As the week draws to a close, markets have kickstarted their engines and are now in full swing. We note the high number of financial releases in the next week. Making a start on Monday, with the release of Sweden’s CPI rate for December, Germany’s Full Year GDP rate for 2023 and Canada’s manufacturing sales rate for November. On Tuesday, we note Japan’s corporate goods price rate for December, Norway’s GDP rate for November, Germany’s ZEW indicators for January and Canada’s BOC Core CPI rates for December. On Wednesday we note China’s industrial output rate for December and their GDP rate for Q4.

Later on, we note the UK’s CPI rate the US Retail sales rate, Canada’s producer prices rate and the US industrial production rate all for the month of December. On Thursday, we note Japan’s machinery orders rate for November, Australia’s employment data for December, the US weekly initial jobless claims figure and the US Philly Fed business index figure for January. On Friday, we note Japan’s Core and Headline CPI rates for December, followed by the UK’s retail sales rate for December, Canada’s retail sales rate for November, the US Preliminary University of Michigan consumer sentiment figure for January and ending off the week is the Eurozone’s preliminary consumer confidence figure for January. As the week draws to a close, markets have kickstarted their engines and are now in full swing.

We note the high number of financial releases in the next week. Making a start on Monday, with the release of Sweden’s CPI rate for December, Germany’s Full Year GDP rate for 2023 and Canada’s manufacturing sales rate for November. On Tuesday, we note Japan’s corporate goods price rate for December, Norway’s GDP rate for November, Germany’s ZEW indicators for January and Canada’s BOC Core CPI rates for December. On Wednesday we note China’s industrial output rate for December and their GDP rate for Q4.

Later on, we note the UK’s CPI rate the US Retail sales rate, Canada’s producer prices rate and the US industrial production rate all for the month of December. On Thursday, we note Japan’s machinery orders rate for November, Australia’s employment data for December, the US weekly initial jobless claims figure and the US Philly Fed business index figure for January. On Friday, we note Japan’s Core and Headline CPI rates for December, followed by the UK’s retail sales rate for December, Canada’s retail sales rate for November, the US Preliminary University of Michigan consumer sentiment figure for January and ending off the week is the Eurozone’s preliminary consumer confidence figure for January.

USD – CPI rates prove inflationary pressures remain in the US economy

The USD seems about to end the week relatively unchanged against its counterparts. On a fundamental level, we note that the Iowa Primaries for the Republican party are due to take place on the 15th of January, effectively kicking of the election season in the USA. On a monetary level, we highlight the speech by New York Fed President Williams on Wednesday in which he stated that the Fed’s monetary policy is restrictive enough to bring inflation down to the Fed’s 2% target. Moreover, he stated that “we will need to maintain a restrictive stance of policy for some time”, which could dampen the market’s expectations of 6 rate cuts by the Fed this year.

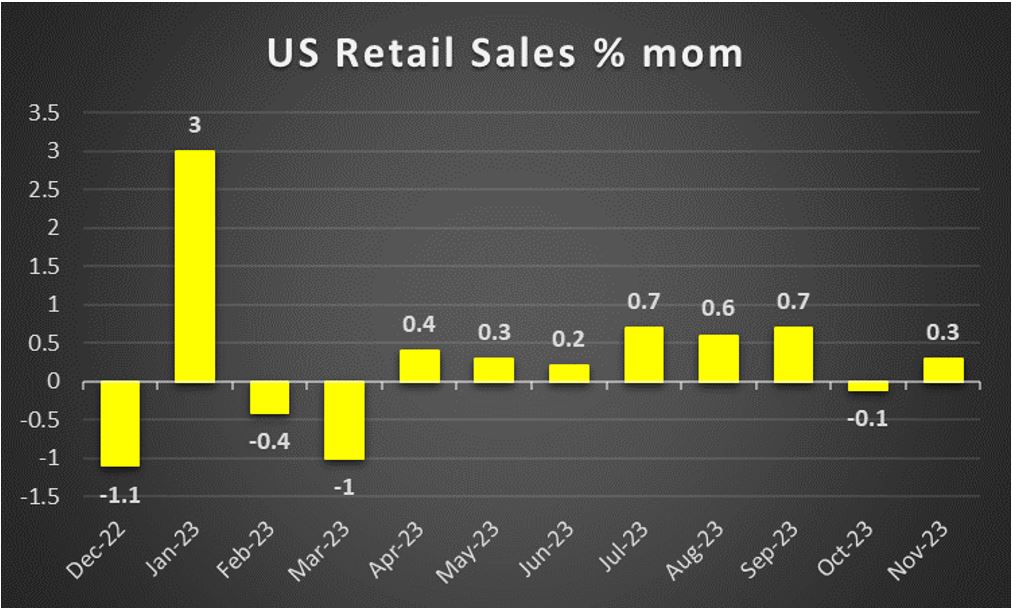

Yet, the relatively hawkish comments appear to have been widely ignored by the market, once again highlighting the market’s divergence from Fed officials. On a macroeconomic level, we note that the US CPI rates for December both Headline and Core rates came in higher than expected, implying persistent inflationary pressures in the US economy. Moreover, the initial weekly jobless claim figure came in better than expected, implying a tight labour market and lastly, the US trade balance figure for November came in higher than expected implying a resilient economy. All signs point to higher economic activity and persistent inflationary pressures for the US economy. Yet the higher CPI rates barely provided support for the greenback, a divergence we must point out.

GBP – BoE Bailey hints at persistent inflationary pressures

The pound is about to end the week higher against the USD, GBP and JPY in a sign of wider strength. On a fundamental level, we note that the UK Government has decided to exonerate wrongly convicted post office scandal victims, who were prosecuted for accounting errors relying on data from faulty Horizon software. On a monetary level, we note that BoE Governor Bailey stated that UK household incomes have risen in recent months and that those factors could mitigate the impact of higher rates.

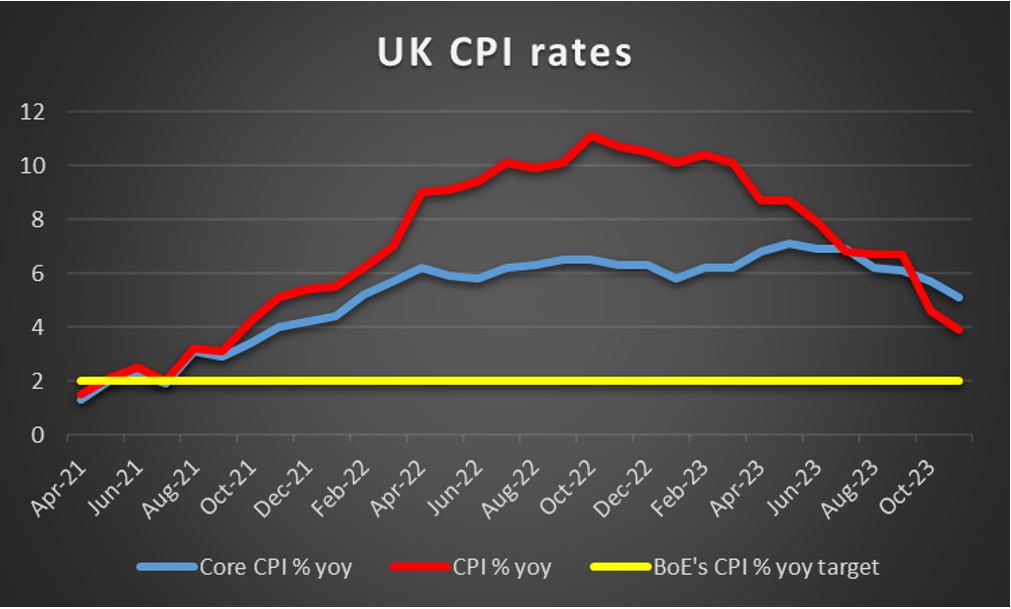

Therefore, should household income increase, we may see the BoE adopting a more hawkish stance, potentially discussing once again the possibility of a rate hike. Such a scenario could support the pound, whereas should wage pressures ease, we may see the pound weakening. On a macroeconomic level, we note the UK GDP rates for November, which came in better than expected, implying an expansion in economic growth, which may provide support for the pound. Lastly, traders may be interested in next week’s December CPI rate for the UK. Should the rate imply persistent inflationary pressures we may see the pound gaining and vice versa.

JPY – BoJ interest rate decision in sight

JPY is losing ground across the board in a sign of broader weakness. On a fundamental level, according to the Japan times, the government is facing some backlash from the opposition for its response to the 7.6 magnitude earthquake. Yet according to polls conducted by the JNN television network, 57% of respondents said the government’s reaction was speedy with only 32% expressive a dissenting opinion.

Nonetheless, we note that Japan’s Tokyo CPI rates for December came in as was expected at 2.1% implying that inflationary pressures in the Japanese economy may be easing. As such, we may see a hesitation from the BOJ’s side to adopt a more hawkish tone, as inflation may not remain above the bank’s target in a sustainable manner. Moreover, a prerequisite according to BOJ Governor Ueda for the bank to abandon its ultra-loose monetary policy was an increase in real wages, yet following the overall wage income of employees figure for November which came in much lower than expected at 0.2% compared to the expected rate of 1.5%, it could weaken the bank’s ambitions to normalize their monetary policy.

In addition, the household spending rate for November decreased and entered negative territory which could spark concern about the economic resilience of the Japanese economy. In conclusion, the aforementioned factors could force the bank’s hand to maintain their current ultra-loose monetary policy, which could weigh on the JPY. Lastly, traders may look at next week’s December CPI rates for Japan, and should they validate that inflationary pressures are easing in the economy, it could further weigh on the Yen. Whereas, should they contradict the Tokyo CPI rates, the release could provide some support for the Yen.

EUR – Fundamentals to lead the way

As the end of the week nears the EUR tends to gain slightly against the USD and JPY, yet is losing some ground against the GBP. On a monetary level, for the time being, ECB policymakers tend to signal a steady policy in January, yet that was already expected by the market. The interesting element may have been that ECB policymakers view the scenario that the Eurozone may have suffered a further contraction of its economy in Q4 2023, implying the possibility of a technical recession in the second half of the past year.

ECB Vice President De Guindo’s comments were indicative as he stated “Soft indicators point to an economic contraction in December too, confirming the possibility of a technical recession in the second half of 2023 and weak prospects for the near term,”. Despite the weak outlook, ECB Board Member Schnabel stated that talk of lowering European Central Bank borrowing costs is premature at this stage, as reported by Bloomberg, contradicting market expectations for extensive rate cuts in 2024.

On a macroeconomic level, we note that the Eurozone’s business climate for December continues to drop deeper into the negatives, yet on the positive side, investors and analysts tend to maintain a less pessimistic outlook for the Eurozone in the next six months. On the inflationary front, we note that the acceleration of France’s HICP rate for December, as noted in the preliminary release was reaffirmed, something that we expect to be the case also for Germany but for the Eurozone as a whole too. In turn, the higher HICP rates may allow the ECB to maintain its narrative for a delay in any rate cuts and thus support the EUR. In the coming week given the lack of high-impact financial releases stemming from the Eurozone, fundamentals to lead the way for the common currency.

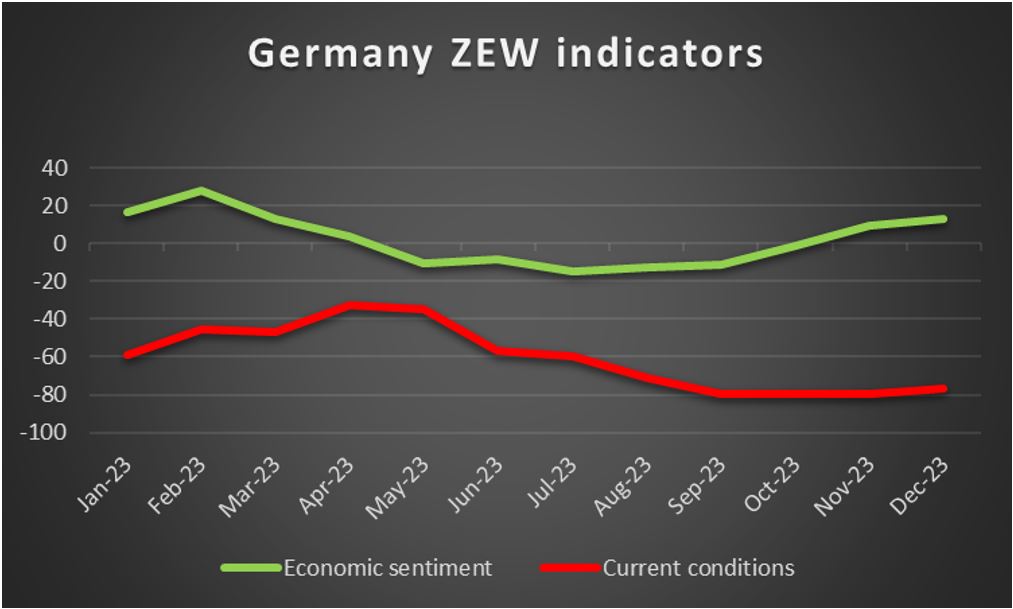

Notable exceptions to that could be Germany’s full-year GDP rate for 23 and January’s ZEW indicators as well as the Eurozone’s preliminary consumer confidence for January as well.

AUD – December’s Employment data in focus

AUD is about to end the week relatively unchanged against the USD. On a macroeconomic level, we make a start by noting that Australia’s CPI rate slowed down to 4.4% yoy for November, which tends to corroborate RBA’s narrative that monetary policy is at sufficiently restrictive levels to ease inflationary pressures further, yet also implies that there is still lots of work to be done. Also, we note the substantially higher–than–expected trade surplus figure for November as it rose to 11.437 billion AUD.

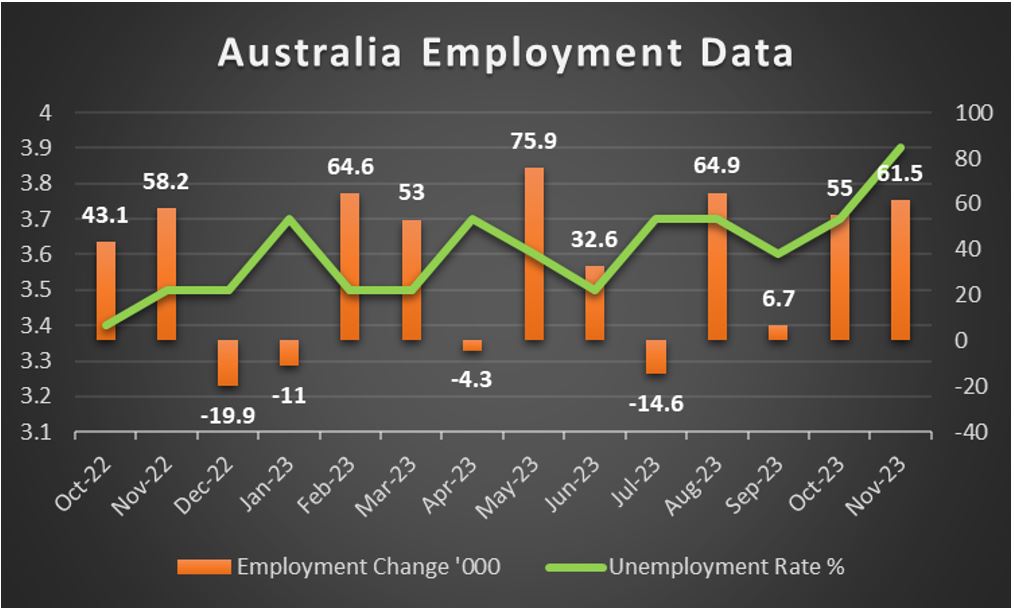

The release highlighted how the Australian economy benefited from its international trading activities in the particular month, with the import growth rate dropping deep into the negatives and the export growth rate accelerating. In the coming week, we highlight the release of Australia’s employment data for December and should they show a rather tight Australian employment market, we may see the Aussie getting some support and vice versa. On a more fundamental level, we note the elections in Taiwan, tomorrow Saturday, as a possible risk factor for the Aussie. Should the incumbent DPP win the elections we may see tensions in the Sino-Taiwanese relationships intensify, which in turn could weigh on the Australian Dollar given the close economic ties of Australia with China.

Furthermore, we note that should the market turn more cautious the Aussie may continue weakening as it is considered a riskier asset given its second nature as a commodity currency. On a monetary level, we note the market’s expectations for the bank to start cutting rates in the summer months and deliver two rate cuts in total for the year, far less than what other central banks such as the Fed, ECB and BoE are expected to deliver, which in turn may keep the Aussie supported on a monetary level in the first quarter of 2024.

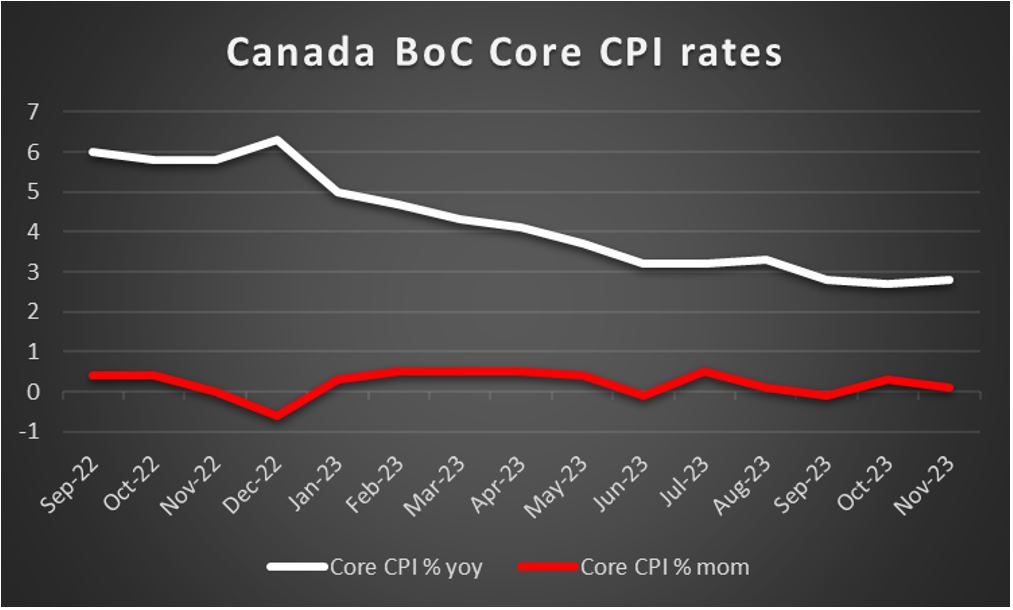

CAD – December’s CPI rates in the epicenter of attention

The Loonie is about to end the week relatively stable against the USD. On a macroeconomic level, we note the wide contraction of the building permits growth rate for November, spelling bad news for Canada’s construction sector.

Furthermore, we note the narrowing of the trade surplus in November, which tends to underscore how the Canadian economy benefitted less from its international trading activity. In the coming week we highlight the release of December’s CPI rates. Should the rates continue to fail to slow down on a headline and core level, or even accelerate, we may see the CAD getting some support as it would allow the BoC to remain on hold for longer.

For the time being, we note that the CPI rates are nearing the bank’s target range of 2.00±1.00%, and we still see the case for the bank to delay any rate cuts. It’s characteristic that in a recent speech BoC Governor Macklem, stated that 2024 is to be a transitionary year, recognized the need for the bank to start cutting rates, yet also stressed that BoC policymakers need to see “not one or two months” but “a number of months” of deceleration in underlying inflation before considering cutting rates, as reported by Bloomberg.

On a fundamental level, we note Loonie’s sensitivity to the market sentiment, given that as a commodity currency, it is considered a riskier asset. Furthermore, given Canada’s status as a major oil-producing economy, we may see oil prices playing a key role in the Loonie’s direction in the coming week.

For the week oil prices seem about to end the week relatively stable yet tensions in the Middle East and especially in the Red Sea stoke concerns of oil market participants for the possibility of a tight supply. Should oil prices be able to escape the boundaries of the past few weeks, to the upside, we may see the CAD getting also support.

General Comment

Overall we expect in the coming week the USD to continue leading the charge over other currencies, given the frequency and gravity of US financial releases. Moreover, we expect volatility to pick up regarding US stock markets given the earnings season. In the coming week, we highlight the release of the earnings reports of Morgan Stanley (#MS), and Goldman Sachs (#GS), on Tuesday and note Alcoa (#AA) on Wednesday and on Friday Travelers (#TRV). Overall interest in US equity markets may get a boost as the headlines in media about the earnings reports released reel in.

As for gold, we note that despite some recovery in the past two days, its price is about to end the week in the reds. The uniform drop of US yields, both in long-term and short-term bonds on Thursday, may have been the main factor allowing for gold’s price to recover some ground, yet it may prove to be too little, too late for gold’s bulls. Also, we note that the negative correlation of the precious metal to the USD seems to have been interrupted in the current week yet we may see it being the main factor behind gold’s movement in the coming week.

이 기사와 관련된 일반적인 질문이나 의견이 있으시면 저희 연구팀으로 직접 이메일을 보내주십시오 research_team@ironfx.com

면책 조항:

본 자료는 투자 권유가 아니며 정보 전달의 목적이므로 참조만 하시기 바랍니다. IronFX는 본 자료 내에서 제 3자가 이용하거나 링크를 연결한 데이터 또는 정보에 대해 책임이 없습니다.