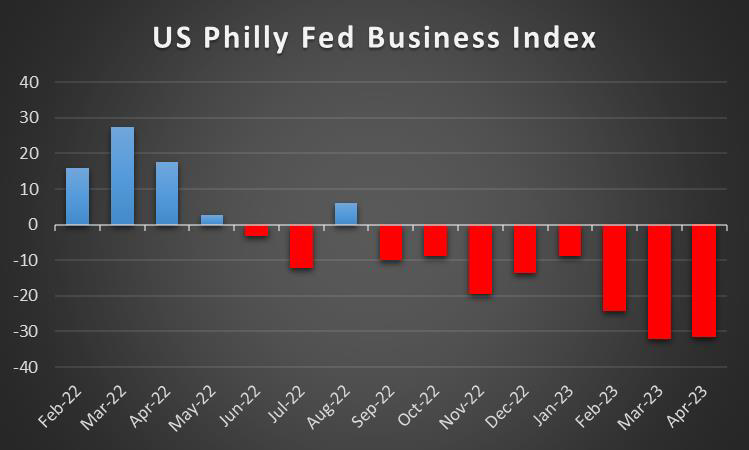

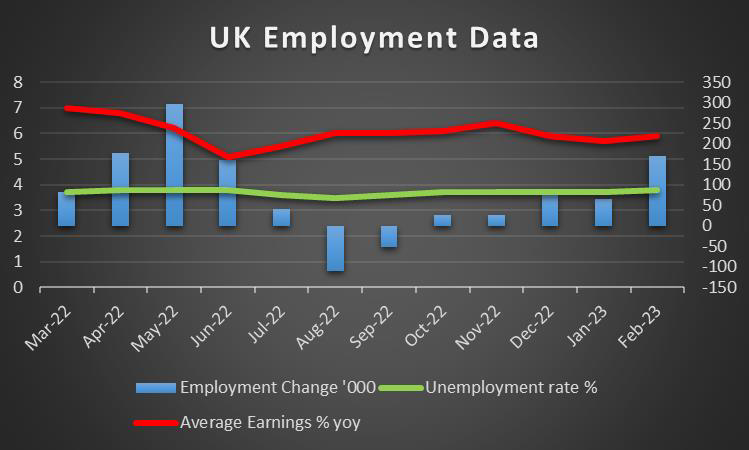

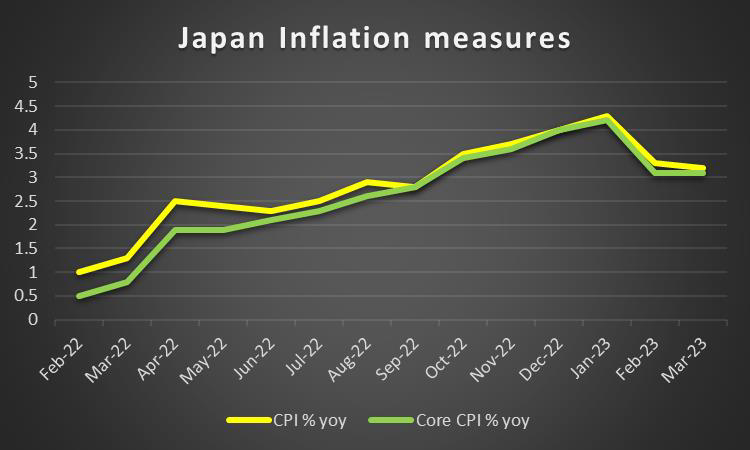

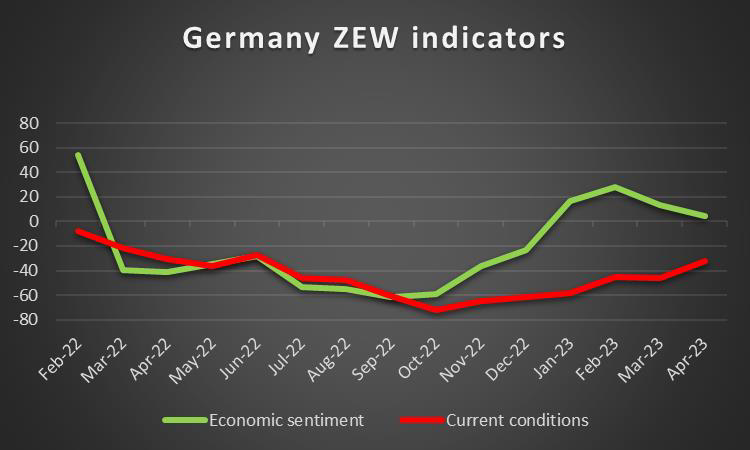

Market worries on a fundamental level tend to remain present as we glance into what next week has in store for the markets. On the monetary front, we note that RBA is due to release its May meeting minutes while a number of policymakers from various central banks are scheduled to make statements and could sway the market’s opinion in either direction. As for financial releases, we make a start on Monday with Japan’s corporate goods prices for April and Sweden’s inflation metrics for the same month. On a packed Tuesday, we note the release of China’s industrial output and retail sales for April, UK’s employment data for March, the Eurozone’s second estimate of the GDP rate for Q1, Germany’s ZEW indicators for May, the US retail sales, Canada’s CPI rates and the US industrial output all for the month of April. On Wednesday, we get the release of Japan’s preliminary GDP rate and Australia’s wage price index both for Q1. On Thursday, we note the release of Japan’s trade data for April and Australia’s employment data for the same month whilst from the US we await the weekly initial jobless claims figure and the Philly Fed business index for May. On Friday we note the release of New Zealand’s trade data and Japan’s CPI rates, both for the month of April whilst during the American session we note Canada’s trade data for March.

USD – Is the US about to default?

The USD seems about to end the week higher against its counterparts. On a fundamental level, market jitters of the US Government potentially defaulting on its debt, have intensified after a high-stakes meeting between US President Biden and US lawmakers, where they failed to reach an agreement about raising the debt ceiling, while another meeting, scheduled for Friday was postponed, implying a lack of common ground between the two parties. The recent comments of US Treasury Secretary Yellen yesterday, that a US default would produce an economic and financial ‘catastrophe’ was characteristic, whilst analysts speculate that the “X-Date” may be as soon as June 1st. The two sides have committed to meeting on a daily basis until an agreement is reached, however we expect the issue to drag on, with the possibility of it being resolved at the very last minute and that may weigh on the market sentiment, especially in the equities markets. Overall, we note the complexity of fundamentals leading the US markets, which currently seem to bear a certain degree of uncertainty given that the stakes are high. On a macroeconomic level, we note that April’s US employment data showcased the tightness of the US labour market with the NFP figure rising and the unemployment rate dropping to practically record low levels, whilst the average earnings growth rate accelerated. This implies that the US employment market may continue feeding inflationary pressures in the US economy. On the other hand, the CPI rates tended to show a different picture. The slight easing of the year-on-year rates was welcomed, yet the acceleration of the month-on-month rates served, as a strong reminder that inflationary pressures are still simmering under the surface. The release tended to send out mixed signals which seemed to have puzzled traders and tended to allow for the continued ambiguity regarding the Fed’s intentions. It was characteristic on a monetary level, that NY Fed President Williams warned on Tuesday, that should inflation not come down, interest rates may have to be increased further. Furthermore, Fed Board Governor Jefferson tried to play down the issue, as he stated that the US economy is slowing down in an “orderly” manner, which also implied optimism that inflation is cooling down. Overall, should Fed policymakers lean on the hawkish side, we may see the USD gaining some support and vice versa, while market worries for a possible US default may weaken the USD unless safe-haven inflows come to the greenback’s rescue.

GBP – BoE hikes rates, warns for more tightening

The pound seems to be losing ground against the USD and JPY, whilst it tends to remain rather stable against the EUR. On a monetary level, we note BoE’s interest rate decision to hike rates by 25 basis points as was widely expected by market analysts. In its accompanying statement, the bank noted that “risks around the inflation forecast are skewed significantly to the upside” despite expecting that inflation “is expected to fall sharply from April”. Also, the bank seems to have dropped its expectations of the UK economy to enter a recession, with the GDP rate being revised from -0.3% to 0.9%yoy by the middle of next year, the largest upwards revision in the bank’s history. In its forward guidance, the bank opened the door to the potential of future rate hikes with the market seeming to position itself in anticipation of this scenario materializing, in the bank’s June and July meetings currently. Also, BoE Governor Bailey’s hawkish comments that inflation remains too high, implied more rate hikes to come. Please note that there is a possibility that the rate hikes may be ending after the summer. The BoE Governor also stated that past rate hikes will weigh more on the economy in the coming quarters, which would also support the idea of the CPI rate slowing down in the coming months. On a macroeconomic level, we note that the Halifax House prices growth rate showed a contraction, possibly also as a result of the BoE’s monetary policy tightening. On the other hand, the release of the GDP rates showed a considerable slowdown on a year-on-year level, while on a quarter-on-quarter level, the anemic growth highlighted prior assumptions of BoE of a flattening GDP rate. Overall, we continue to place considerable focus on BoE’s monetary policy as a factor in deciding the pound’s direction, while the macroeconomic aspects may slightly influence the pound.

JPY – GDP and CPI rates to catch JPY’s attention

JPY is about to end the week flat against the USD, while it gains against the GBP and EUR. On a fundamental level, we note that the Japanese currency may have gotten some safe-haven inflows, given the market worries about a possible recession in the US economy, the possibility of a US default and the risks surrounding the US banking sector. In any case, we expect JPY’s dual nature as a national currency and a safe haven trading instrument, to remain present and if so, could get additional support should the market sentiment become more risk-averse and vice versa. On a monetary policy level, we note the release of BoJ’s summary of opinions for its May meeting. The document practically highlighted the bank’s dovish stance, as it stated that “Given that the inflation rate is likely to decline and a heightening of uncertainties regarding overseas economies has been seen, the Bank should continue with the current monetary easing”. The document practically sealed the idea that the bank is not in a hurry to radically overhaul its ultra-loose monetary policy anytime soon, despite the changing of the guard with Mr. Ueda taking over from Mr. Kuroda, as the new bank Governor. Overall, we see the case for the bank’s dovish stance to continue to weigh on the JPY, as the interest rate differentials in comparison to a number of other central banks such as the ECB and BoE seem to continue to widen. On a macroeconomic level, we note the contraction of the All Household spending growth rate for March, which was indicative of a deteriorating demand side of the Japanese economy, while the current account surplus widened for the same month, implying that the economy benefited from the international payments system. In the coming week, we highlight the release of the preliminary GDP rate for Q1, which would allow us to truly assess the impact of the bank’s ultra-loose monetary policy on economic activity in Japan, while the CPI rates near the end of the week could potentially provide further clues about BoJ’s assumption that inflationary pressures are easing.

EUR – Fundamentals to lead the way

The EUR seems to be losing ground to a greater or lesser degree against the USD, JPY and GBP for the week, implying a general weakening of the common currency. On a fundamental level, market worries about the economic outlook of the Eurozone are still present, albeit to a lesser degree. In contrast to easing market worries for continued social unrest in France and Germany, but also the wider Eurozone. However, on Thursday we received the announcement of the German rail unions going on strike. Hence we plan to continue monitoring the issue, as should it flare up once again, we may see a negative impact on the area’s growth. On the monetary front, we note that Germany’s Bundesbank president Nagel implied that two more rate hikes are possible until the summer break and also mentioned that nothing is off the table for the September meeting. The comments were more hawkish than market expectations, which anticipate consecutive interest rate hikes of 25 basis points, during the bank’s June and July meetings before pausing rate hikes in the September meeting. On the other hand, the slowdown of inflationary pressures, with the exception of the core rate which tends to prove to be slightly more sticky, may suggest that market expectations are on track and Nagel may be getting a little bit ahead of himself. Overall, should the hawkish rhetoric be maintained by ECB policymakers, we may see the common currency getting some support on a fundamental level.

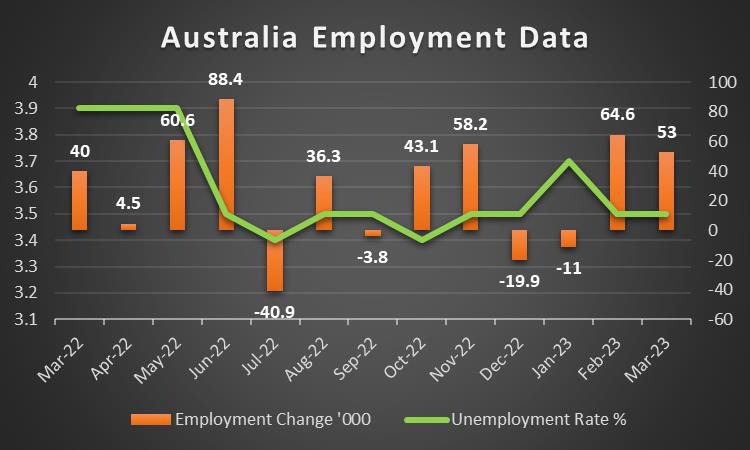

AUD – Australian employment data in focus

The Aussie tended to edge lower for the week against the USD. On a fundamental level, market worries and a slightly risk-off market attitude tended to weigh on the Australian currency, which as a commodity currency may be considered a riskier asset. Should the market worries on a fundamental level intensify, we expect the market sentiment to weigh in even further on AUD in the coming week and vice versa. On a monetary level, after RBA’s rate hike at the beginning of the month, we tend to maintain the view that the bank continues to lean on the hawkish side. Hence we highlight the release of the bank’s May meeting minutes on Tuesday and Aussie traders alongside analysts are expected to scrutinize the document for any indications of the bank’s intentions. On a macro level, we note the slight contraction of the building approvals growth rate, probably also as a result of RBA’s monetary policy tightening, whilst also noting the slight deterioration of business conditions for April. In the coming week, we highlight the release of Australia’s employment data for April and the wage price index for Q1, which is expected to accelerate and if so would imply that the

Australian employment market continues to facilitate inflationary pressures. Yet Aussie traders may also be interested in Chinese data given the close Sino-Australian economic ties. It should be noted that China’s trade surplus for April widened, which was considered a positive for the Chinese economy, yet the exports growth rate slowed down considerably and the import growth rate contracted even deeper into the negatives, both indications of a slowdown, if not a contraction of economic activity in China. In the coming week, we note the release of China’s April industrial output, urban investment and retail sales growth rates, which are expected to give us further indications of economic activity in China and how healthy the demand side of the Chinese economy is. Furthermore, given the close Sino-Australian economic ties, traders may be eagerly awaiting if China’s newly appointed Top Financial regulator Li Yungze a former banker, will rock the boat and bring forth any rapid changes or will choose to maintain the status quo.

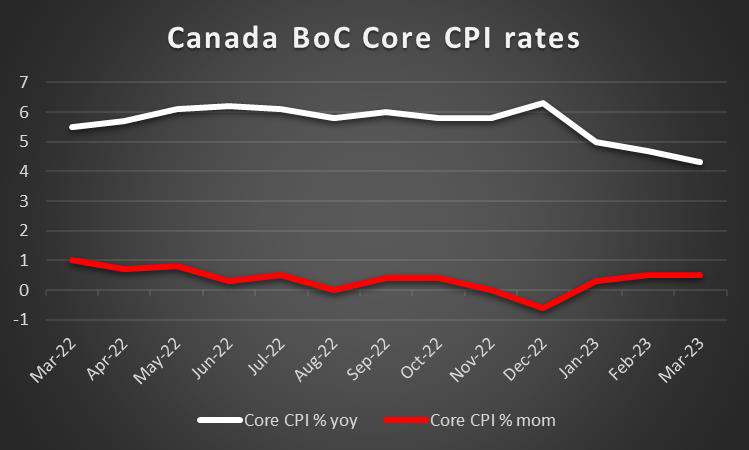

CAD – CPI rates eyed

The Loonie seems to be about to end the week weaker against the USD. On a macroeconomic level, we note the far better-than-expected employment data for April which was released last Friday. It was characteristic that the employment change figure rose, instead of dropping as expected, while the unemployment rate remained unchanged near record low levels, with both indicators showcasing the tightness of the Canadian employment market. In the coming week, we highlight the release of Canada’s CPI rates for April and given the relatively tight Canadian employment market, a possible acceleration of the CPI rates, could prompt the BoC to reconsider another rate hike in its June meeting, thus supporting the CAD. On the other hand, further cooling of inflationary pressures may weaken the Loonie, as it could solidify the bank’s stance to remain on hold. On a fundamental level, we note that oil prices remained relatively unchanged, as traders continue to keep demand and production levels under watch on a global level. Should oil prices escape their relative inactivity, they may provide some support for the CAD should they rise and vice versa, given that one of the main products driving the Canadian economy is oil. Therefore, we cannot understate the possible negative impact of the wildfires in Canada’s key hydrocarbon province have forced Oil producing companies, to reduce production by approximately 320,000 barrels of oil per day, which may have facilitated to the Loonie’s deterioration against the greenback. On the monetary front, we note that BoC’s decision to pause its interest rate hiking path may weigh a bit on the CAD, as the monetary outlook differentials widen, with central banks that continue their hiking path.

General Comment

As a general comment we expect, in the FX market in the coming week that the USD may relent some of the initiative to other currencies, given that the frequency and gravity of US financial releases are to be reduced. Such a development may create a more balanced blend of trading opportunities for market participants. Also given that many high-profile companies have already released their earnings reports for Q1, we may see some market interest shifting towards the FX market from US stock markets, yet overall given the low number of high-impact financial releases the greenback’s impact may prove to be lower than last week. Nevertheless, for US stock markets, we would like to note the release of the earnings reports of Home Depot (#HD) and Vodafone (#VOD) on Tuesday, Cisco (#CSCO) on Wednesday and Walmart (#WMT) and Alibaba (#BABA) on Thursday, which may allow for more focus to be placed on the retail sector, also showing another aspect of the demand side of the US economy on a macroeconomic level. Overall US stock market participants are expected to navigate through a number of issues, including market worries about a possible recession in the US economy, jitters surrounding the US banking sector, the possibility of the US defaulting on its debt, earnings releases and the Fed’s intentions, making fundamentals somewhat perplexed. Should the market sentiment turn more risk-off, we may see US stock markets being in the reds in the coming week. Furthermore, gold’s price seems about to end the week slightly lower. The shiny metal may have gotten some support from the drop in US yields during the week and seems about to maintain the negative correlation characterizing its relationship with the USD. Overall we expect the latter to come to the forefront once again next week and should the USD continue to be on the rise, we may see gold’s price weakening further.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.