade war with the US. The proposal of tariffs on the US has resulted in President Trump announcing a possible 200% tariff on alcohol imported from the EU.”

AUD – Employment data next week

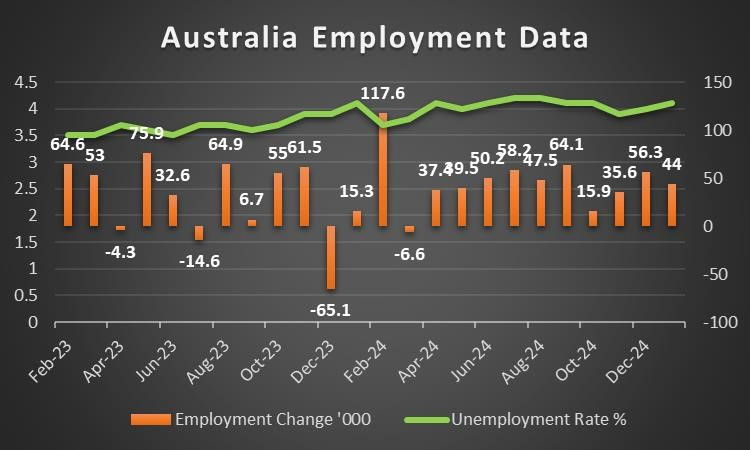

• On a monetary level and macroeconomic level, it was a pretty easy going week for Aussie traders with no major financial releases stemming from the country. However, next week interest may pick up for the Aussie with the nation’s employment data for February being released on Thursday the 200th of March. The prior employment change figure came in at 44k, with the unemployment rate coming in at 4.1%, therefore a figure higher than 44k and an unemployment rate lower than 4.1% could imply a resilient labour market in Australia which in turn could boost the Aussie. On the flip side a figure lower than 44k and an unemployment rate higher than 4.1% could imply a loosening labour market which may weigh on the AUD.

Fundamentally, the Aussie could be influenced by the release of China’s industrial output rate for February which is set to be released on Monday. Given the close socio-economic ties between Australia and China, the industrial output rate may play a role in the direction of the Aussie at least during Monday’s trading session. Economists are currently anticipating the rate to decrease from 6.2% to 5.4% which may imply a reduction in industrial output and thus possibly a reduction in demand for raw materials from Australia and hence a reduction in demand for the AUD. However, should the rate exceed expectations it may instead aid the AUD.

Analyst’s opinion (AUD)

“Overall, given the low number of high-impact financial releases from Australia in the coming week, Aussie traders may focus on the fundamentals. Moreover, financial releases from China could also influence the Aussie.”

CAD – BoC cuts rates by 25 basis points

On a political level, we note that Canada’s ruling party the Liber party has announced that Mark Carney has won the race to succeed Justin Trudeau as Canada’s prime minister. The shift is indicative of the changing geopolitical landscape in Canada and with Trump’s recent attacks on the nation, the Liberal’s now have a chance, according to the polls, to win once again, a scenario which seemed impossible just a month ago.

On a monetary level, we note that the Bank of Canada cut rates by 25 basis points as it was widely expected. The bank in its accompanying statement stated that “The Canadian economy entered 2025 in a solid position, with inflation close to the 2% target and robust GDP growth” which could be imply that the bank’s monetary policy decisions are bearing fruit. Yet, as we had expected the bank noted that “heightened trade tensions and tariffs imposed by the United States will likely slow the pace of economic activity and increase inflationary pressures in Canada”. Essentially implying that the bank may be concerned about the return of inflationary pressures. Hence, it may imply that the bank may ‘pause’ its rate-cutting path, which in turn could aid the CAD.

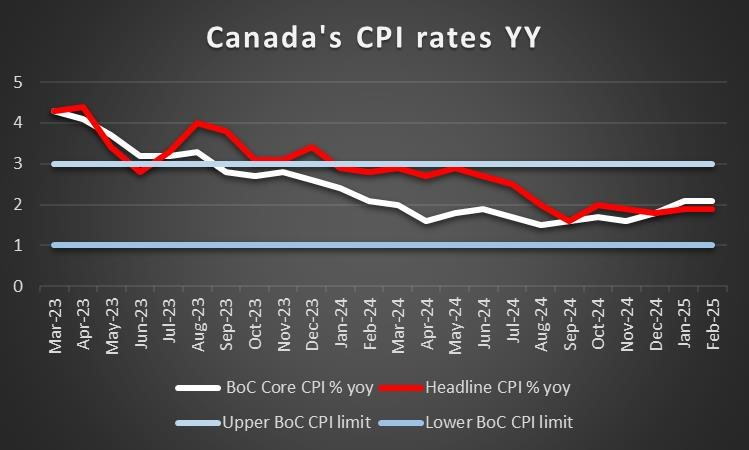

On a macrolevel we highlight the release of Canada’s February inflation print on Tuesday. Should the CPI rates come in lower than the prior readings it could allow the bank to continue cutting rates which in turn could weigh on the CAD. However, should the CPI rates remain near the 2% or come in higher than the prior readings it could allow the bank to remain on hold for a prolonged period of time which in turn could aid the Loonie.

Analyst’s opinion (CAD)

“Loonie traders may see themselves in a period of great uncertainty. The ongoing trade war with the US may raise concern about the return of inflation to the Canadian economy. Moreover, as seen during this week the situation is changing by the day, with tariffs being proposed then revoked. The CPI rates next week, should they remain at 2% could allow the Bank to remain on hold until the resolution or greater clarity on the impact of tariffs on the economy.”

General Comment

As a closing comment, we expect the USD to maintain the initiative in the FX market in the coming week given the Fed’s interest rate decision and President Trump’s frequent announcements in regards to tariffs.. As for US Equities markets the mayhem continues we note the continued drops of all three major equity indexes in the US, namely the Dow Jones, S&P 500 and Nasdaq. As for gold’s price, the precious metal has soared to new all time highs, with the precious metal’s price reaching $3000 per troy ounce. On a political level, heightened uncertainty may exist as the US Government could potentially ‘shut-down’ by the end of the day.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.