The week we are about to leave behind us tended to move in a rather easy-going mood, yet the coming week may start swinging the markets. On the monetary front, a number of policymakers from various central banks are scheduled to make statements throughout the coming week which could sway the market’s mood. As for financial releases we make a start on Monday with the release of Switzerland’s CPI rates for January. On Tuesday, we get Japan’s GDP rate for Q4, UK’s employment data for December, Norway’s and Eurozone’s GDP rates for Q4, while the highlight of the day is expected to be the US CPI rates for January. On Wednesday we get UK’s CPI rates for January, Eurozone’s industrial production for December and the US retail sales growth rate for January. On Thursday we note from Japan the release of the trade data for January and the machinery orders growth rate for December, while from Australia we get January’s employment data and in the American session from the US we note the release of the Philly Fed Business index for February, the weekly initial jobless claims figure and January’s PPI rates. Finally, on an easy-going Friday, we note the release of the UK retail sales growth rate for January.

USD – CPI rates in the epicenter

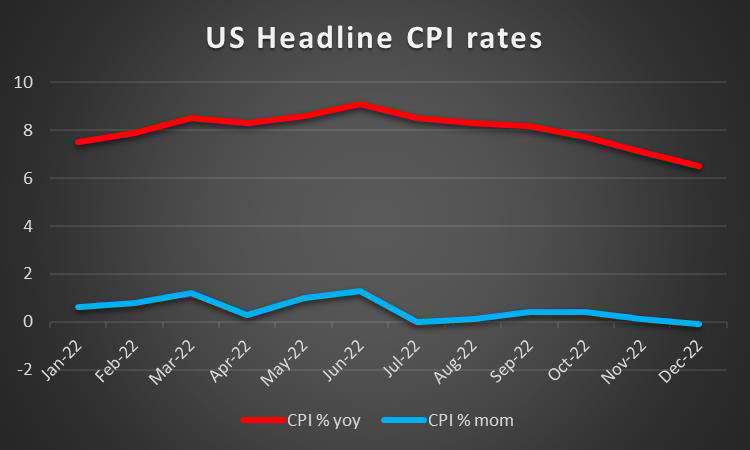

The USD is about to end the week slightly higher than Monday against its counterparts. On the monetary front, we note that we had a number of Fed policymakers making statements. Fed Chairman Powell noted that inflationary pressures have started to ease yet rates have to go higher. New York Fed President Williams highlighted that there is plenty more to do this year in order to get the supply and demand imbalances down, yet he favours rate increases to be at a slower pace. Fed Governor Cook stated that it’s appropriate to move in smaller steps and assess the effects of the cumulative tightening in regards to the economy and inflation. She then added that her hopes for a “soft landing” have increased after the strong jobs report during last week. Fed Governor Christopher Waller raised his concerns that robust jobs numbers run the risk of fuelling consumer spending which would maintain upward pressure on inflation, increasing the probability for it to become entrenched in the economy. Nevertheless, the central bank’s tightening efforts appear to be working, but are “not enough”, adding that the Fed should keep a tight stance for some time. Minneapolis Fed President Kashkari once again declared his resolve that the Fed’s fund rate needs to rise further, as high as 5.4% and if the data support this, maybe even further. The consensus of the bank’s forecasts see the 5.1% as the median terminal rate. That’s why on a macro-economic level we highlight the release of the US CPI rates for January on Tuesday and should the rate slow down even further that could indicate exactly that the monetary policy tightening of the Fed has worked and may ease market worries for a possible extravagant tightening by the bank. On a fundamental level, the challenge to Republicans to raise the debt ceiling, included in President Biden’s State of the Union speech and his, at some points, combative tone tended to make a sensation. Should the debt ceiling rise that would allow for Bidens’ government to actually expand its fiscal policy further, yet that may risk inflationary pressures in the US economy.

GBP – Financial data to shake the pound

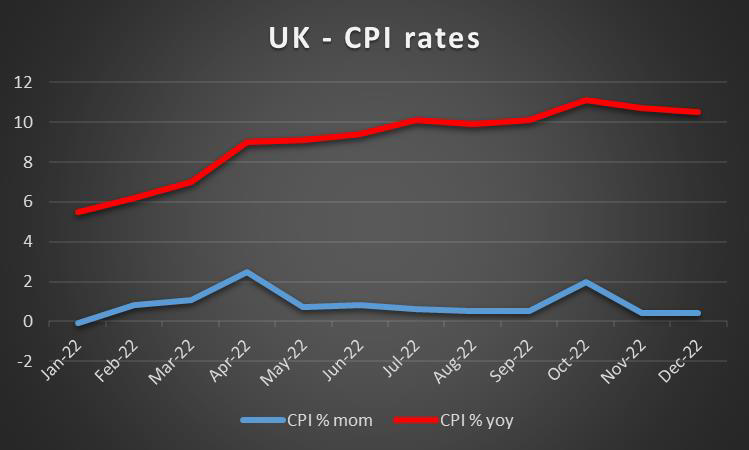

The pound is about to end the week stronger against the USD and the EUR but not JPY. On a macroeconomic level, we note that the contraction of economic activity in the construction sector according to the relative PMI figure for January cannot be in the positives for the UK economy and could be related, if not caused by BoE’s monetary policy tightening. On the other hand, we have to note that the Halifax House prices growth rate was able to remain stable at stagnation levels, a relative improvement for December’s -1.3% mom. Yet the worrying part came on Friday as the GDP rate dropped into the negatives displaying a contraction of the economy. Yet another major issue tormenting the UK is the cost of living crisis, hence we expect the release of UK’s CPI rates for January to be in the epicenter of attention for GBP traders in the coming week. The release is also to be complimented by UK’s December employment data and January’s retail sales and could create some volatility for GBP pairs. On the monetary front we note, BoE MPC member, Katherine Mann’s comments that backed the idea of further rate hikes by BoE as well as her warning that a possible pause may confuse markets should rates rise again. Also, hawkish talk from BoE Governor Bailey tended to support the sterling, as the Governor expressed his concerns about the risks of a persistently high inflation in the UK economy. Please bear in mind that the bank in its latest interest rate decision had signaled a possible downshift in its rate hiking path, while two members of the monetary policy committee dissented with the 50 basis points rate hike decided.

JPY – Choosing the next BoJ head

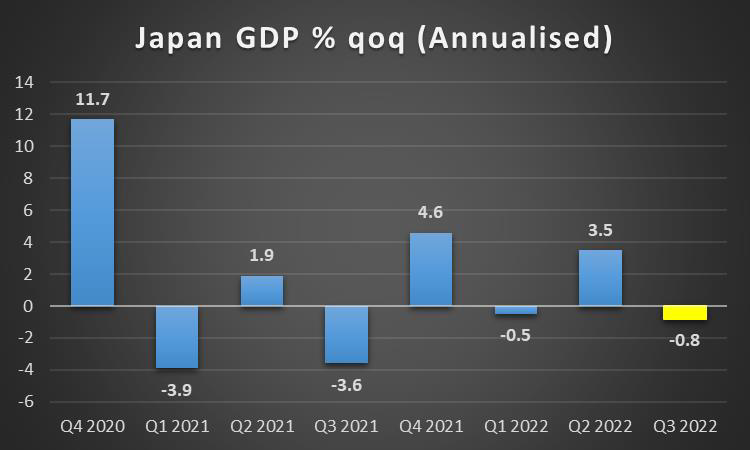

JPY is about to end the week stronger against the USD, EUR and GBP in a sign of broader strength. On a monetary level, the main issue being discussed is the successor of BoJ Governor Haruhiko Kuroda after a report surfaced by Nikkei.com that BoJ deputy governor Amamiya is to be the one, early this week. The report was not confirmed by the Japanese government yet the Deputy Governor is considered to be a dove among BoJ policymakers and would be expected to continue Governor Kuroda’s ultra-loose monetary policy. Yet news just emerged that the Japanese government is considering appointing former BoJ policy board member and economist Kazuo Ueda as the next governor of BoJ. The report by Nikkei.com also stated that the Government had initially approached current BoJ Deputy Governor Amamiya, yet he steadily refused the appointment, please note that JPY edged a bit higher at the release against the USD. Yet in a recent speech of Japanese PM Kishida in Parliament this week, the new Governor is expected to possess strong global communication skills and be able to closely coordinate with global peers. Such a comment could fit perfectly with a former BoJ deputy governor, Mr. Hiroshi Nakaso. A more hawkish shift which may also fall in line with the Japanese Government’s efforts to distance itself from Abenomics, would be former BoJ deputy governor Hirohide Yamaguchi. Mr. Yamaguchi is considered to be a vocal critic of incumbent BoJ Governor Kuroda and his ultra-loose monetary policy settings, and could lead the bank to its first rate hike since 2006. Yet such an interest rate hike could prove to be challenging for Japanese businesses as it could deliver an economic blow, S&P warned. In any case, should Mr. Amamiya be selected that could have a detrimental effect on JPY as he is considered to be the most dovish one among the three, while Mr. Yamaguchi is considered the most hawkish one, and his selection could provide some tailwinds for the Yen. Analysts stated that Japanese Prime Minister Mr. Kishida, may propose the candidate of his selection to the Japanese Parliament as early as next week and his proposal is considered to be a done deal, given that his party enjoys the majority, which could shake the Yen.

EUR – GDP rates in focus

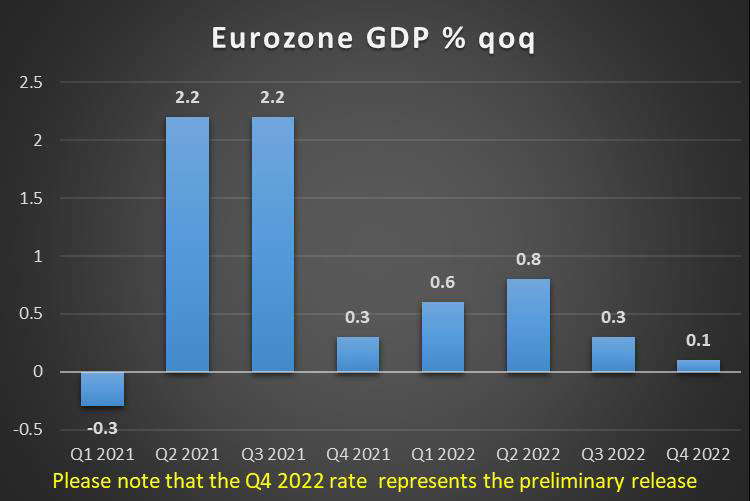

The common currency seems to be edging lower against the USD for the week, but is also losing ground clearly against the JPY and GBP in a sign of a broader weakness. On a macro-economic level, we note that the acceleration of Germany’s industrial orders growth rate for December, yet the disappointment from the contraction noted in the industrial output growth rate for the same month tends to out trump it. The main release though of the week may have been Germany’s preliminary HICP rate for January, whose release has been postponed for more than a week. The results pointed out that inflationary pressures in the German economy eased more than expected, reaching as low as 9.2% yoy and the deceleration may ease ECB’s hawkishness somewhat. Yet we have to note that on a monetary level, ECB Vice President De Guindo’s comments maintained a clear hawkish tone. The ECB Vice President stated in an interview that “I would not rule out that there will be further interest rate hikes after March. The fight against inflation is not won,”. The statement further showcased ECB’s hawkishness and determination to fight inflationary pressures in the Eurozone and raised speculation that the bank may be about to lead monetary policy tightening in an overdrive. On the other hand, ECB’s monetary policy tightening continues to threaten the Eurozone with the risk of a recession, that’s why the release of the second estimate of the GDP rate is expected to be closely monitored next week.

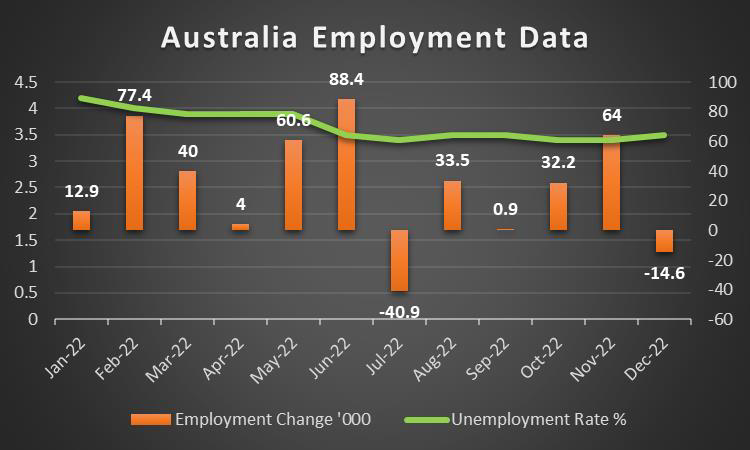

AUD – Australia’s employment data due out

AUD is about to end the week stronger against the USD, despite some weakness being displayed midweek. RBA’s rate hike contributed to the strengthening of the Aussie on Tuesday. The bank as was widely expected hiked rates by 25 basis points and the bank had the confidence to signal more rate hikes to come. The bank’s worries about the inflationary pressures in the Australian economy seem to intensify as Governor Lowe, in his statement mentioned that “In underlying terms, inflation was 6.9 per cent, which was higher than expected”. At the same time, there is confidence in the Australian employment market as the Governor stated that “The labour market remains very tight… Job vacancies and job ads are both at very high levels but have declined a little recently”. Hence it should come as no surprise that the banks’ Governor in his forward guidance stated that “The Board expects that further increases in interest rates will be needed over the months ahead to ensure that inflation returns to target”. Hence we highlight the appearance of RBA Governor Lowe on Wednesday before the Australian Senate. Overall, we see the case for the hawkish stance of the bank to continue to support on a monetary level AUD yet traders should remain also vigilant about China’s fundamentals and reopening. We note that US-Sino diplomatic tensions seem to be on the rise, with the Chinese balloon incident being characteristic. As for financial releases next week, we highlight Australia’s employment data for January to come under the market’s scrutiny. Should the employment change figure return into the positives, hopefully forcing the unemployment rate to tick down, that would imply a rather tight employment market that could support more rate hikes from RBA and thus provide support to the Aussie.

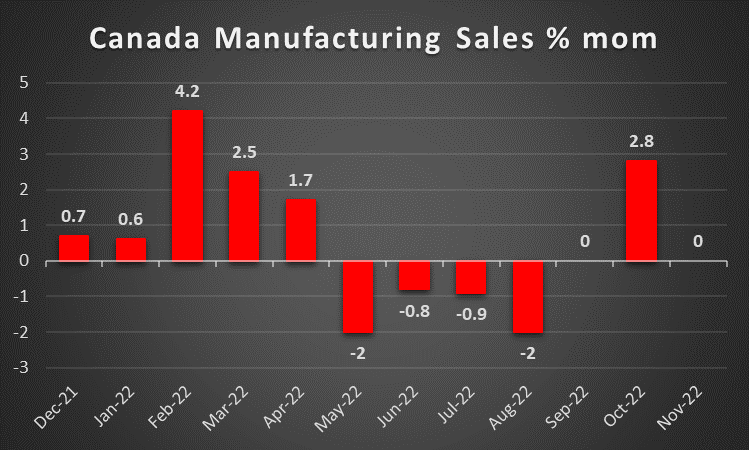

CAD – Fundamentals to take over

North of the US border the CAD is about to end the week lower against the USD. At this point, we would like to note that as these lines are written Canada’s employment data for January are still to be released and could alter Loonie’s direction. On a macroeconomic level, the trade deficit, which was expected to widen, did for December, but not as much as the market expected easing somewhat market worries about the possible adverse effect of Canada’s international trading activities on the economy. Oil prices were on the rise with traders encouraged by expectations for increased demand from China, which could allow oil prices to rise even further, reflecting the positive effect also on the CAD, given that Canada is a major oil-producing country. Also, the drawdown reported by API in its report about US oil inventories for the past week may have provided some support for oil prices yet the effect may have been cancelled out as EIA reported that oil inventories in the US rose further, contradicting API and thus created doubts about the end of the slack in the US oil market. On a fundamental level, we continue to point towards the positive correlation between the CAD and oil prices, which may swell in the coming week. On the monetary front, the Loonie may have found additional support as BoC Governor Tiff Macklem made some hawkish comments, as he was reported stating that the bank is prepared to raise its policy rate further, he also seemed to be quite confident that the bank is not to cut rates anytime soon and that tends to showcase the bank’s hawkishness as well. Overall, given the absence of high-impact financial releases in the coming week, we expect the fundamentals to take the lead regarding Loonie’s direction.

General Comment

Overall and as a general comment, we note that the number of high-impact financial releases from the US is about to increase in the coming week and thus could provide the opportunity for the greenback to retake the initiative over other currencies and lead the markets. Hence we may see the blend of trading opportunities shifting towards the USD. Also, we note that USD stock markets seem to remain relatively unchanged, as if US stock markets maintain a wait-and-see position. Also, US stock markets are still being affected by the earnings season. In the coming week, we note on Tuesday the release from Coca-Cola (#KO), and Airbnb (ABNB) on Tuesday, on Wednesday we note the earnings reports of Cisco (#CSCO), Equinix (#EQIX) and AIG (#AIG) and on Friday of Daimler. Yet there is a plethora of companies that are still to release their earnings reports and sway the market’s mood. We must also note that US stock market participants are also closely monitoring the Fed and Fed policymakers that are scheduled to make statements and could alter US stock market’s direction, while the release of the US CPI rates could have also ripple effects there. On the other hand, we must note that gold’s price seems about to end the week at the same levels it began and more or less seems to have been prevented from making any considerable gains from the US strengthening. Also, the fact that US yields tended to be on the rise may have provided alternative investing opportunities to traders. We expect the negative correlation of gold’s price against the USD to be maintained, with the release of the US CPI rates for January possibly being the highlight. Should the greenback weaken, we may see Gold’s price gaining further.

이 기사와 관련된 일반적인 질문이나 의견이 있으시면 저희 연구팀으로 직접 이메일을 보내주십시오 research_team@ironfx.com

면책 조항:

본 자료는 투자 권유가 아니며 정보 전달의 목적이므로 참조만 하시기 바랍니다. IronFX는 본 자료 내에서 제 3자가 이용하거나 링크를 연결한 데이터 또는 정보에 대해 책임이 없습니다.