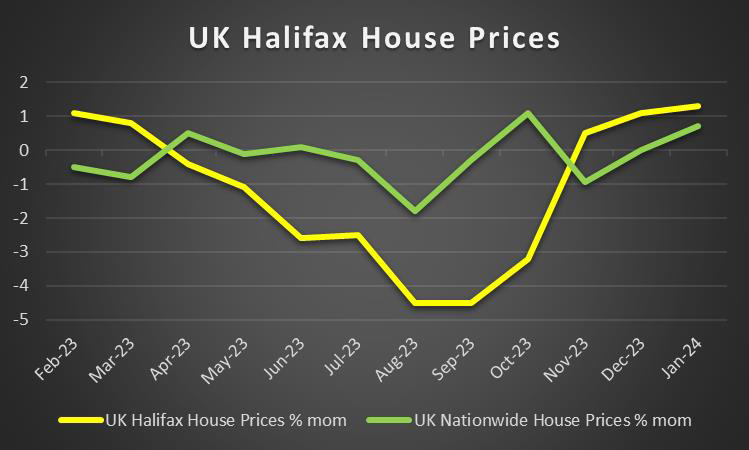

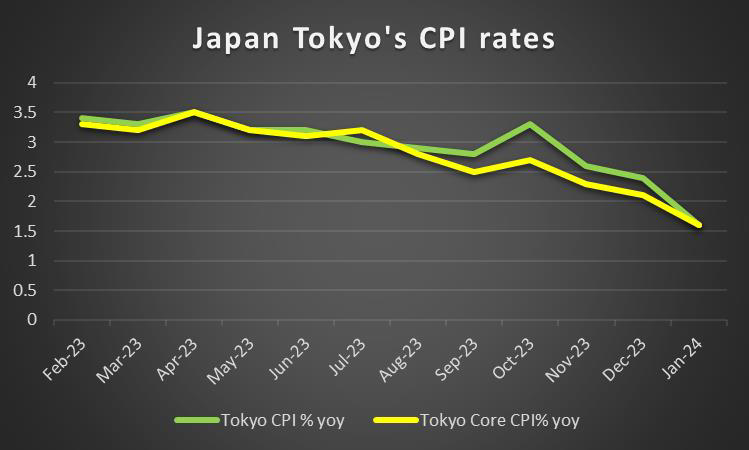

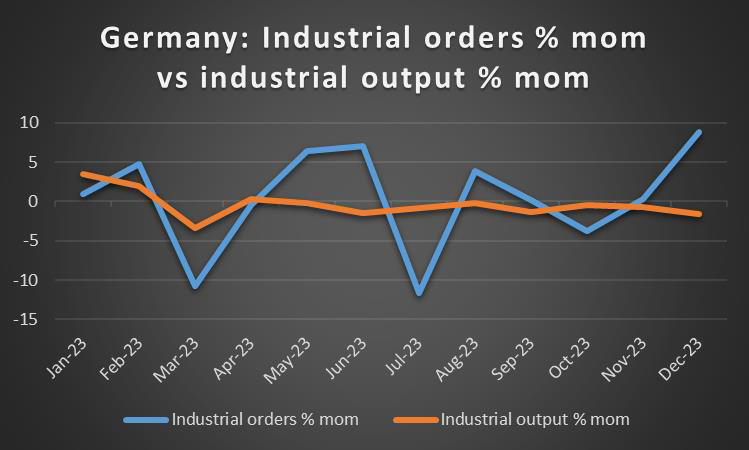

The week is about to draw to a close and we open a window at what next week has in store for the markets. On the monetary front, we note the interest rate decision of the BOC on Wednesday’s American session and the ECB’s interest rate decision on Thursday during the late European session. We also note the speech by BOJ Governor Ueda on Tuesday, the deliverance of the UK’s annual budget to parliament on Wednesday, the post-interest rate decision speech by Lagarde on Thursday and on Friday US President Biden’s Yearly State of the Union speech. As for financial releases, we make a start on a slow Monday, when we get Australia’s building approvals rate for January, followed by Turkey’s and Switzerland’s CPI rates both for the month of February and closing off the day is the Eurozone’s Sentix figure for March. On Tuesday we get Japan’s Tokyo CPI rate for February, the US Factory orders rate for January and the US ISM-Non manufacturing PMI figure for February. On Wednesday, we note Australia’s GDP rate for Q4. On Thursday we make a start with China’s trade balance figure for February, Germany’s industrial orders rate for January, the UK’s Halifax house prices rate for February, the US weekly initial jobless claims figure and Canada’s trade balance figure for January. On a busy Friday we begin with Japan’s current account balance for January, Germany’s industrial output rate and Sweden’s GDP rate both for the month of January, followed by the Eurozone’s final GDP rate for Q4 of 2023 and the highlight of the week which is the US Employment data for February and ending off the week is Canada’s employment data also for February.

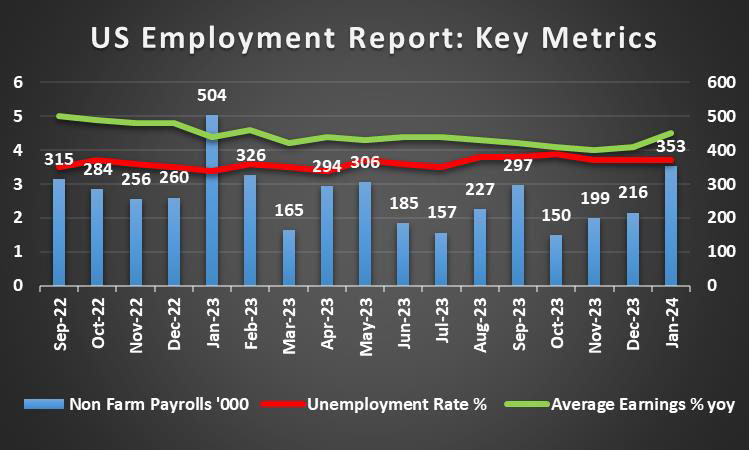

USD – Employment data set to shake the market

The USD is about to end the week slightly higher against the EUR and the JPY, yet remained relatively unchanged against the pound. On a fundamental level, we note that the majority of political commentators now appear to be anticipating a November showdown between incumbent President Biden (D) and Former President Trump (R). On a monetary level, we note that concerns about inflationary pressures remaining entrenched in the US economy seem to still be on the minds of some Fed policymakers. In particular, Atlanta Fed President Bostic seems to be concerned that “economic activity has remained surprisingly resilient in the face of tighter monetary policy”, which is “not the usual recipe for lower inflation”. We tend to agree with the policymaker in this instance, where a resilient labor market and consumer spending appear to be out of sync with the expected impacts of monetary policy. As such, the comments by Atlanta Fed President Bostic, may boost the Fed’s argument of maintaining interest rates higher for longer, which in turn could provide support for the greenback. However, it should be said that the policymaker during his speech also stated that he believes that inflation will decelerate to 2.5% by the end of 2024, which would be nearing the Fed’s inflation target of 2%. On a macroeconomic level, we note the Fed’s favorite tool for measuring inflationary pressures in the US economy, which is the Core PCE rates were released yesterday. The Core PCE rates indicated easing inflationary pressures in the US economy, implying that the Fed’s attempts to cool down the economy, appear to be making their way through the economy, although some concern about the Core PCE rate on a mom level, may prevent a declaration of victory just yet. Thus, the prospect of loosening monetary policy being implemented or maintained by the Fed appears to have weakened the greenback during yesterday’s trading session. Moreover, the 2nd Revision for the US GDP rate in Q4 2023, came in lower than expected, implying a deceleration in economic activity. Nonetheless, the stage is set for next week’s employment data which is anticipated to showcase an easing labour market, thus casting doubt on the bank’s hawkish stance, which in turn could weigh on the USD. Also of note is the ISM-non manufacturing PMI figure which could weigh on the dollar as it is expected to showcase an expansion in activity yet at a slower pace.

GBP – Fundamentals to lead

The pound seems about to end the week in the reds against the JPY and EUR and the USD. On a macroeconomic level, we note that this week was relatively easy-going for pound traders as no major financial releases stemming from the UK were released. However, one financial release did catch our eye, which was the CBI distribute traders survey which was released on Monday. Despite, the release being classed as minor in its importance, the indicator measures the health of the retail sector and its significant improvement from -50 to -7, which vastly exceeded expectations and may have provided support for the GBP. On a monetary level, we note the emergence of some hesitancy on behalf of the BoE to proceed with rate cuts even before the CPI rates drop below the bank’s target of 2% yoy, as seen by BoE Mann’s comments. The policymaker according to the FT claimed that spending habits by wealthy Britons may be actually hindering the bank’s monetary policy goals by “making it harder to curb inflation”. Yet please note that BoE policymaker Mann voted in favour of a rate hike, yet should, more policymakers re-iterate similar remarks that inflation appears to be entrenched in the UK economy, it could lead to the possibility of a rate hike being back on the table, which in turn could boost the GBP, but such a scenario seems farfetched for now. For the time being, we note that the market still currently expects the bank to start cutting rates in August but now expects a total of 2 rate cuts this year, down from 3 since last week. On a fundamental level, we note that the UK’s finance minister Jeremy Hunt, is set to deliver the government’s annual budget to Parliament, which is expected to include tax cuts in order to boost the economy. Given that it is an election year, we tend to also agree with the analysis that tax cuts might be included, as it could provide much-needed political support to the Conservative party which according to POLITICO is trailing the opposition party by 20 points. In such a scenario, the tax cuts could stimulate the economy, which in turn could provide support for the pound.

JPY – Tokyo’s CPI rates in focus

JPY seems about to end the week relatively unchanged against the USD EUR and GBP. We note that on a macroeconomic level, the stabilization of the BoJ Core CPI rate for January implied persistent inflationary pressures in the Japanese economy, which appears to be in line with the bank’s 2% inflation target. Moreover, Yen traders may be looking forward to Japan’s Tokyo CPI rate for February on Tuesday to confirm the persistence of inflationary pressures in the Japanese economy. As such on a monetary level, with the bank’s inflation target now seemingly in sight, as per BOJ policymaker Hajime Takata and according to Reuters, stated that the bank must be prepared to overhaul its ultra-loose monetary policy. The comments made by Takata appear to have provided support to the Yen, as market expectations for a possible rate hike in April seemed enhanced. In our opinion, in order to be convinced that the bank is prepared to normalize its monetary policy during its April meeting, we would require a series of BOJ policymakers to release a series of statements spread throughout March, in which they may imply that the bank is indeed ready to normalize its monetary policy. We do not anticipate a surprise announcement, but rather a series of smaller communications to market participants in order to ensure the transition occurs as smoothly as possible. Such a scenario could provide support for the Yen up until the bank’s meeting. In the coming week, we highlight the release of the aforementioned Tokyo CPI rates for February, the speech by BOJ Governor Ueda, and lastly Japan’s current account goods figure for January.

EUR – ECB interest rate decision due out next week

The EUR seems to have remained relatively stable against the dollar, yet weaker against the Yen and stronger than the pound. On a macroeconomic level, we note France’s GDP rates for February managed to avoid the beginning of a recession, implying an expansion in economic activity in the last quarter of the past year. On the inflation front, we note that the Eurozone’s HICP Rate slowed down less than expected on a year-on-year level and on a month-on-month level even accelerated, implying that inflationary pressures are still simmering under the surface possibly. As such, the contradicting financial releases appear to have cancelled each other out in terms of their impact on the common currency. The easing inflationary pressures though may exercise pressure on ECB’s resolve to maintain interest rates higher for longer. As such, on a monetary

level, market participants may be eyeing next week’s interest rate decision by the ECB, where EUR OIS currently implies a 93.7% probability for the bank to remain on hold at 4.50%. In our view, we agree with the market’s expectations that the bank may remain on hold, yet based on recent statements by ECB Nagel that “it would be fatal if ECB cut rates too early only for inflation to rebound” and ECB President Lagarde’s comments that the bank “needs to be confident that it will lead us sustainably to our 2% target”, we maintain the view that the bank’s accompanying statement may slightly push back against current market expectations of a rate cut in June. In such a scenario we may see the EUR gaining, whereas should the bank’s accompanying statement appear to be dovish, it could weigh on the common currency considerably. In the coming week, we note the Eurozone’s Sentix figure, Germany’s industrial orders rate and the Eurozone’s final GDP rate for Q4 which should it come in lower than expected, it could strengthen market expectations of a rate cut by June and thus may weigh on the EUR and vice versa.

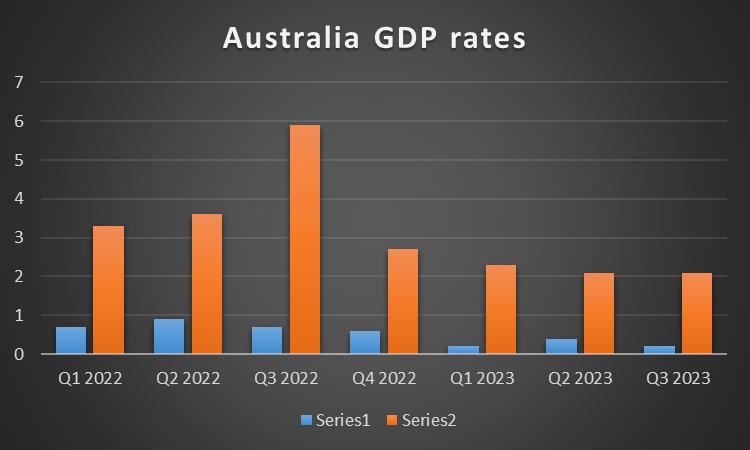

AUD – GDP rate next week

AUD is about to end the week weaker against the USD, bringing an end to its three-week winning streak and surrendering last week’s gains. On a fundamental level, we note that the Aussie’s commodity currency nature tends to make it sensitive to the market sentiment and in particular developments in China given their close economic ties. In particular, Chinese property developer Country Garden has received a liquidation petition by one of its creditors, thus dampening China’s efforts to restore confidence in the property sector, which in turn could lead to reduced demand for raw materials from Australia. On a macro-economic level, China’s NBS and Caixing Manufacturing PMI figures for February tended to highlight that Chinese factories are struggling to increase their activities and as such, could have negative implications for the Aussie. Moreover, adding to Australia’s woes was the Retail sales rate for January which despite turning positive, failed to meet expectations, implying that the Australian consumer may be feeling the impact of the credit crunch, due to high interest rates. Furthermore, the CPI rates for January accelerated, adding pressure on the RBA to remain hawkish, which could further support the Aussie. For next week, we highlight the release Australia’s GDP rate for Q4 which should it come in higher than the previous rate of 2.1%, it may provide support for the Aussie as the Australian economy will have grown faster than expected in the last quarter of 2023.

CAD – BoC’s interest rate decision in focus

The Loonie is about to end the week in the reds for a 9th week in a row against the USD. On a fundamental level, we note the sensitivity of the CAD to the market sentiment as a commodity currency. The positive correlation of the CAD with oil prices appears to have diverged this week despite Canada’s status as a major oil-producing economy. Oil prices this week tended to gain support following reports that OPEC+ was considering to further extend its voluntary oil production cuts, yet the Loonie does not appear to have gotten the memo. Nonetheless, should market worries for a continued tightening from the supply side of the oil market intensify in the coming week, we may see the CAD re-establishing its positive correlation with oil prices. Moreover, Canada’s GDP rates for December sent out mixed signals, with the mom rate coming in lower than expected at stagnation levels whilst on an annualized qoq basis for Q4 the GDP rate accelerated by 1.0%, escaping negative territory thus reducing concerns about a possible recession. Overall, despite the Loonie seemingly on track to end the week in the reds against the dollar, it reacted positively to the release of the GDP rates, thus finding some strength as the week comes to a close. On a monetary level, we highlight BOC’s interest rate decision which is to be delivered next Wednesday, with CAD OIS currently implying an 85% probability for the bank to remain on hold, with the remaining 15% being attributed to a potential rate cut by the bank. Given that the Canadian headline CPI rate for January, slowed entering the bank’s inflation target zone, we anticipate that the bank may remain on hold and in its accompanying statement may opt to be more dovish, should it want to prepare the markets for upcoming rate cuts, which in turn could weigh on the Loonie. Nonetheless, should the bank appear to be hawkish in nature in its accompanying statement, we may see Loonie gaining some support.

General Comment

Overall in the coming week in the FX market, we expect heightened volatility, as high-impact financial releases are stemming from various economies. On the other hand, US stock markets rallied yesterday with the S&P 500, NASDAQ 100 and the Dow Jones taking aim for their recently formed all-time highs. However, on a weekly basis, the Dow Jones is on track to end the week in the reds, a divergence from the other indexes. Nonetheless, should the positive market sentiment be maintained we may see US stock markets printing new all-time highs in the coming week. Also, note that the earnings season seems to be more or less done. Furthermore, also gold’s price seems to be on track to end for the second week in a row in the greens against the dollar. Moreover, the decline of US yields tended to support the precious metal’s price. Last but not least, a small fundamental note, regarding recent political commentary made about a possible armed confrontation between Europe and NATO against Russia, could funnel safe-haven inflows into gold and lead to elevated tensions in the coming weeks.

이 기사와 관련된 일반적인 질문이나 의견이 있으시면 저희 연구팀으로 직접 이메일을 보내주십시오 research_team@ironfx.com

면책 조항:

본 자료는 투자 권유가 아니며 정보 전달의 목적이므로 참조만 하시기 바랍니다. IronFX는 본 자료 내에서 제 3자가 이용하거나 링크를 연결한 데이터 또는 정보에 대해 책임이 없습니다.