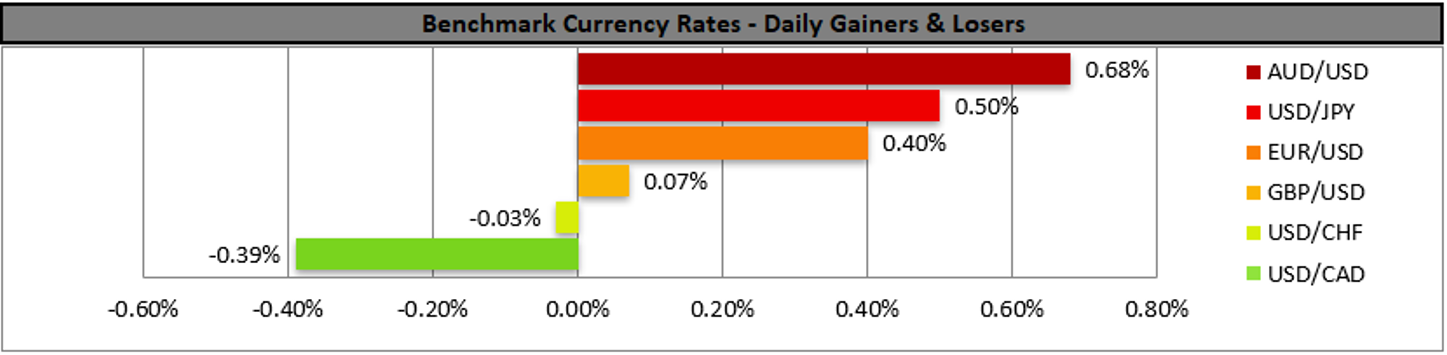

The USD remained relatively unchanged yesterday against its counterparts, as the release of the US inflation report for February failed to excite traders and create substantial volatility. Overall, market forecasts for the slowdown of the CPI rates for February were realised as expected, which in turn may be adding more pressure on the Fed to ease its aggressive rate hiking path, yet we would note that despite the slowdown, inflationary pressures are still strong and thus may maintain the bank’s hawkishness. For the time being the market seems to be pricing in the possibility of a 25-basis points rate hike and Fed Fund Futures imply a probability of 80% for such a scenario to materialize, which is quite lower than a possible 50 basis points rate hike discussed last week. On a more fundamental level, the market worries for a possible contagion of the SVB fallout to the rest of the market seem to be contained at least for now, as all three major US stock market indexes, Dow Jones, S&P 500 and Nasdaq ended their day in the greens, yet the situation is still fragile and the possibility of another bank break down, which could reignite the market’s worries cannot be excluded. Across the pond, we note that the pound found little support from the release of the UK employment data which tended to show that the UK employment market remains tight.

It was characteristic that the unemployment rate remained unchanged at 3.7%, failing to tick up as expected while the employment change figure dropped yet remained above market expectations. Overall, the data may allow BoE to maintain a hawkish stance and proceed with another rate hike next week, as the market expects, yet the catalyst may prove to be the release of the UK CPI rates for February next Wednesday. Across the world, Chinese data showed that economic activity growth rates for February in the industrial sector accelerated, yet were below market expectations, while the urban investment and retail sales growth rates for the same month were also in the greens. Overall, it seems that the Chinese industrial sector got off with a good reopening and is supported also by strong internal demand, which may act as a pillar for the continuance of growth in the Chinese economy and Aussie traders are to keep a close eye on developments, yet AUD may be more influenced by Australia’s February labor data early tomorrow. Also please note that JPY tended to weaken as BoJ Governor Kuroda, stated that the bank must maintain its ultra-loose monetary policy, yet today JPY traders may be on the lookout for any headlines regarding wage negotiations in Japan. A possible substantial increase in wages could continue feeding inflationary pressures and thus support JPY.

USD/JPY rose yesterday yet seems to have hit a ceiling at the 134.80 (R1) resistance line. For the time being, we maintain our bias for a sideways movement given also that the RSI indicator is at the reading of 50. For a bullish outlook, we would require the pair to clearly break the 134.80 (R1) level and aim if not meet the 138.15 (R2) line. Should the bears take over, we may see the pair reversing course and aiming for the 131.40 (S1) support line. AUD/USD was continuously testing the 0.6695 (R1) resistance line yesterday and during today’s Asian session. There seem to be some bullish tendencies for the pair as evidenced by the ascending wedge which the price action has formed over the past 48 hours. Yet, for a bullish outlook we would require the pair to clearly break the 0.6695 (R1) resistance line and aim if not breach 0.6785 (R2) resistance level that served as the upper boundary for the pair’s sideways motion from the 24 of February to the 7 of March. Should the bears take over we may see the pair breaking the upward trendline of the wedge and aim if not breach the 0.6590 (S1) support line.

금일 주요 경제뉴스

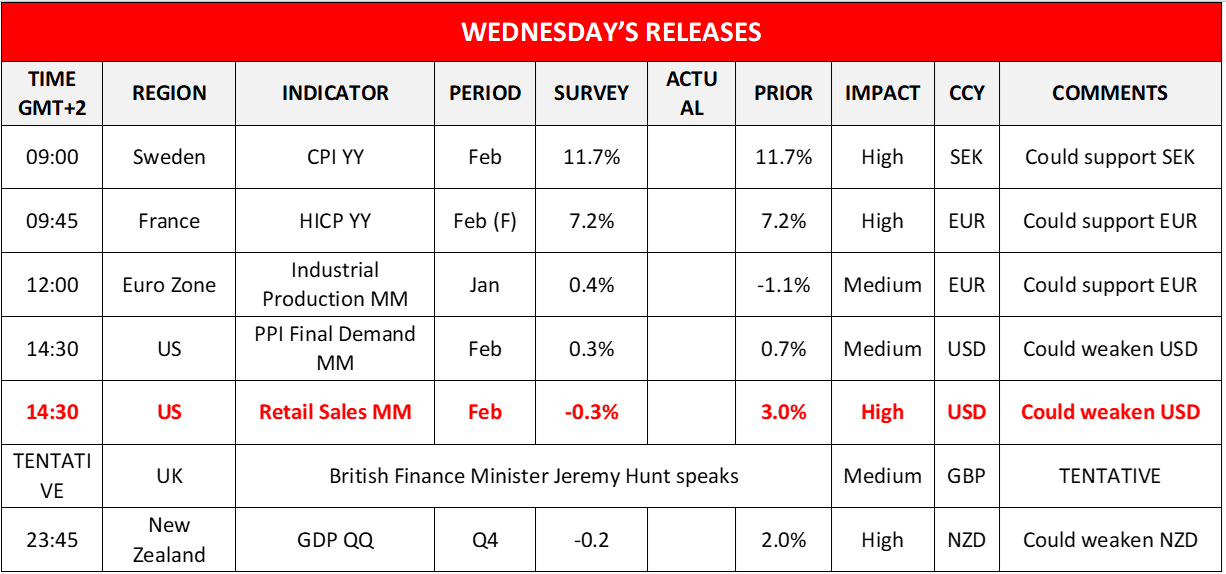

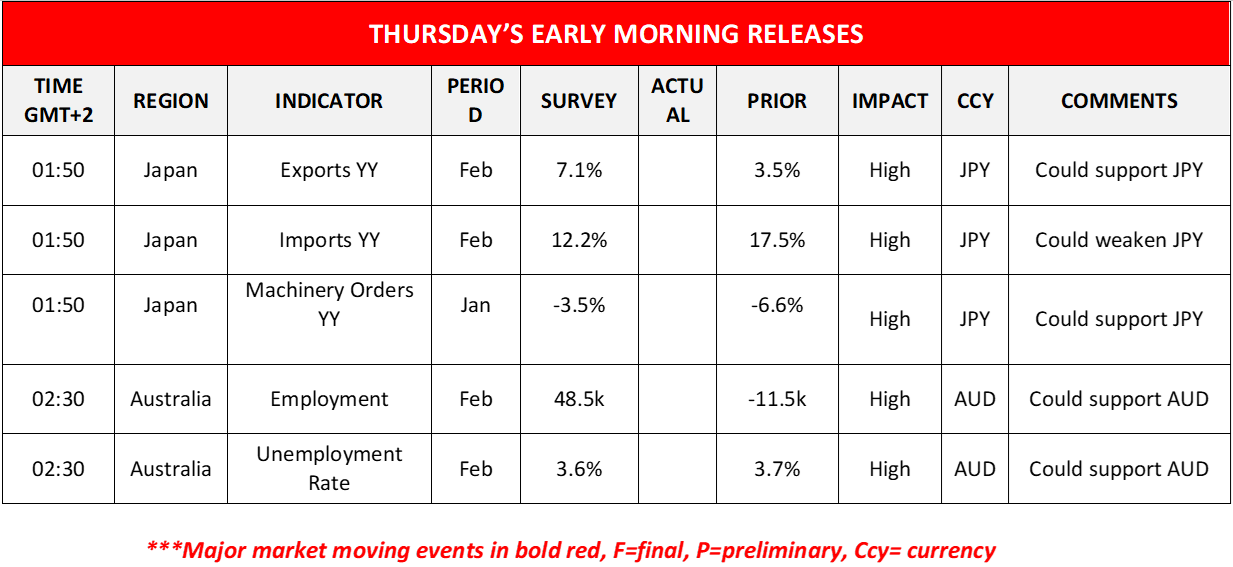

Today in the European session, we note the release of Sweden’s CPI rate for February and France’s final HICP rate for the same month, Eurozone’s industrial production for January, while UK finance minister Jeremy Hunt is scheduled to speak. In the American session, we note the release of the US PPI rates and the retail sales for February. During tomorrow’s Asian session, we note the release of New Zealand’s GDP rates for Q4, Japan’s imports and exports growth rates for February, Japan’s machinery orders for the same month and we highlight Australia’s employment data for February.

USD/JPY 4시간 차트

Support: 131.40 (S1), 128.60 (S2), 126.35 (S3)

Resistance: 134.80 (R1), 138.15 (R2), 140.60 (R3)

AUD/USD 4시간 차트

Support: 0.6590 (S1), 0.6520 (S2), 0.6400 (S3)

Resistance: 0.6695 (R1), 0.6785 (R2), 0.6900 (R3)

이 기사와 관련된 일반적인 질문이나 의견이 있으시면 저희 연구팀으로 직접 이메일을 보내주십시오 research_team@ironfx.com

면책 조항:

본 자료는 투자 권유가 아니며 정보 전달의 목적이므로 참조만 하시기 바랍니다. IronFX는 본 자료 내에서 제 3자가 이용하거나 링크를 연결한 데이터 또는 정보에 대해 책임이 없습니다.