The week is about to end and we open a window at what the calendar has in store for the markets in the coming week. On Monday we get Switzerland’s and Turkey’s CPI rates for July, Euro Zone’s Sentix index for August and the US factory orders for June. On Tuesday, we get China’s services PMI for July, the Czech Republic’s preliminary CPI rates for July, Canada’s trade data for June and from the US the ISM non manufacturing PMI figure for July. On Wednesday we get New Zealand’s employment data for Q2 and Germany’s industrial orders for June. On Thursday, we get China’s trade data for July and Australia’s trade data for June, UK’s Halifax House prices for July, Sweden’s preliminary CPI rates for July, from the UK we get BoE’s interest rate decision, the US weekly initial jobless claims figure, from the Czech Republic CNB’s interest rate decision, and Canada’s Ivey PMI figure for July. On Friday we get Japan’s all household spending and current account balance both for June while BoJ is to release the summary of opinions for the July meeting, while from Canada, we highlight the release of July’s employment data.

USD – Trump’s trade wars to dominate

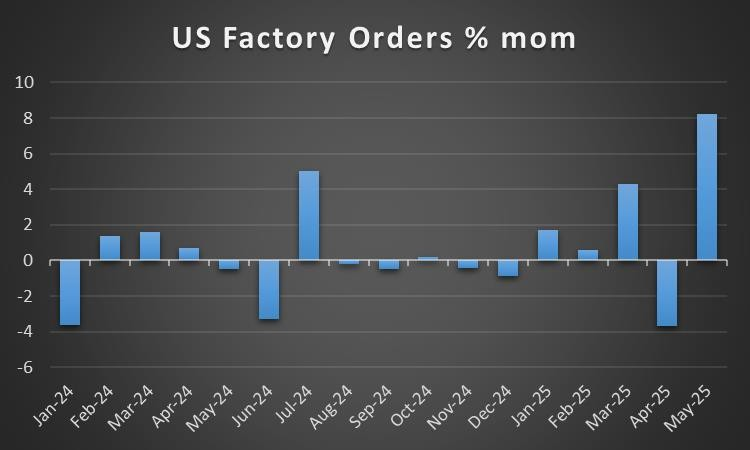

On a macro level for the USD we make a start by noting that as these lines are written the US employment data for July and the ISM manufacturing PMI figure for the same month are still to be released and could shake the markets. In the past few days though two financial releases were of interest. The first would be the release of the US GDP advance rate for Q2. The rate showed that the US economy in the past quarter grew at a faster than expected pace, which tended to lift the US macroeconomic outlook. Also the unexpected acceleration of the June PCE rates both at a a headline as well as at a core level, tended to highlight a relative resilience of inflationary pressures in the US economy. In the coming week, we expect the ISM non manufacturing PMI figure for July, to gather some interest as could also the release of June’s factory orders with both indicators providing clues regarding economic activity in the US, yet other than that the US calendar is rather empty, hence we may see fundamentals leading the greenback.

On a monetary level, The Fed’s interest rate decision was as was widely expected to remain on hold. Overall the accompanying statement and Fed Chairman Powell’s press conference provided little in regards to the bank’s intentions for the September meeting, yet we currently tend to see the case for the bank remaining on hold rather than initiating a new easing cycle. The decision tended to highlight the bank’s dilemma given the evolving international trading environment and the US tariffs. On the one hand the US tariffs may slow down economic activity and growth for the US economy, which could enhance the need for the bank to adopt a more supportive role, easing its monetary policy. Yet on the flip side, tariffs on US imports could also maintain inflationary pressures in the US economy, forcing the Fed’s hand to keep rates unchanged for longer. It’s characteristic of the split within the Fed that two voting members (Waller and Bowman) favoured a rate cut, in a sign of increasing dovish tendencies among Fed policymakers. Yet the market’s expectations for the Fed’s intentions were shifted after the release, as the market now expects the bank to proceed with only one rate cut, in October, instead of the two rate cuts (September, December) expected prior to the release. Should we see, in the coming week, Fed policymakers stressing the need for rates to remain high we may see the USD slipping as the market’s expectations may become even less dovish.

US President Trump’s tariff deadline has come to pass, and the US President intensified the tensions in the US trading relationships with various countries by passing on new tariffs. For Canada, he announced a 35% tariff instead of the earlier 25%, for Swiss products a 39% tariff was announced, also higher than the prior 31%. Canada’s PM Carney responded with disappointment for the new US tariffs, while the Swiss government has responded with “great regret” to the US decision. It should be noted that both countries were in negotiations with the US. It should also be noted that New Zealand is now facing a 15% tariff, and Australia celebrates a 10% levy as it’s considered as low as it gets. Overall, the situation is still not clear, and we may see further tensions that could shake the markets. For the time being the markets seem to be taking the tariff issue pretty well, yet given the unpredictability of US President Trump, we may have some unexpected developments on the issue that could maintain uncertainty in the markets. Analysts highlight that tariffs could average up to 20- 25% on US imports, depending on the each trade deal and volume of trade, which in turn may partially be swallowed by the exporters in reducing their prices in an effort to remain competitive and the rest being rolled over to consumer prices. Should we see an easing of trade tensions we may see the USD getting some support and vice versa.

Analyst’s opinion (USD)

“The number of high impact financial releases from the US is to be reduced in the coming week hence we expect fundamentals to lead the greenback. Should we see Fed policymakers expressing more hawkish comments we may see the USD getting some support and vice versa. On a deeper fundamental level any intensification of trade tensions, given that there are still a number of countries that have not reached a trade deal with the US could weigh on the USD, while a possible easing of trade tensions could provide support for the greenback.”

GBP – BoE expected to cut rates

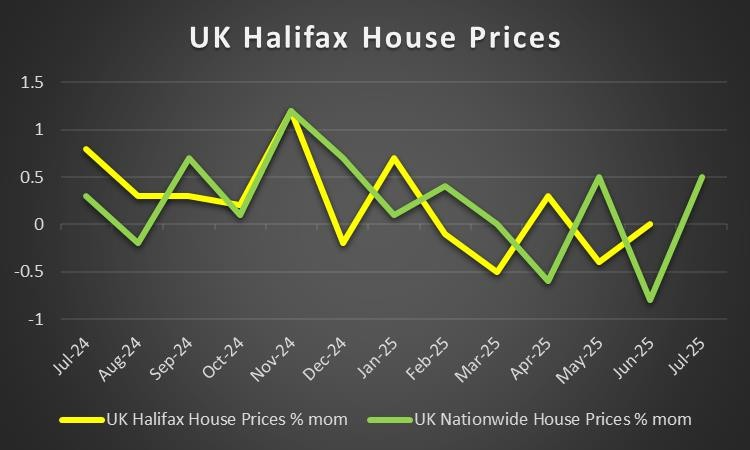

On a macroeconomic level, it’s been an easy week for pound traders, while the UK calendar is rather empty in the coming week as well. Few notable exceptions could be July’s Halifax House prices and the final PMI figures, for the services sector and the composite indicator. Hence we expect fundamentals to lead the way for the sterling.

On a monetary level, BoE’s interest rate decision is expected to draw some attention from pound traders. BoE is expected to cut rates by 25 basis points and lower them to 4.0% and currently GBP OIS imply a probability of 82% for such a scenario to materialise, while the market seems to expect another rate cut in the November meeting, before the year ends. Yet inflationary pressures intensified in the UK economy over June, which may be suggesting that the bank should exercise caution in easing its monetary policy at the current stage. UK employment data tended to be a bit mixed for May with the employment change figure reaching sky high while the unemployment rate ticked up. Should the bank cut rates as expected, market attention is expected to be placed on the bank’s forward guidance. Given that the market is leaning on the dovish side, a forward guidance with a possibly dovish tone, could enhance expectations for another rate cut thus could weigh on the pound. On the flip side, should the bank’s forward guidance be characterised by a relatively hawkish tone we may see the sterling getting some support as the market’s expectations would be contradicted and thus may force it to reposition itself.

On a fundamental level, we maintain our worries for the fiscal position of the UK Government. We may see UK’s Chancellor of the EX Chequers Reeves announcing new taxes and spending cuts as increasing debt and services costs tend to weigh. Such a development could weigh on economic activity, thus the UK economy may be entering a negative spiral on a fiscal level. Should such worries intensify among market participants, we may see the pound losing ground against its counterparts. Its characteristic that the pound is on the retreat against the common currency and the greenback for the month, while its gaining slightly against the JPY.

Analyst’s opinion (GBP)

“In the coming week, we expect fundamentals to lead the pound given the low number of high impact financial releases from the UK. BoE is expected to cut rates, which could weigh on the pound by itself, while should the bank underscore more easing to come, we may see the pound retreating further. Also the fiscal difficulties the UK Government has, could weigh on the pound should market worries about the issue intensify over the coming week.”

JPY – Market sentiment to move the JPY

On a monetary level, we note that BoJ remained on hold on Thursday as was widely expected and its characteristic that the vote was unanimous. In its Outlook for Economic Activity and Prices the bank tends to see underlying inflation as likely to stall due to slowing growth but gradually accelerate thereafter while risks to the inflation outlook seem roughly balanced. Despite the bank also noting that the risks for economic activity are skewed to the downside and that trade policies announced so far could trigger a change in the globalisation trend, we see the decision as keeping the prospect of a possible rate hike until the end of the year alive. Having said that we would also like to add that the bank seemed to be in no hurry to raise rates. Also the announcement of a US-Japanese trade deal tends to remove a substantial part of uncertainty, allowing the bank to see more clearly into the future. It’s characteristic that the market may have pushed further down the line the scenario of a rate hike, yet it still continues to price in a rate hike in the December meeting. In the coming week we highlight the release of the bank’s summary of opinions for yesterday’s meeting and should the document imply that a rate hike is still possible if not probable we may see the Yen getting some support.

On a more fundamental level, the weakening of the JPY against the USD prompted Japan’s Finance Minister Katsunobu Kato to state that officials are alarmed by currency moves. The warning may imply a possible market intervention as the exchange rate reached levels not seen since late March, yet in our opinion, for the time being, we see such a scenario as remote for now. Furthermore, we maintain our worries for the uncertainty in the Japanese political scene. Especially the latest upper house elections, signal not only the weakening of incumbent PM Ishiba’s coalition, but also the rise of the “Japanese First” Sanseito party which may prove to be a turning point for Japanese politics. Overall we tend to see the case of the Japanese Government’s fiscal policy as being in an expansionary mode, which could provide support for the JPY. Also we note that JPY’s safe haven status got a surprise inspection last week given the earthquake in Russia. Hence should we see market worries ease in the coming week we may see JPY slipping.

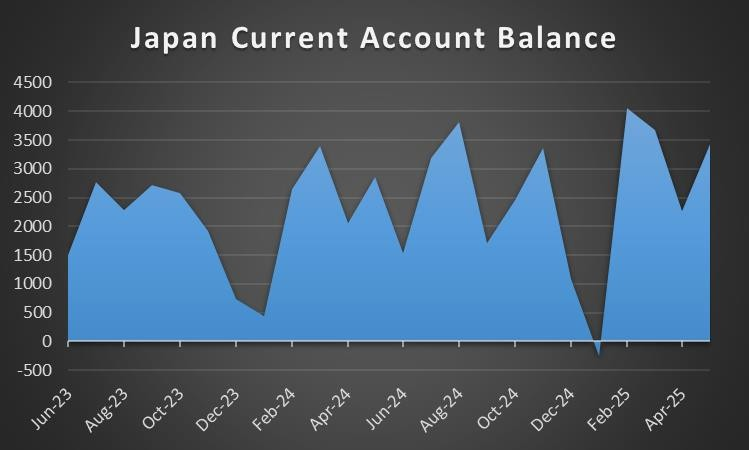

On a macroeconomic level, we note the surprise acceleration of the industrial output growth rate for June, implying wider economic activity in the sector and resilience of the demand side of the Japanese economy, given the less than expected slowing of the retail sales growth rate for the same month. In the coming week we note the final PMI figure of the services sector for July, yet our attention goes to the release of the current account balance and should the surplus widen, it could be spelling good news as it would imply a wider inflow of capital from abroad for the Japanese economy.

Analyst’s opinion (JPY)

“In the coming week we may see JPY’s status as a safe haven asset being the primary factor behind its direction, with a possible easing of the market’s worries weighing. On a monetary level, BoJ’s persistence in tightening its monetary policy may provide some support for JPY, especially if expressed in the release of the bank’s summary of opinions of its last meeting”.

EUR – EU-US trade deal weighed on the EUR

On a fundamental level, we note the agreement announced over a framework of a trade deal between the EU and the US. The agreement stipulates that EU products entering US soil will be applied a 15% tariff, while on steel, aluminum and copper a 50% tariff applies. The EU will be investing an additional $200 billion per year for the next three years and buy US energy products of $250 billion per year for the next three years. EU tariffs on US products are to be eliminated, while the EU will also work in addressing a range of US concerns on EU requirements for US products to enter the EU. For example regulations for US agricultural products are to be abolished or eased. Also the agreement stipulates that the EU and the US will address unjustified digital trade barriers and the EU will be buying significant amounts of US military equipment. The deal was perceived by the markets as being lopsided against the EU and its characteristic that the common currency has tumbled since its announcement against the USD. Overall we tend to agree with the perception of the market and see it as a possible factor weighing on the EUR. On the flip side, one should note that the EU ducked tariffs of 30% which US President Trump had threatened to impose on EU products. Yet one has to note that EU Commission President Von der Leyen had a very tough stance in the trade negotiations with China last week, which may cost the EU dearly. Overall the fundamental situation of the EU tends to weigh on the common currency, as it seems to lock out trade opportunities with China, while trade with the US is to be conducted in less favourable terms for the Union than before.

On a monetary level, we noted in last week’s report that the ECB decided to remain on hold and at the current stage the market expects the bank to keep rates unchanged until the end of the year. Should such expectations intensify, we may see the EUR getting some support, yet the situation is more complex than what may be expected. On the one hand, ECB economists highlighted the risk for downward pressures for inflation intensifying as the US- China trade war may reroute Chinese products from the US to the EU as excess production capacity may be created in Chinese factories. On the other hand, we may add, the increased imports of US energy products, which cost more, could add inflationary pressures on a headline level.

On a macro economic level, we got mixed data as on the one hand growth the preliminary GDP rate for Q2 slowed down considerably signalling that growth was anemic on a qq level the Business climate and Economic sentiment for July improved. Also the HICP rate failed to slow down for the past month, yet remains at the ECB’s target. In the coming week we note the release of the final July PMI figures for the services sector, yet we may also see some interest among EUR traders for the release of the Euro Zone’s PPI rates, Germany’s industrial orders and output as well as Euro Zone’s retail sales, all being for June.

Analyst’s opinion (EUR)

“We expect the US-EU trade deal to continue weighing on the EUR in the coming week, yet market expectations for the ECB to remain on hold may save the day for EUR traders.”

AUD – Worries for US-China trade deal

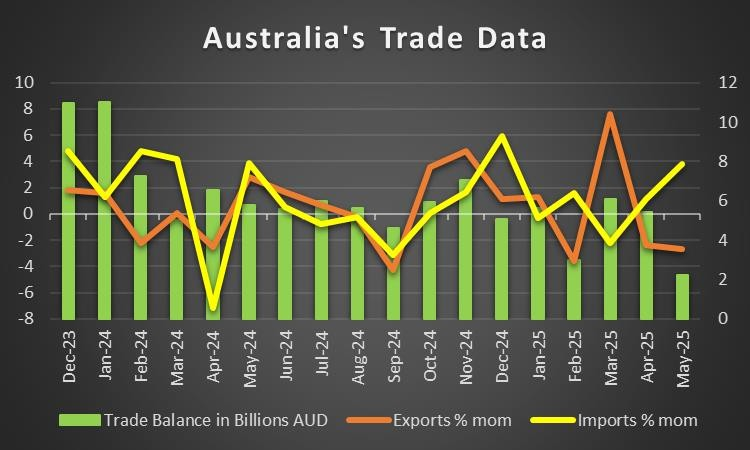

In the past week on a macro level, we note the slow down of Australia’s CPI rates for June and Q2 implying further easing of inflationary pressures in the Australian economy. Yet it should be noted that the retail sales growth rate for the same month accelerated beyond expectations implying a resilience of the demand side of Australian economy. Also for the same month, the building approvals growth rate for June, accelerated instead of slowing down as expected, reaching a stellar 11.9% mm, signalling a possible boom in the Australian construction sector. In the coming week we note the release of the final services PMI figure for July yet we intend to focus on Australia’s trade data for June, given the Australian economy’s export orientation. Should we see the trade surplus widening we may see the Aussie getting some support as it would imply more wealth entering the Australian economy from Australia’s international trading activities.

On a monetary level, we note the market’s expectations for RBA to continue cutting rates, two times more before the year ends, once in mid August and once in November. It seems that the bank intends to continue easing its monetary policy. RBA’s deputy governor Hauser welcomed the slow down of the CPI rates which tended to imply a possible more dovish predisposition by the bank. Yet he also stated that the state of the Australian employment market is still debatable and we would like to add that even with the unemployment rate rising to 4.3%, it’s still at relatively low levels, implying a relatively tight employment market. Should we see the market’s expectations for the bank to cut rates in the August meeting intensifying in the coming week, they could weigh on the Aussie.

On a fundamental level, the US tariffs tend to weigh on the Aussie as market worries for a possible slow down of trade on a global level intensify. Interest of Aussie traders may focus more on the US- Sino trade negotiations, given the close Sino-Australian economic ties. Any improvement of the US- Sino trade relationships could provide support for the AUD while a deterioration could weigh on the Aussie. For the time being news from China are not so encouraging. The manufacturing PMI figures for July tend to imply that Chinese factories are struggling for economic activity. In the coming week, we may see Aussie traders being interested in the release of China’s trade data for July, especially China’s import growth rate and a possible acceleration of the rate could provide some support for AUD. Overall the fundamentals surrounding the Aussie are currently heavily dependant by the US tariffs and as the dust settles from the passing of Trump’s tariff deadlines, should the market sentiment improve we may see the Aussie getting some support as it’s considered a riskier asset, given its commodity nature.

Analyst’s opinion (AUD)

“Should the market sentiment in the coming week improve given the passing of US President Trump’s tariff deadline, while also an improvement of the US-Sino trade could provide some support for the Aussie. Also a possible improvement of Australia’s trade data for June could also provide some support for AUD. Finally given that RBA’s meeting nears, should the market expectations for the bank to cut rates intensify we may see them weighing on AUD.”

CAD – US-Canada trade deal in focus

Maybe the main event in the past few days for Loonie traders was the release of BoC’s interest rate decision. The bank as was widely expected remained on hold, keeping the overnight rate at 2.75%. The bank’s accompanying statement tended to revolve around the US tariffs and their possible consequences on the Canadian economy and allowed for little if any clues to escape about BoC’s future intentions. We note that the bank sees the Canadian economy as showing some resilience, yet at the same time the bank proceeds carefully in regards to its monetary policy intentions. For the time being the market expects the bank to remain on hold until the end of the year. Should such market expectations intensify in the coming week, we may see the CAD getting some support.

On a fundamental level, we had noted in last week’s report that the main issue for Loonie traders is to be the US-Canadian trade negotiations. The issue is expected to continue to tantalise Loonie traders in the coming week as the stakes and uncertainty about its outcome are both at high levels. As mentioned above, the US slapped Canada with higher tariffs and Canada’s intentions to recognise a Palestinian state seem to be complicating the situation as the US President for other, political reasons is now rejecting, or viewing as the possibility of a US-Canadian trade deal as remote. On the flip side Canadian PM Carney had allready announced that negotiations could drag on beyond Trump’s tariff deadline, while also stated that some tariffs are likely. Overall, the fundamentals surrounding a possible US-Canadian trade deal, do not seem to be encouraging at the current stage and any further difficulty could weigh on the CAD, while a possible extension of the negotiations period for a deal by possibly 90 days could provide some support for the Loonie. Also we note the rise of oil prices for the week and should oil prices continue to rise in the coming week, we may see the CAD getting some support given Canada’s status as a major oil producer.

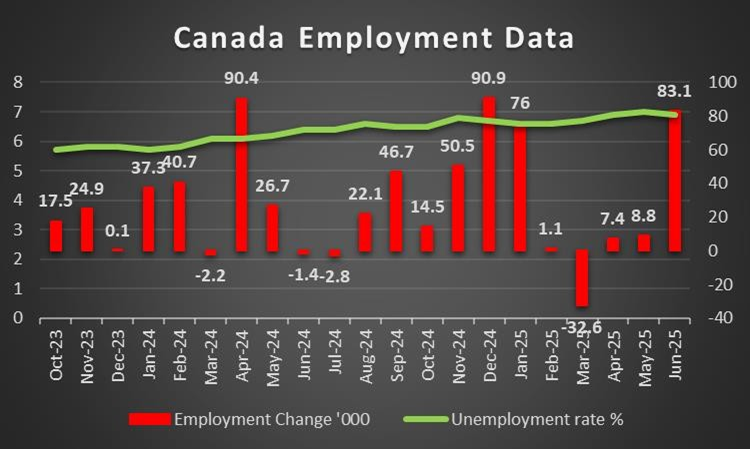

On a macro economic level, we note the release of the GDP rate for May which remained in the negatives for a second month in a row. In the coming week we note the release of Canada’s trade data for June and Ivey PMI figure for July and we highlight the release of Canada’s employment data also for July, next Friday. A possible tightening of the Canadian employment market may be encouraging for BoC to remain on hold and thus provide some support for the Loonie, while a possible cooling of the Canadian employment market could add more pressure on the BoC to ease its monetary policy.

Analyst’s opinion (CAD)

“We expect in the coming week, the US-Canadian trade negotiations to continue tantalising Loonie traders. A possible trade deal could provide some support for the Loonie depending also on its content, while a possible escalation of the trading tensions between the two neighbouring countries could weigh on the CAD. Also we note the release of Canada’s July employment data, as a possible market mover for the Loonie, and a tightening of Canada’s employment market could support the Loonie and vice versa.”

General Comment

In the coming we may see the influence of the USD over the FX market easing as US financial releases and monetary policy events are to be reduced in number and lighter than the past week. Nevertheless US President Trump’s unpredictability could keep the FX market on the edge of its seat. As for US stock markets we note the correction lower on Thursday which seems to have interrupted the bullish perspective. The earnings period is still ongoing and in the coming week we would note the release of the earnings reports of Berkshire Hathaway and Palantir on Monday, Caterpillar and Pfizer on Tuesday, McDonalds, Uber, Airbnb and Walt Disney on Wednesday as well as Ellie Lily on Thursday. As for gold, we note that the precious metal as these lines are written is going through the third week of losses with the strengthening of the USD possibly weighing at the current stage. Should we see the negative corelation being active in the coming week as well, we may see gold’s price retreating further should the USD continue to rise against its counterparts.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.