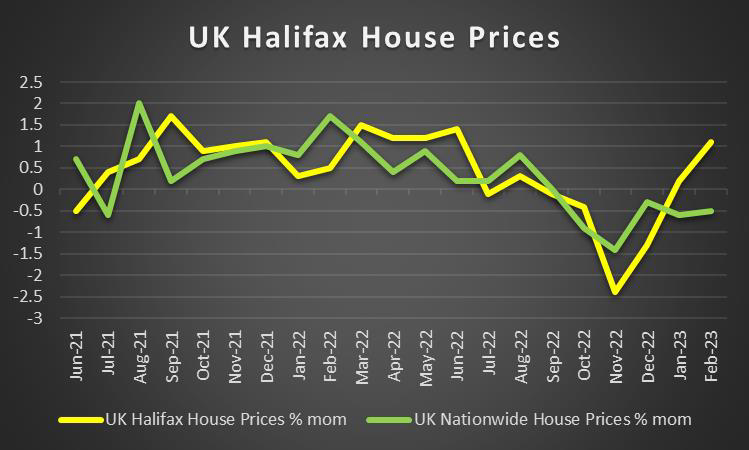

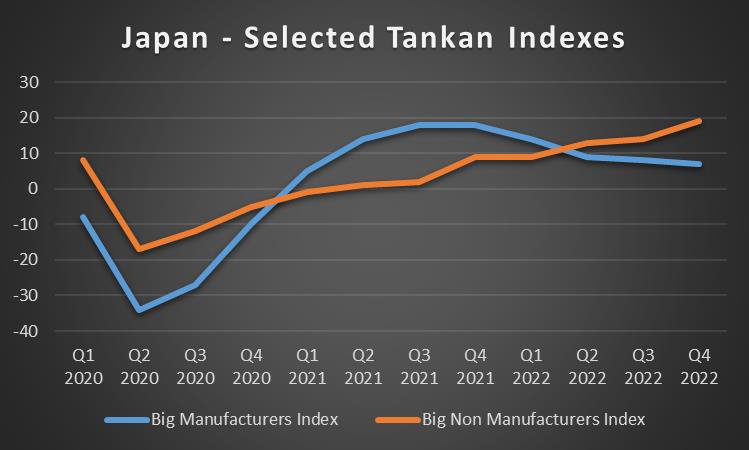

With market turmoil appearing to have subsided for now, we take a look at what next week has in store for the markets. On the monetary front, we note a relatively quiet week from policymakers including public holidays as Christian easter approaches. However, we note the release of Australia’s RBA interest rate decision on Tuesday and New Zealand’s RBNZ interest rate decision on Wednesday. As for financial releases, we make a start on Monday with Japan’s Tankan Manufacturing and Non-Manufacturing index for Q1, China’s Caixin Manufacturing PMI, Switzerland’s CPI rates, Turkey’s CPI rates, Germany’s Final S&P Manufacturing PMI, Canada’s manufacturing PMI and the US S&P and ISM Manufacturing PMI all for the month of March. On Tuesday we note the release of Canada’s Trade Balance for February. On Wednesday, we note the release of Germany’s Industrial Orders for February, Eurozone’s Composite PMI, UK’s Services PMI and the US ISM Non-Manufacturing PMI all for March. On Thursday we note Australia’s Trade Balance and Germany’s Industrial output both for February, followed by UK’s Halifax House Prices for March, Sweden’s GDP for February, the US weekly Initial Jobless Claims figure and lastly Canada’s employment data for March. Finally, on a US-dominated Friday, we note the US Employment report for March, which includes also the NFP figure.

USD – Traders await NFP figure next week

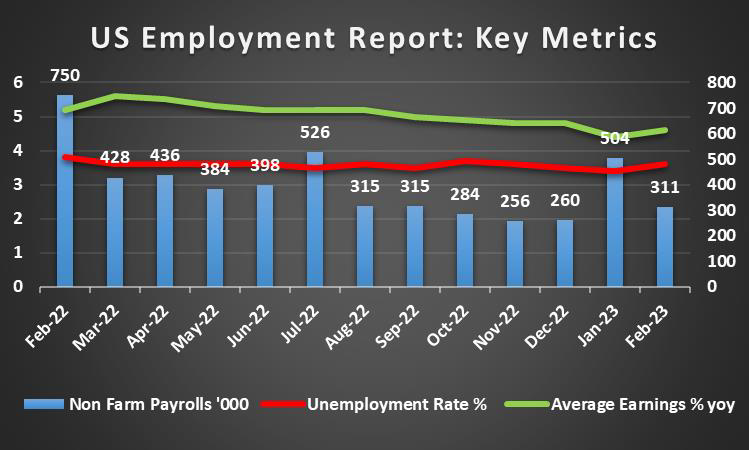

The USD is about to end the week in the reds against its counterparts. On a fundamental level, we note the easing of the market’s worries for a possible overspilling of the banking crisis in the US. The situation remains fragile though and needs monitoring. It was characteristic that St. Louis Fed President Bullard last Friday stated “Even with considerable forward guidance, it is relatively common that not all financial entities adjust their businesses appropriately to the changing environment”. The statement would imply that some entities have failed to adapt to the changing financial environment, at least yet, which would imply that besides, SVB there are other commercial banks that may present liquidity issues in the future. Also, we note Fed Board Governor Barr’s testimony, as he stated that “staff presented to the Federal Reserve’s Board of Governors on the impact of rising interest rates on some banks’ financial condition”. Hence as stated above, we understand the easing of the market’s worries, yet we highlight that the situation is still fragile and needs constant monitoring. On a monetary policy level, we note a continuance of the aggressive hawkish rhetoric of the Fed. Remarkably a relatively hawkish statement from Minneapolis Fed President Kashkari, that there is still “more work to do” to combat inflation, implying that more monetary policy tightening is still necessary. Overall, should policymakers continue to stress the need for more rate hikes we may see the USD gaining some ground. On a macroeconomic level, we note that the final GDP rate for Q4 verified the modest slowdown in comparison to Q3. We expect the market’s attention next week to turn to the release of March’s US employment report. We highlight the NFP figure which is expected to drop and the unemployment rate which is expected to remain at relatively low levels. Overall, should the US employment market remain tight that could support the greenback, as it would allow the Fed to proceed with more monetary policy tightening and vice versa.

GBP – Bailey leads the UK towards the light

GBP is about to end the week substantially higher against the dollar and JPY while remaining relatively stable against the common currency, in a sign of a broader strength. On a fundamental note, we highlight that out of the major economies, the UK appears to have borne the least criticism for its banking industry as the news cycle primarily focuses on the US and the EU thus potentially painting a perception of strength in the UK banking sector. On a monetary level, BoE Governor Bailley’s speech on Monday was hawkish in nature as he stated “what monetary policy can – and must – do is to make sure that the inflation that has come to us from abroad does not become lasting inflation generated at home”. This could be perceived as an indication of the intentions of BoE when they are meeting again on the 11th of May, opening the door to potential further hikes, given also the acceleration of the CPI rates for February. As such we could potentially see inflows into the GBP as a similar rhetoric was echoed by BoE’s Mann, as during a speech she indicated that underlying inflationary pressures would make monetary policy increasingly difficult. Should the BoE officials continue to display such hawkishness we may see a strengthening of the pound. On a macroeconomic level we note UK’s Final GDP for Q4 which accelerated slightly in comparison to the preliminary release indicating that the UK economy has relatively improved and might be entering a period of growth once again yet at feeble levels. On the flip side, any further monetary policy tightening may obstruct economic growth, hence we intend to monitor closely any key financial releases stemming from the UK.

JPY – Safe haven outflows for the Yen

JPY is about to end the week lower than the greenback, common currency and the pound, indicating that the JPY has shown a general sign of weakness as market sentiment returns back to normal. Thus, after safe heaven inflows enjoyed by the Yen during the time of uncertainty in the US markets, JPY now faces outflows. On a monetary policy level, we note that the change in leadership at the BoJ could indicate that new policies may be ushered in, thus upheaving years of ultra-loose monetary settings and translating into potential uncertainty surrounding future policy. We note the statement by BOJ’s new deputy chief Uchida who on Wednesday indicated a willingness to move away from the central bank’s bond yield control policy that saw the frequent intervention of the BOJ in order to stabilize or improve its own currency. As such the potential of less frequent BOJ JGB purchases, could imply that the BOJ is to stop or at least lessen its indirect quantitative easing policy allowing for the Japanese Yen to strengthen. On a fundamental level, we note JPY’s dual nature as a safe haven instrument and a national currency and the possibility of further tensions supporting it, while a further easing of market worries may weaken it. Also, we note the agreement signed between Japan and the US about electric battery raw materials that could open new ways for Japan’s key auto industry. On a macroeconomic level, we note that Tokyo’s CPI rates slowed down for March which tends to foreshadow also a slowdown of inflationary pressures in Japan on a more general level, for the past month. As for economic activity, we note the improvement of Japan’s PMI figure for March of the crucial manufacturing sector, yet also note that the indicators’ reading indicated another contraction for the fourth month in a row.

EUR – Fears of Contagion held at bay

The common currency was on the rise against the USD, CHF and JPY yet seems to be neutral against the GBP for the week. On a monetary level, we note the Eurozone’s increased CPI for February tended to boost EUR traders’ confidence that the bank is to continue to proceed with further monetary policy tightening, yet the easing of inflationary pressures as recorded by the preliminary PMI readings for March seems to be also easing the pressure on the bank to hike rates. It should be noted that the ECB stated in its last interest rate decision that future policy changes, will now be more data dependent. Given though that the CPI rates are still above the bank’s target, should there be a potentially hawkish rhetoric from ECB officials we may see the common currency getting some support. Overall on a macrolevel, the slight worsening of Eurozone’s business climate and in particular the economic sentiment’s worsening for March tends to intensify our worries for the Eurozone. On a fundamental level, the continued social upheaval in France and strikes in Germany may slow down growth and given that the market discounts such developments in advance may weaken the common currency. Also, we have to note that the recent shake-up of Deutsche bank last Friday send shivers down the spine of EUR traders, yet since then market worries seem to have eased, allowing for calmer thoughts. The situation though tends to remain fragile and requires continuous monitoring.

AUD – RBA’s interest rate decision in focus

AUD seems to have remained relatively unchanged against the USD, maybe edging a bit higher as the week draws to a close. On a monetary level, we note that Treasurer Chalmers seeks bipartisan support for an overhaul of the RBA, including proposals to transfer power from the RBA to a new committee of economic specialists and fewer meetings to discuss interest rate decisions, including regular press conferences by the bank governor to explain monetary decisions. We highlight though, RBA’s interest rate decision on Tuesday and the market widely expects the bank to remain on hold. Please note that the bank is expected to stand pat after 10 consecutive rate hikes. Should the bank actually remain on hold as expected, the market’s focus is expected to shift towards RBA’s forward guidance in Governor Lowe’s statement. Should the Governor signal that the bank intends to pause its rate hikes, we may see the Aussie weakening. On a macro level, we note that economic activity seems to have contracted across sectors for March which tends to be worrisome and actually may support the notion of RBA remaining on hold, allowing for Australian businesses to take a breather. On a more fundamental level, a possible deterioration of the US-Sino relationship may weaken it, given the close Sino-Australian economic ties. Especially considering the recent moves of China to conduct its first Yuan-settled LNG trade with a French company and the announcement by Saudi Arabia that its cabinet approved a memorandum awarding Riyadh the status of dialogue partner in the Shanghai Cooperation Organization. On a macro level, we highlight the slight drop of China’s NBS manufacturing PMI figure potentially signaling a slower expansion of economic activity in the sector and thus could imply fewer exports of raw materials from Australia to China. Overall given the low number of high impact financial releases stemming from Australia in the coming week we expect fundamentals to be in the driver’s seat for the Aussie.

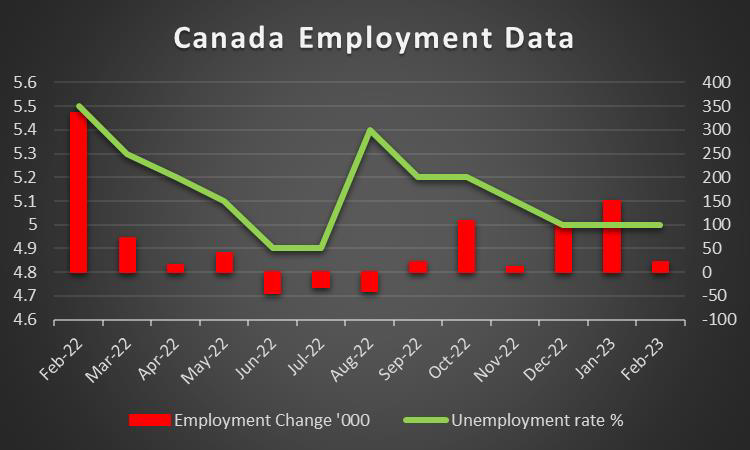

CAD – Canada’s employment data at the end of the week

Also, the CAD seems to show greatly improved against the USD for the week. It should be noted that Canada’s Manufacturing and employment data for March are set to be released next week. On a macroeconomic level, we highlight the acceleration of the retail sales growth rate for January which tends to imply that the average Canadian consumer is willing and able to actually spend more in the Canadian economy, thus contributing to its recovery. On the monetary front, following BoC’s last interest rate decision to remain on hold we note BoC’s Gravelle statement on Wednesday that the bank anticipates inflation to decrease in the following months, thus solidifying its view to remain on hold, i.e. pausing its rate hiking path. On a more fundamental level, we note that WTI’s price seems to have substantially increased for the week in comparison to last week, given the tight oil market in the US as presented by the weekly drawdowns in US oil inventories but also the possibility of tighter oil supplies from the Iraqi Kurdish area. Should the bullish tendencies for the commodity’s price be maintained, the support building up could be reflected in the CAD given that Canada is a major oil-producing country. Furthermore, on a fundamental level we note as a positive development, Rock Tech Lithium’s new first of it’s kind lithium conversion plant in Germany potentially.

General Comment

As a closing comment, in the event of no ground-breaking news, we may see the market remaining relatively calm, possibly returning back to normality, despite the situation with the banking sector still bearing a certain degree of uncertainty. Following the prevention of Deutsche Bank experiencing a bank run the market seems to have calmed down the bank crisis rhetoric. In a more general sense, we may see the USD increasing its influence over the FX market as the gravity and frequency of US financial releases tends to increase in the coming week, with the highlight being the US employment report for March next Friday, On the monetary front, we would like to note the upcoming interest rate decision of RBNZ next Wednesday. Currently, NZD OIS imply a 97.8% probability of a 25-basis point hike, which if realised, could support the Kiwi, especially if it’s accompanied by a hawkish rhetoric. In the equities market, seems to have improved especially in the US with a positive overspill in Europe as well. Also, the stabilisation of US yields may allow gold traders to be more optimistic. The negative correlation of the precious metal’s price with the USD was relatively visible this week with minor changes seen in both trading instruments. With the stabilisation of the USD we saw gold remaining also relatively stable as well, as traders await US economic data next week. Nevertheless, the drop below the psychological threshold of US$2000 per ounce at some point during the week could be indicative that the mentality of traders may be shifting, thus we may see the bears take over the precious if US data comes in stronger than expected, supporting the greenback.

이 기사와 관련된 일반적인 질문이나 의견이 있으시면 저희 연구팀으로 직접 이메일을 보내주십시오 research_team@ironfx.com

면책 조항:

본 자료는 투자 권유가 아니며 정보 전달의 목적이므로 참조만 하시기 바랍니다. IronFX는 본 자료 내에서 제 3자가 이용하거나 링크를 연결한 데이터 또는 정보에 대해 책임이 없습니다.