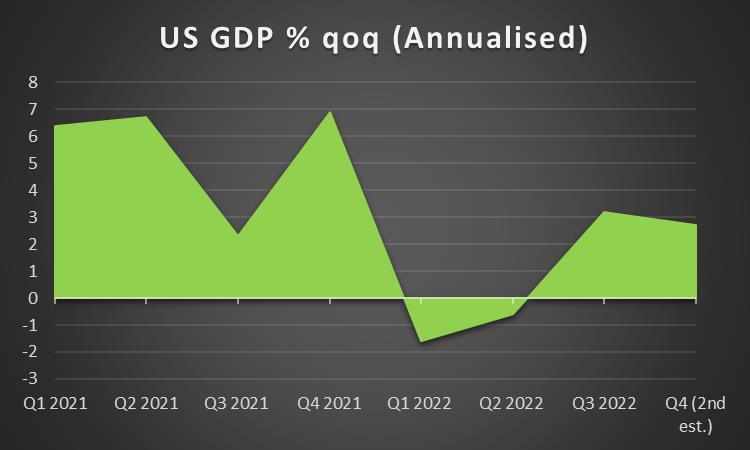

With market worries easing after UBS took over Credit Suisse and the Fed’s interest rate decision, we are about to take a look at what next week has in store for the markets. On the monetary front, we note that a number of policymakers from around the world including Fed officials are scheduled to make statements that could sway the market’s opinion. Also, we note the release from the Czech Republic of CNB’s interest rate decision on Wednesday. As for financial releases, we make a start on Monday with Germany’s Ifo and UK’s CBI distributive trade indicator, both being for March. On Tuesday we note the release of Australia’s retail sales for February, France’s business climate for March and the US consumer confidence for the same month. On an easy-going Wednesday, we note the release of Germany’s forward-looking GfK indicator for April. On Thursday we get Switzerland’s KOF indicator, Eurozone’s business climate and Germany’s preliminary HICP rate all being for March while from the US we note the final GDP rate for Q4 and the weekly initial jobless claims figure. Finally, on a busy Friday, we note the release from Japan of Tokyo’s CPI rates for March, Japan’s preliminary industrial output growth rate for February, China’s NBS manufacturing PMI figure for March, France’s and Eurozone’s preliminary HICP rate for March, UK’s final GDP rate for Q4 and in the American session we note from the US the release of the consumption rate for February, the core PCE price index for February and the final university of Michigan consumer sentiment for March, while form Canada we note the release of the GDP rate for January.

USD – Fed signal’s proximity to terminal interest rate

The USD is about to end the week in the reds against its counterparts. The Fed’s interest rate decision may have been one of the decisive factors behind USD’s weakening. FED Chair Powell on Wednesday announced that the bank would be raising interest rates by 25 basis points as was anticipated. During his speech, Fed Chairman Powel stated that “The U.S. banking system is sound and resilient” to reassure markets for the US banking sector and that the bank will continue to pursue its primary purpose of “maximum employment and inflation at the rate of 2 percent”. We note the change in the tone of Chair Powell’s speech in comparison to the previous interest rate decision, as the statement, on Wednesday seemed to sound dovish, given that the content seemed to signal that a pause of rate hikes nears, while at the same time, the bank stressed once again its determination to curb inflationary pressures. Furthermore, during the Q&A session of his press conference, Chairman Powell also stated that the scenario of a “no-hike” was also considered during Wednesday’s meeting but given how recent SVB’s collapse was, there was little time to measure its long-term impact in addition to conducting an internal review. Fed Chairman Powell also welcomed an independent review. It’s also characteristic that Fed policymakers do not expect the bank to raise rates for the year above 5.25% according to the new dot plot, which implies that only one more rate hike could be expected. On a fundamental level

though we must note that US Treasury Secretary Yellen, stated that the US government is not considering a “blanket insurance” for all US deposits, which tended to inflate uncertainty somewhat.

GBP – BoE’s dovishness on display

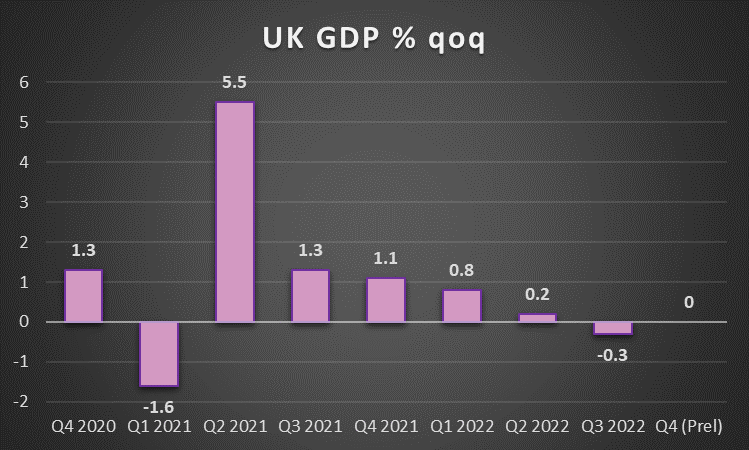

GBP is about to end the week near the same levels against the greenback, weaker against JPY and is losing clearly ground against the common currency. On a monetary level, we note BoE’s interest rate decision. The bank as was expected hiked rates by 25 basis points, raising its interest rate to 4.25%. It should be noted that the balance of power within the bank remained unchanged and the rate hike was voted by 7-2, with two MPC members preferring the bank to remain on hold as in the last meeting. In its accompanying statement the bank highlighted that despite an unexpected acceleration of the CPI rate in the last release, inflation is expected to fall sharply in the coming months of the year. Overall the persistence of the bank that inflation is to fall sharply in the year, tends to keep the possibility of the bank pausing its rate hikes in the near term alive. Yet currently, market expectations are for the bank to deliver another 25 basis points rate hike in its May meeting before pausing. It should be noted that local press quoted BoE Governor Bailey as being “more optimistic” despite rates rising. BoE’s double-edged stance may allow the market to carry about with the pound’s direction in the coming week. On a fundamental level, we note that the UK Parliament voted in favour of the Windsor Framework with the overwhelming majority. The vote not only allows for the EU-UK trade relationships to improve but also solidifies Rishi Sunak’s position as the PM of the UK, following political turmoil since Liz Truss left. On a macroeconomic level, it should be noted, that in line with the accelerating CPI rates the retail sales growth rate accelerated beyond expectations for February, which tended to signal an optimistic sign for the demand side of the UK economy despite the ongoing cost of living crisis tormenting the UK economy. Next week we highlight the release of the GDP rates for Q4, given the substantial worries of the market for the weak growth of the UK economy.

JPY – Safe haven outflows for the Yen

JPY is about to end the week stronger than the weakening USD, near the same levels against the pound and is edging higher against the EUR over the past few days. It could be the case that the easing of market worries about the turmoil in the banking sector since Monday may have led JPY to experience some safe haven outflows, yet the Japanese currency seems to be benefiting from USD’s weakening. Hence we tend to highlight JPY’s double nature, as a national currency and an international safe haven, which may be an important factor behind its direction for the coming week. On a monetary level the summary of opinions for BoJ’s March interest rate decision, reaffirmed the current board’s support for the bank’s ultra-loose monetary policy, yet some cracks seem to have appeared, as the negative side-effects of the bank’s dovish stance were debated. It will be a burden upon the new BoJ Governor, Mr. Ueda, to take the lead and alter the bank’s stance, yet for the time being, we expect no radical changes and that may weigh on JPY over the coming

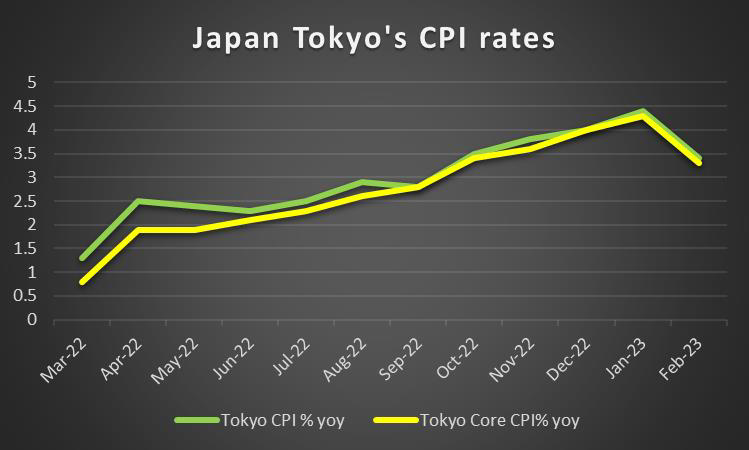

week. It should be noted that on a macroeconomic level the easing of the country’s CPI rates for February, both on a headline and a core level tends to ease also the pressure on the bank to tweak its monetary policy. In the coming week, we note the release of Tokyo’s CPI rates for March on Friday, which is to provide a glimpse at the tendencies characterizing the inflationary front in Japan.

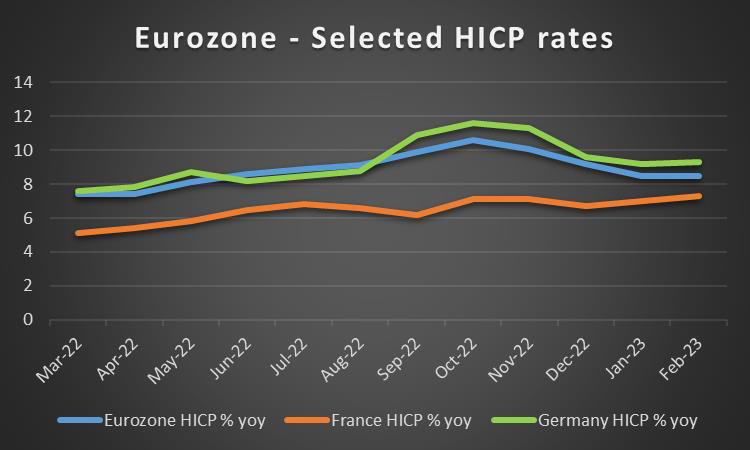

EUR – HICP rates at the center of attention for EUR traders

The common currency was on the rise against the USD and GBP yet seems to be edging lower against the JPY for the week. On a monetary level, we note that ECB President Lagarde’s comments tended to boost EUR traders’ confidence that the bank is to continue to proceed with further monetary policy tightening. In the dilemma set before the European central bank on whether to ease its hawkishness in order to calm the banking sectors’ turmoil and further tightening to curb inflationary pressures, ECB President Lagarde stated that there is no trade-off between the two. She stated that the ECB is able to provide an aiding line if needed to European banks through its existing toolkit, yet at the same time, she highlighted that the option for the bank to continue hiking rates remains open. Yet further rate hikes are to be data-dependent and especially on the inflationary front. Hence we highlight the release of the area’s preliminary HICP rates for March next week, which is expected to gather substantial attention from EUR traders. Should the rates slow down convincingly, we may see the pressure on the bank to maintain its hawkish approach easing. For the time being the market seems to be pricing in another 25 basis points rate hike in its next meeting and another on in the July meeting before pausing, a scenario that would bring the refinancing rate to 4%. On a macro level, data tend to imply that the situation remains worrying despite the improvement of various preliminary PMI figures for March, Germany’s manufacturing sector showed another, deep contraction of economic activity for the month. Also Germany’s ZEW indicators for the same month, which showed a more pessimistic outlook and deteriorating conditions on the ground for the largest economy of the Eurozone which tended to feed worries for the economic outlook of the largest economy in the Zone. On a fundamental level, we note the political and social unrest in France as Macron’s Government enforced the rise of the retirement age by two years, from

62 to 64. Should the issue magnify, we may see it having an adverse effect on the common currency given a possible slowdown of the second-largest economy in the Eurozone and the overall uncertainty.

AUD – Mixture of Chinese and Australian data for Aussie traders

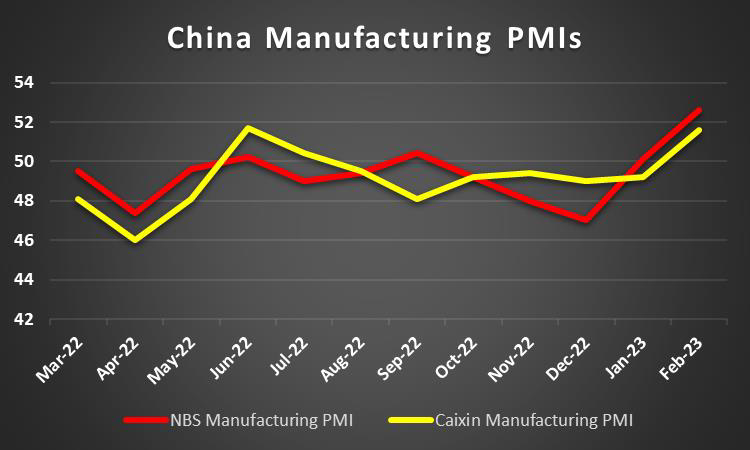

AUD seems to remain relatively unchanged against the USD, maybe edging a bit lower as the week draws to a close. On a monetary level, we note that RBA Assistant Governor Kent seemed to downplay the importance of the banking sector crisis in deciding monetary policy. It was characteristic as he was reported stating that “the Board would consider financial conditions at its next policy meeting in April, but that was just one of many factors”. There was a wide discussion whether the bank would pause its rate hiking path in its next meeting or not, yet the recent rate hikes of the Fed and ECB seem to suggest otherwise. For the time being, we note that the market widely expects the bank to remain on hold in its early April meeting, according to AUD OIS. It should be noted that the bank in the accompanying statement of Governor Lowe for its latest interest rate decision seemed to be easing its hawkishness, also highlighting the possibility that despite an acceleration of the inflation rate, the CPI rate may have peaked. On a more fundamental level, a possible improvement of the market sentiment may benefit the commodity currency AUD while on the flip side, a possible deterioration of the US-Sino relationships may weaken it, given the close Sino-Australian economic ties. On a macro level, we note the contraction of economic activity as displayed by the preliminary PMI figures for March, particularly in the manufacturing sector. In the coming week we note the release of the retail sales growth rate for February which is to show how healthy the demand side of the Australian economy is, while we also highlight the release of China’s NBS manufacturing PMI figure and should the indicator’s reading rise further, that could signal a faster expansion of economic activity in the Chinese manufacturing sector and thus could imply more exports of raw material from Australia to China.

CAD – GDP rates at the end of the week eyed

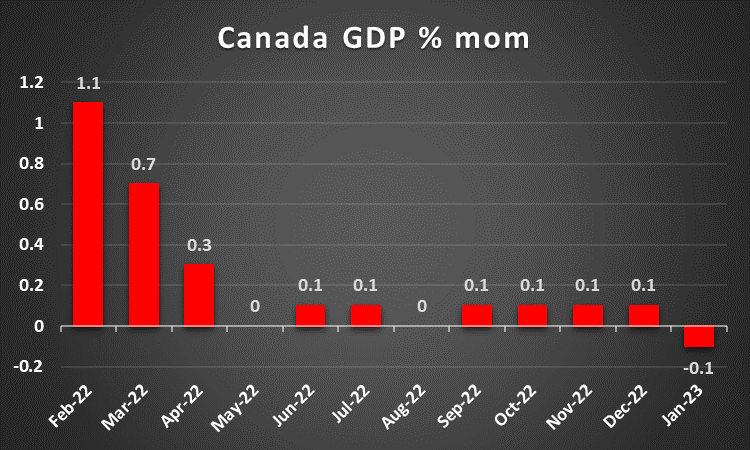

Also, the CAD seems to show little movement against the USD for the week and is about to end near the same levels it began if not lower. It should be noted that Canada’s January retail sales are still to be released and could alter the Loonie’s direction. On a macroeconomic level, we highlight the slowdown of the core and headline CPI rates on a year-on-year level, which may ease the market’s pressure on BoC to resume its rate hiking path. It was characteristic that the bank remained on hold in its last meeting on the 8th of March. It should be noted though that the bank was concerned about inflation remaining above its 2.00%±1.00% target range as in its deliberations ahead of the release the bank noted that services inflation “is proving sticky”, as per minutes released last Wednesday. For the time being, we note that the market expects the bank to deliver another rate hike in the bank’s April meeting hence any dovish comments by BoC policymakers may weigh on the Loonie. On a more fundamental level, we note that WTI’s price seems to edge higher for the week and should the bullish tendencies for the commodity’s price be maintained, we may see some support building up also for the CAD given that Canada is a major oil-producing country. As for financial releases, we would note the release of Canada’s GDP rate for January on Friday and an additional contraction may weaken the Loonie.

General Comment

As a closing comment, should there be no surprises, we may see the market’s worries easing, possibly a normalisation process beginning, despite the situation being still quite fragile. It’s characteristic how market worries suddenly intensified during today’s European session after Deutsche Bank’s share price dropped almost 9% after a sudden rise in the cost of insuring against its default. Should the issue blow out of proportions, we may see EUR tumbling and the possibility of evolving in a full melt down of the market is to be increased. Also, we note that the frequency and gravity of high-impact financial releases tends to ease, which may allow for calmer thoughts among market participants and may provoke an easing of USD’s dominance in the FX market. On the monetary front, we would like to note the rate hike of the Swiss National Bank by 50 basis points on Thursday, despite the turmoil in the Swiss banking sector and its suggestion that more monetary policy tightening is coming. The release tended to provide instant support for the Swiss Franc which is about to come out stronger for the week against the USD. In the equities market, we note that the main US indexes remained relatively unchanged since the start of the week maybe even gaining a bit. A possible improvement of the market sentiment in the coming week may allow them to rise even further and we would highlight to that end, any statements of Fed policymakers. Also, the drop of US yields seems to allow the USD to weaken further for the week while at the same time allowing for gold’s price to edge higher. The negative correlation of the precious metal’s price with the USD seems not to have been on display this week as gold’s price remained relatively unchanged, failing to take advantage of the weakening USD. Nevertheless, the rise above the psychological threshold of US$2000 per ounce at some point during the week was a reminder of what gold’s bulls are capable of once the greenback weakens.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.