In the grand scheme of things regarding the oil market we note the continuance of the weakening of oil prices, despite a correction higher over the past few days. Today on the fundamental side we take a look at the situation of the US oil market and then continue to examine the demand side as well as the supply side .The report is to be concluded with a technical analysis of WTI’s daily chart.

Oil: Overview Report

The situation on the ground of the US oil market

We make a start with the situation on the ground about the US oil market and begin by noting that the Baker Hughes US active oil rig count dropped by two implying an easing of the demand side in the US oil market. Yet the market was taken by surprise on Tuesday as API reported a drawdown of -2.349 million barrels in US oil inventories, which was wider than the market’s expectations and implied a relative tightening of the US oil market.

Nevertheless, the tightness for the US oil market was also confirmed by the EIA crude oil inventories figure on Wednesday, as it showed also a wider drawdown than expected, this time of -4.259 million barrels. Given that the US oil market seems to remain tight as demand levels tended to surpass total oil production, it could provide some support for oil prices, especially if the relative tightness is evident in the readings of the coming week.

The demand side

We note that the market still has extensive worries about the demand side of the oil market especially from China, as the red giant seems to be struggling to increase economic activity in the manufacturing sector. Yet tomorrow we note the release of China’s industrial output and urban investment growth rates for November and both rates are expected to show an acceleration.

Should the rates accelerate we may see expectations for increased oil demand from China rising that could provide some support for oil prices. Yet we also note the Fed’s interest rate decision yesterday that showed that the bank is ready to proceed with extensive rate cuts in the coming year, which in turn implies an improvement of the financial environment and the prospect for increased economic activity in the US.

The same applies also for market expectation regarding BoE’s and ECB’s interest rate decisions later on and such easing of monetary policy could support oil prices somewhat and vice versa. Also the Fed’s interest rate decision had as a byproduct the weakening of the USD which in turn tends to support the largely USD denominated commodity.

The supply side

For the time being there seems to be an oversupply of the oil market. Yet investors are keeping a close eye on OPEC producers and want to see whether the production cuts, as announced by OPEC+ will be implemented. To that end, the market seems to expect the production data of the first quarter next year to be of the utmost importance. Overall should there be indications for a possible lowering of production levels by Saudi Arabia, it may have a bullish effect on oil prices.

Yet there is still wide uncertainty about the production side as the intentions of Venezuela, Russia and Iran cannot be predicted with relative certainty. Especially, we still remain worried about Venezuela’s intentions regarding annexing a large part of Guyana. A meeting is to take place between the leaders of the two countries, yet should the meeting end fruitless, we may see tensions rising once again that may threaten directly the supply side of the international oil market and thus push oil prices higher. Also, the Israeli conflict is still ongoing and there is extensive protest in Middle East countries about the latest developments, which could spark renewed worries for oil supply.

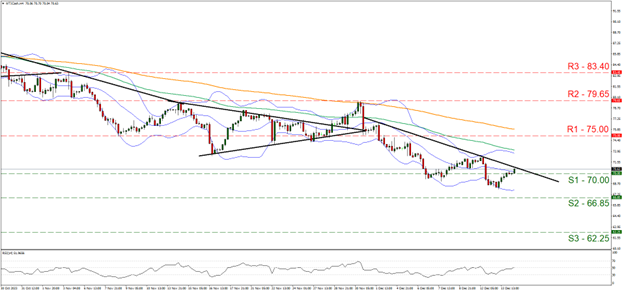

Oil: Technical Analysis

WTI Cash Daily Chart

- Support: 70.00 (S1), 66.85 (S2), 62.25 (S3)

- Resistance: 75.00 (R1), 79.65 (R2), 83.40 (R3)

For the time being there seems to be an oversupply of the oil market. Yet investors are keeping a close eye on OPEC producers and want to see whether the production cuts, as announced by OPEC+ will be implemented. To that end, the market seems to expect the production data of the first quarter next year to be of the utmost importance.

Overall should there be indications for a possible lowering of production levels by Saudi Arabia, it may have a bullish effect on oil prices. Yet there is still wide uncertainty about the production side as the intentions of Venezuela, Russia and Iran cannot be predicted with relative certainty. Especially, we still remain worried about Venezuela’s intentions regarding annexing a large part of Guyana.

A meeting is to take place between the leaders of the two countries, yet should the meeting end fruitless, we may see tensions rising once again that may threaten directly the supply side of the international oil market and thus push oil prices higher. Also, the Israeli conflict is still ongoing and there is extensive protest in Middle East countries about the latest developments, which could spark renewed worries for oil supply.

면책 조항:

본 정보는 투자 자문이나 투자 권유가 아닌 마케팅 커뮤니케이션으로 간주해야 합니다.