The week is about to end and we are to enter the holiday period of the season. A high number of traders are expected to be off line and thus the markets may calm down, yet at the same time thin trading conditions may apply, which in turn allow for unexpected situations to emerge in the markets. Yet the calendar is not totally empty for the coming two weeks. We note on Monday the 22nd of December the release from Australia of RBA’s December meeting minutes, while in China PBoC is to release its interest rate decision, in the UK the final GDP rate for Q3 is to be released and in Canada BoC is to release the summary of monetary policy deliberations for the December meeting. On Tuesday the 23rd of December we get October’s US durable goods orders, the US preliminary GDP advance rate for Q3, Canada’s GDP Rate for October, the US industrial output for the same month and the US consumer confidence for December. On Wednesday the 24th of December we get from Japan BoJ’s October meeting minutes and from the US the weekly initial jobless claims figure, while the following day BoJ Governor Ueda is scheduled to speak and on Friday we get from Japan the December CPI rates of Tokyo and the preliminary industrial output rate for November. On Monday the 29th ion Japan, BoJ is to release the summary of opinions for the December meeting, and on Tuesday the 30th of December we get Switzerland’s December KOF indicator and we highlight the release from the US of the FOMC December meeting minutes. On Wednesday, the last day of the year, we note the release of China’s NBS PMI figures for December and the US weekly initial jobless claims figure. On January the 1st we note the release of China’s Caixin manufacturing PMI figure for December. Finally on Friday the 2nd of January, we note the release of UK’s nationwide house prices for December and the Czech Republic’s revised GDP rate for Q3.

USD – Preliminary GDP rate for Q4 in focus

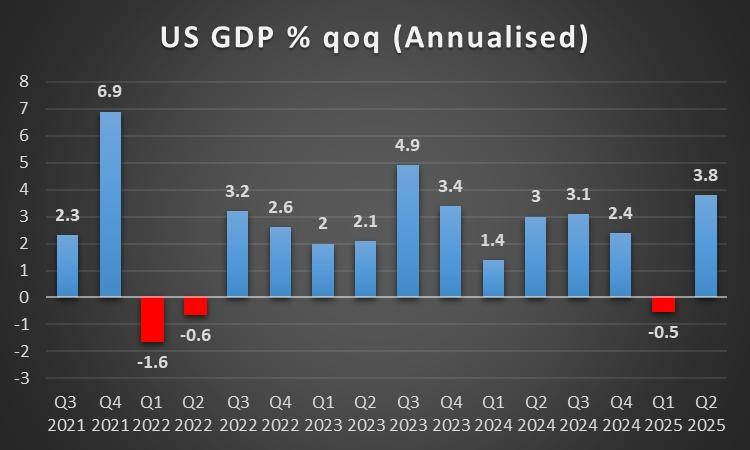

On a political level for the US, we must note that during this week that the US’s beef with Venezuela has continued as the US appears to be pushing forward the “Donroe” doctrine, with President Trump seeking to possible overthrow the Venezuelan Government. In particular, the US has essentially imposed a blockade of all sanctioned oil tankers entering and leaving Venezuela, increasing economic pressure on the country. On a macroeconomic level, we should note the release of the US GDP rate for Q3, which is due out next Tuesday and is expected to come in at 3.2% which would be lower than the prior rate of 3.8% and could thus weigh on the dollar, as the nation’s economic growth may be threatened. Moreover, the US CPI rates for November were released yesterday and tended to showcase easing inflationary pressures in the US economy, with Core CPI easing to its slowest pace since 2021. In turn the financial release may increase pressure on the Fed to continue cutting rates with the new year, which could weigh on the dollar. Lastly, considering this will be our last weekly report for the year, we would also like to note the FOMC’s December meeting minutes which are due out on the 30th of December. Considering how polarized the meeting was, we wouldn’t be surprised to see a predominantly hawkish tone emerging with in the minutes which could aid the dollar.

Analyst’s opinion (USD)

“The dollar could gain considering how Fed policymakers have emerged in droves and questioned the decision for the Fed to cut rates. The deep divisions within the bank as it gears up to welcome it’s new Fed Chair next year makes for a very tricky situation. In our view we wouldn’t be surprised to see policymakers pushing back against a rate cut at the beginning of 2026, which could aid the dollar in turn.”

GBP – UK’s GDP rate for Q3 To be released

On a monetary level for the UK, we definitely must note the BoE’s interest rate decision yesterday where the bank cut rates by 25 basis points to 3.75%. The decision though was a close one with 5 members voting for a rate cut whilst 4 voted in favour of the bank remaining on hold, showcasing that the meeting was what we would refer to as a “live” one. Moreover, considering how close the decision was, any upcoming financial releases in the new year could easily shift the balance of power within the bank which in turn could lead to the next few meetings being decided on a knives edge. Nonetheless, the decision to cut is dovish in nature and with Governor Bailey’s comments that he saw the scope for “some additional policy easing”, the sterling could possibly face bearish pressures in the future. On a macroeconomic level for this week, we would like to note the release of the UK’s CPI rates for November which came in lower than expected at 3.2% on a headline level which is lower than the expected rate of 3.5% and even lower than the prior rate of 3.6%, implying easing inflationary pressures in the UK economy. In turn the easing inflationary pressures in the UK could pave the forward for a more dovish tone being adopted by policymakers with the new year, which could weigh on the pound. Furthermore, of interest for cable traders could be the release of the UK’s final GDP rates for Q3 which are due out on Monday, the 22nd of December. Should the final GDP rate come in higher than 0.1% it may showcase a resilient UK economy which could aid the sterling and vice versa. Lastly, with the new year, the UK’s nationwide house prices rate for December are due out on the 2nd of January 2026 and could thus garner interest from traders.

Analyst’s opinion (GBP)

“The easing of the CPI rates could pave the way forward for a more dovish sentiment from BoE policymakers with the new year, which could weigh on the sterling. The pound may have gained yesterday, but that was as a result of the US inflation print coming in lower than expected.”

JPY – BoJ hikes by 25 basis points, signals more to come.

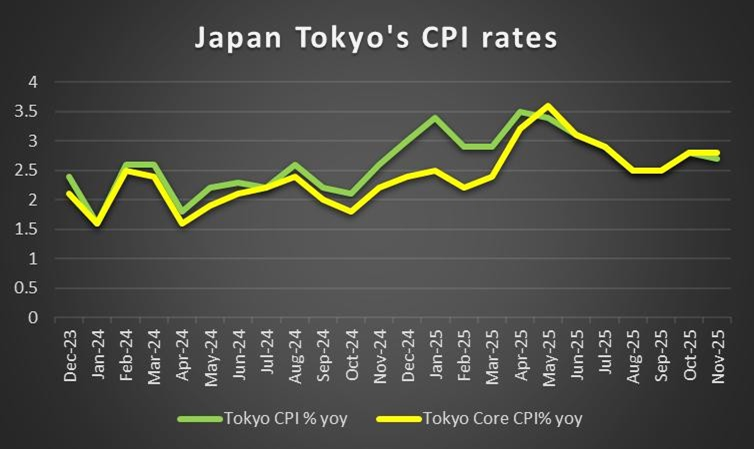

The BOJ’s interest rate decision occurred earlier on today. The bank hikes by 25 basis points, as was widely expected by market participants. Nonetheless, the decision to hike rates brings the bank’s interest rate to levels last seen 30 years ago. In the bank’s accompanying statement it was noted that “the Bank, in accordance with improvement in economic activity and prices, will continue to raise the policy interest rate and adjust the degree of monetary accommodation”, showcasing a clear willingness that the bank may continue to hike interest rates with the new year. Hence, the accompanying statement could be perceived as hawkish in nature and thus should BOJ policymakers adopt an increasingly hawkish tone, it may provide support for the JPY. To end the monetary policy aspect of our paragraph, we would like to note that the BOJ’s meeting minutes and summary of opinions are both due to be released within the next two week. Hence, traders may be looking as to how policymakers may be approaching their monetary policy decisions next year and if some policymakers had opted for a bigger rate hike. Nevertheless, the releases may garner attention as the year comes to an end. On a macroeconomic level, Japan’s nationwide CPI rates for November were released during today’s Asian session and tended to be in line with projections by economists. Specifically, the Core CPI rate on a year-on-year level came in at 3.0%, which was the same as the prior reading. Although it should be noted that the headline rate did come in lower than the prior rate at 2.9% versus 3.0%, tending to imply easing inflationary pressures in the Japanese economy, which may have weighed on the Yen. For next week, the Tokyo CPI rates for December are due out on Friday and participants may be looking to see the latest inflation print for Japan. Hence an acceleration could aid the JPY and vice versa.

Analyst’s opinion (JPY)

“We see the case for the BOJ hiking with the new year as they have clearly signalled their intentions to do so. Albeit the BOJ is facing some pushback from the Japanese Government, yet in spite of this we wouldn’t be surprised to see them continuing with incremental rate hikes.”

EUR – ECB holds the line!

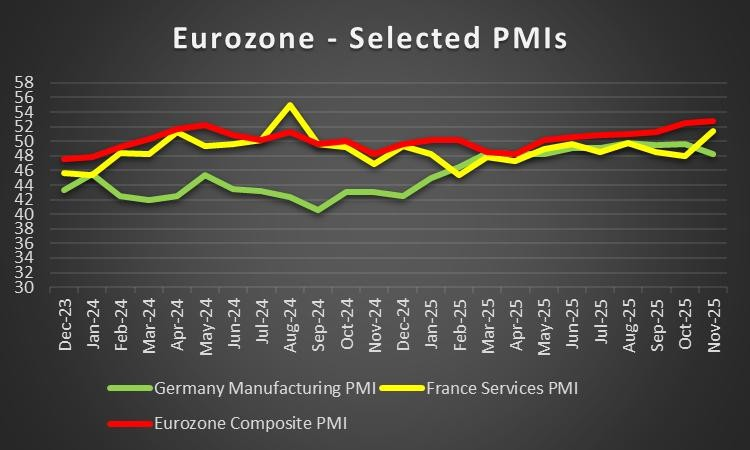

On a monetary level, the ECB remained on hold yesterday. Notably in her press conference, ECB President Lagarde noted that staff expectations for inflation have been revised slightly higher and economic growth forecasts for the next two years have been raised. Moreover, ECB President Lagarde noted that the economy has remained resilient. Overall, the bank’s decision and the upwards revisions tend to imply that the bank may remain on hold for a prolonged period of time, which may be perceived as slightly hawkish in nature. Although, if we’re being honest, it is not something unexpected but nonetheless could be perceived as relatively hawkish in nature which could aid the EUR. On a macroeconomic level, it wasn’t an optimistic week for the Eurozone, as Germany’s preliminary manufacturing PMI figure and France’s preliminary services PMI figure alongside the Zone’s preliminary composite PMI figure all for the month of November, came in lower than expected. Moreover, the Zone’s headline CPI rate slowed down to 2.1% which was lower than expected, implying easing inflationary pressures in the Eurozone. Overall, the narrative emerging from the Eurozone’s financial releases tended to be dovish in nature and may have weighed on the common currency. Looking ahead, it’s set to be a pretty easy going two weeks up until the new year for EUR traders with no major financial releases expected.

Analyst’s opinion (EUR)

“The ECB in our view may likely remain on hold for a prolonged period of time. An issue, though, will be France, who continues to fail to pass a budget once again.”

AUD – RBA minutes due out Monday

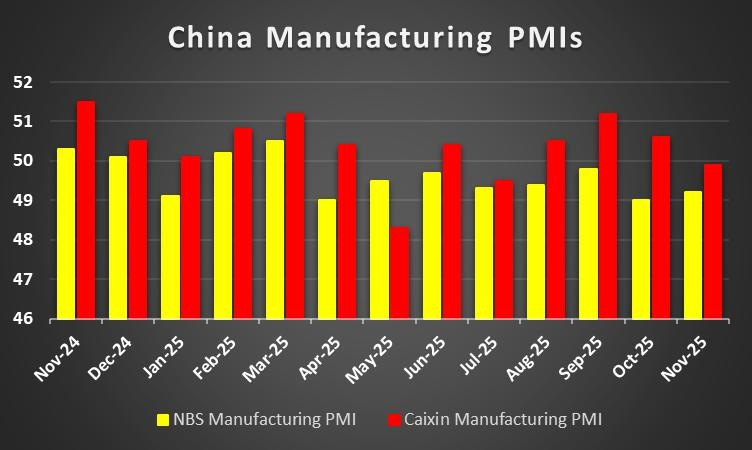

It was a pretty easy-going week for Aussie traders considering there were no major financial releases stemming from Australia. On a general level, the nation is still recovering following the horrific and devastating attack which occurred in Australia this week and thus internal and external observes may be more focused on the Government’s response to the crisis rather, which could lead to minimal references to policy decisions for the coming week or so. On a macroeconomic level, considering the lackluster of financial releases from Australia, we turn to China who is a key trading partner and thus the release of the NBS manufacturing and non-manufacturing PMI figures next Wednesday, which could garner attention from Aussie traders. In particular, should the figures showcase an improvement i.e, narrowing contraction of the sectors or even an expansion, it may imply that demand for raw materials from Australia may increase which could aid the Aussie and vice versa. On a monetary policy level we would like to note the release of the RBA’s December meeting minutes on Monday where we wouldn’t be surprised to see a hawkish tone emerging. In particular, should it appear that the RBA may be considering a rate hike with the new year it may provide support for the Aussie against it’s counterparts. Whereas a more muted tone could have a muted impact on the AUD as the year comes to an end.

Analyst’s opinion (AUD)

“The Aussie may not end the year with a bang, but given their close economic ties with China, there is some interest as the year nears a close. Looking at 2026, the RBA’s stance may be more hawkish than their counterparts which could provide the Aussie with an opportunity to gain some strength.”

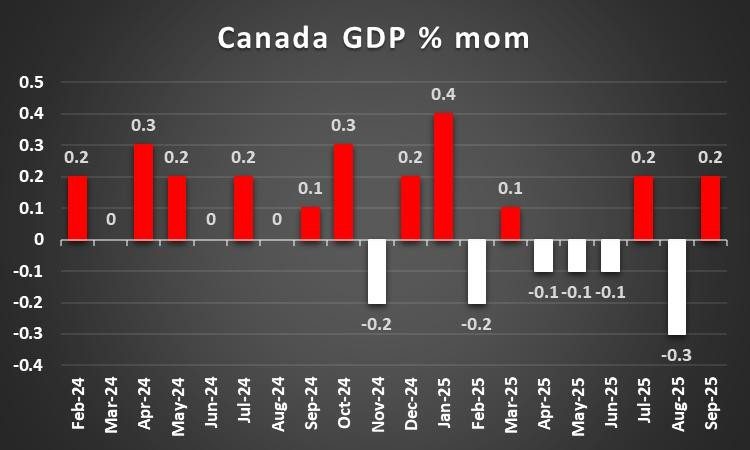

CAD –Canada’s October GDP rates to move the Loonie

On a macroeconomic level, Canada’s CPI rates for November were released earlier on this week. The Core CPI rate on a mom level came in lower than expected, implying disinflation in the Canadian economy as the rate came in at -0.1%. Moreover, some other CPI indicators noted the easing of inflationary pressures in the economy, which in turn may have weighed on the Loonie. On a monetary level, BoC Governor Tiff Macklem noted earlier on this week that the bank will be reviewing its monetary policy framework in 2026, which we are keen on seeing, considering the monetary policy implications. Notably, the Governor noted that “Inflationary pressures continue to be contained despite added costs related to the reconfiguration of trade. Total CPI inflation has been close to the 2% target for more than a year now, and we expect it to remain near the target” which tends to imply that the bank could remain on hold for the foreseeable future. In the coming week traders may be interested in Canada’s GDP rate for October, as it will be the last significant financial release stemming from the nation as the year comes to an end. Hence, an improvement could give the Loonie a boost and vice versa. Moreover, next week we are set to receive the BoC’s deliberations for their December meeting on Monday. The deliberations will be interesting for Loonie traders considering BoC Governor Macklem’s comments which we mentioned in this paragraph. Overall, should the bank imply that they may remain on hold for the foreseeable future it could provide support for the Loonie and vice versa.

Analyst’s opinion (CAD)

“The BoC appears to be in a good position with their monetary policy and thus any adjustments at this stage could be reactionary. As seen by Governor Macklem, the expectation that inflation may remain near the bank’s 2% target showcases to us that an adjustment at this stage may be unnecessary.”

General Comment

As our closing comment for our final edition of the week ahead report for 2026, we’d like to review some of the movements we saw in the markets during the year. Starting with the US Equities markets, all three major indexes formed new all-time highs despite some worries around March. Their continued resilience is optimistic, albeit fuelled by massive AI spending, which we will get to in just a moment. The continued AI spending in our view raises concerns for 2026, as major firms have essentially engaged in self-funding with money flowing between companies investing in each other. An argument has been made that in comparison to the dot com bubble, firms are better off with their cash reserves, yet if tangible results are not produced within the first two quarters of 2026, we may see the AI bubble unravelling. To clarify, we support that the AI developments may produce results and generate revenue in the future, but in order to justify the massive spending incurred this year, such firms may be under pressure to produce results in the near future. Onto the commodities markets, tensions between the US and Venezuela are ongoing and in our view we wouldn’t be surprised to see the US continuing its economic embargo on the nation in an attempt to force the Maduro regime out of office. For Gold, the precious metal has reached historic highs and may continue to do so, as we live in tumultuous times. As a closing comment, we would to wish our readers happy holidays and a happy new year.

이 기사와 관련된 일반적인 질문이나 의견이 있으시면 저희 연구팀으로 직접 이메일을 보내주십시오 research_team@ironfx.com

면책 조항:

본 자료는 투자 권유가 아니며 정보 전달의 목적이므로 참조만 하시기 바랍니다. IronFX는 본 자료 내에서 제 3자가 이용하거나 링크를 연결한 데이터 또는 정보에 대해 책임이 없습니다.