The greenback tended to edge lower against a number of its counterparts yesterday and during today’s Asian session, as overall the market seemed to be rather lazy with little volatility. We note that also that US stockmarkets failed to pick up on their rebound made in the past week and are about to end the second quarter in the reds reflecting the market’s cautiousness. Gold’s price edged lower yesterday rendering back any gains made at Monday’s opening and it seems that the ban on Russian gold imports did not impress traders nor did the prospect of a tight supply for the precious metal worry them. Today we highlight the release of the US consumer confidence for June and the indicator’s reading is expected to drop implying a greater degree of pessimism for the average US consumer, which could have a negative effect on the USD as it follows also a string of weak data from the US in the past week. On the monetary front we expect the usual hawkishness of the Fed to be expressed by New York Fed President Williams who will be speaking during tomorrow’s Asian session.

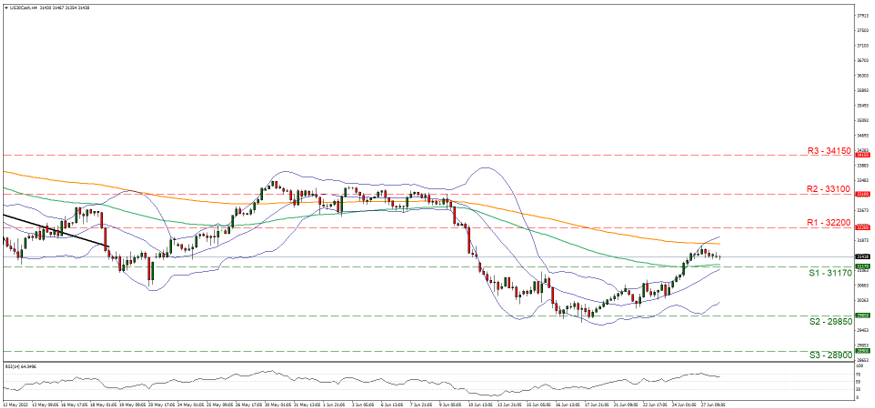

Dow Jones seems to have stabilised after breaking the 31170 (S1) resistance line, now turned to support. Given that the index’s price action seems to have calmed and the RSI indicator below our 4-hour chart is still high yet is sliding towards the reading of 50 implying that the bulls are losing steam we tend to maintain a bias for a sideways motion initially. Should the bears take over, we may see the index breaking the 31170 (S1) support line and aim for the 29850 (S2) support level. On the other hand should the bulls be in charge of the index’s direction once again, we may see the pair picking up and aiming if not breaching the 32200 (R1) resistance line, aiming for higher grounds.

Common currency gains ahead of Lagarde’s speech

The common currency was on the rise against the USD, but also the GBP and JPY in a sign of wider strength yesterday, yet we must note that it corrected lower during today’s Asian session. It should be noted that EUR traders may have started to price in the possibility of an acceleration of inflationary pressures in the Eurozone as the relevant preliminary releases for June are due out this week. Today in the European session we note the release of France’s consumer confidence for June which is expected to drop a bit and could cause the EUR to slip as it would imply less optimism among consumers of the second largest economy in the Zone. On the monetary front we highlight in the American session ECB President Lagarde which will making the introductory speech at ECB’s Forum on central banking in Frankfurt. At the same forum ECB Board member Schnabel will be speaking and we may see both policymakers reiterating the banks’ intentions for a 25 basis points rate hike in July and a contingent rate hike in September.

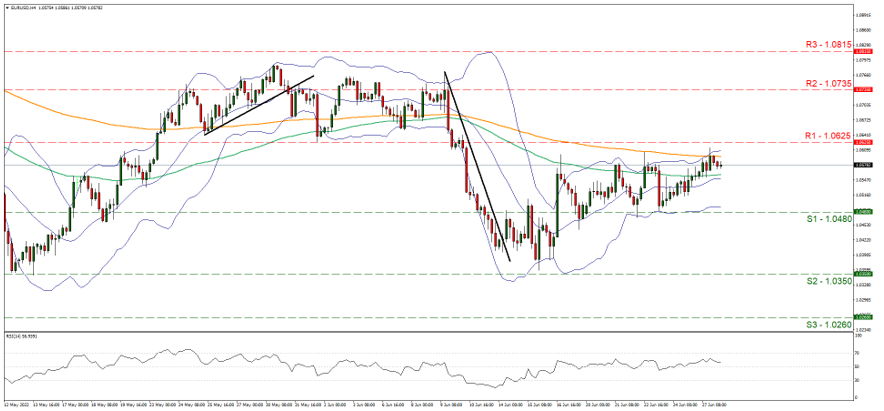

EUR/USD was on the rise yesterday aiming but not reaching for the 1.0625 (R1) resistance line before correcting a bit lower. Overall we tend to maintain our bias for a sideways motion of the pair and for us to switch in favour of a bullish outlook we would require EUR/USD’s price action to clearly break the 1.0625 (R1) resistance line and for the pair to form consecutive higher highs and higher lows. Should the pair actually find extensive fresh buying orders along its path, we may see the pair breaking the 1.0625 (R1) and actively aim if not breach the 1.0735 (R2) resistance level. Should a selling interest be expressed by the market we may see EUR/USD breaking the 1.0480 (S1) line and aim for the 1.0350 (S2) support level.

Other highlights for today

In addition we would like to note for oil traders the release of the weekly API crude oil inventories figure and another considerable rise of oil inventories may have an adverse effect on the rising oil prices, while during tomorrow’s Asian session we get Japan’s retail sales for May.

US 30 Cash H4 Chart

Support: 31170 (S1), 29850 (S2), 28900 (S3)

Resistance: 32200 (R1), 33100 (R2), 34150 (R3)

EUR/USD H4 Chart

Support: 1.0480 (S1), 1.0350 (S2), 1.0260 (S3)

Resistance: 1.0625 (R1), 1.0735 (R2), 1.0815 (R3)

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.