As the US employment report for July and Canada’s employment data are still to be released, we take a look into what next week has in store for the markets. On the monetary front, despite policymakers from central banks around the world are taking a break, there are still some which are scheduled to make statements and could sway the market’s opinion. As for financial releases the calendar tends to ease and we have an early start on Sunday with the release of China’s trade data for July. On Monday we get Japan’s current account balance for June as well as Eurozone’s Sentix index for August. On Tuesday we have a rather slow day while on Wednesday we get China’s PPI and CPI rates for July and we highlight the release of US CPI rates for the same month. On Thursday we note the release of the weekly US initial jobless claims figure, as well as the US PPI rates for July and on Friday we get from the UK the GDP rates for June and Q2, Eurozone’s industrial output for June as well as the preliminary University of Michigan consumer sentiment for August.

USD– CPI rates the next big test for the USD

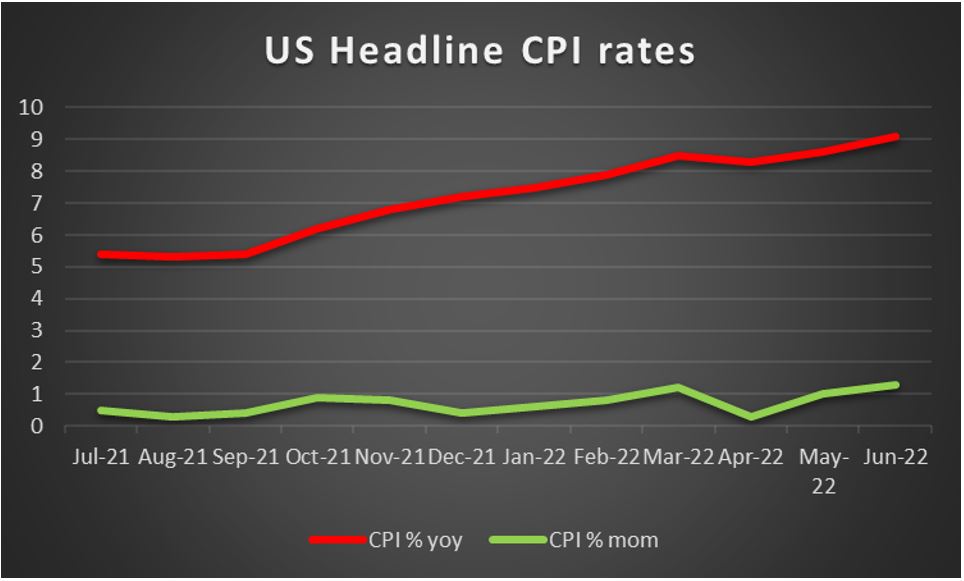

The USD is about to end the week near the same levels it begun on Monday yet the US employment report for July which is still to be released could alter the greenback’s direction. On the monetary front, we note that Fed policymakers seem to maintain a rather hawkish tone. Its characteristic that Minneapolis Fed President Kashkari, a well-known dove, specifically stated “The more likely scenario is we would continue raising (interest rates) and then we would sit there until we have a lot of confidence that inflation is well on its way back down to 2%.“ It is understandable that when even a dovish policy maker makes such comments, that the Fed’s intentions are clearly leaning on the hawkish side, which could provide some support for the greenback as monetary policy differentials could favour it. On a more fundamental level, we highlight US House Speaker Nancy Pelosi’s trip to Taiwan, the first of a high ranking US official in 25 years on the island, which intensified the frictions in the US-Sino relationships, creating market turbulence and safe haven inflows for the greenback on Tuesday. The Chinese responded angrily, yet in a restraint manner which tended to ease the market’s worries somewhat. On the other hand, we may see China maintaining the issue which could re-enhance market worries, hurt riskier assets and favor safe havens. In the coming week, we highlight the release of the US CPI Rates for July on Wednesday, and the headline rates are expected to slowdown and if actually so could imply that inflationary pressures in the US economy have peaked, something that could ease the pressure on the Fed to continue to hike rates at a fast pace. Also from the US we note the release of the weekly initial jobless claims figure on Thursday and the PPI rate for July on the same day, while on Friday we get the preliminary University of Michigan consumer sentiment for August.

GBP – GDP rates eyed

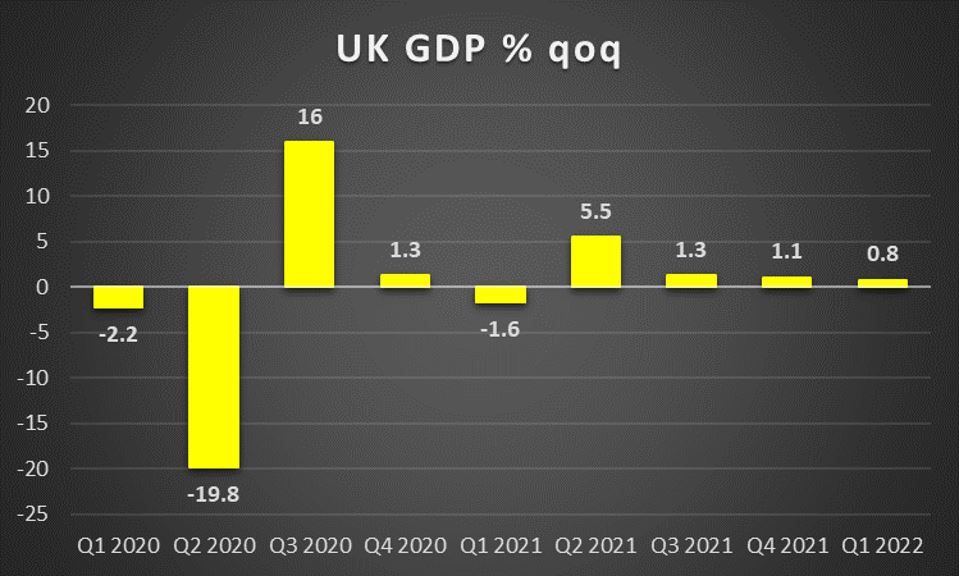

The pound is about to end the week slightly lower against the USD and JPY and notably lower against the EUR. BoE’s interest rate decision may have weakened the pound. The aftershocks of BoE’s interest rate decision yesterday, weighed on the sterling, closing the day in the reds, as the 50-basis points hike was largely anticipated and already widely priced in. On the other hand though, the bank struck a tone of uncertainty as it stated that the next rate hikes are to be data dependant and characteristically the bank stated that “Policy is not on a pre-set path”. Moreover, the failure of BoE’s members to deliver a unanimous vote came to a surprise at the time of the release, raising credibility concerns, alongside BoE’s grim warning of a long recession ahead for Britain. The pessimistic outlook seemed to weigh on the pound and that’s why we highlight the release of the UK GDP rates for June and Q2 on Friday. Should the GDP rates actually start to slow down or even drop into the negatives, that would practically reaffirm BoE’s negative outlook for the UK economy and could weigh considerably on the pound. On the other hand, the bank’s warning seems to also help the market anticipate and price in such negative data. Please note that on Friday besides the GDP rates for June and Q2, we also note the release of the Industrial output for June, the Manufacturing output for June and the trade balance for the same month.

JPY – Roller coaster movement for JPY

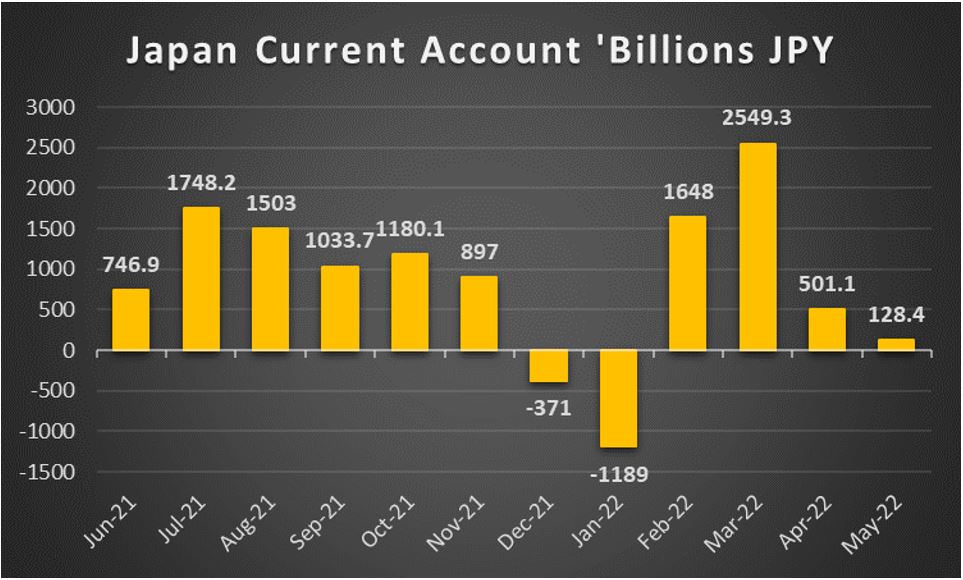

JPY seems about to end the week at the same levels it begun against the USD, as well as against the GBP and EUR. Yet the description fails to describe the rollercoaster ride of the past few days for JPY traders. Overall, we continue to highlight how BoJ’s dovish monetary policy continues to affect the JPY and is of key importance for its direction. We note that officials of the Ministry of Finance (MoF) in Japan seem to be foreshadowing that the bank may have to abandon its 0% cap on long-term interest rates. It’s characteristic that Reuters reported that MoF official Saito stated, “we must bear in mind the BOJ’s current policy won’t last forever. Sometime in the future, it won’t buy as much bonds as it does now, and will no longer peg interest rates at a set level,”. Such a scenario could provide some support for JPY, yet seems to be still in the distant future for the time being. On a more fundamental level, we tend to note JPY’s dual nature as a national currency and a safe haven. Should there be tensions in the international political scene, we may see JPY gaining as investors may navigate to its relative safety. As for financial releases we would like to note the release of Japan’s Current Account balance for June as well as well as the Corporate Goods prices for July.

EUR – Steady she goes

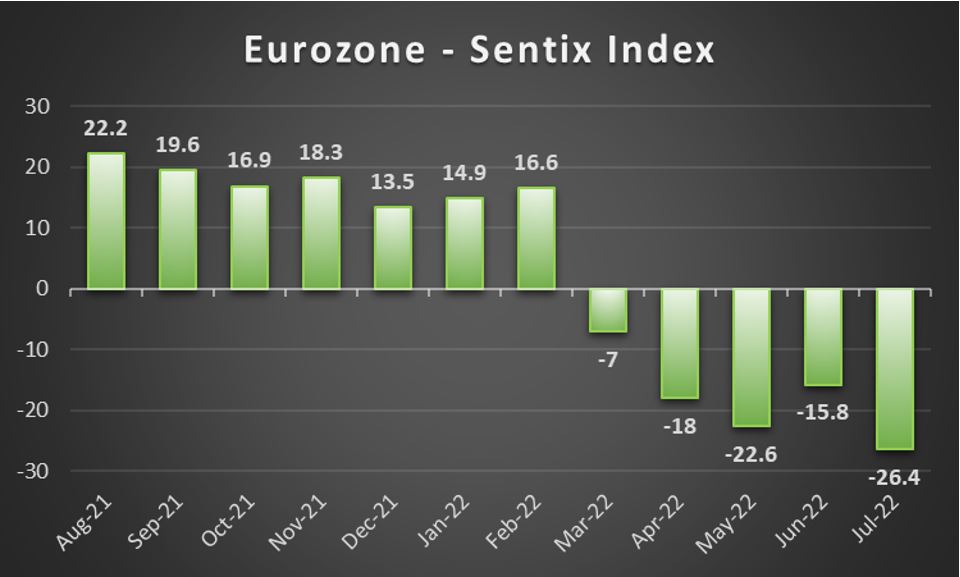

The common currency seemed to remain relatively stable against the USD and JPY yet gains slightly against the GBP. On a fundamental level the worries for Eurozone’s economy due to the war in Ukraine and the tensions in its relationship with Russia are still intense. The possible insufficiency of natural gas supplies from Russia still looms over Europe like a spectre. On the monetary front, ECB’s pivot in its latest meeting towards tightening its monetary policy is still present and the pressure seems to be rising to deliver another 50 basis points rate hike in the September meeting. The issue of fragmentation of borrowing costs for member states of the Eurozone is still an issue especially for countries like Italy, yet as Bloomberg reports, the bank seems to have deployed billions of Euros in bond purchases to shield Italy, displaying its determination not to allow the spread of borrowing costs between member states to widen out of control. The flexible reinvestment of the Pandemic Emergency Purchases Program (PEPP) seems to be the first line of defence for the bank currently and not the Transmission Protection Instrument (TPI) which tends to imply that the bank’s policy also carries a substantial degree of depth with it. As for financial releases we would like to note that the contraction of economic activity across sectors and member states, as signalled by the preliminary Composite PMI figure of the Eurozone for July, was reaffirmed which was a negative on a macroeconomic level. Yet Germany’s trade surplus surprisingly widened creating some hopes, as the economic powerhouse of the area regained its ability to export products. The coming week is about to be a rather slow week regarding financial releases, yet we would still like to note the release of Eurozone’s forward looking Sentix index for August on Monday, the final HICP rates of July for Germany and France on Wednesday and Friday respectively, while on Friday we also get Eurozone’s industrial output growth rate for June.

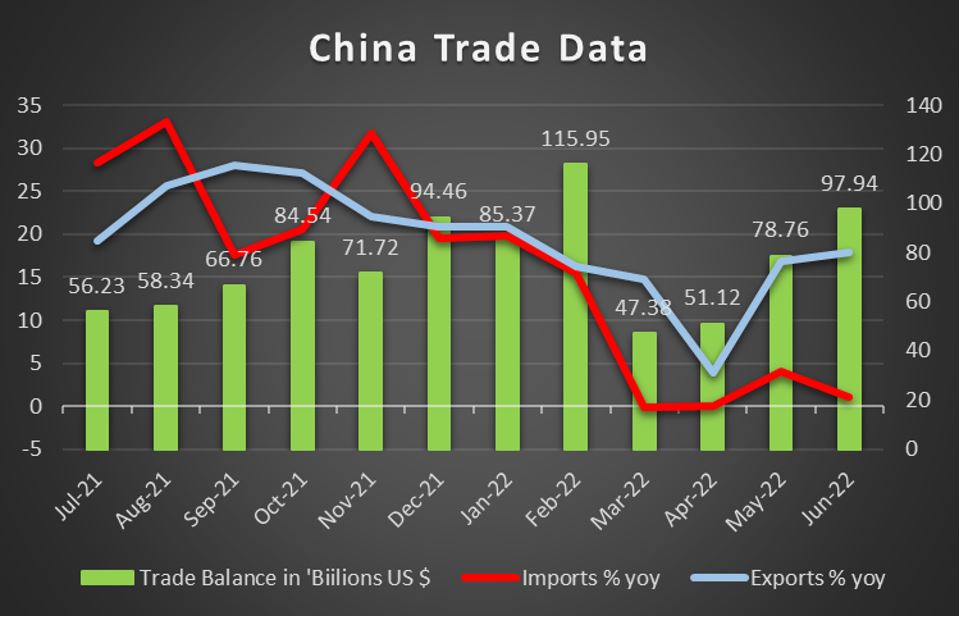

AUD – China’s trade data and optimism to move AUD

AUD seems about to end the week near the same levels the week begun on Monday against the USD, despite some increased volatility being present. Especially RBA’s interest rate decision on Tuesday tended to weaken the Aussie. It should be noted that the Aussie tended to weaken against the USD despite RBA delivering a double rate hike, as was widely expected. In Governor Lowe’s accompanying statement, it was reaffirmed that “The Board expects to take further steps in the process of normalising monetary conditions over the months ahead, but it is not on a pre-set path. The size and timing of future interest rate increases will be guided by the incoming data and the Board’s assessment of the outlook for inflation and the labour market”. The fact that the bank stated that there is a degree of uncertainty in its future rate hikes, given that it is not “set on a pre-set path” allowed for the Aussie to drop and could weigh as the bank relented a part of its decisiveness. In the coming week, given the low number of high impact financial releases from Australia, we expect fundamentals and market sentiment to be the primary factors behind the Aussie’s direction. Should the market sentiment be positive and more risk oriented, we may see AUD getting some support as a commodity currency. On the other hand should the tensions in the US-Sino relationships escalate further, we may see the Aussie weakening, given the close ties of the Australian and the Chinese economies as well as the wide amount of raw materials exported from the land of the down under to the Red Dragon. Hence we highlight the release of China’s trade data for July on Sunday, especially the import growth rate. We would also like to note the release of China’s inflation metrics for July on Wednesday while from Australia we note the release of the consumer sentiment for August and business confidence and business conditions for July, all coming out on Tuesday.

CAD- Oil prices to be watched out for

The CAD remained rather steady against the USD in the past few days, maybe with some slight losses and the drop of WTI prices may have adversely affected the Loonie. It should be noted that the positive correlation between oil prices and the CAD was on display once again maybe though not to the extent we expected. Oil prices slid lower in the past few days, despite OPEC announcing meagre increases in production levels for the commodity, which underscored the limitations in the capacity of major oil producing countries. On the other hand, we must note that US oil reserves tended to balloon further as both the API and EIA weekly oil inventories figures showed. The issue seems to be intensifying as problems are reported in shipping the commodity out of the US and we may see oil reserves in the US rising further in the coming days, especially for Cushing. Should that be the case we may see oil prices slipping further which may intensify the bearish tendencies for the CAD. On the monetary front we expect BoC’s monetary policy tightening intentionsto be maintained and thus, could provide some support for the Loonie. On a more fundamental level we expect, given also the lack of high impact financial releases, the market sentiment to be the main driver for the CAD. Should the market sentiment be more risk on and positive, we may see the commodity currency getting some support and vice versa. Also please note that Canada’s employment data for July are still to be released later today and could alter the CAD’s direction before the week ends.

General Comment

As a closing comment we expect the greenback to maintain its initiative over other currencies in the FX market given the number of high impact financial releases stemming from the US, with the highlight being the CPI rates for July on Wednesday. On the other hand, other currencies could also come under the spotlight once again in certain moments during the week. Overall, we would like to note that we are entering the holiday period hence we may see lower volatility being present for the markets, while in regards to US stockmarkets, we expect the earnings season to continue to keep traders busy, yet the number of high profile companies releasing earnings reports seems to be narrowing, which could reduce the interest of traders especially in the periphery rather than the core of the markets. Last but not least we must note that gold’s price was on the rise, for a third consecutive week, as the precious metal capitalised from the, up until now, relative inactivity of the greenback. We expect the negative correlation with the USD to be maintained in the coming week and could define gold’s direction.

Avertissement :

Ces informations ne doivent pas être considérées comme un conseil ou une recommandation d'investissement, mais uniquement comme une communication marketing. IronFX n'est pas responsable des données ou informations fournies par des tiers référencés, ou en lien hypertexte, dans cette communication.