Market sentiment seems to have improved somewhat yet uncertainty is still present. In the coming week, we note that on the monetary front, the Fed is to release the minutes of its last meeting on Tuesday, as is also RBA. We also note that on Thursday, we get the interest rate decisions of Sweden’s Riksbank and Turkey’s CBT. As for financial releases, we make a late start on Tuesday with Canada’s CPI rates for October, and on Wednesday we get UK’s CBI trends for November, from the Eurozone the preliminary Consumer confidence for the same month and from the US, October’s durable goods orders and the weekly initial jobless claims figure. On Thursday we get November’s preliminary PMI figures of Australia, France, Germany, the Eurozone and the UK, as well as Norway’s GDP rate for Q3 and on Friday we get the November preliminary PMI figures of Japan and the US as well as Japan’s CPI rates for October, Germany’s Ifo indicators for November and Canada’s September retail sales growth rate.

USD – Fed’s minutes to provide more insight

The USD retreated substantially across the board for the week, as the US CPI rates for October slowed down more than expected, indicative of the easing of inflationary pressures in the US economy and solidifying the market’s expectations for the Fed to abandon its rate-hiking path and remain on hold. It should be noted that according to Fed Fund Futures (FFF) the market now expects the Fed to remain on hold and proceed with a rate cut as early as May next year. Also, the release of October’s CPI rates overshadowed the statements made by Fed Chairman Powell last week in which the Fed Chairman hinted that more rate hikes would be possible if needed. We do not underestimate the possibility of some Fed policymakers continuing to lean on the hawkish side, given that the CPI rates are still substantially higher than the Fed’s target, yet we see the balance of power within the central bank as tilting towards a more cautious approach. We expect the release of the Fed’s last meeting minutes, to shed more light on the banks’ intentions. Should the document include a more hawkish tone we may see the greenback getting some support. On a macro level, our worries for the US economic outlook intensified somewhat from the data this week and intend to focus on the release of the preliminary S&P PMI figures of November.

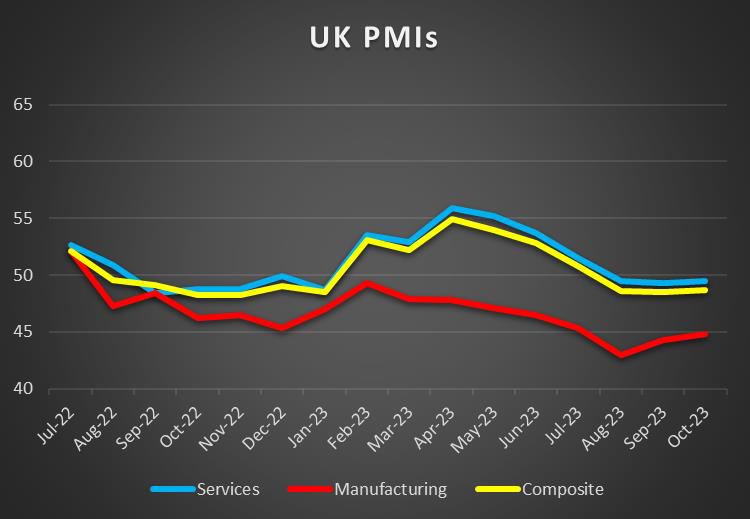

GBP – Preliminary Services PMI in sight

The pound is about to end the week higher against the USD and to a lesser degree against the JPY and the EUR. Overall though the movement could be perceived as a sign of strengthening of the pound. It should be noted that the pound strengthened despite the CPI rates slowing down more than expected, both at a core and a headline level. The slowdown is expected to solidify BoE’s decision to remain on hold, as the cumulative rate hikes seem to be working in slowing inflationary pressures in the UK economy. It should be noted though that BoE policymakers are highlighting the need for rates to remain high for a longer period, an idea that pushes against some market expectations for the bank to proceed with rate cuts earlier. Hence we may see pressures for the bank to proceed with another rate hike easing, yet the fact that the CPI rates are still way above the bank’s CPI target of 2% is forcing the bank to maintain the interest rates at high levels. On a macroeconomic level, we note that September’s employment data tended to show that the UK employment market remained tight, with the average earnings growth rate despite slowing down remained at relatively high levels, implying that the UK employment market may continue to support inflationary pressures in the UK economy.

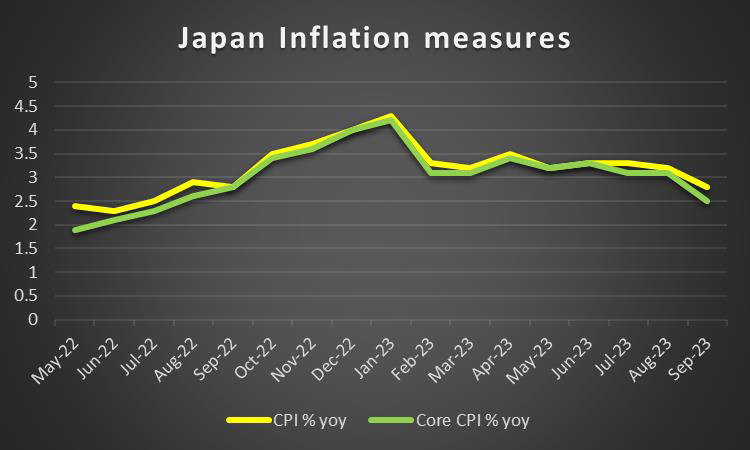

JPY – CPI rates in the epicenter

JPY is about to end the week stronger against the USD, but not against the EUR and the GBP. On a macroeconomic level, we note the wide contraction of the GDP rate for Q3, both on a quarter-on-quarter level as well as on a year-on-year level. The spectre of a recession in the Japanese economy seems to be intensifying. Furthermore, we note that the trade balance turned again into a deficit, albeit not as wide as expected in another negative development for an export-oriented economy like the Japanese one. Hence the role of the Bank of Japan becomes central, as it supports the Japanese economy by maintaining an ultra-loose monetary policy. But there are increasing discussions as to whether the bank is about to start changing its policy, exit ultra-loose settings and move towards a relative normalisation. The comments of Governor Ueda, mentioned also in the last report were characteristic in that direction. On both a monetary level and a macroeconomic level, we highlight the release of October’s CPI rates. Should the rates continue to slow down we may see the market expectations for BoJ altering and thus weaken JPY. Furthermore, we note the release of the preliminary PMI figures for November, especially of the manufacturing sector and a possible reading below October’s 48.7, could signal another wider contraction of economic activity in the key manufacturing sector, intensifying even further worries for Japan’s economic outlook.

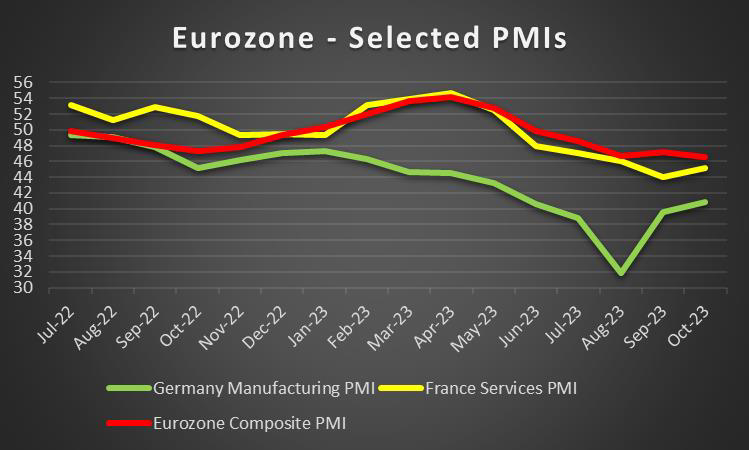

EUR – Preliminary PMI’s in focus

The common currency is about to end the week higher against the USD and the JPY, yet edged lower against the GBP. On a monetary level, we note that the ECB seems prepared to maintain rates at their current levels, as bank officials despite noting the possibility of inflation picking up tend to maintain firmly currently, the idea that the current level of interest rates is able to slow down inflation to the bank’s target. Overall we tend to maintain the view that the current stance of the bank seems to provide some support for the common currency. On a macroeconomic level, we note that the slight contraction of the GDP rate for Q3 was confirmed, while Eurozone’s September industrial growth rate contracted more than expected. On the positive side we note that Germany’s ZEW indicators showed for November, that the economic sentiment improved yet current conditions on the ground for the largest economy of the Eurozone remain difficult. With inflation slowing we turn our attention towards growth and highlight the release of the preliminary PMI figures for November. We place special focus on Germany’s manufacturing sector which is also considered to be the spearhead of Eurozone’s economy. We do expect another contraction of economic activity yet probably shallower which could provide some support for the EUR.

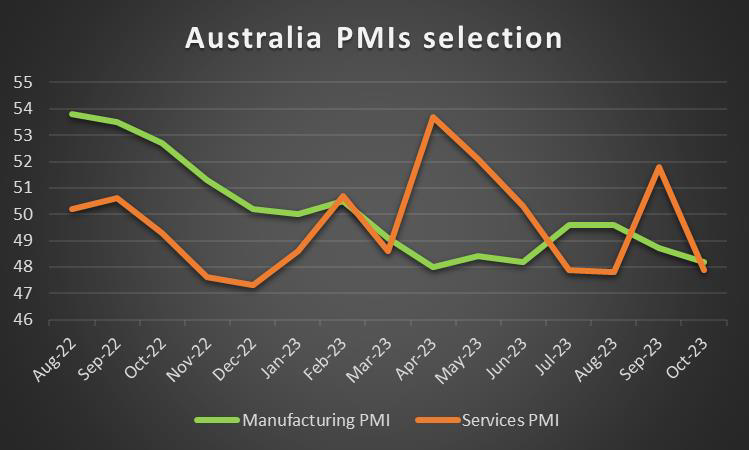

AUD – Fundamentals to take over

The Aussie is about to end the week higher against the USD. On a monetary level, we note that after the last rate hike the market seems to expect that the bank has reached its terminal rate and is to remain on hold for the coming months and well into 2024. Overall the bank seems to maintain a hawkish view, more in the sense of a vigilant stance and such a stance on a monetary level could provide some support for the Aussie, yet more light on the issue is expected to be shed by the release of RBA’s last meeting minutes. On a macroeconomic level, we note the mixed employment data for October with the unemployment rate ticking up, while the employment change figure returned into the positives and the wage price index for Q3, accelerating which could maintain demand and thus inflationary pressures in the Australian economy. On a fundamental level, we note that a positive market sentiment could provide some support for AUD and furthermore, we tend to express our worries about the headwinds faced by China in its recovery efforts, especially in the construction sector which could weigh on the Aussie given the close economic ties of Australia and China. On a deeper fundamental level, we note the progress reported on the possible improvement of the US-Sino relationships, after US President Biden met with his Chinese counterpart Xi Jinping a development that could provide some support for AUD.

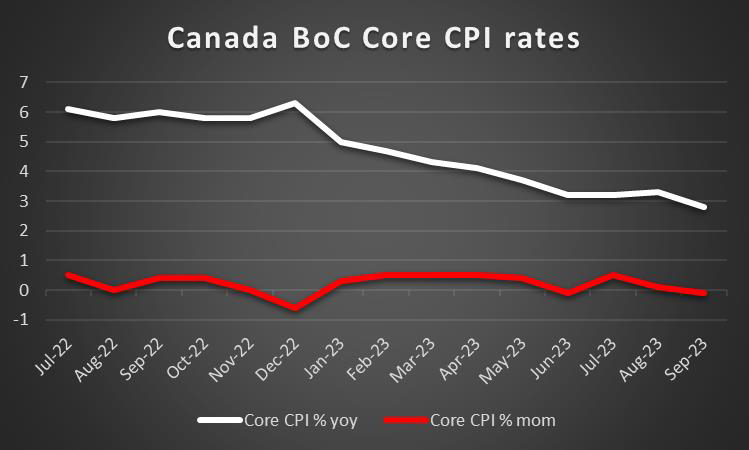

CAD – CPI rates to move the Loonie

The Loonie is about to end the week stronger against the USD. On a monetary level, we maintain the view that Bank of Canada tends to keep a hawkish stance and note that the market increasingly expects the bank to hike rates by 25 basis points in its next meeting. We expect that should the bank maintain its hawkish rhetoric in the coming week, we may see the Loonie getting some support. On a macro level, the market’s expectations for BoC’s further move seem to be linked also to the release of Canada’s CPI rates for October on Tuesday. A possible acceleration of the rates may intensify the market’s expectations for the bank to hike rates and thus support the CAD. Furthermore, we note the release of September’s retail sales growth rate and another contraction of rate could weaken the Loonie. On a fundamental level, we note the fourth continued weekly drop of oil prices may have clipped the gains of the Loonie, given that Canada is a major oil-producing economy. We note that currently demand worries and a slack in the US oil market seems to be feeding oil bears further and should oil prices continue to drop we may see them weighing on the Loonie as well.

General Comment

In the coming week, we expect volatility to ease somewhat in the FX market given that the frequency and gravity of financial releases are to ease. Hence we may also see the USD relenting some of the initiative in the FX market to other currencies, which in turn could allow for a more balanced trading mixed to emerge. As for the US equities markets, we note that the positive market sentiment seems to have been maintained with all three major US stock market indexes, namely the Dow Jones, Nasdaq and S&P 500 ending the week in the greens. The earnings season is still on, yet most of the high-profile companies have already released their earnings reports. Nevertheless, we would like to note on Tuesday the release of earnings reports of Nvidia (#NVDA), Best Buy (#BBY), HP Inc (#HPQ) and Baidu (#BIDU). Overall we expect that should the positive market sentiment be maintained, we may see US stockmarkets aiming for higher grounds. In regards to gold we note that the negative corelation with the USD, seems to be working given that gold’s price recovered last week’s losses. We note that the gold’s price rose possibly also due to the drop of US yields since the start of the week. Should the USD extend its losses in the coming week, we may see gold’s price benefiting.

이 기사와 관련된 일반적인 질문이나 의견이 있으시면 저희 연구팀으로 직접 이메일을 보내주십시오 research_team@ironfx.com

면책 조항:

본 자료는 투자 권유가 아니며 정보 전달의 목적이므로 참조만 하시기 바랍니다. IronFX는 본 자료 내에서 제 3자가 이용하거나 링크를 연결한 데이터 또는 정보에 대해 책임이 없습니다.