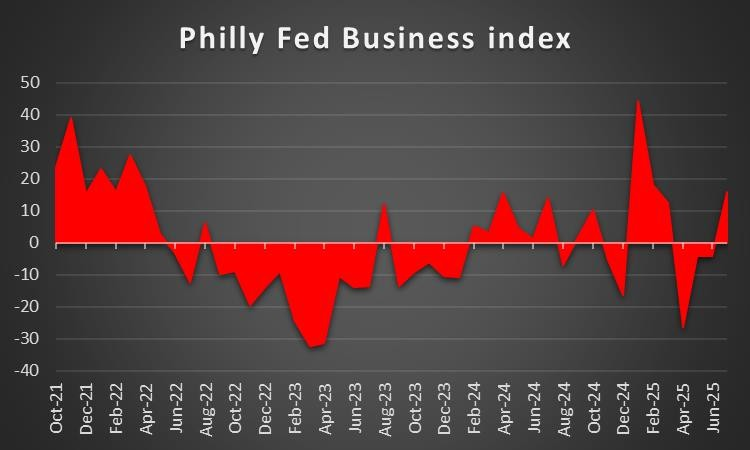

The week is nearing its end and we have a look at what next week has in store for the markets. On Monday we get Japan’s chain store sales for July and on Tuesday we get Canada’s CPI rates for the same month. On Wednesday we note the release of Japan’s machinery orders for June and trade data for July, from China we get PBoC’s interest rate decision from New Zealand RBNZ’s interest rate decision, UK’s CPI rates for July, Euro Zone’s final HICP rates for July and the Fed releases the minutes of the July meeting. On a busy Thursday, we get New Zealand’s trade data, Australia’s, Japan’s, Germany’s, France’s, Euro Zone’s and the UK’s preliminary PMI figures for August, UK’s CBI trends for August, Canada’s business barometer for August and producer prices for July and from the US, the weekly initial jobless claims figure and Philly Fed business index for August. On Friday we get Japan’s CPI rates for July and the UK retail sales also for July and Canada’s retail sales for June.

USD – Fed’s meeting minutes in sight

On a monetary level, the market’s expectations for the Fed to ease its monetary policy were considerably amplified. It’s characteristic that Fed Fund Futures (FFF) now imply a 92.7% probability for the bank to cut rates by 25 basis points in its next meeting, and the rest implies that a 50 basis points rate cut is also possible. Hence, the message conveyed by FFF is that the market no longer considers whether the bank will cut rates or not, but by how much. Also, the rhetoric of Fed policymakers has turned more dovish since the release of weak employment data for July, but also the substantial downward revisions of the NFP figure for June and May implied fast, deteriorating conditions in the US labour market. At the same time, inflationary pressures tend to remain resilient, but Trump’s tariffs do not seem to have elevated consumer prices in a meaningful way yet. On the other hand the release of the US PPI rates for July showed considerable acceleration implying that importers suffered a considerable increase in prices, which could be rolled over to consumers in the coming months. Lastly, there is always political pressure from the US Government and US President Trump personally, for the bank to ease its monetary policy. In a latest development, US Treasury Secretary Scott Bessent yesterday called for a “series of rate cuts,” and also stated that the US Central Bank could begin its rate-cutting path with a double rate cut in the September meeting. We highlight the release of the Fed’s meeting minutes on Wednesday as the document may provide more clarification for the Fed’s intentions. On a fundamental level, Trump’s tariff wars are ongoing and on a fundamental level, we focus today’s meeting with Russian President Putin. Over the past week, media had highlighted the possibility of a deal under which Ukrainian territory could be given to Russia in exchange for peace. Yet White House officials have downplayed the possibility of such a scenario and its characteristic that they regard the meeting more like a “listening exercise” for the US President. Also the notion of a second meeting emerged, after a short while, hence today’s meeting is expected to be of a preparatory nature to see if the two sides actually agree on what is to happen and should an agreement be reached, then Ukraine and possibly the Europeans will be invited. At the current stage we see the case for Russia to have little incentive for a peace treaty and may prefer to play hardball. On the other hand the US President seems to be allready hardening his positions, yet the media report that Trump told Ukrainian President Zelensky, that he will not discuss territory divisions with Putin. On the flip side the Russian President Putin has initiated a charm offensive, and seems to see the Ukraine issue as one among others, possibly seeking a wider agreement on a range of issues in the US-Russian relationships. On the other hand, rumours are being spread that the US President may offer Russian access to rare earths and an easing of sanctions of Russian oil exports to get a ceasefire, a scenario that seems more plausible. Should the meeting result in a thawing of tensions in the US-Russian relationships, we may see the USD getting some support, while should the summit result in a failure we may see it weighing on the USD.

Analyst’s opinion (USD)

“For the time being fundamentals, monetary policy and financial data seem to align in showing more USD weakness in the coming week.”

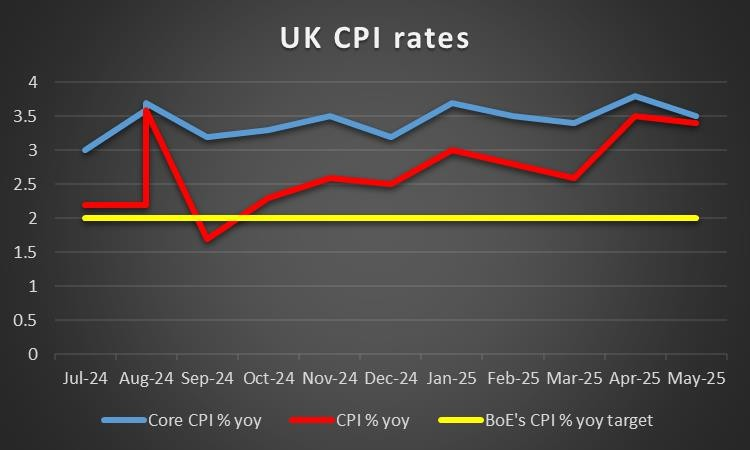

GBP – UK’s July CPI rates on the horizon

On a macroeconomic level, we had some good news for the pound. We make a start with the UK employment data for June, which that the unemployment rate remained unchanged at 4.7%, while the employment change figure rose to a stellar 238k, widely surpassing market expectations, and providing a tightening tone to the UK employment market which is a positive. Yet the main release for the week, may have been the preliminary GDP rates for Q2. The rates both on a qoq and a yoy level, slowed down less than expected, signalling a relative resilience of the UK economy. It should be noted that the less-than-expected slowdown of the GDP rates was also accompanied by an acceleration of the manufacturing and industrial output and the services indicator, all being for June. Thus the release tended to improve the macroeconomic outlook of the UK thus providing some support for the pound. In the coming week, we highlight the release of the UK’s July CPI rates. May we remind our readers that the Bank of England (BoE) expects the CPI rates to accelerate before slowing down and should such a scenario be materialised on Wednesday, we may see the pound getting some support. Also on a macro level, we may see the release of the preliminary PMI figures for August, being a market mover for the pound, with special focus being on the services sector reading. Should we see a rise in the indicator’s reading we may see the sterling getting some support as it would imply a faster expansion of economic activity in the key UK services sector. On a monetary level, we note the market’s expectations for the BoE to deliver another rate cut in the December meeting. The market expectations are characteristic of a possible pause in the bank’s rate cutting path which could provide some support for the GBP. The picture on a political level for pound traders has not changed fundamentally. The UK government seems to maintain its fiscal tightness with a £41 billion black hole needs to be covered. For the time being any tax changes may have to wait until UK Chancellor of the Exchequer Reeves delivers her Autumn budget. For the time being we may see UK politics continuing to weigh on the pound somewhat.

Analyst’s opinion (GBP)

“we continue to view financial releases as the primary factor behind the GBP’s direction in the coming week. A possible acceleration of the July CPI rates could provide additional support for the pound. Market expectations for BoE’s intentions and the UK government’s fiscal tightness continue to be important yet in the coming week, may remain in the background.”

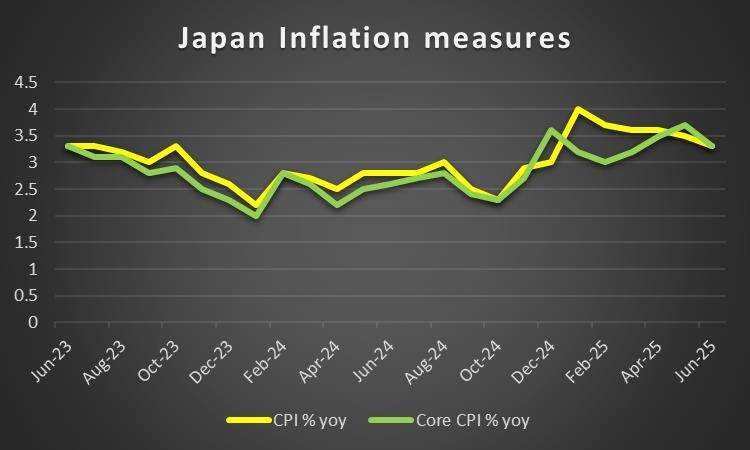

JPY – Japan’s July CPI rates in focus

For JPY traders on a macroeconomic level, we highlight the release of Japan’s preliminary GDP rates for Q2 in today’s Asian session, the rates accelerated beyond market expectations showing growth again for the Japanese economy and removing the spectre of a recession at the current stage. In the coming week, we highlight the release of Japan’s CPI rates for July on Friday. The release gains on importance as BoJ considers inflation as critical in regards to its rate hiking intentions. Should we see the rates accelerating implying further resilience of inflationary pressures in the Japanese economy, we may see the JPY getting some support. Yet a possible slowdown of the rates could weigh on the JPY as the market’s hawkish expectations may ease. For the time being we note that the market expects the bank to deliver a rate hike in the December meeting. The comments of US Treasury Secretary Bessent on Wednesday about how BoJ have gotten “behind the curve” by postponing any rate hikes, a sense that we share. Overall should we see the market’s expectations for BoJ intensifying we may see the JPY getting some support and vice versa. On a fundamental level, we cannot underestimate JPY’s safe haven qualities, and a possible easing of the market’s worries on a fundamental level, may weigh on the Yen.

Analyst’s opinion (JPY)

“We see the case for the release of Japan’s July CPI rates to be closely watched by JPY traders next Friday and a possible acceleration of the rates could provide some support for the Yen. On a monetary level, the slightly hawkish expectations for BoJ may keep the JPY supported, yet an easing of the market’s levels on a global level, could weigh fundamentally on JPY.”

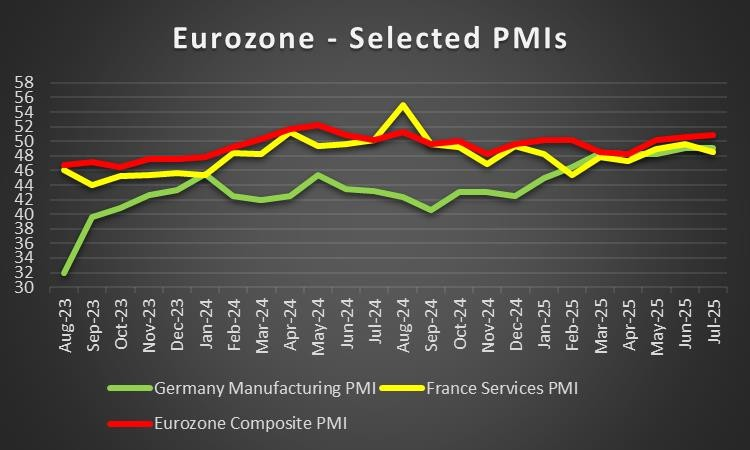

EUR – Preliminary August PMIs in the epicenter

On a fundamental level, EUR traders are expected to keep a close eye on the meeting of US President Trump with Russian President Putin later today. Should the meeting be a success, depending always on the content, possibly reaching a ceasefire in the Russian Ukrainian front, the EUR may be able to enjoy some support on a fundamental level, as its southeastern flank may temporarily calm down. On a monetary level, the market’s expectations are for the bank to remain on hold beyond year’s end, until early spring 25, in a clear sign that it tends to lean on the hawkish side. Given the summer lull in Europe, we expect few announcements if any from the ECB, yet should the market’s expectations for the bank to maintain rates for longer be enhanced we may see the EUR getting some support. On a macroeconomic level, we note the release of Euro Zone’s final HICP rate for July on Wednesday, yet little change is expected if any, from the preliminary release’s 2.0%yy. The highlight of the coming week for EUR traders is expected to be the release of the preliminary PMI figures for August, with special interest being set on indicator of Germany’s manufacturing sector, but also France’s services sector and Euro Zone’s composite index. A possible improvement of the indicators’ readings could imply some expansion of economic activity in the zone which in turn could provide some support for the common currency and vice versa.

Analyst’s opinion (EUR)

“On a fundamental level, we highlight the Trump-Putin meeting as a possible high-risk event for the single currency’s direction, yet in the coming week, we may see the release of the preliminary PMI figures could enhance volatility for EUR pairs.”

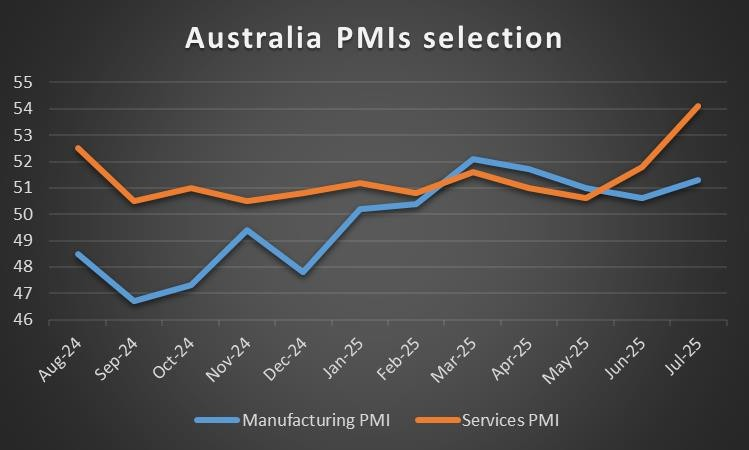

AUD – Fundamentals to lead the Aussie

In the coming week on a macroeconomic level, we note for Aussie traders the release of the preliminary PMI figures for August with some increased focus possibly being set on the manufacturing sector. A possible rise of the indicators’ readings could provide some support AUD as it would signal a faster expansion of economic activity in Australia. Yet other hence, that the Australian calendar is pretty empty of high impact financial releases, hence, we expect fundamentals to lead the Aussie. On a monetary level, the release of Australia’s employment data for July, highlighted a relative tightness of the Australian labour market, as the unemployment rate ticked down to 47.2% and the employment change figure rose to 24.5k, both readings being largely expected. Yet the release seemed to give RBA some breathing space as it eased the pressure to continue its rate cutting path. It’s characteristic that in its latest interest rate decision, Australia’s central bank highlighted inflation and employment as two key sectors to watch out for, in deciding its monetary policy. Currently the market seems to expect the bank to remain on hold in its September meeting and proceed with a rate cut in November the last for the year. Should such market expectations be maintained or even be enhanced, we may see the Aussie being supported on a monetary level in the coming week. On a fundamental level we note the close Sino Australian economic ties, as a possible factor affecting AUD’s direction. The latest macroeconomic developments in China with the Urban investment, retail sales and industrial output growth rates for July slowing down beyond market expectations, tend to bet worrying for macroeconomic outlook of China showing aa substantial easing of economic activity for both the production and demand side of the Chinese economy. On an even deeper fundamental level, and given that the Aussie is considered a commodity currency and a riskier asset in the FX market, should market worries for US President Trump’s tariff wars ease further, we may see the Aussie getting some support and vice versa.

Analyst’s opinion (AUD)

“In the coming week we expect the Aussie to be primarily being led by fundamentals given the low number of high impact financial releases from Australia on the calendar. Should the risk sentiment in the markets grow we may see the AUD getting some support and vice versa.”

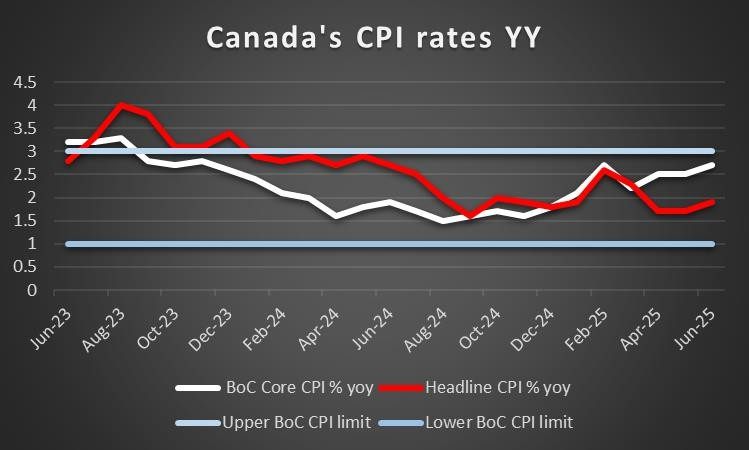

CAD – July’s CPI rates under the limelight

Loonie traders are expected to be quite busy in the coming week on a macroeconomic level. On Tuesday we get Canada’s CPI rates for July. A possible acceleration on a headline and core level of the CPI rates could add more pressure on the BoC to remain on hold in its next meeting and as such provide some support for the Loonie. It should be noted that July’s employment data tended to weigh on the CAD as despite the unemployment rate remaining unchanged at 6.9%, the employment change figure dropped deep into the negatives reaching -40.8k, creating some worries for the conditions in the Canadian employment market. Coming Thursday we note the release of Canada’s business barometer, which “shyly” remained above the cut off point of 50 for the month of July, implying more optimism for the outlook of the Canadian economy. Should the indicator’s reading drop below 50 for the month of August, we may see the Loonie slipping. Lastly on Friday we get the retail sales growth rate for June, which is in the negatives for the month of May signalling a contraction of retail sales, should the rate dive even deeper into the negatives, it could be spelling trouble for the demand side of the Canadian economy. On a monetary level, we note the market’s current expectations for BoC to remain on hold until December and deliver a rate cut just before the year ends. Should we see the market in the coming week, intensifying its expectations for a further delay of an interest rate cut by the BoC, we may see the Loonie losing ground in the FX market. On a fundamental level, the fallout of reaching a trade deal with the US continues to weigh fundamentally on the Loonie, yet the market may slowly be digesting it. Yet a high number of items exported from Canada to the US remains tariff free given that they fall under CUSMA (Canada US Mexico Agreement). Nevertheless Canada is now trying to bolster its trade relationships with Mexico which could provide some support for the Loonie. Also we note the downward direction of oil prices as a factor which could weigh fundamentally on the Loonie, should be extended in the coming week, given Canada’s status as a major oil producer

Analyst’s opinion (CAD)

“In the coming week we expect financial releases to lead the Loonie, with the release of the July CPI rates being particularly watched. A possible acceleration of the rates could provide some support for the CAD.”

General Comment

In the coming week, we expect the USD to ease its influence in the FX market given that the number and gravity of high impact financial releases is to be reduced. That could allow for other currencies to get the initiative and come under the spotlight, thus creating an even more balanced trading mix in the FX market. Also in the FX market, we note the release of New Zealand’s RBNZ interest rate decision next Wednesday. The bank is widely expected to cut rates by 25 basis points lowering rates to 3.00% from current 3.25%. yet for the Kiwi to drop a rate cut may not be sufficient. The market besides a rate cut next Wednesday seems to be pricing in another rate cut in the November meeting. Hence should the bank cut rates as expected and proceed to issue a forward guidance that will be leaning on the dovish side we may see the Kiwi slipping. Yet should the bank fail to express some dovish tendencies, possibly also hesitating for further easing of its monetary policy we may see NZD getting some substantial support as the markets could be taken by surprise and be forced to readjust their expectations. As for US stockmarkets, their upward direction seems to be maintained implying a relative optimism and a more risk oriented approach by the market but also tends to bear witness for the AI frenzy among investors in US equities. As for earnings reports we note in the coming week the releases of BHP on Monday and Xiaomi on Tuesday, while for the retail sector we note the releases of the earnings reports of Home Depot and Walmart on Tuesday and Thursday respectively. As for gold’s price we note that its sideways motion seems to continue, despite the USD Index moving up and down. Overall we tend to view the negative correlation of the two trading instruments as being currently inactive, which allows gold to remain relatively stable, possibly in a sign of a wait and see position of gold traders.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.