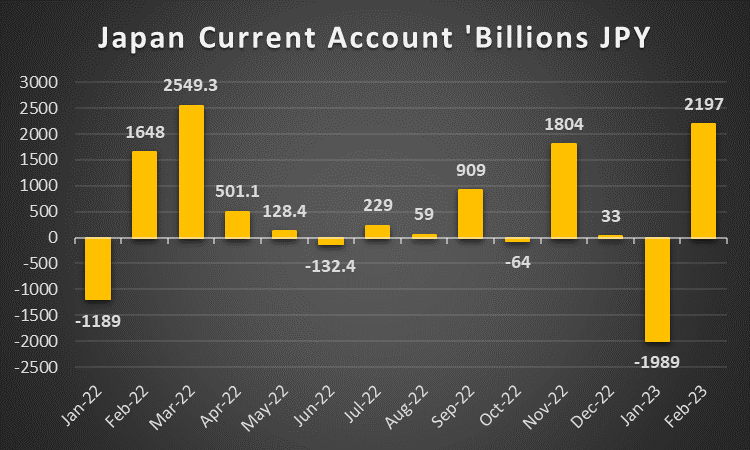

Market worries of a recession have heightened in the last few weeks and with investor sentiment further deteriorating, we look at what next week has in store for the markets. On the monetary front, we note a relatively quiet period in regard to monetary policymakers. Nevertheless, we note the release of the BOJ’s summary of opinions from its board members from its April meeting and BoE’s interest rate decision, both on Thursday. As for financial releases, we make a start on a quiet Monday with Australia’s Building Approvals and Germany’s Industrial Output, both for the month of March. On Tuesday, during the Asian session, we note Australia’s Retail Trade rate for Q1 followed by China’s Trade data for April. On Wednesday, during the European session, we note Norway’s CPI rates for April and in the American session, we highlight the important US CPI rates for April. On Thursday, we make a start during the Asian session, with Japan’s Current Account balance for March, China’s PPI and CPI rates for April and in the European session we note the Czech Republic’s CPI rate for April and during the American session, we highlight the US Weekly Initial Jobless Claims figure and PPI rates for April. Lastly, on a loaded Friday, we begin during the European session with the UK’s Manufacturing Output for March and the UK’s Preliminary GDP rates for Q1, followed by Norway’s GDP rate for Q1 and during the American session, we note the release of the US Preliminary University of Michigan Consumer sentiment figure for May.

USD – Fed hikes by 25 basis points, but is that enough?

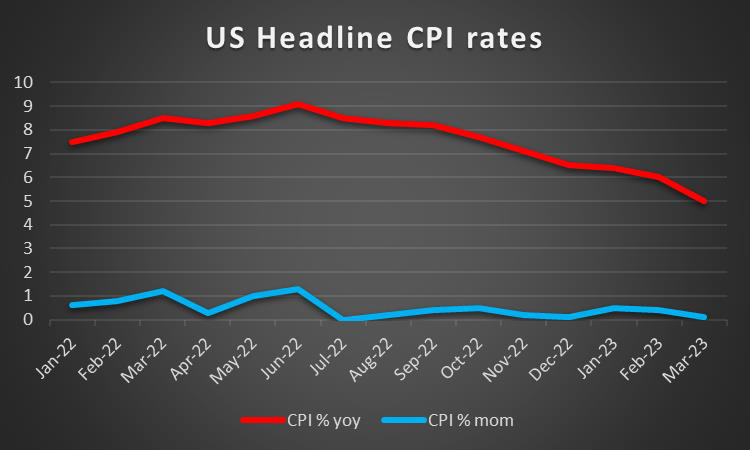

The USD is about to end the week in the reds against its counterparts. On a fundamental note, we note that the White House released a statement outlining the potential risks of a default. Following on last week’s report, the White House outlines in the event of a protracted default that “Unlike the Great Recession and the COVID recession, the government is unable to help consumers and businesses”. Further fueling fears of a US default could lead to the greenback further weakening against its peers as we near the ‘X-Date’. Furthermore, we highlight the fact that yet another U.S bank has collapsed this week, with First Republic being sold to JPMorgan, which has heightened fears of a potential banking crisis as Pacific West Bancorp and First Horizon throw punches as to who will collapse first. On a monetary note, we highlight the FOMC’s decision to hike interest rates by 25 basis points, with heavy emphasis being placed on Fed Chair Powell stating that the FOMC has removed the passage that states that the Fed “anticipates that some additional policy firming may be appropriate”. In addition to stating that the removal of the sentence has a “meaningful change” may be interpreted that the Fed may remain on hold during their next meeting. Bloomberg has claimed that Federal Reserve Governor Jefferson will be nominated to replace the Vice-chair slot previously held by Brainard, whilst Economist Adriana Kugler would be nominated to fill an open board slot. On a macroeconomic level, we note the release of the US Core PCE rates for March last Friday, implying that there is still high inflationary pressures persisting in the US economy which may lead to future rate hikes as the Core PCE rates remain stubbornly high. Lastly, dollar traders may be looking forward to next week’s US CPI print for April and the preliminary University of Michigan’s Consumer sentiment for May expected to come in lower, thus weakening the dollar. Also please note that as these lines are written the US employment report for April is still to be released and may materially alter the greenback’s direction.

GBP – BoE prepares for another rate hike

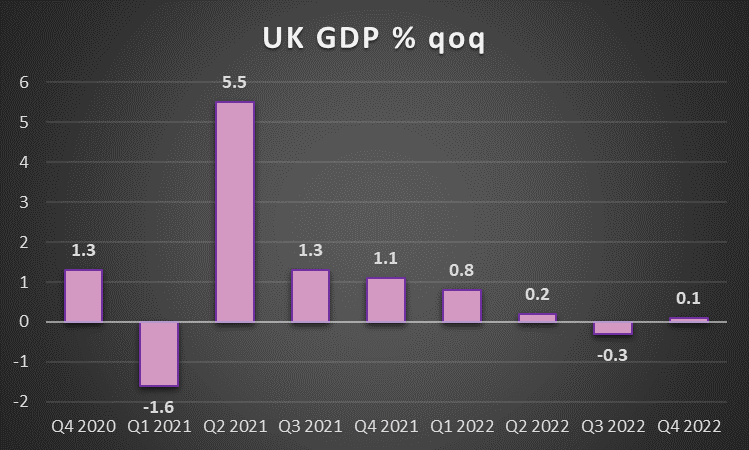

The pound is about to end the week stronger against the euro and the dollar, yet lower than last week’s close against the Yen. As the UK prepares for the coronation of King Charles the 3rd, on a fundamental note, we note Deutsche Bank’s decision to acquire UK broker Numis for $410m, signaling confidence in the London stock market, after regulators blocked Microsoft’s $69 billion deal to acquire Activision last week. On a monetary level, we highlight BoE Governor Bailey’s comments on Thursday, where he implied that as a result of high-interest rates, the probability of defaults has increased for the near future. This statement could be interpreted that the BoE decided to remain on hold during next Thursday’s meeting yet GBP OIS implies at the time, an 85% probability for the bank to proceed with another 25 basis points rate hike. Furthermore, Economist Megan Green who is set to join the MPC on the 5th of July stated on Thursday that the “banks need to look at medium-run inflation which could be a couple of years”, implying that inflationary pressures may continue for a prolonged period. It’s characteristic that the headline CPI rate for March despite slowing managed to remain in double digits, highlighting the cost of living crisis in the UK. This may place support for BoE’s aggressive rate hike policy, as traders turn their attention to next week’s Preliminary GDP rate for Q1, as an indication of the economic impact that the BoE’s monetary policy tightening may have had. Should the bank hike rates, by 25 basis points as expected and maintain a hawkish tone in its accompanying statement, foreshadowing more rate hikes to come, we may see the Sterling jumping. On a macroeconomic level, we note the release of the UK’s Final Services PMI for April which ticked upwards, indicative of greater than expected expansion of economic activity in the UK services sector, as the data indicates a more positive economic outlook than initially feared.

JPY – BoJ stresses that Asian Banks are sound and resilient

The JPY is about to end the week in the greens against the common currency, the pound and the greenback. Overall, the JPY may be experiencing temporary support against the greenback, as the banking crisis saga continues with Pacific West Bancorp being lined up on the firing line. BoJ Governor Ueda during a luncheon in South Korea stated to the press that Japanese Banks are likely to be immune to the financial turmoil in the US and Europe, as Asian banks have ample capital bases. This could be perceived as a slightly hawkish statement that the BoJ under Governor Ueda may play a more dominant role, that is independent of its traditional allies and as such may set the BoJ in a new direction in the future. On a macro level, we note the relatively quiet week enjoyed by JPY traders as there are a number of public holidays this week. Despite this, we note that the Manufacturing PMI figure for April came in as was expected and that the Household Confidence figure for April also ticked upwards. Given the lack of financial releases, traders may place heavier emphasis on next Tuesday’s household spending for March which are predicted to provide contradicting figures on a MoM and a YoY level. Concluding traders should be weary and pay attention to the banking situation in the US as the JPY may experience safe haven inflows due to increased market worries.

EUR – ECB Hikes by 25-basis points, hints that more hikes are on the table

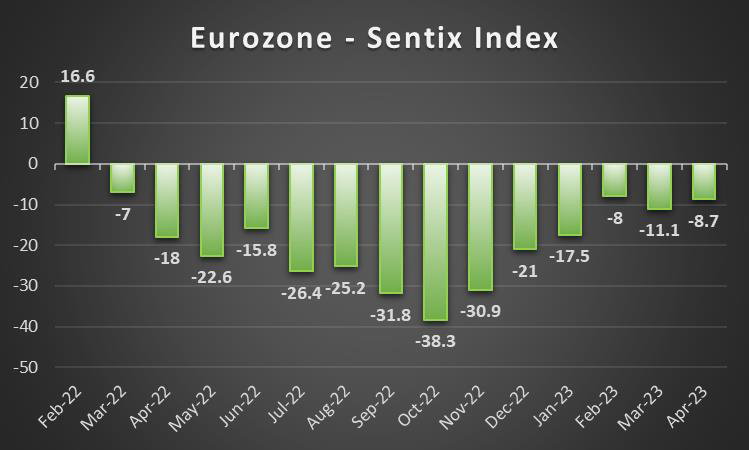

The common currency is on track to end the week weaker against the pound and the Yen, however it appears it will end the week stronger against the dollar. Fundamentally, we note the escalating violence between protestors and police officers in France, as the strikes continue in one of Europe’s largest economies, against the government’s decision to raise the retirement age. On a monetary front, we highlight the 25-basis point hike by the ECB on Thursday, followed by ECB President Lagarde’s press conference in which she stated that “underlying price pressures remain strong”, opening the possibility for further interest rate hikes. However, we note that despite the hawkish remarks, the EUR has weakened against its counterparts as traders may have expected a more hawkish approach. Also, President Lagarde indicated that there was discontent between policymakers, with some favoring a 50 basis point hike. Also, the following comment in ECB’s accompanying statement that “policy rates will be brought to levels sufficiently restrictive” seemed to underscore the bank’s hawkish intentions. On a macro-outlook, we note that Eurozone’s HICP rate for April ticked upwards on Tuesday, implying that inflationary pressures are still high in the Eurozone, strengthening the case for future rate hikes. Lastly, EUR traders may be shifting their attention to Germany’s Industrial output rates for March which are due on Monday, where a higher-than-expected rate could support the common currency, assuming that Europe’s largest economy projects strong economic resilience. Please note that the number of high-impact financial releases stemming from the Eurozone is to be reduced, which in turn may allow for fundamentals to take over.

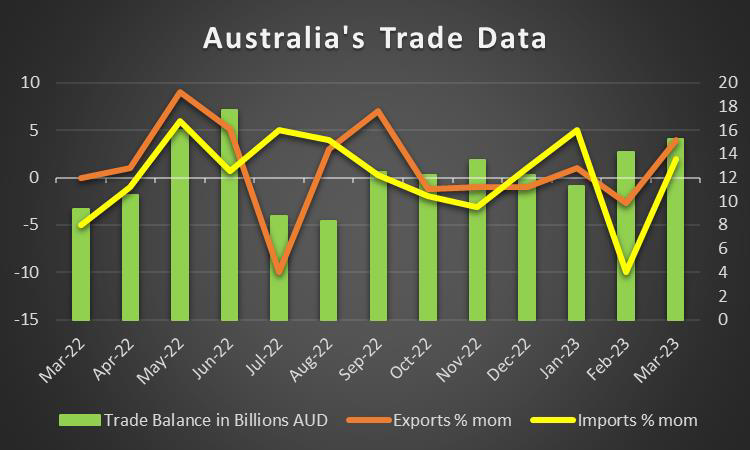

AUD – AUD suprises the markets by increasing interest rates by 25 basis points

The Aussie recouped the ground that was lost against the USD last week by ending this week in the greens. On a fundamental note, we give emphasis to key players in the Pacific theatre as the US-Sino relationship deteriorates, considering the recent report by FT that US-listed options that track Chinese stocks have more than halved since hitting a record last November. This may provide some indications that the deteriorating relations between the US and China are affecting investors, which may affect the AUD due to the heavy reliance of the Australian economy on the demand for its exports by China, contradicting its military alliance with the US. On a monetary level, we note the surprise 25 basis point interest rate hike by the RBA on Tuesday. As a result, the Aussie gained following Governor Lowe’s accompanying statement, which stated that “Inflation in Australia has passed its peak, but at 7 per cent is still too high”. In addition, RBA’s forward guidance stated that “some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe” which maintains an element of hawkishness in the bank’s intentions, thus further supporting the Aussie. On a macroeconomic level, we highlight the release of Australia’s Preliminary Retail sales for March on a mom basis ticking upwards on Wednesday, providing support for the Aussie. However, the NBS and Caixin PMI manufacturing figures for April declined below 50, thus indicative that Australia’s largest trading partner may not be experiencing the economic growth that was anticipated following China’s reopening. Furthermore, given Australia’s heavy dependence to export its goods to the Chinese economy, traders may be placing considerable emphasis on next Tuesday’s Chinese Imports rate for April as it could translate into decreased demand for Australian goods thus weakening AUD and vice versa.

CAD – BoC hints that the bank is willing to increase interest rates if inflation persists

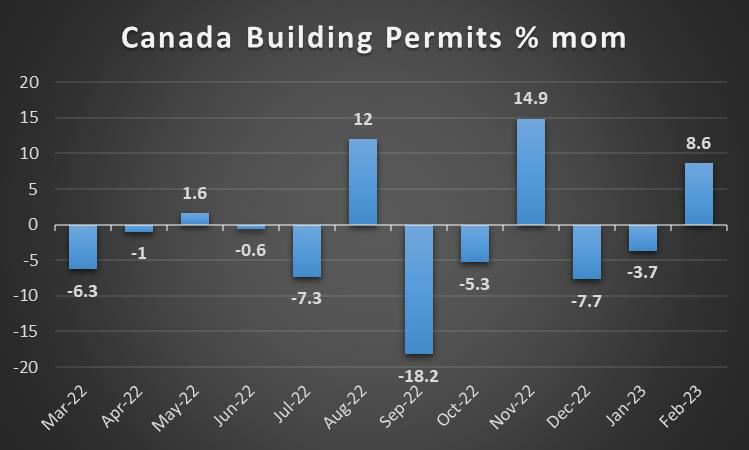

The Loonie strengthened against the dollar for the week. Fundamentally we note that Canada’s federal workers have struck a deal with the government on Monday, effectively ending the country’s largest ever public-sector strike. This may further inspire confidence in the Canadian economy, and as a result may be translated into support for the CAD. Also, we note the merger between one of Canada’s largest banks Toronto Dominion and US-based First Horizon has been called off, spiking renewed banking fears. Given Loonie’s second nature as a commodity currency, it remains highly sensitive to market sentiment as it is considered a riskier asset. On a monetary tone, BoC’s Macklem spoke on Thursday, implying the need for further data gathering in order to properly assess the inflationary pressures persisting in the economy, as the current financial environment is highly volatile. Furthermore, Governor Macklem indicated the bank is willing and able to increase interest rates if needed. On a macroeconomic level despite Canada’s trade data for March coming in higher than expected on Thursday, Loonie traders remained spooked from Canada’s GDP rate for February coming in lower last Friday. Therefore traders now await April’s employment data due to be released later on today, which are predicted to deteriorate slightly, thus further weakening the Loonie. Lastly, we note that WTI temporarily dropping below $65 per barrel this week, which weakened the CAD given its predominant export product being Oil thus, as the liquid gold’s price declines so may the CAD.

General Comment

As a closing comment, banking fears have made their way to the surface, with the US equities sector bleeding as market worries intensify. Hence, we continue to highlight that stock market traders will have to navigate between next week’s US CPI print, the Fed’s intentions, worries for the banking sector and earnings releases. We note some support for some companies that beat the market’s expectations, such as Pfizer and Starbucks. When it comes to next week’s earnings we note on Monday PayPal(#PYPL). On Tuesday we note Airbnb (#Airbnb. Lastly, on Wednesday we note Walt Disney (#DIS). Furthermore, we note that the deteriorating greenback has been reflected in the shiny metal’s price as gold printed new all-time highs on the heels of a banking crisis in the US. The drop of US yields may have also been reflected in gold’s price as the relative deterioration in US yields may be further support for the precious. Lastly, we note that the low number of high-impact financial releases next week in the FX market, may pave the way for fundamentals to dictate the direction of the market although the BoE’s interest rate decision and US CPI print could drive up traders’ interest on related pairs.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.