We leave behind us an exciting week for the FX market maybe with the strengthening of the USD being the most characteristic movement in the past few days. In the coming week, a plethora of high impact financial releases and monetary policy events are expected to shake up the markets. On the monetary front, we highlight the release of the FOMC’s interest rate decision on Wednesday the 4th of May, which is to be followed by BoE’s interest rate decision on Thursday the 5th of May. Before these two interest rate decisions we get on Tuesday the 3rd of May, RBA’s interest rate decision, which is also expected to hike rates. On second base, we would also like to note the release of Norway’s Norgesbank and the Czech Republic’s CNB releases that could generate substantial interest for their respective currencies. As for financial releases we make an early start tomorrow Saturday with China’s NBS and Caixin manufacturing PMI figures for April, which may affect the market on Monday, while on Monday we also note the release of the US ISM manufacturing PMI figure for April. On Tuesday we get the US factory orders growth rate for March and on Wednesday we get New Zealand’s employment data for Q1 as well as the US ISM non-manufacturing PMI figure for April. On Thursday we note the release of Australia’s trade data for March while the crown of financial releases for the week is expected to be April’s US employment report on Friday the 6th of May.

USD – Fed’s interest rate decision and April’s employment report

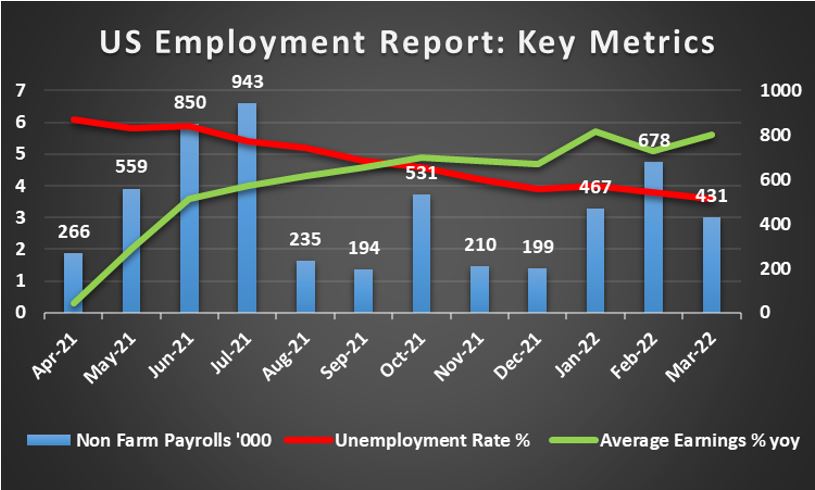

The USD Index skyrocketed since Monday making one of the biggest jumps for the past two years. It’s characteristic that the demand for the USD was so high that at some point reached a multi-year record high point. Worries for a possible mild recession, tended to provide safe haven inflows, while the market’s hawkish expectations for the Fed’s meeting next Wednesday tended to feed the bulls even further. It should be noted that Fed Funds Futures (FFF) seem to imply a probability of 93.9% currently, for the bank to hike rates by 25 basis points. We tend to expect the bank to maintain a hawkish tone, probably citing a tight US employment market, the high inflationary pressures in the US economy and the need to curb them. Given Fed Chairman Powell’s statements last week that taming inflation was absolutely essential and a decision for a 50 basis points rate hike is possible on Wednesday, we may see the market expecting more. Should the bank actually deliver a double rate hike we may see the support for the USD growing further, especially should it be accompanied by hawkish comments. On a fundamental level, we note that the market’s attention remains at least partially shifted towards US stockmarkets as the earnings season is still on. We expect that tendency to continue into next week as we have a number of high profile companies that are to release their earnings reports for Q1. Also the decline of the US GDP rate (advance) for Q1 into the negatives took the markets by surprise on Thursday and tended intensify market worries for a possible recession of the US economy, while also forced the USD to halt its ascent against other currencies. As for financial releases we note from the US on Monday, the release of the ISM manufacturing PMI figure for April, on Tuesday we get the Factory orders growth rate for March and on Wednesday we get the ADP national employment figure for April as well as the ISM non-manufacturing PMI figure for the same month. On Thursday, we get the release of the weekly initial jobless claims figure and finally we highlight on Friday the release of the US employment report for April. Should the rates and figures paint the picture of a tight US Employment market that could provide some support for the USD as it would imply that the Fed gets a green light to continue with the tightening of its monetary policy. Special focus is being placed on the Non-Farm Payrolls (NFP) figure, the unemployment rate and the average earnings growth rate.

GBP – BoE’s interest rate decision in focus

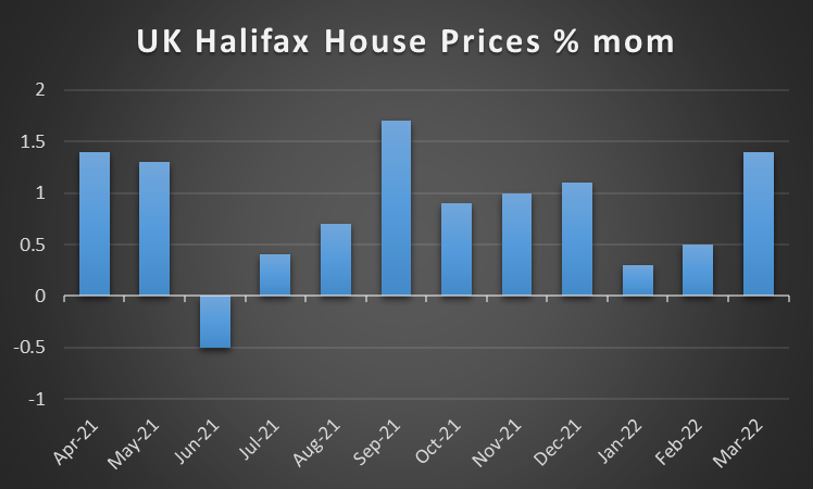

The pound retreated heavily against the USD, to a lesser degree against the JPY and seems about to remain rather stable against the EUR for the week. Pound traders are now refocusing towards BoE’s interest rate decision on Thursday. The bank is widely expected to hike rates by 25 basis points, raising the interest rate from 0.75% to 1.00%. It’s characteristic that the market seems to have fully priced in such a scenario according to GBP OIS. It should be noted that the market’s expectations are even more hawkish given that it has priced in, either fully or partially, more rate hikes to come until the year’s end. Given that the market seems to have fully priced in, such a rate hike, it may take more to excite the markets and support the pound. Hence should the bank actually deliver a 25 basis points rate hike as expected, we may see the market’s attention turning towards the accompanying statement. Should the bank maintain a clearly hawkish, confident tone, we may see the pound getting further support as such a tone would indirectly reaffirm the market’s hawkish expectations for further rate hikes to come. On the flip side, should the tone of the document show some degree of hesitation about the future and that the bank remains cautious, we may even see the market’s reactions turning bearish for the pound as it would be a dovish hike by the BoE. As for financial releases, it’s expected to be a rather easy going week, given that the only high impact data due out could be the Halifax House prices for April, on Thursday. Hence, we would not be surprised to see fundamentals taking the lead in regards to the pound’s direction.

JPY – JPY’s weakening allowed to continue

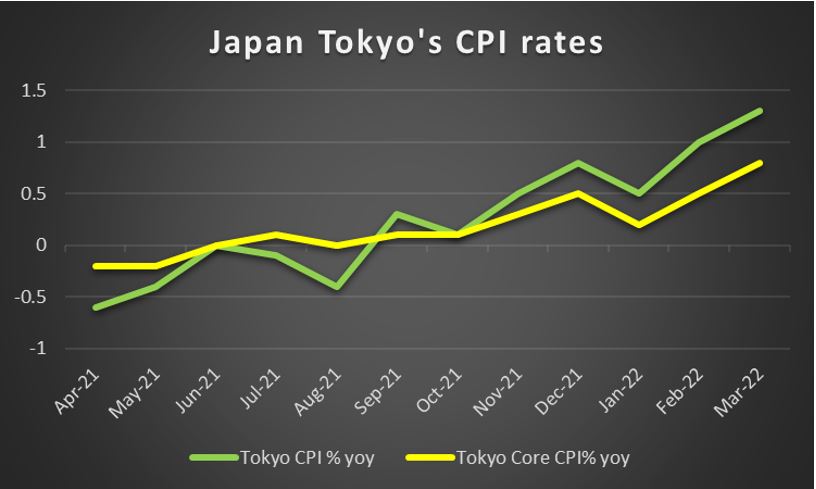

JPY’s weakening practically was allowed to continue against the USD for an eighth week in a row. It should be noted though that the JPY was gaining against the pound and the common currency in a movement which resembled a halt in the downward motion of the Japanese currency. In a latest development, BoJ’s interest rate decision practically renewed the weakening of JPY on Thursday. The bank maintained its interest rate at -0.10% as was widely expected, yet also decided that “The Bank will purchase a necessary amount of Japanese government bonds (JGBs) without setting an upper limit so that 10-year JGB yields will remain at around zero percent.” Hence the ultra loose monetary policy of BoJ with its massive stimulus program is being maintained, which in turn may continue to weigh on JPY. Given that the rate of JPY against the USD has reached an multi year low point, worries were raised, yet BoJ Governor Kuroda in his press conference sounded rather relaxed as he mentioned that “We haven’t changed our view that a weak yen is positive for Japan’s economy as a whole”. The bank is expected to maintain its ultra loose monetary policy also in the future as according to the bank consumer inflation, excluding energy and volatile food prices, is expected to hit 1.5% yoy in 2024, yet that is still below the bank’s target of 2.0% yoy. On a more fundamental level, the Yen is expected to maintain its dual role as a safe haven and a national currency. Hence any intensification of the market’s worries on a global level are expected to to provide inflows for the Yen and vice versa any improvement of the market sentiment to produce outflows. As for financial releases, we note on Tuesday the final reading of the Jibun Bank Manufacturing sector PMI indicator for April and on Friday we note the release of Tokyo’s CPI rates for April.

EUR – Dark fundamentals for the EUR area

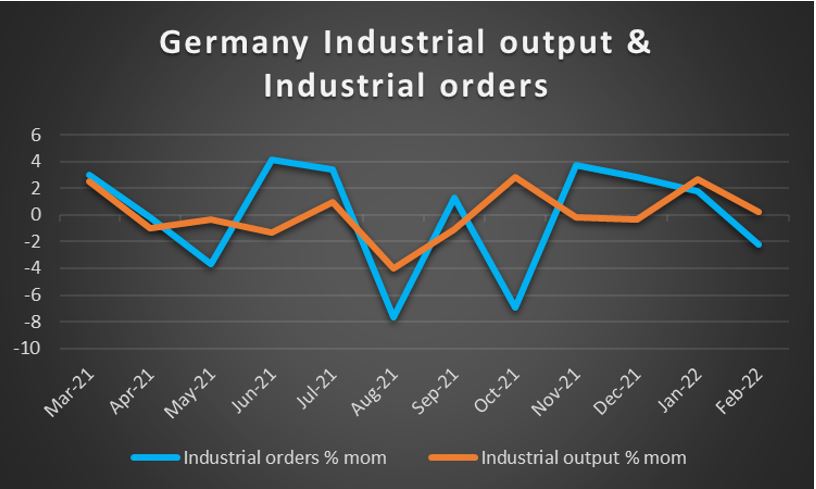

EUR’s drop against the USD intensified substantially in the past few days against the greenback, while the common currency seems to be losing ground against the JPY as well, but not the GBP. Please note that April’s preliminary HICP rates for France, Germany and the Eurozone as a whole accelerated beyond market expectations once again practically underscoring the high level of inflationary pressures in the Eurozone. Also the GDP rates accelerated disproving any worries currently benig present about the expansion of theEurozone’s economy due to the war in Ukraine. The releases are expected to intensify the pressure on the ECB to tighten its monetary policy. It should be noted that ECB President Lagarde last week hinted towars a rate hike in the summer if financial conditions allow it, yet some ECB policymakers seem to remain keen on hiking rates and ending the bond purchasing program of the bank at a faster pace. But given the uncertainty in Eurozone’s economic outlook, the balance of power within the ECB may still be tilting towards the doves. On a fundamental level the war in Ukraine and the sanctions imposed on Russia tend to weigh on the common currency. The recent halt in the supply of Russian gas to Poland and Bulgaria, as they have not met Moscow’s demands to pay in Roubles, was another painful reminder of Europe’s and the Eurozone’s dependency on Russian energy products. It should be noted though, that Germany is no longer opposing banning the trading of Russian oil within the Eurozone, yet nothing has been mentioned for Russian natural gas. Overall, should the tensions with Russia intensify, ie. if Russia cuts off natural gas to other members of the EU, we may see the common currency retreating and vice versa while should a solution be worked out or indications to that end be provided, we may see the EUR gaining. As for financial releases, we note the release of Germany’s trade data for March on Wednesday, the final PMI figures for April on Monday and Wednesday and Germany’s industrial orders and output growth rates for March on Thursday and Friday respectively.

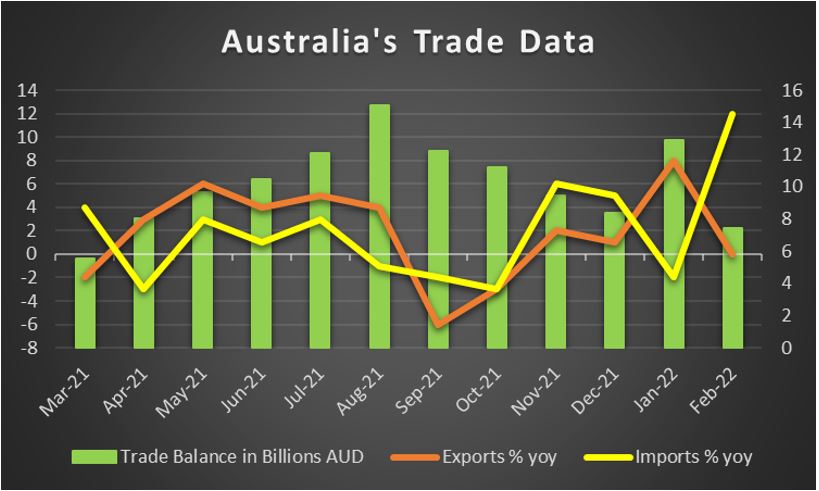

AUD – RBA to move the Aussie

The Aussie is about to end the fourth week in the reds against the USD despite some support it got today. It should be noted that Aussie traders in the coming week are expected to focus on the release of RBA’s interest rate decision on Tuesday’s Asian session. The bank is widely expected to hike rates by 25 basis points and its characteristic that AUD OIS imply a probability of 81% for such a scenario to materialise. It should be noted that Reuters, citing a recent survey among economists expects the bank to proceed with only a 15 basis points rate hike next Tuesday. In its’ April meeting the bank had mentioned in Governor Lowe’s accompanying statement that “Inflation has increased in Australia, but it remains lower than in many other countries; in underlying terms, inflation is 2.6 per cent and in headline terms it is 3.5 per cent” and also cited uncertainty for the matter. The acceleration of the headline rate to 5.1% yoy, in Q1, may now force the bank to leave any hesitation behind it and start tightening its monetary policy in a more intense and fast manner. Should the bank proceed with a rate hike and Governor Lowe express a hawkish tone in his accompanying statement on Tuesday we may see the Aussie getting some substantial support. On the other hand should the bank proceed with a 15 basis points rate hike and/or express cautiousness and hesitation we may see the support for the AUD being limited. Also note that, the bank is expected to provide new projections on the path of inflation for Australia. Please also note that the Aussie as a commodity currency tends to be boosted by a positive market sentiment and vice versa, and we would expect that tendency to be expressed next week as well. On a more fundamental level, we note that the consecutive lockdowns in China, may weigh on the AUD as a substantial amount of Australia’s economy is linked to Chinese production levels, through exports of raw materials. Hence, we would expect Aussie traders to keep a close eye over the release of the China’s manufacturing sector’s PMI figures for April on Saturday. Should the readings show further contraction of economic activity in China’s particular sector we may see the Aussie being adversely affected on Mondays’ opening. Yet besides the chinese data on Saturday, we would also note the release of Australia’s retail sales and building approvals growth rates on Wednesday and Thursday respectively, while on Thursday we also get Australia’s trading data, all rates and figures being for March.

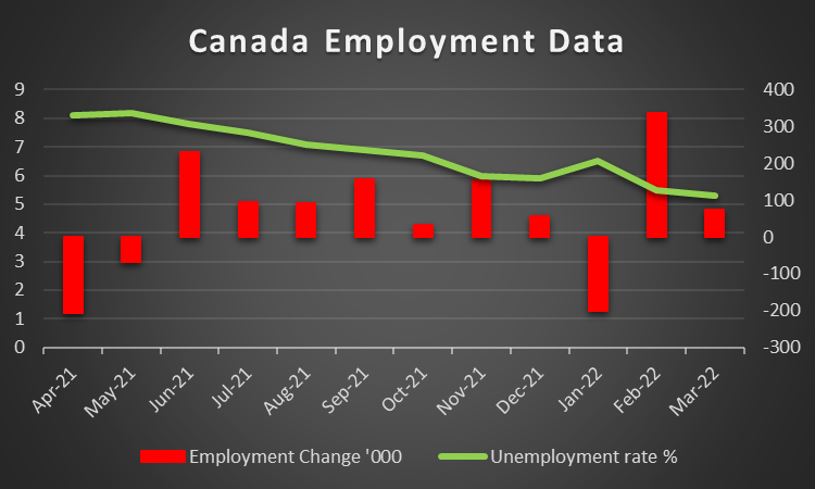

CAD – Trade and employment data eyed

The CAD seems to be losing ground against the USD for a fifth week in a row, yet to a lesser degree. Overall the recent strengthening of the US stockmarkets tended to improve the market sentiment which in turn could have cancelled out some of the bearish sentiment for the CAD as well. Also the rise of oil prices tended to provide some support for the Loonie and we would not be surprised to see that tendency being continued in the coming week as well, should oil prices actually remain supported. Oil prices seem to be squezed by conflicting fundamentals as on the one hand the Chinese lockdowns tend to create worries for the demand side of the commodity. On the flip side, the war in Ukraine, the sanctions on Russian oil and the unwillingness of other oil producing countries to hike oil production levels, tend to increase expectations for a tightness in oil supply. We must note though that Canada’s retail sales for February decelerated, yet not as much as was expected, while the GDP rate for the same month is still to be released as these lines are written. In the coming week we note the release of Canada’s manufacturing PMI figure for April on Monday, while on Wednesday we get the Canada’s trade data for March. A possible widening of February’s trade surplus could provide support for the CAD as it would imply that the Canadian economy, benefited more from its international trading transactions. On Friday, we highlight the release of Canada’s employment data and should they show a possible tightening of the Canadian employment market, we may see the Loonie getting further support as it would be a first step for BoC to tighten its monetary policy even further and at a faster pace.

General Comment

As a final comment for the report, we expect the market’s attention to remain partially shifted in the US stockmarkets as we get a number of earnings reports for high profile companies such as Pfizer (#PFE), eBay (#EBAY) and Ali Baba (#BABA), just to name a few, among many. It should be noted that US stockmarkets were able to bypass the negative GDP report for Q1 yesterday and tend to maintain their optimism in today’s premarket hours, recovering some of the lost ground since the start of the week. Yet we would expect US equities markets to also be influenced in their direction from the Fed’s interest rate decision on Wednesday and the release of the US employment report for April on Friday, as ripple effects are possible beyond the FX market. In the FX market, we expect the USD to continue to be in the driver’s seat over other currencies, given the high impact and frequency of financial releases and monetary events scheduled. The pound, CAD and the Aussie could also have their spotlight at certain points during the week. As for Gold we note that the negative correlation of the precious metal was present in the past few days given that the strong USD tended to weigh on gold’s price, yet maybe not as proportionally as expected, thus gold prices may have also other factors in play, driving its price.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.