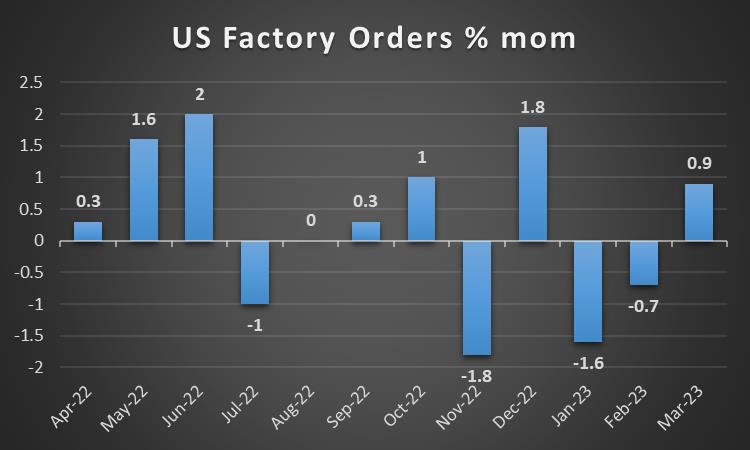

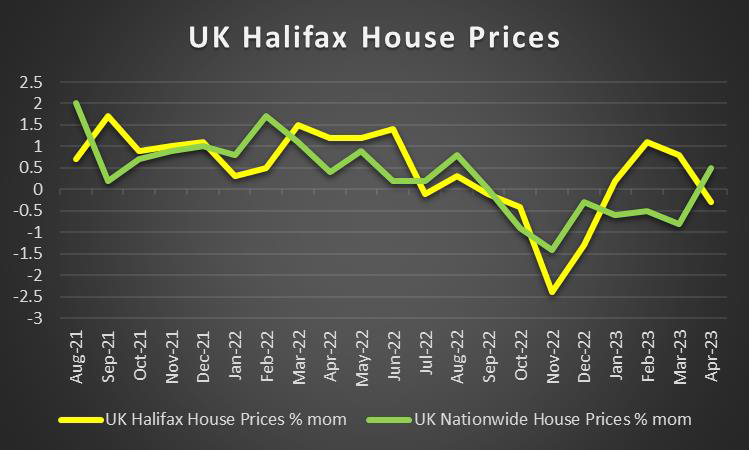

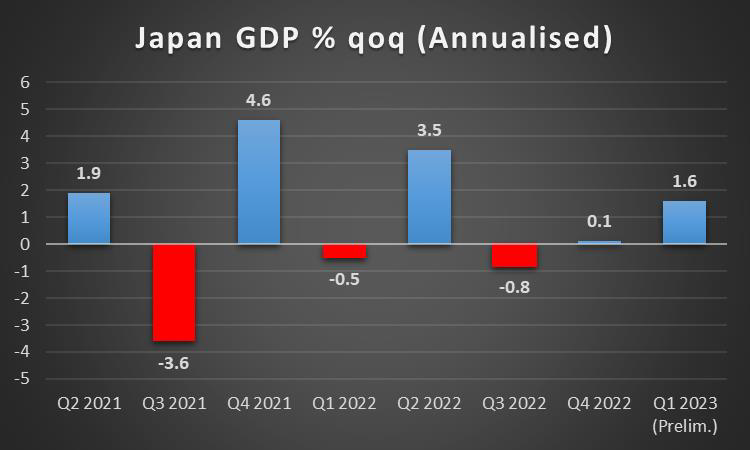

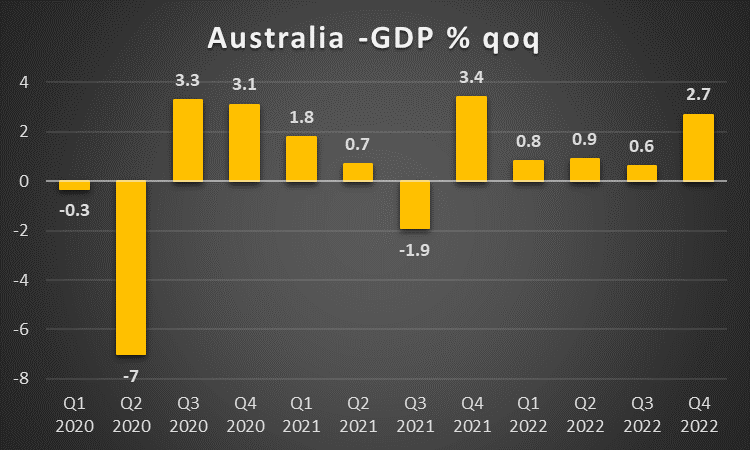

Markets seem to remain in a wait-and-see position, while the US employment report for May is still to be released and could shake the markets before the weekend. In the coming week, we note on the monetary front the interest rate decisions of Australia’s RBA on Tuesday and Canada’s BoC on Wednesday. As for financial releases, we make an early start on Monday with Switzerland’s and Turkey’s CPI rates for May, Eurozone’s forward-looking Sentix index for June and from the US we get the factory orders for April and the ISM non-manufacturing PMI figure for May. On Tuesday, we note the release of Germany’s industrial orders for April. On Wednesday, we get Australia’s GDP rate for Q1, China’s trade data for May, Germany’s industrial output for April, UK’s Halifax House prices for May and Canada’s trade data for April. On Thursday we get Japan’s GDP rate for Q1, Australia’s trade data for April, Eurozone’s GDP rate for Q1 and the US weekly initial jobless claims figure. Finally, on Friday we note the release of China’s inflation metrics for May, Sweden’s GDP rate for April, Norway’s CPI rates for May and Canada’s employment data for the same month.

USD – Debt ceiling deal reached.

The USD seems to have weakened for the week against its counterparts, yet the US employment report is still to be released and could alter its direction as the week is about to close. Fundamentals tended to lead the way as a deal between the White House and the Republican-led House of Representatives has been reached. The deal was submitted by Biden and was approved by the House of Representatives and the Democratic-led Senate as was expected, voted the bill through. Given the averted US default , the appears to have been an improvement of the market sentiment, which may have provided support for the US equities markets. On a macroeconomic level, our worries for the outlook of the US economy tend to be maintained given also that the ISM manufacturing PMI figure remained below the reading of 50, implying another contraction of economic activity for the US manufacturing sector. On the monetary front, we note that the market’s expectations for the Fed to skip a rate hike in its June meeting seem to have intensified. Also, the market seems to expect another rate hike in the bank’s July meeting and to start cutting rates from September onwards. We may see the bank skipping a rate hike in June, yet in our opinion the acceleration of the Core PCE rate for April was a stark reminder of how sticky inflation is in the US economy. We expect the Fed to maintain a hawkish stance and be ready to act if necessary and we would not be surprised to see the bank maintaining high rates well through the year until Q2 2024. Should Fed policymakers maintain their hawkish rhetoric we may see the USD being supported on a monetary level.

GBP – Cost of living crisis.

The pound seems about to end the week stronger against the USD, the EUR and to a lesser degree JPY in a sign of trust on behalf of the markets for the sterling. On the pound’s fundamentals, we note that the cost of living crisis in the UK maybe still is the main issue. It’s characteristic that inflation of prices on food products slowed down yet was still at 15.4% according to the British Retail Consortium, while Reuters reports inflation on food at 19% yoy. At the same time, analysts mention the possibility of “voluntary” price controls, at least on essential food items. It’s understandable that the headline CPI rate in the UK economy, despite slowing down, is still at a higher level than the US and the Eurozone. That is something that exactly Bank of England MPC member Catherine Mann highlighted in recent statements she made, while she also noted the wider gap between headline and core CPI rates. The statements tended to highlight also the hawkish intentions of the bank and we note that the market seems to expect the bank currently, to continue hiking rates until it reaches a peak level at 5.5% (currently 4.5%) in its November meeting. We tend to agree with market expectations on this one and expect the Bank despite some dissents among its policymakers, to maintain a hawkish stance, which could provide some support against its counterparts.

JPY – BoJ: Too big to hike?

JPY is about to end the week slightly higher against the greenback and the common currency but not the pound. On the fundamental side, we expected the failed launch of North Korea’s spy satellite to provide some safe haven inflows for JPY, but the overall effect seems to have been immaterial. Nevertheless, we tend to keep a close eye over the second nature of JPY as a safe haven for the international markets and should uncertainty

be on the rise we may see JPY getting some support and vice versa next week. Also on the fundamental side, we note Japan’s decision to set aside $26 billion for childcare measures which may burden even further the heavily indebted Japanese economy. On the monetary front, we note BoJ’s extraordinary meeting, which tended to provide some support for JPY. Overall though we expect the bank to maintain its ultra-loose monetary policy settings in place for now, which in turn may weigh on the Yen. The importance of the bank’s settings on a global level, was highlighted by IMF’s warning to the bank to keep its current settings in place yet be ready to shift policy if needed. In a similar tone, the ECB warned that a possible normalization of BoJ’s monetary policy settings could strain the global bond market. On a macroeconomic level, we highlight the unexpected contraction of Japan’s industrial output and the slowdown of the retail sales growth rate, both for April, showing problems on both the production and the demand side of the Japanese economy. Furthermore, the report by Reuters that Japan’s long-term economic policy platform draft, will “strive to eradicate Japan’s long-held deflationary mindset” through bold monetary, flexible fiscal policy, could weaken the BoJ’s attempts to support the economy with its ultra-loose monetary policy, thus should the BoJ hint at a change in policy, we may see the Yen gaining, as the report is anticipated to be released on the 16th of June, which would also coincide with the BoJ’s monetary policy meeting.

EUR – Easing inflation may soften ECB’s hawkishness.

The common currency seems to end the week slightly higher against the USD for the week, yet is losing ground against the GBP and JPY, implying a degree of weakness on behalf of the EUR. A weakness that may also be related on a macroeconomic level, with the slowdown of inflationary pressures in Germany, France, Spain and the Eurozone as a whole. May’s preliminary releases tended to be telling. It was characteristic that the HICP rates slowed down in all occasions mentioned beyond market expectations, in a signal that ECB’s monetary policy tightening seems to be working. Such data may also soften the approach of some ECB policymakers which in turn may weaken the common currency further. For the time being we still see that some more rate hikes may be required by the bank, yet it’s restrictive monetary policy seems to be bringing in the desired effects, albeit at a slow pace. In the wider picture, that was also the message of ECB President Christine Lagarde in statements she made on Thursday. For the time being the market seems to expect two more 25 basis-point rate hikes by the bank and then for ECB to remain on hold for the rest of the year, something that may already have started to be priced in by the markets. On a fundamental level, we note the planned strikes in the transportation sector still threaten Europe’s substantial tourism industry, while the intentions of the German Government for the installation of Geothermal heat pumps in every home finds considerable resistance and overall fundamentals seem to weigh on the single currency.

AUD – RBA to remain on hold for now.

AUD seems to be ending the week higher than the USD. On the fundamental side and given the close economic ties between China and Australia, we still are worried about the rebound of the Chinese economy. It’s characteristic that China’s NBS manufacturing PMI figure for May remained below the reading of 50, actually dropping even lower, implying another contraction of economic activity in the Chinese giant, feeding our worries. Yet we have to note that the Caixin sister indicator for the Chinese manufacturing sector tended to show the opposite with its reading rising above 50, implying an expansion and blurring the picture. Should there be further signs of contracting economic activity in China, we may see the Aussie losing ground as Australia exports a wide amount of raw materials to China. On a macroeconomic level, we note the contraction suffered by April’s building approval growth rate, which cannot be good news for Australia’s construction sector, yet on the other hand the Capital Expenditure ticked up for Q1, showing some confidence on behalf of Australian businesses to actually invest in the Australian economy. In the coming week, we highlight the release of the GDP rate for Q1, yet another event may steal the spotlight and that is to be RBA’s interest rate decision. The bank is marginally expected to remain on hold with AUD OIS currently implies a probability of 54.58% for such a scenario to materialize. There is a high possibility of a hawkish surprise from RBA though, as the CPI rate accelerated for April and the bank is considered to be very data-dependent at the current stage. Should the bank hike rates, or even remain on hold and keep a hawkish rhetoric we may see the Aussie getting some support with anything less could weaken AUD.

CAD – BoC also to stand pat.

The Loonie appears to be gaining ground against the USD for the week. On a macroeconomic level, we note that the wide acceleration of Canada’s GDP rates beyond market expectations for Q1, supported the Loonie substantially providing a more optimistic view of the Canadian economy and boosting CAD traders’ confidence. We highlight in the coming week the release of Canada’s employment data for May and should they show further tightening of Canada’s employment market we may see the CAD gaining further support. On a fundamental level, we note that the positive correlation of the CAD with oil prices seems to have been interrupted as oil prices are about to end the week lower. On the production side of oil, we highlight OPEC+’s meeting and should the meeting result in a decision to further cut production levels, we may see oil prices getting some support and vice versa. Overall, should oil prices be on the rise next week, we may see CAD appreciating as well, given that Canada is a major oil-producing economy. On the monetary front, we highlight BoC’s interest rate decision next Wednesday and the bank is expected to remain on hold at 4.5%. CAD OIS imply currently a probability of 65.16% for such a scenario to materialize. Nevertheless, the market also expects the bank to deliver another 25 basis points rate hike in the July meeting before pausing its rate-hiking path for the year and a possible cautious tone on behalf of the bank may set market expectations into doubt, potentially weakening the CAD.

General Comment

Overall, we expect volatility to start picking up in the FX market and the USD may relent some of the initiative to other currencies, given that the frequency and gravity of high-impact financial releases stemming from the US is expected to drop. That may allow other currencies to come under the spotlight and create a more balanced blend of trading opportunities. As for the US stock markets we maintain our worries for the path of tech shares in the current AI frenzy and highlight the rise of Intel’s share price as such an example. We also note as a continuance of last week’s report that NVIDIA’s share price has started to correct lower, yet due to the weakening of the greenback and the debt ceiling crisis being averted, all major US stock market indexes, namely the Dow Jones 30 , S&P 500 and NASDAQ 100 appear to have halted their descent this week. Back in the FX market we note the weakening of the Turkish Lira that has intensified in the current week. Fundamentally Erdogan’s re-election, securing another five-year term, galvanizes the market’s expectations for a continuance of unorthodox economic policies. With inflation running at 43.68% yoy (officially), the country’s net FX reserves diving into the negatives and CBRT currently showing no willingness to raise rates, practically following Erdogan’s current wishes, there seems to be little supporting the Lira. On the other hand, we have to note that Turkey’s GDP rate accelerated beyond expectations and the industrial complex seems to be holding on, while the touristic season has begun which could provide some FX inflows over the coming months. In addition, reports by news outlets that Mehmet Simsek , may join the cabinet as the Finance Minister, implying a return to orthodox economic policies, which may provide some support for the Lira should it be confirmed by the Government over the weekend. Last but not least we note that gold’s price seems to have benefitted from the relative inactivity of the USD. Yet, overall we tend to maintain the view that the negative correlation of the USD with gold’s price may remain present in the coming week as well.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.