The USD tended to remain supported on Friday as the release of the Core PCE price index showed that inflationary pressures were still strong in the US economy for January. The relative rates accelerated both on a month-on-month as well as on a year-on-year level surpassing the market’s expectations, intensifying the expectations that the Fed is to maintain an aggressive, hawkish stance in order to curb inflationary pressures in the US economy. On the flip side, US stock markets dropped maintaining their bearish movement, as also did gold’s price pressured by the strengthening of the USD. At this point we would also like to note on a fundamental level, our worries for possible further escalation in the tensions in the US-Sino relationships given China’s involvement in the war in Ukraine, which could hurt riskier assets and the Aussie in particular. In the UK we highlight on a fundamental level the developments regarding Brexit and note that UK PM Rishi Sunak is to meet with EU chief Ursula Von der Leyen, to discuss a new Brexit deal which is to be followed by the relative statements and could shake the pound.

GBP/USD edged lower aiming for the 1.1925 (S1) support line. The RSI indicator is near the reading of 30 implying a bearish sentiment of the market for cable, yet for a bearish outlook we would require a clear breaking of the S1. Yet should the bears be actually in charge, we would expect GBP/USD not only to break the 1.1925 (S1) support line but also to aim if not reach the 1.1740 (S2) support level. Should the bulls take over we may see cable reversing course, breaking the 1.2115 (R1) resistance line, paving the way for the 1.2270 (R2) resistance level.

AUD/USD continued to drop breaking the 0.6720 (R1) support line, now turned to resistance. We tend to maintain a bearish outlook for the pair currently, given that the RSI indicator is below the reading of 30 and a downward trendline dictates the pair’s movement. Should the selling interest be maintained, we may see AUD/USD breaking the 0.6625 (S1) support line aiming for even lower grounds. Should the pair find fresh buying orders we may see AUD/USD reversing course, breaking the prementioned upward trendline, the 0.6720 (R1) resistance line and aim for the 0.6800 (R2) resistance level.

Other highlights for the day:

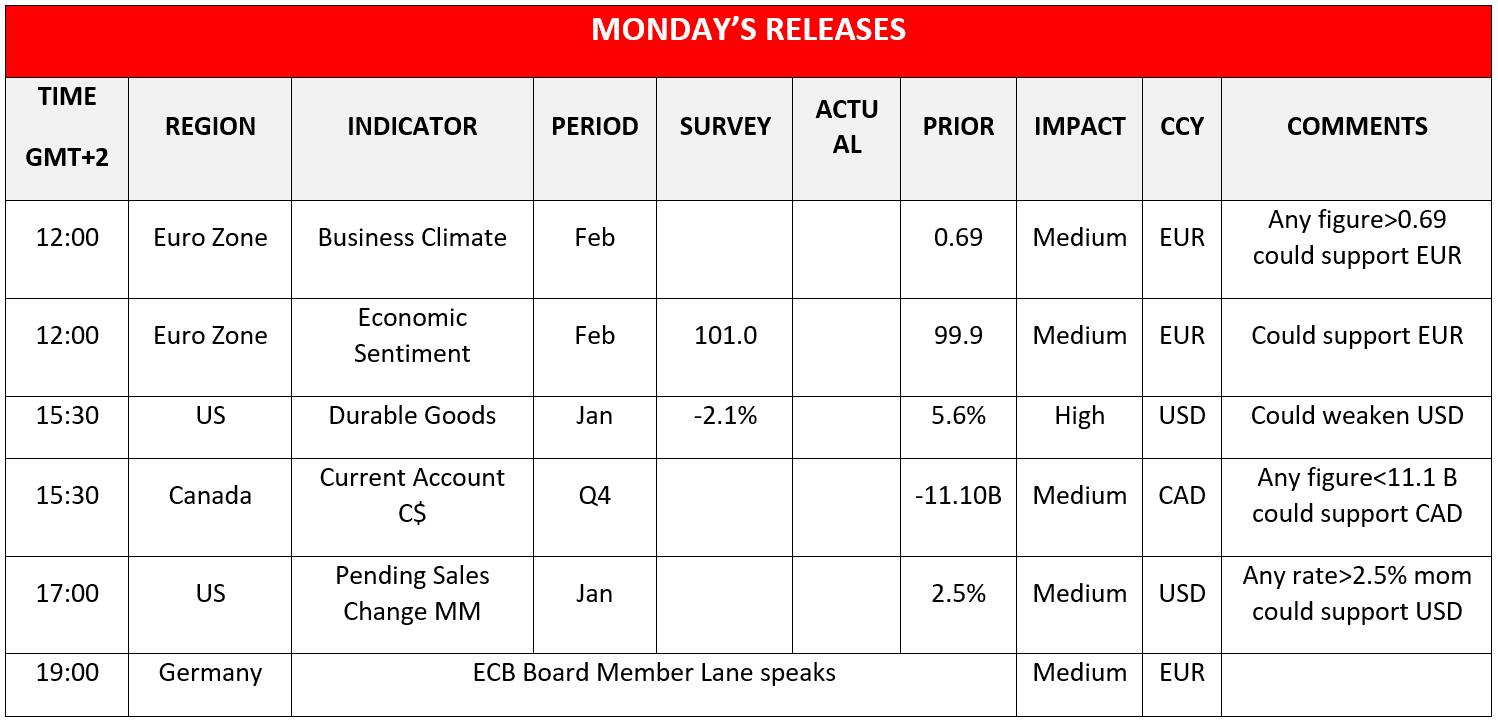

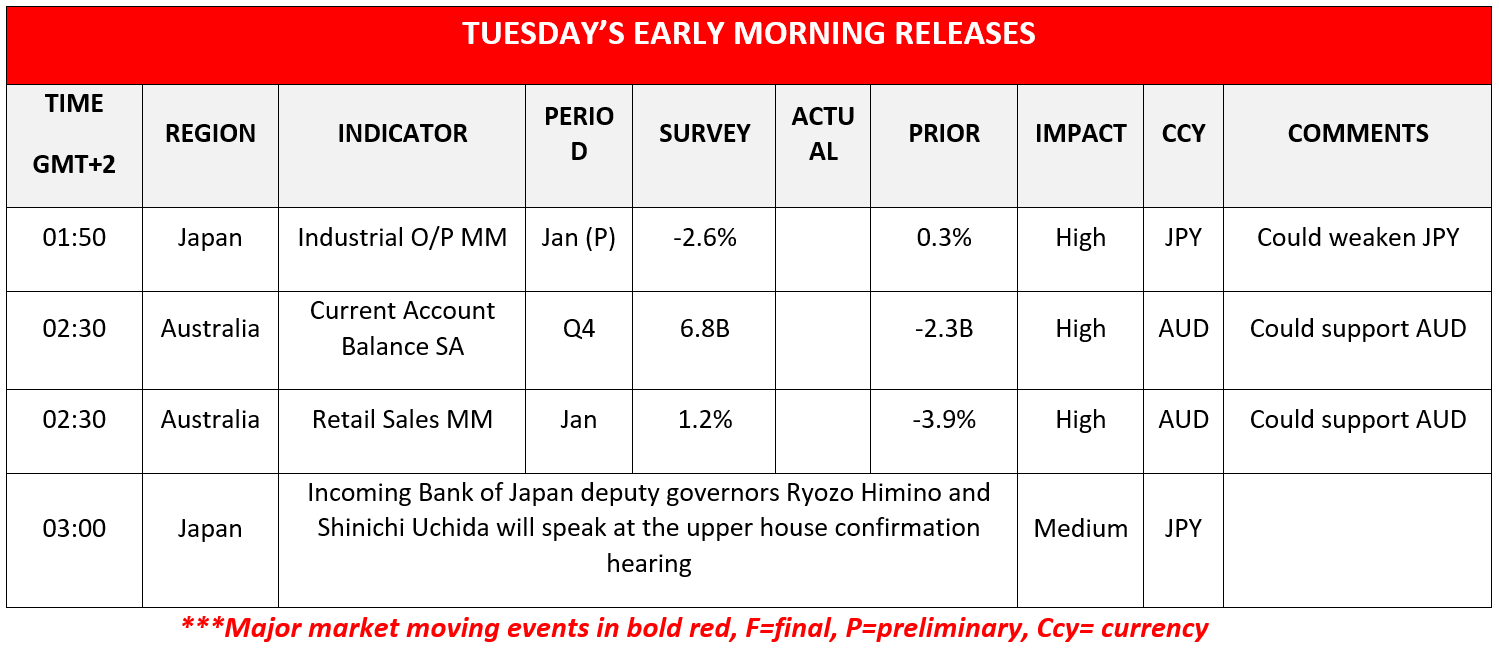

During today’s European session, we note the release of Eurozone’s business climate and economic sentiment indicators for February. In the American session, we get the US durable goods orders for January, the US pending home sales rate for January and Canada’s current account balance for Q4, while ECB board member Lane is to make statements. During Tuesday’s Asian session, we note the release of Japan’s preliminary industrial output growth rate for January and from Australia we get the current account balance for Q4 and retail sales for January.

As for the rest of the week

On Tuesday, we get France’s preliminary HICP rate for February, and from Canada, we get the GDP rates for Q4 and the US consumer confidence for February. On Wednesday we note the release of Australia’s GDP rates for Q4, China’s NBS and Caixin manufacturing PMI figure for February, while from Germany we get the preliminary HICP rate for February, from the US the ISM manufacturing PMI figure for February, UK’s Halifax House Prices for February, and Germany’s industrial orders for January. On Thursday we note the release of Australia’s building approvals growth rate for January, the Eurozone’s preliminary HICP rate for February and the weekly US initial jobless claims figure. On Friday, we note the release from Japan of February’s Tokyo CPI rates, from the Czech Republic the GDP rate for Q4, from the Eurozone the final Composite PMI figure for February and from the US the ISM non-manufacturing PMI figure for February.

GBP/USD H4 Chart

Support: 1.1925 (S1), 1.1740 (S2), 1.1565 (S3)

Resistance: 1.2115 (R1), 1.2270 (R2), 1.2465 (R3)

AUD/USD H4 Chart

Support: 0.6625 (S1), 0.6545 (S2), 0.6440 (S3)

Resistance: 0.6720 (R1), 0.6800 (R2), 0.6900 (R3)

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.