There seems to be an element of hesitation among stock market participants for US equities markets to advance higher. In this report, we are to discuss the effect of the release of January’s US employment report, the Fed’s decision and intentions as well as upcoming releases and earnings reports expected in the coming days and for a rounder view conclude with a technical analysis of the S&P 500.

January’s US employment report comes in stronger than expected

The main market mover of the past week may have been the release of the US employment report for January. The release shook the markets as, despite consensus for an easing of the tightening of the US employment market, the actual rates and figures highlighted its resilience. It’s characteristic that the Non-Farm Payrolls figure instead of dropping as expected, rose to 353k and the jump highlighted the ability of the US employment market to create new jobs. At the same time, the unemployment rate failed to tick up and remained unchanged at 3.7%, highlighting the continuance of the tightness of the US employment market. The release as such, tends to allow more leeway for the Fed to maintain rates high for a longer period, as one part of its mandate, promoting employment, is covered and forces the bank’s focus on bringing inflation down to its 2% target. Furthermore, the release tends to underscore the narrative of the bank for a possible soft landing of the US economy. Market-wise, the release obliged the market to reposition itself, yet US stock markets were able to overcome the obstacle and edge higher for the day.

Fed remains on hold signals high rates for longer

On the monetary front, we note that the Fed remained on hold as was widely expected. In its accompanying statement, the bank seems to be taking its time regarding the possibility of any rate cuts. Fed Chairman Powell in his press conference stated that March is not a base scenario for rate cuts. Please note that the market had already shifted before the release, expecting the first rate cut in May. The market currently, seems to expect the bank to deliver 5 rate cuts until the year has ended. We tend to be even less dovish and suspect that the bank may start cutting rates in the summer and deliver 3-4 rate cuts in the current year. Overall we tend to note that Fed policymakers are expected to continue making statements that could at least partially contradict market sentiment regarding the bank’s intentions, which may weigh on US stockmarkets. Should such a scenario start emerging, it would imply that tight financial conditions in the US economy are to be maintained for longer, which in turn may shrink revenue and profitability margins.

Upcoming earnings releases and US CPI rates

The earnings season is still on and headlines about earnings and revenue of various companies are still exciting traders. We make a start today with Ali Baba (#BABA) and highlight Walt Disney (#DIS). Disney missed the market expectations for its revenue figure slightly in the past two quarters and the figure may be closely watched by traders today, yet our concern is also on its streaming service. The big question may be whether the company was able to widen its customer base, in a highly competitive landscape characterising the streaming sector. Furthermore, we note Disney’s intentions to start cracking on password sharing. Other US companies to watch out for in the coming days could be Philip Morris (#PM) tomorrow, on Friday Pepsico (#PEP) and next Tuesday AirBnb (#ABNB) and Coca Cola (#KO).

From the prementioned releases, we note rival companies PepsiCo and Coca Cola. Analysts tend to expect Pepsico’s revenue figure to rise from 23.45B to 28.38B, yet its EPS figure to drop from 2.25 to 1.72. The projections tend to imply a cost structure issue for the staples company and such figures may imply an inconsistency with the narrative that a series of price hikes may have benefited the profit margins. On the other hand Coca Cola’s earnings and revenue figures are expected to be lower than prior quarter and could weigh on the company’s share price. In both cases, the obesity drugs in the market may have had an adverse effect on the companies’ revenue figures as demand for beverages and snacks may have eased.

On a more fundamental level, we note the release of the US CPI rates for January next Tuesday. Should the rates slow down beyond market expectations we may see market anticipation for the Fed to start cutting rates early being enhanced and thus boost the buying interest in US stock markets.

기술적 분석

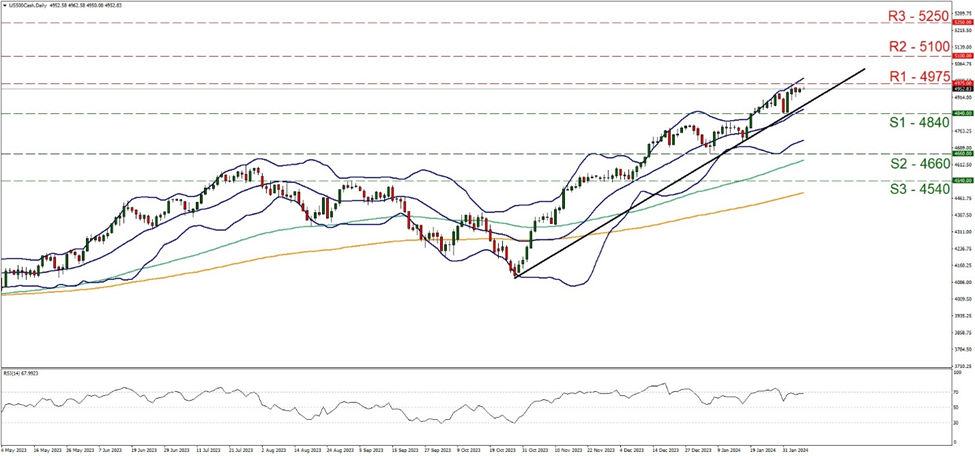

US 500 Daily Chart

Support: 4840 (S1), 4660 (S2), 4540 (S3)

Resistance: 4975 (R1), 5100 (R2), 5250 (R3)

S&P 500 rose 4 weeks in a row yet for the time being, bulls seem to have hit a ceiling at the 4975 (R1) resistance line and the index shows some stabilisation since the start of the week. We tend to maintain our bullish outlook for S&P 500, given that the upward trendline guiding the index since the 27 of October last year remains intact. Please note that the 200, 100 and 20 moving averages maintain an upward slope supporting the bullish outlook. Also, despite the price action nearing the upper Bollinger band, there is still some room to play for the bulls. Furthermore, we note that the RSI indicator below our daily chart, remains near the reading of 70, implying a strong bullish sentiment on behalf of the market, yet at the same time may also imply that the index is nearing overbought levels and may be ripe for a correction lower. Should the bulls maintain control over the index, we may see it breaking the 4975 (R1) resistance line, which is a record-high level for the index and we set the next possible target for the bulls at the 5100 (R2) resistance level. On the flip side for a bearish outlook we would require the index’s price action to initially break the prementioned upward trendline, in a first signal of an interruption of the upward motion and continue to break the 4840 (S1) support line and thus start paving the way for the 4660 (S2) support level.

이 기사와 관련된 일반적인 질문이나 의견이 있으시면 저희 연구팀으로 직접 이메일을 보내주십시오 research_team@ironfx.com

면책 조항:

본 자료는 투자 권유가 아니며 정보 전달의 목적이므로 참조만 하시기 바랍니다. IronFX는 본 자료 내에서 제 3자가 이용하거나 링크를 연결한 데이터 또는 정보에 대해 책임이 없습니다.