The week is coming to an end and we open a window at what next week has in store for the markets. On Monday we make a start with Japan’s machinery orders rate for November and Canada’s 1YR and 5YR loan prime rates for January. On Tuesday we get the UK’s employment data for November, followed by the Zone’s and Germany’s ZEW figures for January, Canada’s CPI rate for December and New Zealand’s CPI rate for Q4.On Wednesday we note the start of the World Economic Forum. On Thursday, we get Japan’s trade balance for December, the UK’s Nationwide house prices rate for January, Norway’s interest rate decision, Turkey’s interest rate decision, the US weekly initial jobless claims figure, Canada’s retail sales rate for November and the Zone’s preliminary consumer confidence figure for January. On a busy Friday, we note Australia’s preliminary manufacturing PMI figure for January, Japan’s CPI rates for December and preliminary manufacturing PMI figure for January, followed by the BOJ’s interest rate decision, Sweden’s preliminary GDP rate for Q4 and unemployment rate for December, France’s preliminary services PMI figure, Germany’s preliminary manufacturing PMI figure the Eurozone’s preliminary composite PMI figure, the UK preliminary manufacturing PMI figure, the US preliminary manufacturing PMI figure and lastly the UoM final consumer sentiment figure all for the month of January.

USD – Trump’s inauguration on Monday

On a political level, President-elect Trump’s inauguration is set to occur on Monday the 20th of January. We note the release of the US CPI rates for December this week. Despite the confirmation of the headline CPI rate accelerating from 2.7% to 2.9%, the Core CPI rate came in lower than expected at 3.2% versus 3.3%. The lower-than-expected Core CPI rate, tended to take the spotlight as it could allow the Fed to cut rates earlier than expected, as seen by the adjusted Fed Fund Futures which currently implies a rate cut by the Fed in May rather than September. In our view, the lower-than-expected Core CPI rate is a positive indication for the Fed’s progress against inflation, yet is not definitive as both readings remain above the Fed’s 2% inflation target. For next week for dollar traders we would like to point out the release of the US preliminary S&P manufacturing PMI figure, which may provide greater insight into the current situation of the manufacturing sector of the economy. We would also like to note that the incoming administration may dictate the dollars direction in the coming week, as their comments and potential policies could have significant effects on the dollar.

GBP – Manufacturing PMI figures next week

The UK’s CPI rates for December were released earlier on this week. The headline rate came in lower than expected at 2.5% versus 2.6%, implying easing inflationary pressures in the UK economy. Moreover, the UK’s GDP rate for November and Industrial production rate for the same month came in also lower than expected. Overall, this week’s financial releases for the UK tend to paint a concerning picture for the economy and thus could amplify calls for the BoE to cut rates in their February meeting and to potentially continue cutting rates during the year. In particular, GBP OIS currently implies an 84.2% probability for the bank to cut rates by 25 basis points in their February meeting. Moreover, aiding to the narrative may be BoE deputy Governor Breeden who spoke earlier on this week and in her remarks noted that “inflation has fallen materially over the past year”. In our view if next week’s preliminary manufacturing PMI figure for January continues to show a contraction in the manufacturing sector, it could further amplify calls for a more aggressive rate-cutting cycle by the BoE in an attempt to aid the economy. In turn, this may weigh on the pound should such a scenario occur. Yet, in the event that the manufacturing PMI figure for January comes in higher than expected, it may cast doubt on our aforementioned hypothesis which in turn could aid the GBP.

JPY – BOJ decision next week

The main event for Yen traders in the upcoming week, may be the BOJ’s interest rate decision on Friday. The majority of market participants are currently anticipating the bank to hike by 25 basis points, with JPY OIS currently implying a 79.13% probability for such a scenario to materialize. Furthermore, BOJ Governor Ueda stated according to Reuters that the bank “will discuss whether to raise interest rates at the next week’s policy meeting”, which appear to have echoed remarks by BOJ Deputy Governor Ryozo who implied that interest rates remaining at their current levels would “not be normal”. In turn it appears that BOJ policymakers may be inclined to hike interest rates in their meeting next week, and as such we would not be surprised to see such a scenario occurring, which may aid the JPY. On a macro-economic level, next week may be of interest for Yen traders, with the release of Japan’s CPI rates for December on Friday, which are set to be released prior to the banks decision. As such, a hotter than expected inflation print, could pressure the BOJ to pump the breaks on a potential rate hike, or potential adopt a slight dovish tone. Whereas, an inflation print which could imply that the inflation is on its way down to the bank’s 2% target, could provide the BOJ with greater confidence for a rate hike.

EUR – ECB appears poised to continue cutting rates in 2025

For the Eurozone, we must make a start by discussing the recent comments made by some ECB policymakers. Specifically we would like to note the comments made by ECB Villeroy and ECB Chief Economist Lane. Starting with ECB Villeroy, who has stated according to Bloomberg that “it makes sense to cut rates to 2% by summer”, essentially providing a clear rate cutting path for the ECB in their upcoming meetings in his view. Furthermore, ECB Chief Economist Lane earlier on this week implied that the potential easing of inflationary pressures could justify further rather cuts, yet the bank was not in a position to make a promise. Overall, it appears that the rhetoric emerging from ECB policymakers, may be dovish in nature which in turn could weigh on the common currency ,should that rhetoric continue to be echoed. In terms of financial releases, the French and German CPI rates confirmed an acceleration of inflationary pressures in their respective economies. However, despite the acceleration, inflation remains near the banks 2% target and thus should further readings confirm our aforementioned scenario, it could weigh on the EUR, as the “doves” within the ECB may gain further confidence to continue on their rate cutting approach. For next week we would like to note the release of the preliminary manufacturing PMI figure from Germany, France’s preliminary services PMI figure and the composite PMI figure for the Zone. These three financial releases may be crucial for the EUR, given the significant contributions made by the French and German economies to the Eurozone. Hence a continued or even wider contraction, may spell trouble for Eurozone and could lead the ECB on a more aggressive rate cutting approach. On the flip side, should the figures come in higher than the prior readings, it may ease concerns regarding the Eurozone’s economic outlook and could thus aid the EUR.

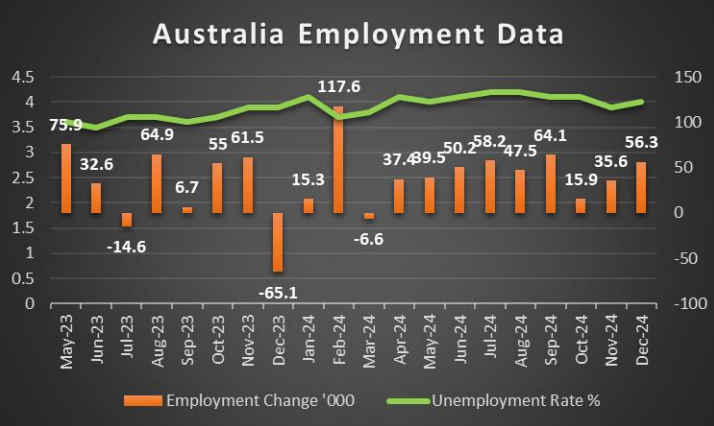

AUD – Employment data released earlier on this week

On a macroeconomic level we note the release of the Australian employment data for November this past Thursday. The employment data showcased a mixed labour market, with the unemployment rate increasing from 3.9% to 4.0%, yet the employment change figure for December significantly exceeded expectations by coming in at 56.3k versus 14.5k. The higher-than-expected employment change figure may have aided the Aussie, yet we remain concerned about the uptick in the unemployment rate. In particular, the mixed employment data could increase pressure on the RBA to remain on hold in their next meeting. Our justification is that the labour market remains relatively tight as seen by the unemployment change figure, yet not tight enough to mandate a possible rate hike as the unemployment rate increased by 0.1%. At the same time, the data in our view may not provide substantial confidence to the RBA should they decide to cut rates. As such traders may be looking towards next week’s preliminary manufacturing PMI figure for January, in order to acquire a better picture of the state of the Australian economy. Hence, should the figure come in higher than the prior reading of 47.8, it may increase pressure on the RBA to adopt a wait and see approach which in turn could aid the Aussie. On the flip side, a wider contraction could increase pressure to cut rates in an attempt to aid the manufacturing sector which could weigh on the AUD.

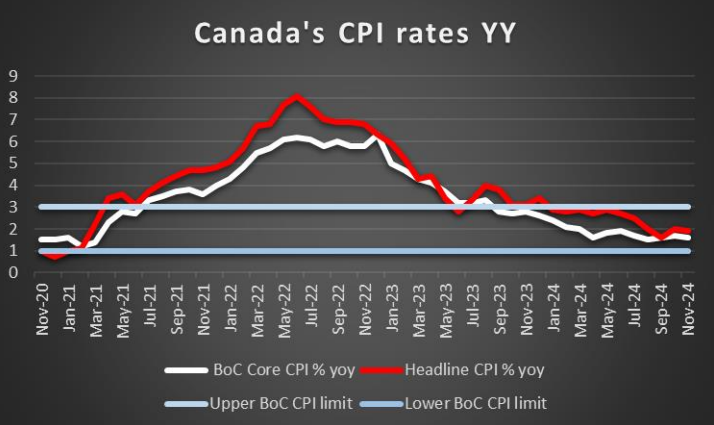

CAD – Canada gearing up for a trade war with the US?

Before diving into the possible tit-for-tat tariffs between Canada and the US as stated by our title, we must first look at what the market had in store for Loonie traders this week. The financial releases stemming from Canada where bleak this week, with nothing major to note however next week may be slightly more interesting as we get Canada’s CPI rate for December and retail sales rate for November. Focusing on the CPI rates should the release showcase an acceleration of inflationary pressures in the Canadian economy, it could dampen the current market expectations of a rate cut by the BoC in their January meeting, as seen by CAD OIS which currently implies a 71.2% possibility for the bank to cut 25 basis points. Such a scenario could aid the Loonie and vice versa. Moving to the political developments this week, Canada appears to be preparing for a tit-for-tat tariff war with the US, if President-elect Trump follows through on his comments to impose a 25% tariff on all Canadian imports into the US. If such a scenario unfolds after Trump’s inauguration on Monday, it may spark concerns in regards to the resilience of the Canadian economy and could thus weigh on the CAD. On another note, oil prices have risen for another week and thus may provide some support to the CAD given the nation’s status as an oil exporter.

General Comment

Overall we expect the dominance of the USD over the FX market to continue in the coming week, with President Trump’s inauguration date set for Monday. Financial releases may be the stage at certain points, but the new administration’s actions may take precedent and thus the dollar may continue dominating the FX markets.As for US stockmarkets, all three major indexes appear to be ending the week in the greens, yet we maintain some concern. As for gold, we note that the precious metal’s price appears to be ending the week in the green’s for a third week in a row. On a geopolitical level, we would like to note that Israel and Hamas appear to have agreed to a ceasefire deal in principle, yet until we see an actual document and the upholding of such a ceasefire, we remain very sceptical as to whether or not it will be maintained.

이 기사와 관련된 일반적인 질문이나 의견이 있으시면 저희 연구팀으로 직접 이메일을 보내주십시오 research_team@ironfx.com

면책 조항:

본 자료는 투자 권유가 아니며 정보 전달의 목적이므로 참조만 하시기 바랍니다. IronFX는 본 자료 내에서 제 3자가 이용하거나 링크를 연결한 데이터 또는 정보에 대해 책임이 없습니다.