It’s Friday and as usual we are going to take a look at what next week has in store for the markets. On Monday we get China’s Caixin manufacturing PMI , Turkey’s CPI rate the Zone’s preliminary HICP rate and the US ISM Non-Manufacturing figure all for February. On Tuesday we get the RBA’s last meeting minutes. On Wednesday we get Australia’s GDP rate for Q4, Switzerland’s February CPI rate, the Czech Republic’s preliminary CPI rate for February the Eurozone’s final composite figure for February, the UK’s final figure for February and the US ADP National Employment figure February.On Thursday, we make a start with Australia’s building approvals rate for January, Sweden’s preliminary CPI rate for February, Turkey’s interest rate decision and the ECB’s interest rate decisions, followed by Lagarde’s presser, the US weekly initial jobless claims figure and Canada’s trade balance figure for January. On Friday we get China’s trade balance figure for February, Germany’s industrial orders rate for January, the UK’s halifax house prices rate, the Zone’s revised GDP rate for Q4, the US employment data for February and Canada’s employment data also for February

USD – US Employment data next week

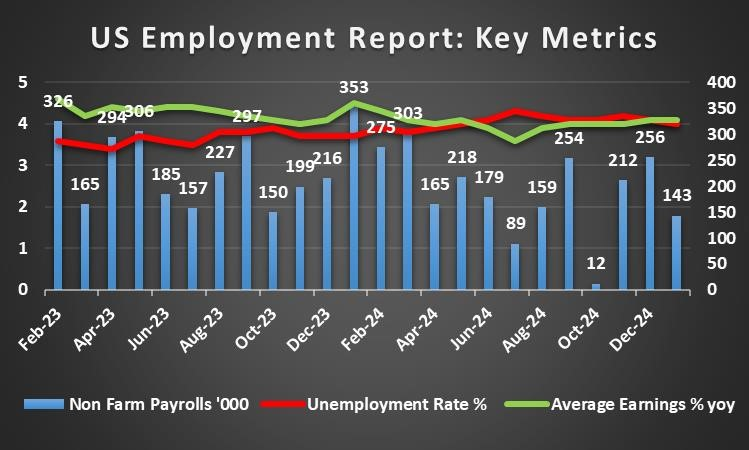

In terms of upcoming financial releases stemming from the US, next week is set to be interesting for dollar traders. In particular we are referring to the release of the US Employment data for February, which is set to garner significant attention up to and during it’s release. The current market expectations are for the NFP figure to showcase a loosening labour market by coming in at 133k which would be lower than last month’s figure of 143k. However the unemployment rate and average earnings rate are expected to remain steady at 4.0% and 4.1% respectively. Nonetheless, should the employment data come in as expected, it could imply a loosening labour market which in turn could increase pressure on the Fed to cut rates earlier than expected which could weigh on the dollar. On the flip side a deviation from the expected figures which could imply a resilient labour market could instead “validate” the restraint seen by the Fed and could thus aid the greenback.

On a political level, we note that President Trump has hinted that the 25% tariff on imports from Canada and Mexico may go ahead next week on the 4th of March. Moreover, the President also stated this Wednesday that he may impose a 25% import tariff on EU exports into the US. Generally speaking, the possibility of trade wars occurring between the US and the affected nations could cause concern about the resiliency of the global economy, in addition to the possible increase in inflation as a result. Hence, we remain vigilant to any developments which may occur next week in regards to the US’s tariff ambitions and the possible retaliatory measures from the EU, Mexico and Canada.

Analysts opinion (USD)

“The tariff ambitions by the US President appear to be sparking concern in the markets. The employment data next week is certainly an even worth monitoring for reasons we have stated in our above paragraph. We should note that at the time writing the US Core PCE rates have yet to be released and could thus change our narrative for next week.”

GBP – Fundamentals to continue leading the pound

On a macroeconomic level, we note that the UK faced a lacklustre week with no major financial releases stemming from the country. Looking at next week’s financial releases traders may be interested in the release of the UK’s Halifax house prices for February on a month-on-month basis. Should the financial release showcase a higher rate than 0.7%, it could potentially aid the British pound, as it may infer that inflationary pressures in the economy may have not dwindled and thus could provide at best some support for the pound.

On a monetary level ,we would like to note the comments made by BoE Ramsden who stated per Reuters that “British inflation is at least as likely to undershoot the Bank of England’s latest forecasts as it is to match them, potentially requiring faster rate cuts,” implying that the bank may embark on a more aggressive rate cutting path than what was previously anticipated. In turn his comments could be perceived as dovish in nature and could thus weigh on the pound. However, should other BoE policymakers emerge to challenge this “dovish” rhetoric it could potentially aid the pound

Analyst’s opinion (GBP)

“Given the absence of high impact financial releases from the UK and the relative stability of the UK Government, we would not be surprised to see the pound ceding control of it’s direction to other stronger currencies in the coming week.”

JPY – Uncertainty over inflation in the Japanese economy?

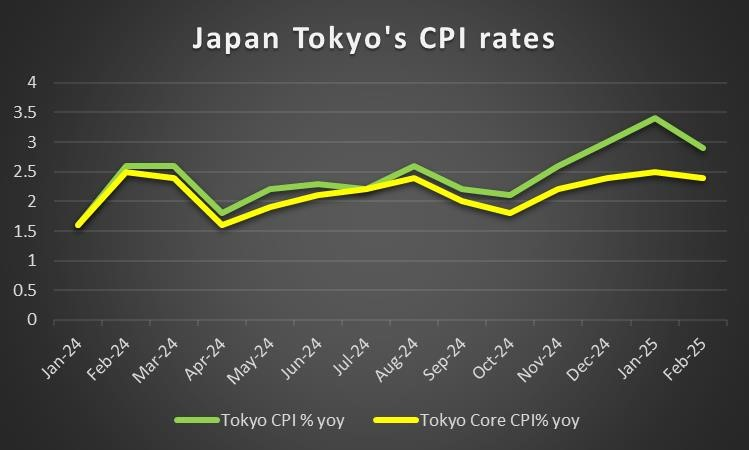

On macroeconomic level, the BOJ’s Core CPI rate on a year-on-year basis came in hotter than expected at 2.2% versus the expected rate of 2.0% and even higher than the prior rate of 1.9%. The hotter than expected inflation print tended to paint a picture that inflationary pressures in the Japanese economy tend to be accelerating. In turn, this may increase pressure on the BOJ to continue on its rate hiking policy in their next meeting, in an attempt to counter inflation. In turn this could aid the JPY and even more so should BOJ policymakers imply that further rate hikes are to come during the year. On the flip side should BOJ policymakers showcase some concern and opt for a much more gradual rate hiking path it could weigh on the JPY. However, the Tokyo CPI rates which were released earlier on today, showcased easing inflationary pressures with the Core PCE rate coming in at 2.2% versus 2.3% which is even lower than last month’s rate of 2.5%.

Analyst’s opinion (JPY)

“The contradiction between the CPI rates may be of some concern for the BOJ and could thus increase calls for more information to be gathered. Yet we remain steadfast in our opinion that the BOJ may continue raising rates during the year which could aid the JPY as the banks counterparts appearing to be remaining on hold or cutting rates”

EUR – German elections could shake the Euro

On a political level for Europe, we must of course mention the recent elections in Germany. In first place was the CDU/CSU union with 28.5% of the vote, followed by the AfD’s historic victory with 20.8% and in third place was the SPD with 16.4%. The elections seems to have shaken Germany’s political core. Next up is the ratification of the vote on the 14th of March, yet given the result the CDU/CSU will require a coalition in order to Govern Germany. This possibility was concerning, as some worried about a coalition government with the AfD which is considered to be far- right. Yet, that has been ruled out by the CDU which has vowed to maintain the “firewall” and thus the easiest way to reach the minimum 316 seats would be to bring back the grand-coalition with the SPD. Such a possibility could support the EUR, yet a failure to form a coalition which could force another election could weigh on the common currency

On a monetary level we note the ECB’s interest rate decision which is due to be released next Thursday. The current market expectations for the decision are for the bank to cut rates by 25 basis points, with EUR OIS currently implying a 98.21% probability for such a scenario to materialize. In such an event, the decision to cut rates could weigh on the EUR. However, should the ECB decide to remain on hold it could boost the EUR as it could be perceived as hawkish in nature. Yet with a 98.21% probability, for the ECB to cut rates by 25 basis points, we turn our attention to the banks accompanying statement and ECB President Lagarde’s presser following the decision. Should the accompanying statement be perceived as hawkish or dovish in nature it could aid or weigh on the EUR respectively, with the same possibilities being true for ECB Lagarde’s press conference.

Analyst’s opinion (EUR)

“Germany’s elections have concluded without a hitch. However, we would like to see the composition of the Government and the possible coalition between the SPD and the CDU/CSU aka the Grand Coalition, yet should the CDU/CSU break the so called ‘firewall’ the implications on the EUR could be significant. On another note, we would like to see how Europe will respond to Trump’s claims that he may impose a tariff on the EU. Lastly, we wouldn’t be surprised to see the ECB proceeding with a 25bp cut, as we have constantly stressed that the EU’s economy and in particular Germany requires a boost. Yet a tariff on the EU could upend the ECB’s meticulous planning”

AUD – RBA minutes due out next week

On a monetary level, in the land of down under, the RBA’s last meeting minutes are set to be released next week. As a reminder the bank cut rates by 25 basis points in their last meeting, with the bank highlighting the uncertain outlook in its accompanying statement. Moreover, RBA Governor Bullock had stated that the bank cannot declare victory on inflation. In turn we wouldn’t be surprised to see the RBA’s last meeting minutes showcase a willingness to garner further information before continuing on their rate cutting path which in turn could be perceived as hawkish in nature.

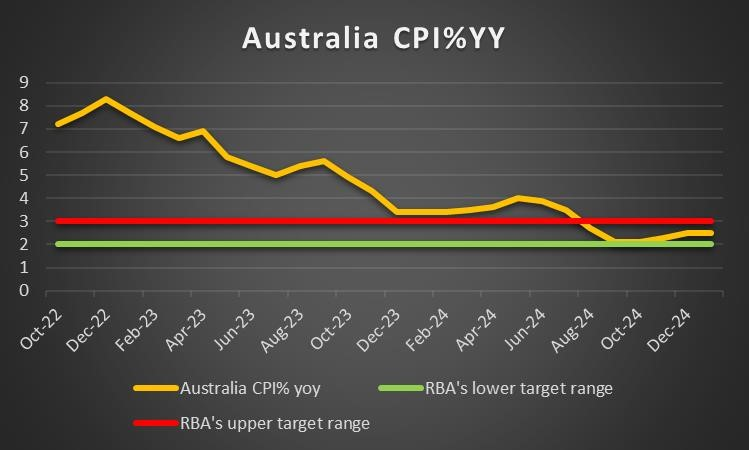

However, on a macroeconomic level we should note the release of Australia’s CPI rate for January tends to cast some doubt on the concerns of RBA policymakers in regards to the inflation narrative. Specifically, Australia’s CPI rate on a yoy basis for January came in lower than expected at 2.5% versus the expected rate of 2.6% yet remained the same as the prior reading of 2.5%. The lower than expected rate may ease worries about an acceleration of inflationary pressures in the economy, yet it’s failure to ease and remain steady at 2.5% could also imply that the bank still has some work to do. Lastly ,traders may be interested in the release of Australia’s building approvals rate for January next Thursday.

Analyst’s opinion (AUD)

“Although the CPI rates failed to showcase the expected acceleration of inflationary pressures in the Australian economy, the CPI rate remaining steady at 2.5% is still a concern. Thus, we wouldn’t be surprised to see RBA policymakers maintain their presumed hawkish tone of refraining from declaring victory against inflation. In turn this could aid the AUD. Yet should financial releases cast doubt on that scenario, it could instead weigh on the AUD”

CAD – Employment data next week

On a political level, we must note that US President Trump has nodded that the 25% tariff on Canadian exports to the US which was postponed, appears to be “on track” with that potentially occuring on the 4th of March which would be Monday. In turn the possibility of tariffs and a retaliation by Canada, could raise concerns about the true economic strength of the economy. Hence should the tariffs go through, it could impact the CAD.

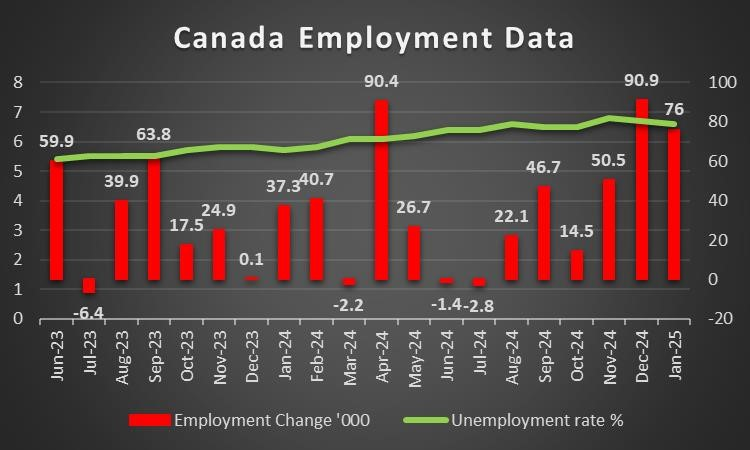

On a macroeconomic level, for next week we would like to focus on the release of Canada’s employment data for February which is due out on Friday. According to economists the unemployment rate is expected to remain steady at 6.6% and thus attention may turn to the employment change figure. Should the figure come in higher than the prior figure of 76k it may imply a tight labour market and could thus aid the CAD. Whereas a lower figure than 76k could imply a loosening labour market and could instead weight on the Canadian dollar.

Analyst’s opinion (CAD)

“We remain interested in the CAD and in particular the tariff narrative. Specifically, the potential measures Canada may take to retaliate if Trump’s 25% tariff proceeds as planned by next week. Furthermore of interest will be the employment data on Friday although with the US NFP figure also due out at the same time, Canada’s financial releases could be overshadowed”

General Comment

As a closing comment, we expect the influence of the USD in the FX market to increase next week given the importance of the US Employment data. Moreover, we remain vigilant to developments in regards to the possible tariffs which could be imposed by the US on Mexico and Canada. In the US Equities markets we are concerned, with the S&P500 continuing on its downwards trajectory for a second week in a row. As for gold’s price, the upward motion seems to have stopped, with gold’s price sharply declining for the week .as the precious metal’s price is constantly reaching new record highs and is about to end the week in the greens for an eighth consecutive time, driven mostly by safe haven inflows.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.