US stock markets have extended their reach over the past week capitalizing on weaker US economic data and currently 트레이더 appear overoptimistic at the start of the earnings season, despite ongoing worries for a recession. In this report we aim to present the recent fundamental and economic news releases that impacted the US stock markets, look ahead at the upcoming events that could affect their performance and conclude with a technical analysis.

US stock markets trade higher following the CPI print

Equity markets traded higher following last week’s US CPI print. As was mentioned in last week’s report, market analysts had predicted the US CPI at 5.2% whereas the official figure came in at 5.0%. The lower than anticipated CPI print was indicative of reduced inflationary pressures following the Fed’s aggressive interest rate hiking path in its fight against inflation. Following the release of the CPI data, US equity markets capitalized on a weaker greenback which was pressured by the anticipation that the Fed may ease on its hiking policy in order to reflect the current economic situation. In addition to a stronger Industrial production figure on Friday allowed equities 트레이더 to ride Wednesday’s CPI print momentum into Friday’s trading session. However, other financial releases such as the Retail sales figure which ticked down may have capped gains, as it may be indicative that consumers are feeling the effects of 높음 interest rates, thus being less likely to continue current spending levels. This may translate into a weaker equities market, as reduced spending will eat away at the extraordinary profit margins enjoyed by companies, that were followed by the re-opening of global markets after covid, where due to consumers having high disposable incomes, lead to increased spending. Despite the equities markets overall gaining as a result of economic data indicating a reduction in inflationary pressures, the hawkish rhetoric from the Fed remained unchanged, as the FOMC indicated that they anticipate a mild recession to occur in the US economy. Moreover statements made by Fed officials supported the Fed meeting minutes ,such as Fed Governor Waller who stated during a speech on Friday, “This growth would mean that, so far, tighter monetary policy and credit conditions are not doing much to restrain aggregate demand”. Also, according to Reuters Minneapolis Fed President Kashkari stated last Wednesday, that allowing inflation to stay would be even worse for the labour market, implied that the Fed may need to raise interest rates further. Equity 트레이더 may anticipate the remaining three speeches by FOMC members Bowman, Waller and Cook throughout the week, as they may re-iterate hawkish remarks potentially weakening the bullish tendencies in the equities market. Lastly, we would also like to make a comment about the market’s expectations for a recession reflected from the movements of the U.S Treasury bond yields. It’s characteristic that the US 10-year yield and 2-year yield, both ticked upwards, reaching levels seen on the 14 of March, highlighting that the risk of a recession is estimated being higher overall by the markets, as we near the Fed’s interest rate decision on the 3rd of May. Such market sentiment could sink morale, which may lead 트레이더 to adopt a more short-term outlook to the equities market since fears of a recession persist.

Earnings season has arrived

Reckoning day has arrived for many companies, with special interest being placed upon large 그리고 regional banks which due to announce earnings. Last Friday the equities markets received a fresh injection, following better than anticipated earnings by JPMorgan (#JPM), Wells Fargo (#WFC) 그리고 Citigroup (#C) posting higher than expected earnings. On Tuesday we saw Johnson & Johnson (#JJ) followed by Bank of America (#BAC), Lockheed Martin (#LockheedMT) supporting the rally by posting better than expected earnings, whereas Goldman Sachs (#GS) reported slightly weaker earnings 그리고 Netflix (#NFLX) reported mixed earnings. Despite some outliers, the equities markets continued their upwards trajectory, however on Wednesday they appeared to have slightly weakened, indicative of heightened recession fears as was noted by the increase in both the US 2-year and 10-year treasury yields, as cracks in the so far stellar earnings period are appearing. In particular, Tesla (#TSLA) whose earnings at the time of this report are yet to be released, announced that US automobile prices will be reduced for a sixth time this year, potentially indicating a reduction in demand as they attempt to curb any negative impact in its share price, in the event that their earnings fail to meet expectations. Furthermore, we note that Walt Disney (#DIS), according to Bloomberg, is set to eliminate thousands of jobs next week including 15% of its entertainment division staff. This could be a continuation of Disney’s plan to reduce $5.5 billion in annual costs and an attempt to drum up investor confidence before its earnings report due on the 10 of May. Overall, equities 트레이더 may find short term support in the market, but in general, heightened fears of a recession could mean that the support from positive earnings is only a temporary support mechanism.

기술적 분석

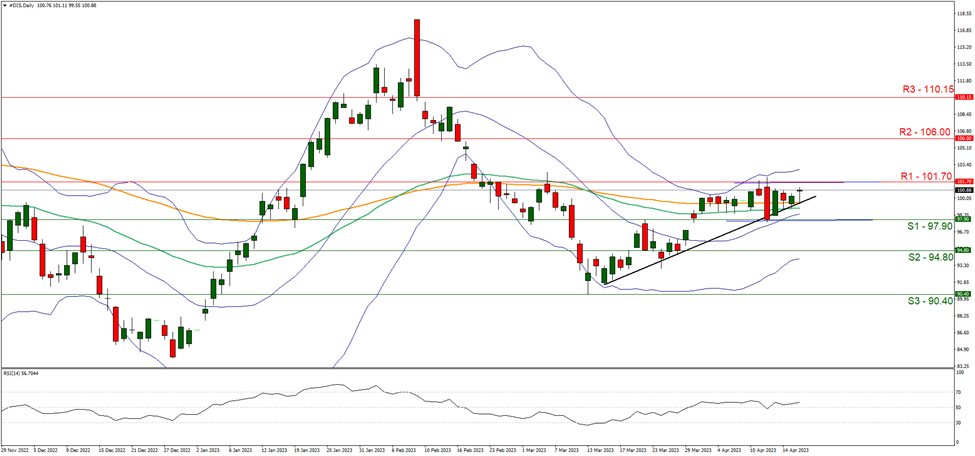

#DIS Daily Chart

Support: 97.90 (S1), 94.80 (S2), 90.40 (S3)

Resistance: 101.70 (R1), 106.00 (R2), 110.15 (R3)

Looking at #DIS Daily chart we observe investors reacting favorably to today’s employee reduction announcement, as we approach Walt Disney’s earnings date release. We hold a neutral outlook for Walt Disney, if the price action remains between the 97.90 (S1) support and the 101.70 (R1) resistance levels. Supporting our case is the RSI indicator below our daily chart which currently stands near 50 and the formation of a sideways channel since the 12 of April, indicating an indecisive market surrounding “the land where dreams come true”. However, we note that there is also a formation of an upwards trendline since the 15 of March that has yet to be broken, potentially implying bullish tendencies for the stock. For a bullish outlook, we would like to see a clear break above the 101.70 (R1) resistance level and the move towards the 106.00 (R2) resistance barrier. For a bearish outlook we would like to see a clear break below the 97.90 (S1) support level with the next possible target for the bears being the 94.80 (S2) support base.

이 기사와 관련된 일반적인 질문이나 의견이 있으시면 저희 연구팀으로 직접 이메일을 보내주십시오 research_team@ironfx.com

면책 조항:

본 자료는 투자 권유가 아니며 정보 전달의 목적이므로 참조만 하시기 바랍니다. IronFX는 본 자료 내에서 제 3자가 이용하거나 링크를 연결한 데이터 또는 정보에 대해 책임이 없습니다.