An interesting week is about to draw to a close and we prepare for next week’s releases. Yet as these lines are written we still wait for the release of the US employment report for June and Canada’s employment data for the same month, which could alter the overall picture of the market today. In the coming week, on the monetary front, we note the release on Wednesday, of New Zealand’s RBNZ and Canada’s BoC interest rate decisions. As for financial releases, we make a start on Monday with the release of Japan’s current account balance for May, China’s inflation metrics for June, Norway’s CPI rates for June, Eurozone’s Sentix index for July and Canada’s building permits for May. On Tuesday we get Australia’s consumer confidence for July and Business conditions for June, UK’s employment data for May and Germany’s ZEW indicators for July. On Wednesday we get from Japan the corporate goods prices for June and Machinery orders for May and in the American session, we highlight the US CPI rates for June. On Thursday we note the release of China’s trade data for June, UK’s GDP and manufacturing output for May, Eurozone’s industrial output also for May, and from the US the weekly initial jobless claims figure and the PPI rates for June. On Friday we note the release of Sweden’s CPI rates for June, Canada’s manufacturing sales for May and from the US the preliminary University of Michigan consumer sentiment for July.

USD – US CPI rates eyed

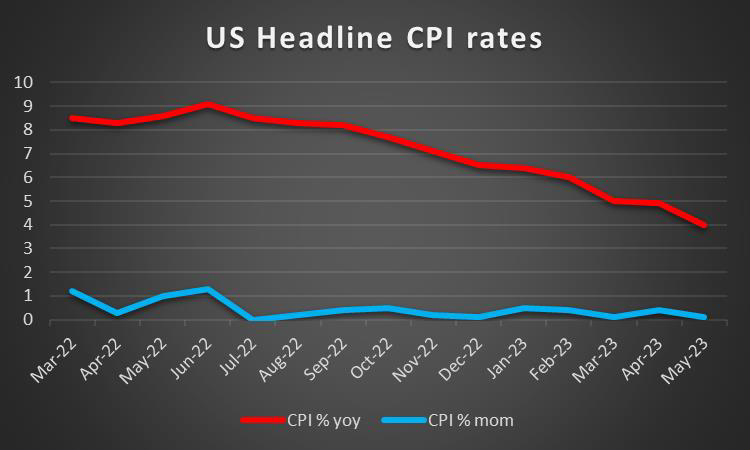

The USD seems about to end the week near the same levels it began, yet as we noted before the US employment report for June with its NFP figure, is still to be released and could alter USD’s direction. Last week did not end that well for the USD as the slowdown of the Core and headline PCE price index growth rates for May, tended to imply that inflationary pressures in the US economy seem to be cooling off. The release tended to enhance market expectations for a possible easing of the Fed’s hawkish stance and thus weakened the USD. Yet a deeper insight into Fed policymaker’s intentions was provided by the release of FOMC’s June meeting minutes. The minutes showed that there was a debate on whether to hike rates in the June meeting or not, yet decided to skip a rate hike, in order to allow for more time to evaluate the overall effect of the cumulative tightening on the US economy. Yet the minutes also tended to imply that the rate hiking path of the Fed has not come to an end. Overall there was little new, yet the reaffirmation of the bank’s hawkish intentions provided support to the greenback. Furthermore, there is still a question of whether the bank is to deliver one or two 25 basis points rate hikes until the end of the year, yet we imagine that should be more dependant on the incoming data. That’s why we highlight the release of June’s US CPI rates next week,which in conjunction with June’s employment report could be the deciding factor behind the Fed’s next interest rate decision on the 26th of July. Should the CPI rates stall to slow down or even accelerate a bit and at the same time the US employment report shows that the US employment market remains tight, we may see the bank’s determination to curb inflationary pressures intensifying, which in turn may provide some support for the USD and vice versa.

GBP – GDP and employment data in focus

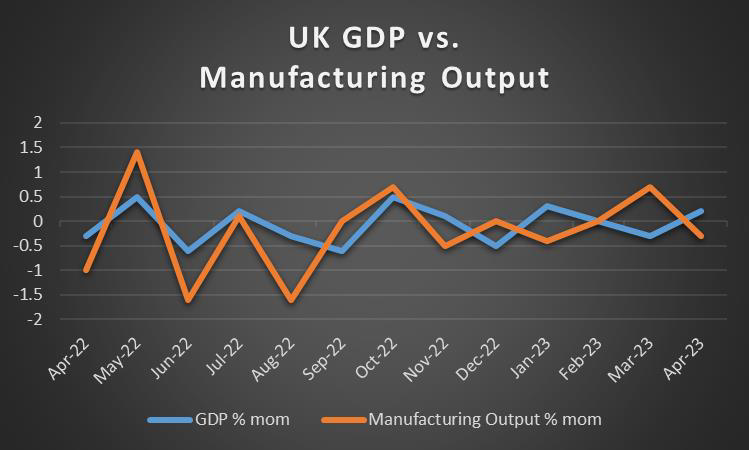

GBP seems to be about to end the week stronger against the USD, the EUR and is losing ground against JPY. We view the market’s expectations for a hawkish BoE to be of the main driving factors behind GBP’s strengthening. It’s characteristic that Megan Greene, which is to join BoE’s monetary policy committee (MPC), stated that rates may remain at higher levels than the pre-coronavirus period even if inflation starts falling. The statement tended to reinforce the view, that the replacement of former BoE MPC member Tenreyro, which tended to be more dovish, is leaning towards the hawkish side and thus may enhance the bank’s aggressiveness in the face of a stubborn inflation. Currently, the markets expect the bank to deliver a 50 basis points rate hike in its early August meeting and continue to raise the interest rate until it hits 6.50% from the current 5.00%. For the time being BoE’s monetary policy outlook and especially the differentials with other central banks seem to be providing support for the pound. Yet as we mentioned on various occasions, monetary policy tightening comes at a cost and it’s characteristic that the growth rate of the UK economy remains at anemic levels. Hence we highlight in the coming week the release of the data for the UK employment market, which seems to be still holding out, while also the release of May’s GDP and manufacturing output growth rates which is expected to be also closely watched.

JPY – Weakening halted

JPY seems about to end the week in the greens against the USD, the EUR and the GBP, in a sign of broader strength. On a fundamental level, the warnings of Japanese officials, hinting towards a possible market intervention seem to have caused some nervousness to JPY bears. It’s characteristic that Reuters reported that “Japan’s top financial diplomat Masato Kanda said on Tuesday authorities were in close contact with U.S. Treasury Secretary Janet Yellen and other overseas officials “almost every day” on currencies and broader financial markets”. The comments could be also viewed as some form of verbal market intervention as the Japanese Government supports JPY with statements, yet has not actually intervened in the markets buying Yens. We expect the issue to be maintained in the coming week albeit it would seem as if JPY found a footing to advance. On the other hand, there were no signs of BoJ altering its dovishness to a comma. Should BoJ’s dovishness be expressed once again by policymakers or even intensify, we may see JPY weakening further as monetary policy differentials could weigh on JPY. On the other hand, JPY’s role in the international markets as a safe haven may also be on display and Japanese currency could attract safe haven inflows should the market’s worries for a possible recession in the US economy and/or a global economic slowdown, intensify. On a macroeconomic level, the better-than-expected Tankan indexes for Q2, seem to show that the sentiment tends to improve for the outlook of the Japanese economy as it’s recording a steady recovery.

EUR – Fundamentals to take over

EUR is about to end the week slightly lower against the USD, but also the JPY and GBP in a sign of a wider weakness. On a monetary level, some of ECB’s policymakers seem to maintain their hawkish views, allowing for market expectations to intensify for possible rate hikes even after the summer. Germany’s BuBa President and ECB policymaker Nagel verified at the beginning of the week his view that the bank had still a long way to go in raising interest rates, which tended to imply that a September rate hike is also quite possible. A scenario that the market seems to be increasingly pricing in. It should be noted though that economic activity is shrinking and that was also verified for the manufacturing sector in June, especially for Germany. At the same time we note that Germany’s trade surplus narrowed implying that the largest economy in the Eurozone, benefitted less from its international trading activity. On the inflation front, we note that Eurozone’s PPI rate showed that prices at a producer’s level contracted once again, in May, yet at a less intense manner as in April. On the demand side of Eurozone’s economy, we note that retail sales failed to grow in May, while the year on year growth rate even contracted, implying that the average consumer in Eurozone’s economy may not be willing and/or able to actually spend more, thus contributing less to its recovery. In the coming week, we note the release of the final HICP rates for June, yet given the lower number of high-impact financial releases stemming from the Eurozone, we expect fundamentals to be in the driver’s seat for the common currency.

AUD – China worries are intense

AUD’s weakening against the USD, for a third week in a row seems to continue. On a macroeconomic level, we note that the weakening of AUD was maintained despite the Building approvals growth rate accelerating widely beyond expectations in May and Australia’s trade surplus for May widening despite being expected to narrow. On a monetary level, we note that RBA during Tuesday’s Asian session remained surprisingly on hold, despite market expectations for the bank to hike rates by 25 basis points. RBA cited that they need “some time to assess the impact of the increase in interest rate”. Yet, the bank noted that inflation still remains high and that some further tightening may be required in the future. On a more fundamental level, we note that Aussie traders tend to turn their attention towards China, given the close Sino-Australian economic ties. Hopes were raised on Thursday as US treasury Yellen traveled to China in an effort to improve the US-Sino relationships, a development that may have a positive impact on the Aussie as well, should it be successful. For the time being though worries about China’s recovery tend to be extended, weighing on the Aussie, as the expansion of economic activity seems to be waning despite the Chinese government’s efforts for the Chinese economy to recover. Furthermore, the deterioration of the market sentiment due to worries of possible overtightening of monetary policy in various developed countries tends to weigh on the Aussie as it is considered linked to the global economic recovery and a riskier financial instrument, as a commodity currency.

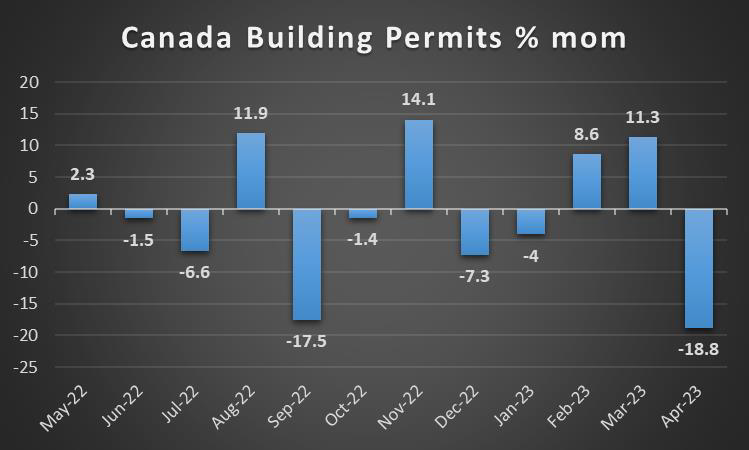

CAD – BoC’s interest rate decision in the epicenter

The CAD is about to end the week in the reds against the USD for a second week in a row, yet the US and Canadian employment data for June are still to be released and may alter that picture. On the monetary front in the coming week, we highlight the release of BoC’s interest rate decision on Wednesday. The bank is expected to hike rates by 25 basis points next week yet the markets’ expectations show tha the issue is not a closed case. It’s characteristic that CAD OIS, currently imply a probability of 58.44% for such a scenario to materialize, while the rest implies that the bank may remain on hold at 41.56%. Despite the fact that BoC in its June meeting took the markets by surprise hiking rates while citing high inflationary pressures and the market’s expectations, we see the case for the bank to remain on hold on Wednesday. The considerable slowdown of the headline and Core CPI rates for May could allow the bank to skip a rate hike in its coming meeting in order to get a more comprehensive understanding of what impact its cumulative monetary policy tightening may have had on the economy. Furthermore the fact that RBA remained on hold while the Fed also stood pat at their last meetings, may provide cover for the BoC as well. In such a case we may see the CAD slipping while a possible rate hike may provide support for the CAD if also the accompanying statement is hawkish. Loonie traders on the other hand should also keep a close eye on oil prices as a possible drop may weigh on the CAD as well.

General Comment

As a closing comment, we expect the USD to maintain the initiative in the FX market over other currencies given that high-impact financial releases stemming from the US are expected. Also at this point, we would like to make a comment about New Zealand’s RBNZ interest rate decision. After thirteen consecutive hikes and raising the cash rate by a total of 525 basis points the market seems to expect the bank to remain on hold Thursday and we tend to concur. Yet we may see the bank in its accompanying statement remaining on guard to fight inflationary pressures in New Zealand’s economy, given that the CPI rate is still at very high levels. As for US equities markets, we note that the earnings season is about to begin and could shift some of the market’s interest towards US stock markets. In the coming week, we highlight the release of Wells Fargo (#WFC), Citigroup (#C) and JP Morgan (#JPM) in a fresh sign about the health of US banks, yet we also point towards aluminium producer Alcoa Inc (#AA). Furthermore, we note that gold’s price seems to be dropping for a third week in a row respecting the slight strengthening of the USD and given that the US yields were on the rise in the past few days. On the side, we note that, worryingly enough the US bond yield curve’s inversion seems to be intensifying. Overall we expect the negative correlation of gold with the USD to be maintained in the coming week and highlight the release of the US CPI rates for June, especially given that gold is also used a hedging instrument against inflation.

이 기사와 관련된 일반적인 질문이나 의견이 있으시면 저희 연구팀으로 직접 이메일을 보내주십시오 research_team@ironfx.com

면책 조항:

본 자료는 투자 권유가 아니며 정보 전달의 목적이므로 참조만 하시기 바랍니다. IronFX는 본 자료 내에서 제 3자가 이용하거나 링크를 연결한 데이터 또는 정보에 대해 책임이 없습니다.