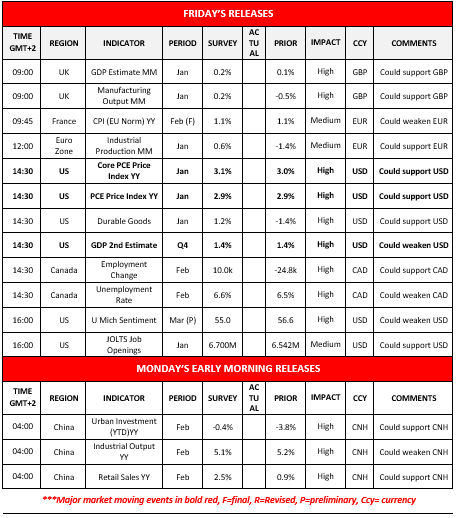

US January PCE and revised Q4 25 GDP rates in focus

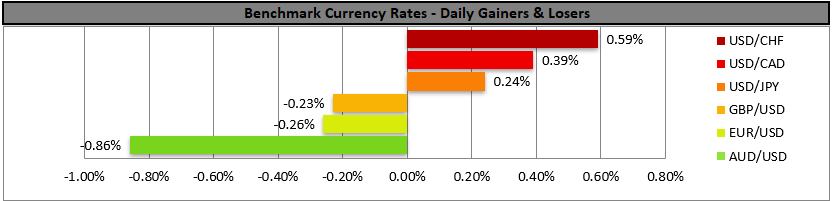

The USD continued to strengthen against its counterparts in the FX Market yesterday supported by save haven inflows as the war in Iran continues to tantalise the markets. We view the market’s worries for the US-Iranian war as the main issue the market is focusing upon, yet we also note the release of the US January PCE and the US Q4 25 GDP rates as possible points of interest for market participants and a possible acceleration of the rates could imply a resilience of inflationary pressures in the US economy and a faster growth of the US economy in the last quarter of the past year, with both accelerations possibly supporting the USD.

Canada’s February employment data could shake the Loonie

Also we note the release of Canada’s February employment data as a possible market mover for the Loonie. Forecasts are mixed, with the employment change figure expected to rise and the unemployment rate expected to tick up. The release gains on importance as the BoC releases its interest rate decision next week and a tightening of the Canadian employment market could provide support for the Loonie and vice versa.

Escalation of US-Iranian war pushes oil prices higher

The US-Iranian war seems to have no end in sight as on the one hand, Iran’s new Supreme Leader vowed to keep the Straits of Hormuz and market worries for the supply side of the international oil market intensified, pushing oil prices higher. It should be noted that US efforts to tame the rise of oil prices, like the waiver issued the exports of Russian oil, seem to fail to calm the markets at the current stage. Should we see the dead end being prolonged, we may see oil prices continuing to rise.

Risk off sentiment weighs on US equities

The uncertainty about the war in Iran and its possible consequences intensified in the markets, thus the risk-off market sentiment was enhanced and tended to weigh on US equities. Should we see market worries intensifying further, we may see US stock markets edging even lower.

Autres points forts pour aujourd'hui

Today we get the UK GDP rates, the preliminary US UoM consumer sentiment for March and the US JOLTS job openings figure for January. In Monday’s Asian session, we get China’s Industrial Output for February.

Charts to keep an eye out

USD/CAD

USD/CAD was on the rise yesterday after bouncing on the 1.3550 (S1) support line at the start of the week. We currently maintain a bias for a sideways motion of the pair as long as its price action remains within the boundaries set by the 1.3550 (S1) support line and the 1.3720 (R1) resistance barrier, the levels the pair largely respected since the start of February. Should the bulls take over we may see USD/CAD breaking the 1.3720 (R1) resistance line and start aiming for the 1.3880 (R2) level. Should the bears be in the driver’s seat, we may see USD/CAD relenting the gains of the past two days, breaking the 1.3550 (S1) support line clearly and continuing to start aiming for the 1.3420 (S2) support level.

WTI

WTI’s price soared yesterday in the widest rally since Monday, and managed to break consecutively the 90.85 (S2) and the 93.90 (S1) resistance lines, both now turned to support and continued even higher to test the 97.35 (R1) resistance line. We intend to maintain our bullish outlook for WTI’s price as long as the upward trendline guiding it remains intact, yet at the same time we issue a warning for a possible correction lower as we consider WTI’s price as being at overbought levels. Should the bulls remain in charge of the WTI’s direction, we may see its price action breaking he 97.35 (R1) resistance line and start aiming for the 100.90 (R2) resistance level. For a bearish outlook, which we currently see as remote, we would require WTI’s price to drop below the 87.10 (S3) line. Calendar follows

USD/CAD Daily Chart

- Support:1.3550 (S1), 1.3420 (S2), 1.3285 (S3)

- Resistance: 1.3720 (R1), 1.3880 (R2), 1.4020 (R3)

WTI Daily Chart

- Support: 93.90 (S1), 90.85 (S2), 87.10 (S3)

- Resistance: 97.35 (R1), 100.90 (R2), 107.00 (R3)