With the coronavirus claiming over 1200 lives and no end in sight, we are about to take a look in the next week. It should be noted that the confusion created by mistakes in the victim counts (i.e. double counts of deceased) or the revision in the number of people affected, caused from new diagnostic procedures seem to intensify the situation further. Virus related worries continue to affect the markets and worries also for the economic consequences seem to grow, not just for China, Australia or New Zealand but also for Europe and to a lesser or greater extent the rest of the world. On a different note, Turkey’s CBRT is to release its interest rate decision this week, and analysts are not quite sure, if the bank is about to cut rates once again. As for financial data we expect a heavy load for the coming week as a substantial number of releases are due out. Focus is expected to be on the release of the preliminary Markit PMIs for February on Friday the 21st, yet a number of other financial data which are also very important proceed them. But first things first.

USD – Fed’s minutes and financial data in focus

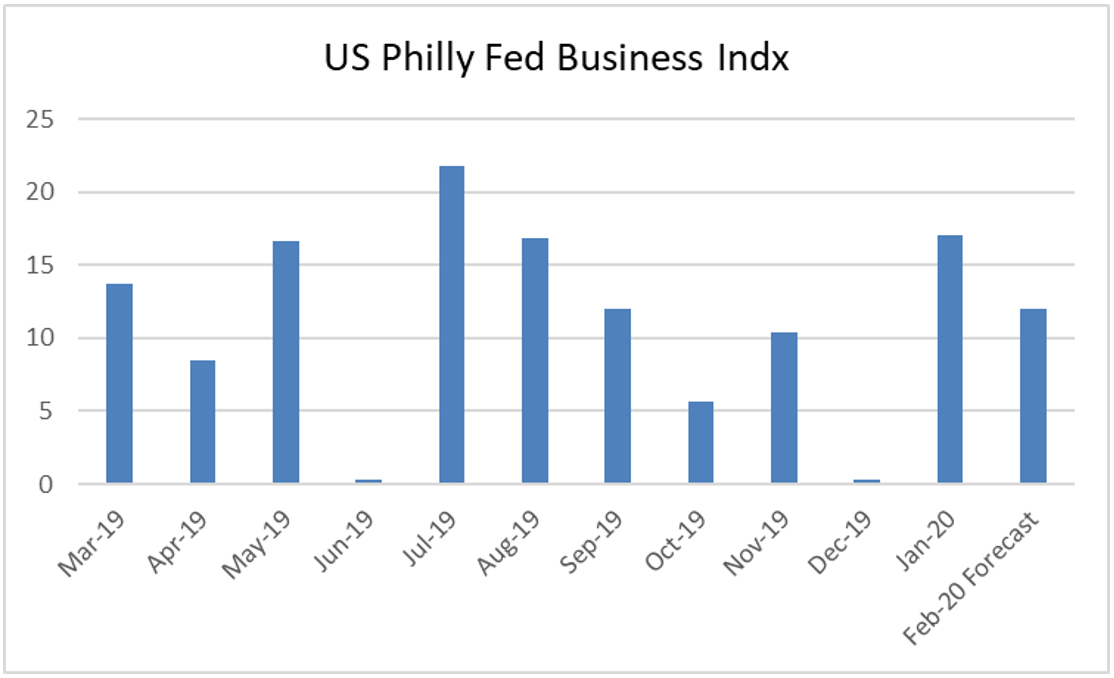

Despite the primaries of the US presidential election dominating the headlines about the US politics, the markets seem to show little effect. After the New Hampshire primary closing, Sanders seems to lead the race, while at the same time Bloomberg seems to be gaining on election dynamics and all of that with Super Tuesday set on the 3rd of March fast approaching. On the monetary front a number of speeches made by Fed officials, including Fed Chair Powell’s two day testimony at the US Congress, seemed to show content with the current US financial metrics. At the same time though, some worries have started to emerge about the effect of the corona virus and we could see the issue starting to cause some deeper worries for the US economy. Staying on monetary policy issues, Trump’s nominations to fill the two vacant seats in the Fed, were discussed in the US Congress and despite the nomination of Christopher Waller not making any severe headlines, Judy Shelton’s nomination seems to be at least controversial with even some Republican Senators having doubts on whether to approve it. It would take just one vote from the Republican camp to switch sides for her not to be approved. On the other hand, should both new members of the Fed’s Board be approved by the Senate, we could see the Fed turning more dovish as both nominees had at various times expressed such views. The issue is expected to continue to meet the headlines next week, as the US Senate will reconvene for the issue. As for next week’s monetary policy events, a number of Fed officials are scheduled to speak, yet the spotlight falls on the release of the minutes of the Fed’s last meeting. Analysts are expected to scrutinise the document for any clues about the Fed’s future intentions and a more in depth insight. Especially the Fed’s commitment for inflation to accelerate is expected to be closely examined. As for financial releases, we tend to note the New York Fed Manufacturing index for February on Tuesday, the PPI rates for January on Wednesday, the Philly Fed Business Index for February on Thursday and the Markit preliminary PMIs for February on Friday. Please note that US markets are to be closed for a public holiday on Monday.

GBP – Financial releases to guide the pound

Should we single out one political issue that shook the pound in the past few days, that would be the reshuffling of the UK Cabinet. In a characteristic move by UK’s PM Boris Johnson, resembling a tightening of political control, the UK cabinet was reshuffled and in a schocking move, Chancellor of the Ex Chequers Javid was more or less forced to hand in his resignation. Media reported that the UK finance minister Javid had to resign after his denial to remove his advisers and replacing them with officials from Johnson’s office. However we suspect that the UK Finance minister was pressed to resign as he was opposing plans for a larger fiscal stimulus which was promoted by Johnson’s close advisor Cummings. The removal of Javid as finance minister, strengthens market expectations for a wider fiscal stimulus to be included in March’s budget, possibly easing further the necessity for a monetary stimulus by the BoE. Hence, the whole event had a bullish effect on the pound and we could see any news about the expected fiscal stimulus for the UK economy playing a substantial role in GBP’s direction next week. Also, we wouldn’t be surprised to see headlines about a possible substantial corporation tax rate cut, which could also strengthen the pound. On the other hand we expect further developments in regards to the post Brexit relationships of the UK with the EU. Should there be a further hardening of the EU stance, or diverging signals from the two sides, foreshadowing tough negotiations, we could see the GBP slipping. As for financial releases, pound traders are to have a busy week ahead, as on every day, besides Monday, we get important financial data from the UK. On Tuesday, we get the UK employment data for December, on Wednesday UK’s main inflation measures for January, on Thursday UK’s retail sales growth rates for January and on Friday UK’s preliminary PMIs for February, with the Services sector PMI standing out.

EUR – Preliminary PMIs for February eyed

Germany’s politics seem to continue to be in a slump, with the race for the head position of the CDU being quite intense. The Thuringia event seem to have set the whole German political scene in doubt and political uncertainty seems to loom over Germany. As for the macro economic aspect of Germany and the euro-area, recent releases relating to growth and manufacturing output disappointed the markets as they underperformed market expectations, or where rather lukewarm. The weakening of the common currency especially against the USD, was characteristic. The market seemed to be focusing on worries on the extensive slowdown of the German economy. Please note that Germany is considered the economic powerhouse for the trading block. At the same time it should be noted that worries seem to extent to other economies of the area such as France and Italy. Also, the corona virus effect for the Eurozone cannot be reliably measured at the time, yet we expect the hit to be substantially adverse for the Eurozone. As for the monetary policy front, ECB’s President Lagarde, seemed to defend the bank’s low rate policy in her speeches over the past few days. A characteristic comment made was that inflation remains some distance below the bank’s medium-term aim. The comment underscored the bank’s resolvenes to remain accomodative as long as inflation does not substantially acceleerates to meet the bank’s target. As for next week, a number of speeches is scheduled, however we will also be keeping an eye out for the meeting where the 27 EU countries will meet to discuss the 2021-2027 budget. Especially any hints for a possible fiscal stimulus could provide a boost for the common currency on Thursday. As for financial releases we expect the preliminary PMIs of Germany, France and the Eurozone as a whole, for February on Friday to catch EUR-traders eyes. Should the PMIs show a wider contraction and/or slowdown of economic activity for the area, we could see the common currency slipping further. Special attention as usual is expected to be placed upon Germany’s manufacturing sector. However before that, we get Germany’s ZEW economic sentiment for February on Tuesday, while on Thursday we get Eurozone’s flash consumer sentiment also for February.

AUD – RBA minutes and employment data to move the Aussie

The Aussie seems to be recovering after last Friday’s hit and poised to close higher for the week against the USD. Corona virus worries seem to continue to dominate the AUD’s direction. Should the negative headlines about the issue contninue to reel in we could see the Aussie starting to weaken once again. For the coming week we tend to focus on the RBA’s minutes which are due out on Tuesday’s Asian session. After the statements made by RBA’s governor, which practically lifted the bar for any possible future rate cuts as well as the more optimistic tone of the accompanying statement of RBA’s latest interest rate decision, market analysts are expected search the document, for what would make the bank actually tick or bring a possible rate cut nearer. Also it should be noted that on Wednesday we get Australia’s first labour data release with the wage price index for Q4, while on Thursday the employment change figure and the unemployment rate both for January are due out. Given the wheight that RBA has placed on the labor market we could see the releases gaining on attention. Also on Fridays’ Asian session, we get Australia’s PMIs for February.

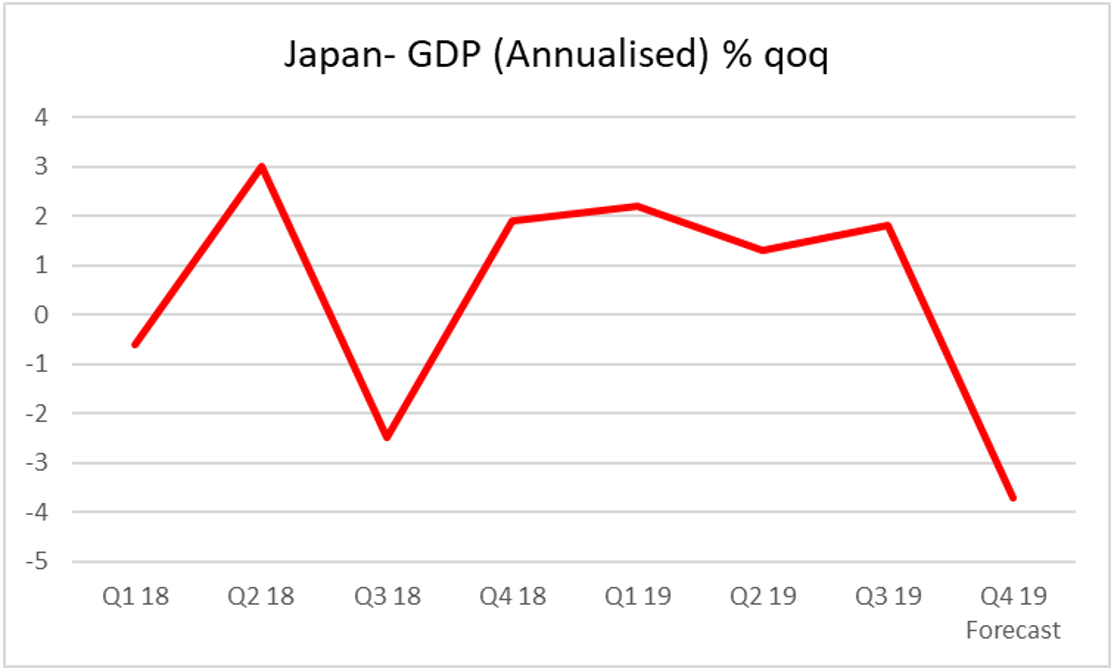

JPY – Safehaven flows and financial releases affecting JPY’s direction

JPY stabilised over the past few days, against the USD, indicating that safehaven inflows may have weakened somewhat. However as the news broke out that China had in fact a far higher number of patients infected with the Coronavirus than initially mentioned, the Japanese currency spiked, during Thursday’s Asian session. The incident served as a painfull reminder of the seriousness of the situation of the Coronavirus and at the same time the role of the Japanese currency as a safe haven. We expect that the issue is to contninue to create turbulance for JPY, also in the coming week as further developments seem to be on the way and could affect JPY’s direction either way, depending on the news. Also statements made by BoJ officials are not be underestimated, as in the past few days, indicated increased worries on the bank’s behalf for the effect of the coronavirus on the Japanese economy. It should be noted that comments were made also for the Monday’s GDP growth rate releases by implying that Japan’s Q4 2019 GDP may have contracted sharply due to overseas slowdown, sales tax hike impact and hit from natural disasters. Should that be the case, then we could expect a nasty surprise for JPY traders on Monday’s GDP release. Yet JPY traders will have a quite busy week as besides the release of the GDP growth rates for Q4 on Monday, we will also get the machinery orders growht rate for December on Wednesday, along with January’s trade balance and on Friday January’s inflation rates along with the preliminary Jibun manufacturing PMI for February.