As the week is nearing its end we have a look at what next week’s calendar has in store for the markets. We make a start on Monday with China’s NBS PMI figures and Germany’s Ifo indicators, both releases being for January. On Tuesday, we get from the US December’s durable goods orders and January’s consumer confidence. On Wednesday, we get from Australia, Q4’s CPI rates, Sweden’s GDP rate for December and New Zealand’s December trade data. On the monetary front we note the release for Canada of BoC’s interest rate decision and we highlight the release from the US for the Fed’s interest rate decision. On Thursday, we get from France, Germany, the Eurozone the preliminary GDP rate for Q4 24 and we also note Switzerland’s January KOF indicator, Euro Zone’s January economic sentiment for January. In the American session we highlight the release of the US GDP advance rate for Q4 25 and note the release of the weekly initial jobless claims figure. On Friday, we get from Japan Tokyo’s CPI rates for January, Chinas’ Caixin manufacturing PMI figure for January, France’s and Germany’s preliminary HICP rates for the same month, the US consumption rate and PCE rates both for December and Canada’s GDP rate for November.

USD – Fed’s interest rate decision in focus

On a political level we note Trump’s inauguration that did not pass unnoticed with a slew of executive orders. We highlight three , the first would be the crackdown on immigration the second ,would be the intentions to apply tariffs on imports from Mexico and Canada (tariffs were announced also on US imports from the EU and China) from February 1st and the third the withdrawal of the US from the Paris agreement. The first two are expected to enhance inflationary pressures in the US economy, while the third may be a prelude to Trump’s call for oil “drill, baby drill”, thus possibly weighing on oil prices. Overall, the actions of the Trump administration are expected to be supportive for the USD, yet any hesitation towards applying tariffs on US imports could weigh on the greenback.

On a monetary level, we highlight the Fed’s interest rate decision next Wednesday. The market’s expectations as expressed by Fed Fund Futures are for the bank to remain on hold in the January meeting and its characteristic that the market has almost fully priced in such a scenario to materialise. The market also seems to expect the bank to proceed with a rate cut in the June meeting and that rate cut being possibly the only one for 2025 if the bank doesn’t cut rates also in December. We expect the bank to remain on hold and possibly intensify its hawkishness in its accompanying statement and Fed Chairman Powell’s press conference about half an hour later. Should that be the case it could verify if not enhance the market’s expectations for the bank remaining on hold for a prolonged period, thus supporting the USD and weighing on US stockmarkets. On the flip side should the Fed’s decision be characterised by a less than expected hawkish tone, the release may weigh on the USD and support US stockmarkets as it would imply a faster easing of financial conditions in the US economy.

On a macroeconomic level, we highlight two releases next week that could prove to be market movers. The first would the GDP advance rate for Q4 24. Should the rate accelerate further it could support the USD as vit would imply that the US economy has grown at a faster pace in the last quarter of the past year. Also on Friday we get the PCE rates for December and a possible acceleration of the rates could support the USD as it would imply a resilience of inflationary pressures in the US economy. Both releases if accelerate may harden the Fed’s hawkish stance and force the market to alter its perceptions for the bank’s intentions.

Analyst’s opinion (USD)

“We expect the USD to remain supported in the coming week on a fundamental level, based on what was described above. Yet should there be doubts about Trump’s intentions to impose tariffs or should the Fed sound less hawkish than expected, or the GDP rate for Q4 25 disappoints the markets, we may see the USD retreating. We highlight the possibility of increased volatility from Wednesday onwards as we get the Fed’s interest rate decision on Wednesday, the GDP rate on Thursday and the PCE rates on Friday”

GBP – Fundamentals to lead the way

The pound seems to be in a curious state as it seems to end the week in the greens against the USD and JPY yet seems to be losing ground against the EUR. We note that on a fundamental level worries tend to surround the pound. UK gilt yields corrected a bit lower over the past two weeks yet are still at relatively high levels. The rise of UK gilt yields tends to underscore the lack of confidence of investors for the outlook of the UK economy. Overall expectations for low growth, sticky inflation and relatively low business confidence tend to feed investor’s distrust for the pound. On the positive side the UK seems to have avoided tariffs from Trump’s administration on exports of UK products to the US, at least for now. On a fiscal level we note the Labour Government’s intentions for a tight fiscal policy and we tend to worry that it may lead to low growth thus possibly entering the UK economy in a negative spiral.

On a monetary level, we note the market’s expectations for the BoE to proceed with a rate cut in the February meeting and continue with another one possibly in May. Overall any signs for the bank proceeding with the rate cut in its February meeting could weigh on the pound and vice versa. On the flip side we note BoE’s willingness to proceed in cooperation with the UK Government in pro-growth reforms for the banking sector, yet note that deregulation of the banking sector should be handled with care, especially in the UK.

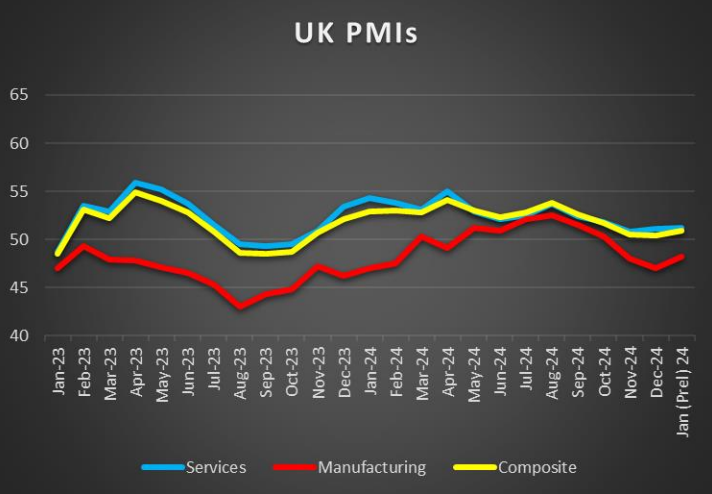

On a macroeconomic level, we note the release of the UK employment data for November. The data showed a loosening UK employment market with the unemployment rate ticking up and the employment change figure dropping. One interesting exception was the average earnings growth rate which accelerated beyond expectations in a reminder that the UK employment market may continue feeding inflationary pressures in the economy. Other than that we note the release of the CBI business optimism figure which dropped far deeper into the negatives supporting the notion mentioned in the fundamentals before for low business confidence. Overall the data released were not supportive for the pound with the great exception of the January preliminary PMI figures which showed an improvement in both the services and manufacturing sectors, which tends to enhance hope for growth in the coming quarters.

Analyst’s opinion (GBP)

“In the coming week, fundamentals may be leading the pound, given the low number of high impact financial releases from the UK. We highlight especially monetary policy as the next meeting of BoE will be nearing and should market expectations for the BoE to cut rates in February intensify, we may see the pound losing ground”

JPY – BoJ hiked rates as expected

On a fundamental level we note that Japan may not have been affected by the intentions of Trump to impose tariffs on US imports directly, yet the possibility of a slowing global economy tends to worry Japanese policymakers. On the brighter side, Fitch affirmed its rating of Japan at “A” with a steady outlook. There seems to be political stability which could be considered as a plus for the Yen, yet even with the USD retreating against its counterparts over the week, JPY remains at dangerously low levels. Hence the possibility of carry trade resuming by selling the Yen remains with a substantial possibility and if so could drive the Yen lower. On a political level, PM Ishiba seems to be seeking support in a cross party consensus to support his minority government as it does not control the Diet. Last but not least, we note the safe haven qualities of JPY and should we see uncertainty rising among market participants we may see JPY getting some support.

On a monetary level, we note BoJ’s interest rate decision early today. The bank hiked rates by 25b basis points to reach 0.5%, a level not seen for BoJ since 2008. Overall the tightening of the bank’s monetary policy, was supportive for JPY and the accompanying statement allowed for the notion of more rate hikes to come in the future. Currently the markets seem to expect BoJ to proceed with another 25 basis points rate hike, probably in July or September, which could maintain some support for the JPY. Also we would not be surprised to see the bank intervening in the markets in order to support the Yen should it be weakened substantially.

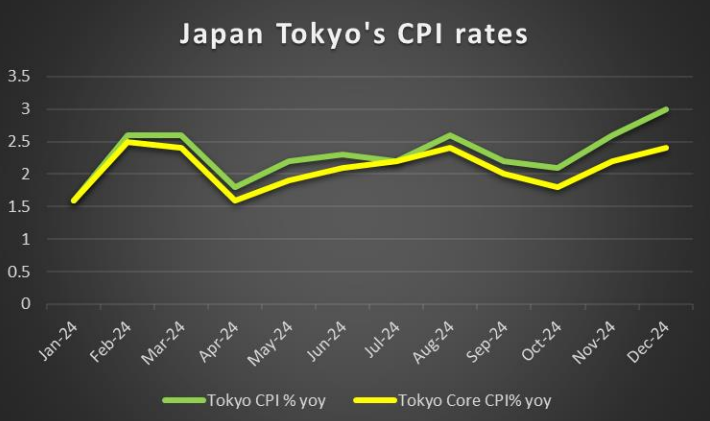

On macroeconomic level, we highlight the acceleration of the CPI rates for December. The release highlighted the resilience of inflationary pressures in the Japanese economy which tend to support BoJ’s narrative. We also note the reversal of Japan’s trade deficit into a surplus in December, despite a slow down of the export growth rate, implying that more wealth entered the Japanese economy. Furthermore the machinery orders growth rate for November accelerated instead of falling into the negatives as expected, implying greater confidence on behalf of businesses to actually invest in the Japanese economy. Overall financial data tended to be supportive for JPY in the past few days.

Analyst’s opinion (JPY)

“Given BoJ’s rate cut, PM Ishido’s comments and the acceleration of the CPI rates for December we tend to view the JPY as being possibly supported in the coming week and lay our interest primarily on the fundamental side in regards for its direction”

EUR – ECB to cut rates

On a political level we highlight that Germany’s pre-election period is entering its final month and the park stabbing in Aschaffenburg is shifting the agenda of elections further to the right. In general, the political situation in Germany but also in other countries such as France does not boost the confidence of EUR traders and tends to be weighing on the common currency. Furthermore, the worries for Germany’s economic and energy outlook are intense and also tend to weigh on the EUR. The recent reiteration of Trump’s intentions to impose tariffs on US imports of EU products makes the situation even worse. Overall, we see the case for EUR fundamentals to weigh on the common currency over the coming week. An element which could provide some support for the EUR in the coming week would be any hesitation on behalf of US President Trump to actually impose tariffs.

On a monetary level, we highlight ECB’s interest rate decision next Thursday. The bank is widely expected to cut the refinancing and deposit rates by 25 basis points and currently EUR OIS imply a probability of 95.5% for such a scenario to materialise. The market also expects the bank to proceed with another three rate cuts within the year. Please note that recently ECB policymakers have stated that Trump’s tariffs, should they be imposed, could expedite the bank’s rate cutting path. Hence should the ban actually proceed with a 25 basis points rate cut as expected it could weigh on the EUR, yet we suspect that given that the market is expecting more rate cuts to come, attention is to be placed also on the bank’s forward guidance which is to be included in the bank’s accompanying statement and ECB President Lagarde’s press conference later on. So volatility for EUR pairs is expected to be extended beyond the time of the release as such. Should the accompanying statement and Lagarde’s press conference be characterised by sufficient dovishness to verify or surpass the market’s expectations we may see the bearish tendencies for EUR being enhanced.

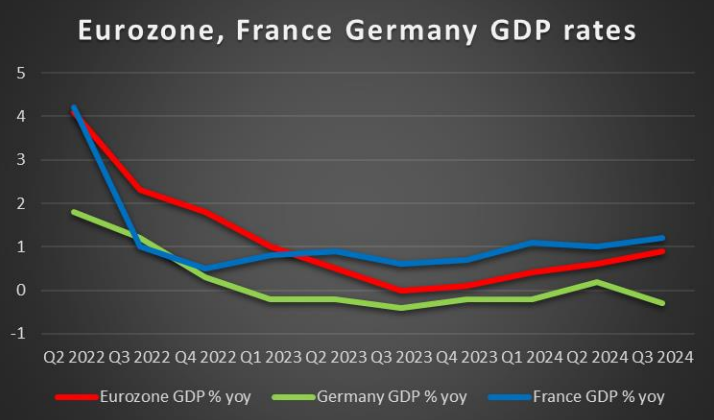

On a macroeconomic level, things are not looking that good either. Inflation has eased considerably over the past year in the Euro Zone which allowed the ECB to start lowering its interest rates, the name of the game in the Euro Zone is called growth. The release of the Preliminary PMI figures for December may have showed some improvement yet remained largely below the reading of fifty, in manufacturing sector and across member states in a sign of decreasing economic activity in the Eurozone and remain worrying for Germany, the economic powerhouse of the block. In the coming week we highlight the release of the preliminary GDP rates for Q4 25 of France, Germany and the Euro Zone as a whole. Should the GDP rates slow down or even show a shrinking of Euro Zone’s economy it could weigh on the EUR. Similarly should the December preliminary HICP rates of France and Germany slow down it may also weigh on the EUR as such a release may allow for further easing of ECB’s monetary policy.

Analyst’s opinion (EUR)

“We see the case for fundamentals, ECB’s monetary policy and financial releases aligning towards weakening the EUR in the coming week. Overall, the EUR is a difficult case for the bulls, yet specific issues such as any hesitation on behalf of Trump to impose tariffs on European products imported in the US, could provide some respite for the single currency”

AUD – December’s CPI rates to shake the Aussie

On a fundamental level we highlight the effect that developments regarding China may have on the Aussie. The issue has clearly demonstrated its importance in the past few days as Trump seemed determined to impose tariffs on US imports of Chinese products. Such a development could have slowed down economic activity in China’s manufacturing sector which could entail a reduction of Australian exports of raw materials to China. Yet in Friday’s Asian session, US President Trump stated that he could reach a trade deal with China while characterised his talk with Chinese leader Xi as “friendly.” The news provided support for the Aussie on a fundamental level. Hence we note that further signals that the US and China could reach a possible trade deal and avoid the US imposing tariffs on Chinese products could further support AUD. Also please note that in the coming week we also get China’s manufacturing PMI figures for January and should they show a faster expansion of economic activity in the sector, it could provide some support for AUD.

n a monetary level, we note the market’s expectations for RBA to finally start cutting rates in its mid-February meeting and proceed with another two rate cuts during the year. Please note that the bank has raised and kept rates high for a prolonged period and the pressure on the bank to start cutting rates seems to be considerable. Yet economists tend to warn the bank not to rush to any rate cuts as it could re-ignite inflationary pressures in the Australian economy. Should we see market expectations for RBA to proceed with a rate cut in the next meeting, we may see them also weighing on the Aussie and vice versa. Yet we may see the market’s expectations about RBA’s intentions being influenced also be the release of the Q4 CPI rates next Wednesday.

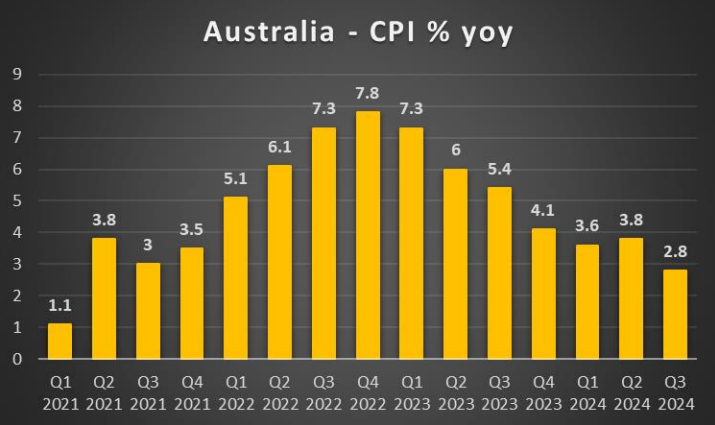

On a macroeconomic level, we note the improvement of Australia’s PMI figures as a positive signal despite the manufacturing related reading remaining below the level of fifty, implying another contraction of economic activity. In the coming week we note the release of December’s business confidence and conditions readings yet the highlight is expected to be the release of Q4’s CPI rates. The rates are expected to slow down on a year on year level and if actually so, could weigh on the AUD as it could enhance the market’s expectations for RBA to proceed with a rate cut in the February meeting. Yet the projected slow down still allows for the headline CPI rate to remain in upper half of the bank’s inflation target zone (1%-3%) and thus may not be conclusive for a rate cut just yet.

Analyst’s opinion (AUD)

“We expect the Aussie to form its direction in the coming week primarily by two factors with the first being the issue whether Trump will be able to reach a trade deal with China, avoiding imposing tariffs by February 1 st. Such a development could support the Aud and vice versa. The second issue is related with inflation and concerns the release of Australia’s December CPI rates and should the rates show an easing of inflationary pressures in the Australian economy, the release could weigh on the Aussie”

CAD – BoC to ease monetary policy further

On a fundamental level, we note that Trump’s threat to impose tariffs on US imports of Canadian products, tends to weigh on the CAD. The options for Canada do not seem good as it faces a choice between retaliation and appeasement. In both cases it seems like a lose-lose situation for the Canadian economy. At the same time the Canadian Government is facing budgetary issues given also the US threats and all of that is to be faced in a power vacuum practically with Canadian PM having resigned his position and it’s questionable if a successor is to win a no confidence vote, thus paving the way for general elections in Canada, which were to be held anyway in October. Yet the prospect of Conservative government may be supportive for the Loonie. Furthermore we note the possible effect of oil prices on the Loonie given Canada’s status as a major oil producing economy. Should oil prices continue to fall as they have over the past week, we may see them having a bearish effect on the Loonie.

Yet the highlight for CAD traders in the coming week is to be on a monetary level, as BoC is to release its interest rate decision. The bank is currently expected to cut rates in its meeting on Wednesday by 25 basis points, lowering them to 3% and CAD OIS imply a probability of 90% for such a scenario to materialise. The market also expects the bank to proceed with another rate cut by BoC probably in its April meeting. Should the bank cut rates as expected we may see the market’s attention turning towards BoC’s intentions and thus forward guidance. Should the bank’s accompanying statement be characterised by a dovish tone, practically verifying the markets dovish intentions, we may see the Loonie losing some ground.

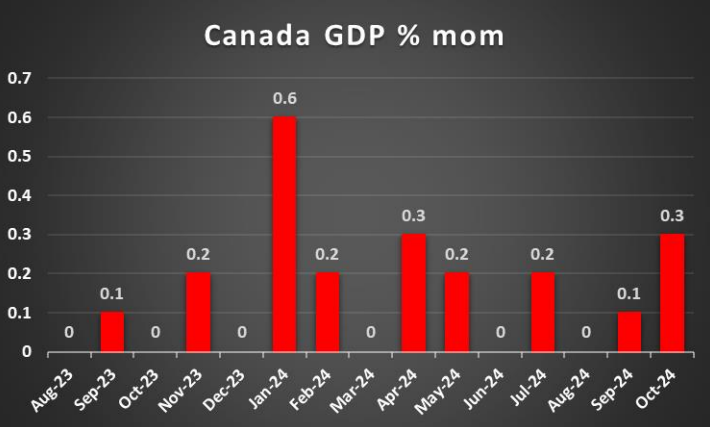

On a macroeconomic level, we note the easing of inflationary pressures in the Canadian economy on a headline level year on year, yet the respective core rate accelerated. In both cases though the CPI rates remain in the lower half of the BoC’s inflation zone target (1%-3%) which may have enhanced the market’s expectations for the bank to proceed with a rate cut in its Wednesday meeting. In the coming week we note the release of January’s business barometer and highlight the release of the GDP rate for November which is to show whether the Canadian economy grew in the particular month. Should the rate accelerate, we may see the CAD getting some support.

Analyst’s opinion (CAD)

“In the coming week, we expect CAD traders to be primarily influenced by the possibility of Trump imposing tariffs on US imports from Canada and if actually so could weigh on the Loonie. Also should BoC cut rates as expected and signal that more are to come, we may see the event also weighing on the Loonie”

General Comment

Overall we expect the USD to maintain the initiative over other currencies in the FX market given that he gravity and frequency of the US fundamentals are key to the market’s direction. Other currencies may come under the spotlight at certain points over the week which may allow for a more balanced trading mix to emerge. As for US stock markets we note that the earnings season is in full swing. Market interest is expected to heighten next Wednesday as we get the earnings reports of Microsoft (MSFT), Meta Platforms (META), Tesla (TSLA), IBM (IBM) and Alibaba ADR (BABA). Hence we may see the market readjusting its interest in the tech sector. Also US President Trump on Tuesday announced a private sector investment of up to $500 billion to fund infrastructure for artificial intelligence, aiming to outpace rival nations in the business-critical technology, as per Reuters, a move that is also expected to be supportive for US stockmarkets and intensify the markets’ interest in AI. As for gold’s price we note its bullish outlook with its upward motion intensifying as it nears the record high level of $2900. The uncertainty created on a fundamental level from Trump’s statements and actions tend to feed gold bulls as does the weakness of the USD.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.