After a rather easy-going week, we open a window in what next week has in store for the markets. On the monetary front, we highlight the release of the Fed’s interest rate decision on Wednesday, yet also ECB’s and BoJ’s interest rate decisions on Thursday and Friday respectively are expected to gather substantial interest among traders. But it’s expected to be an exciting week also due to the release of a number of high-impact financial data. On Monday we make an early start with New Zealand’s trade data for June and continue with the preliminary PMI figures for July of Australia, Japan, France, Germany the Eurozone as a whole, the UK and the US. On Tuesday we note the release of Germany’s Ifo indicators for July, UK’s CBI trends for industrial orders and the US consumer confidence for July. On Wednesday we get Australia’s CPI rates for Q2 and on Thursday, we get Germany’s forward-looking Gfk Consumer sentiment for August, UK’s CBI distributive trades for July and from the US we highlight the release of the preliminary GDP advance rate for Q2 and not the release of June’s durable goods orders as well as the weekly initial jobless claims figure. On Friday we make a start with Japan’s Tokyo CPI rates for July, Australia’s final retail sales for June, France’s preliminary GDP rate for Q2, France’s and Germany’s preliminary HICP rates for July, Switzerland’s KOF indicator for July, Canada’s GDP rate for May and from the US we note the release of June’s consumption rate and Core PCE price index as well as the final University of Michigan consumer sentiment for July.

USD – Fed’s meeting eyed

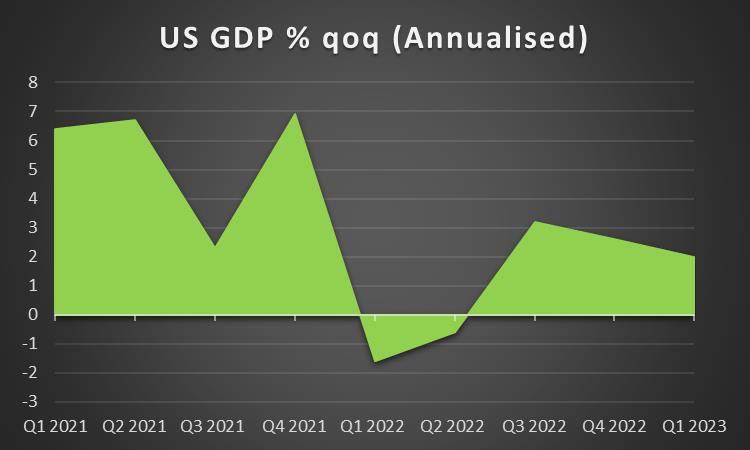

The USD seems to be able to halt its downward trajectory over the past two weeks against its counterparts, maybe even edged a bit higher in the past few days. On a macroeconomic level, the deeper contraction reported for industrial production in June tends to enhance our worries about the outlook of the US manufacturing sector, and the release of the Philly Fed Business index for July tended to provide little comfort. Furthermore, the wider drop in the number of house starts and building permits intensified our worries also for the US construction sector. But it’s not only production side data that were not showing a good performance, as the US retail sales growth rate slowed down for June instead of rising disappointing traders. In the coming week, we have a number of high-impact financial releases from the US and we highlight the preliminary GDP rate for Q2. Should the releases imply further slowdown or even contraction of economic activity we may see the USD losing some ground. Yet we expect market attention to be placed mainly on the monetary front as the Fed is to release its interest rate decision. The bank is expected to deliver a 25-basis-point rate hike and the market is expecting the bank to remain on hold after that until the end of the year. Nevertheless, some Fed policymakers have expressed the opinion that another or even more rate hikes may be required in order to return inflation to the Fed’s 2% target. Yet CPI rates slowed down considerably in June, thus easing the pressure on the Fed to proceed with more rate hikes. Hence should the bank actually deliver the 25 basis

points rate hike as expected and maintain a rather hawkish tone in its accompanying statement foreshadowing more rate hikes to come we may see the USD getting asymmetric support as the market may have to reposition its expectations. On the flip side, should the bank sound uncertain or allow for the notion that it has reached its terminal rate, then the market’s expectations are to be justified and we may see the USD losing some ground.

GBP – Inflation eases

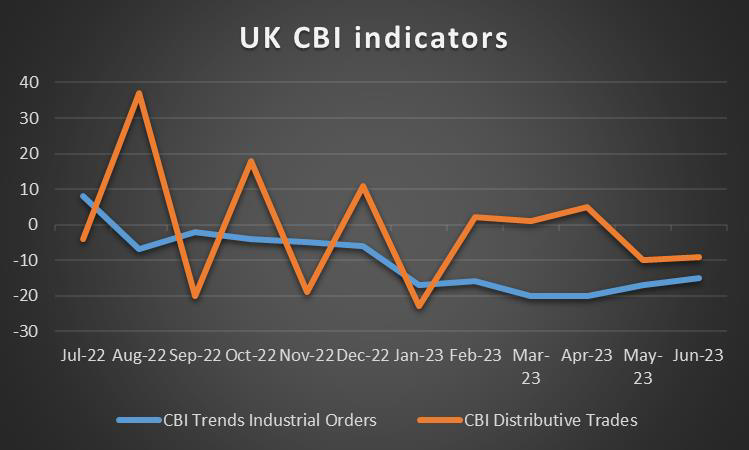

The pound seems about to end the week lower against the USD, the EUR but not JPY. The weakening of the pound is understandable on a macroeconomic level after the slowdown of UK’s CPI rates for June. The easing of inflationary pressures was characteristic as the rates slowed down in June, more than expected both on a headline as well as on a core level. Nevertheless, the rates are still at very high levels, considering BoE’s target of 2%. Hence, BoE still has to maintain an aggressive rate-hiking stance, yet the slowdown of the CPI rates tends to ease the pressure on BoE. The market’s expectations for the terminal interest rate seem to have been lowered and are now expected to reach 6.0% by the end of the year. It’s characteristic that the UK bond yields dropped after the inflation prints were released with the 10-year bond yield dropping as low as 4.184% a level not seen since February. Overall though we tend to maintain our expectations for the bank to continue being aggressively hawkish, especially after the replacement of former BoE MPC member Tenreyro with Megan Greene, which seems to be leaning towards the hawkish side strengthening the balance of power in favour of the hawks further. On the other hand, though BoE’s monetary policy tightening, tends to slow economic growth in the UK hence we tend to highlight the release of the preliminary PMI figures of July, with special emphasis on the services sector indicator. Should the readings show an additional slowdown of economic activity in the UK we may see the pound slipping, but we also expect the CBI indicators to gather attention by pound traders.

JPY – BoJ’s to remain dovish

JPY seems about to end the week lower against the USD and the EUR and slightly the pound, in a sign of broader weakness. On a macroeconomic level, we note the improvement of the trading balance, turning marginally positive in June, for the first time in the past two years. The release could be perceived as another positive sign of Japan’s economic recovery. On the other hand, the easing of inflationary pressures in June seems to be stalling. Yet, BoJ seems to be determined to maintain its ultra-loose monetary settings in place. It’s characteristic that BoJ Governor Ueda stated that to reach sustainably and in a stable manner the bank’s 2% inflation target, there is still some ground to cover. The statement also tends to strengthen the notion that the bank is not yet ready to tweak its Yield Curve Control (YCC) policy. Hence the bank’s meeting in the coming week is coming under the market’s magnifying glass. The bank is expected to maintain the interest rate at -0.10 and characteristically JPY OIS implies that the market has that scenario almost fully priced in. Given also the statements of BoJ Governor Ueda mentioned before we expect the bank to maintain its dovish

stance in the accompanying statement. Should the bank actually remain dovish as expected, we may see JPY weakening as monetary outlook differentials with other central banks would be expected to widen. On a more fundamental level, we highlight JPY’s dual nature as a safe haven and a national currency. Hence should the market sentiment turn more risk-oriented, that may provide some outflows for JPY and vice versa.

EUR – ECB to hike rates again

The common currency edged lower against the USD in the past week, while tended to gain extensively against the pound and to a lesser degree against the JPY. On a macro level, we note that the slowdown of the HICP rate for June in the Eurozone was confirmed yet EUR traders are to have a busy week ahead. Making a start on Monday with the release of July’s preliminary PMIs with the market focus expected to be placed on Germany’s manufacturing sector. On Tuesday we note Germany’s Ifo indicator for July, yet the highlight of the week for EUR traders is expected to be ECB’s interest rate decision on Thursday. The bank is expected to hike rates by 25 basis points and currently, EUR OIS imply a probability of 97.76% for such a scenario to materialise. The market currently, seems to be expecting the bank to hike rates again in September. Hence should the bank actually deliver the rate hike as expected, the next points of attention are to be the accompanying statement and ECB President Christine Lagarde’s press conference. Should the bank maintain its hawkish tone we may see the common currency getting some support while should the bank signal that its terminal rate has been reached or is nearing we may see the EUR retreating. Yet EUR trader’s interest is to be maintained as on Friday we note the release of France’s and Germany’s preliminary HICP rates for July and France’s preliminary GDP rate for Q2. Should the HICP rates stall to slow down we may see EUR getting some support.

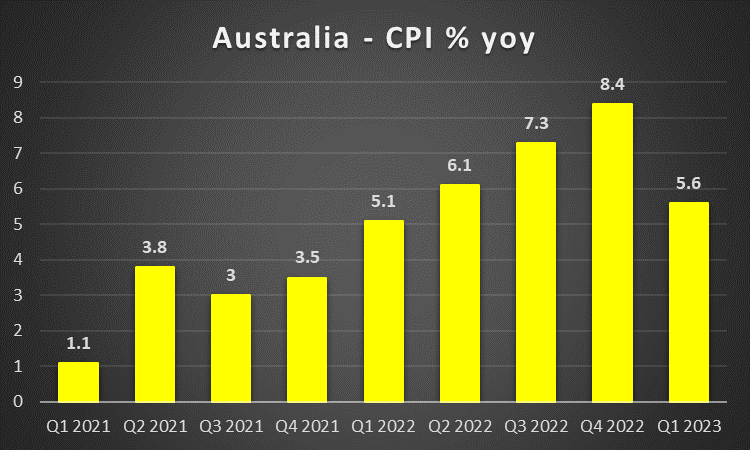

AUD – CPI rates in focus

AUD is about to end the week lower against the USD yet recent data tended to limit the Aussie’s losses. On a macroeconomic level, we note that Australia’s employment data for June beat expectations, with the unemployment rate ticking down while the employment change figure dropped less than expected. The

better-than-expected data may sharpen RBA’s hawkishness somewhat. We note that the release of RBA’s minutes for the July meeting tended to imply that more rate hikes may be required for inflationary pressures to be satisfactorily curbed. Characteristically the document stated that “Members agreed that some further tightening of monetary policy may be required to bring inflation back to target within a reasonable timeframe, but that this depended on how the economy and inflation evolve”. On the side we would also note that RBA Governor Lowe is to step down after the end of his term, as he received substantial criticism on a political level for hiking rates for the bank increasing the interest rate and is to be replaced by RBA Deputy Governor Michelle Bullock, starting from mid-September. Yet we do not expect the bank to alter its monetary policy because of a change of leadership and to remain mostly data-driven. In the coming week, we would highlight the release of the CPI rates for Q2 and should there be an acceleration of the rates and given the tightness of the Australian employment market we may see the pressure building up on RBA for another rate hike. On a more fundamental level, we note that the measures taken by the People’s Bank Of China to support the Yuan tended also to provide support for AUD. Let’s not forget that at the start of the week, the release of China’s GDP rates and other data tended to create some worries for the recovery of the Aussie and thus weakening the Aussie. Also, should the market sentiment turn more risk-oriented, we may see the Aussie getting some support as it is considered a more risky asset given its commodity-linked nature and vice versa.

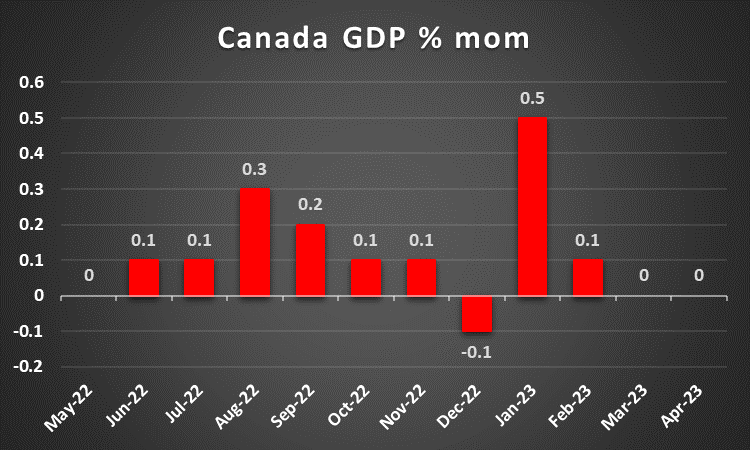

CAD – CPI rates slow down

The CAD is about to end the week in the greens against the USD for the second week in a row. It should be noted that even the considerable slowdown of Canada’s CPI rates for June was not able to halt the CAD’s winning streak. It’s characteristic that the headline rate slowed down and entered BoC’s 2-3% target range, with the core rate still remaining just barely out of range. The release tended to enhance market expectations for the bank to remain on hold in its September meeting, yet another rate hike in the coming months is still possible. So there is still some uncertainty is maintained for the bank’s intentions. It should also be noted that the number

of house starts has risen for June bearing good news for the construction sector of Canada in spite of BoC’s cumulative tightening. Please note that the retail sales growth rate for May is still to be released and could alter CAD’s direction. In the coming week, we note the release of Canada’s business barometer for July on Thursday and the GDP rate for May due out on Friday. Especially a possible acceleration of the GDP rate could provide additional support for the Loonie. On a more fundamental level, we note that oil prices edged higher for a fourth week in a row. Oil prices seem to be caught between a tightening supply side which tends to support oil prices and a weakening demand outlook for the commodity, especially from China which tends to weigh on the commodity’s prices. Should oil prices continue to be on the rise, we may see the Loonie getting some support given that Canada is a major oil-producing economy.

General Comment

As a general comment, we expect volatility to rise in the coming week as the number of high-impact financial data is to increase as are also the number of monetary policy events mentioned before. The USD may increase its dominance in the FX market mainly, yet certain releases may allow other currencies to navigate more independently. Yet the initiative over moves in the FX market is to remain in USD’s hands, with the release of the US GDP rate for Q1 and the Fed’s interest rate decision weighing considerably. Yet the Fed’s interest rate decision, is to have wider ripple effects as it can affect also US stock markets as well as gold’s price. It should be noted that US stock markets maintained their upward motion over the past week. The earnings season is in full mode with corporations such as large banks like Wells Fargo, JP Morgan, City Group, Bank of America, Morgan Stanley and Goldman Sachs surpassing market expectations and showing overall some resilience considering the tight financial environment in the US. Other companies’ earnings reports such as Tesla and Netflix had a negative impact on their share price. In the coming week we expect a shift of the market attention towards the tech sector as we expect the earnings releases of Microsoft (#MSFT), eBay (#EBAY), Meta Platforms (#META), Alphabet (#GOOG), Intel Corporation (#INTC) and Amazon (#AMZ) among others. As for gold’s price, we note that the precious metal seems to have taken advantage of USD weakness as it was on the rise. We expect the negative correlation of the USD with gold’s price to be maintained in the coming week with the US yields also playing a substantial role given that US Bonds tend to be a competing trading instrument to gold. Should the USD gain, Gold’s price may drop and vice versa.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.