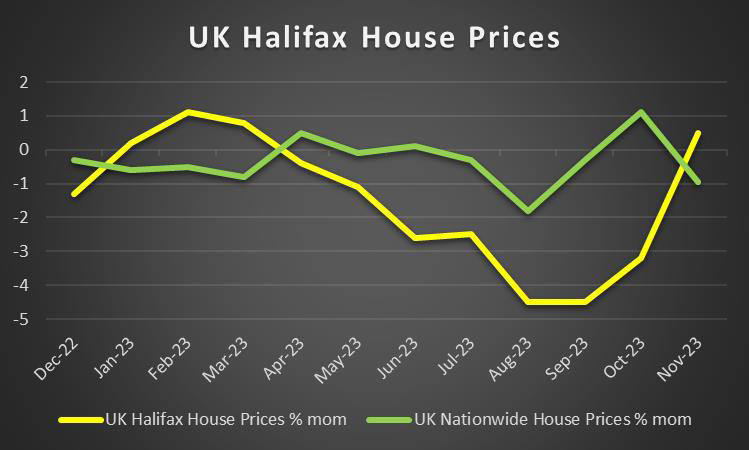

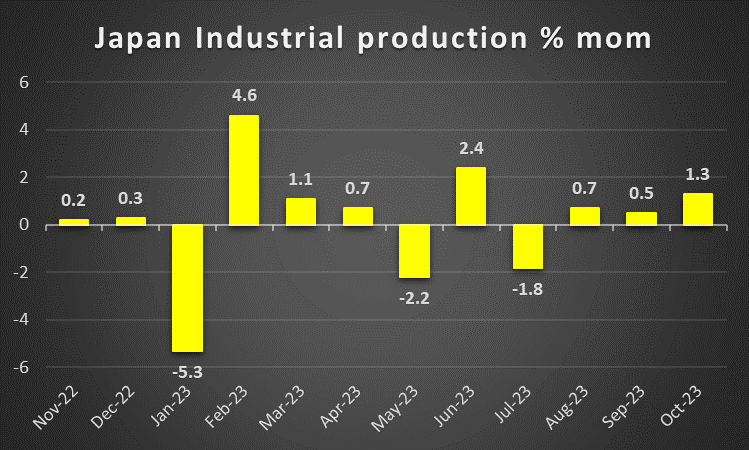

As the week draws into a close markets are slowly entering a sleep mode for the holiday season. We note the low number of financial releases in the week between Christmas and New Year. We note the possibility of thin trading conditions being present in the markets and could also extend beyond the first days of 2024. Yet the first week of January is expected to be quite interesting with a number of high-impact financial releases from various countries. Making a start with next week, we note the release of Japan’s industrial output for November and the US weekly initial jobless claims figure on Thursday and the UK’s Nationwide house prices on Friday. In the first week of 2024, we make a start on Tuesday with China’s Caixin manufacturing PMI figure for December, and Canada’s Manufacturing PMI figure for December. On Wednesday we note the release of Turkey’s CPI rate for December and the US ISM Manufacturing PMI figure for December and on Thursday we get Frances’ and Germany’s preliminary HICP rates for December and from the US the ADP national employment figure for December and the weekly initial jobless claims figure. On Friday, we get Sweden’s GDP rate for November, UK’s Halifax House prices for December, the US and Canada’s employment data for the same month, the US factory orders for November and the ISM non-manufacturing PMI figure for December. On the monetary front we highlight from Australia, RBA’s interest rate decision on the 2nd of January.

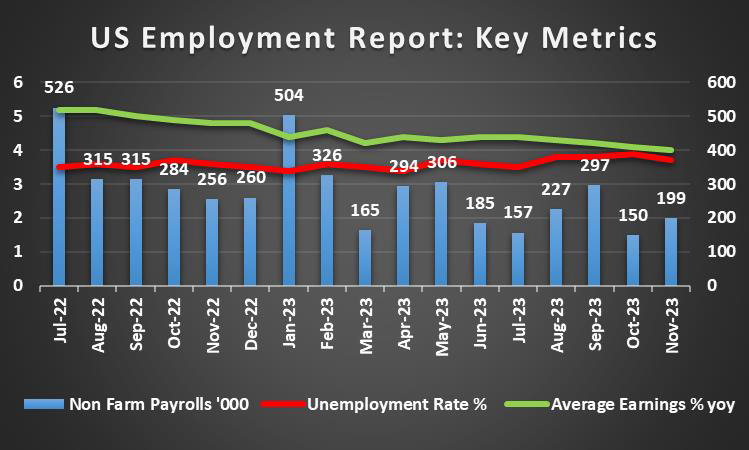

USD – US Employment data with the beginning of the new year

The USD seems about to end the week in the reds against its counterparts. On a monetary level, we note that Fed officials attempted to ease the market’s expectations for six rate cuts next year, since last Friday, yet with limited effect in changing the market’s perspective on monetary policy. Hence the market’s dovish expectations may have been among the main USD movers over the past week. On a macroeconomic level, we note the release of the Core PCE rates later on today, which are expected by economists to indicate, easing inflationary pressures in the US economy and may intensify the market’s expectations for the Fed. In such a scenario, we may see the dollar weakening and vice versa. Next week, we note a relatively quiet week in terms of financial releases, due to the Christmas holiday season. However, with the new year, we note the US Employment data, which is anticipated by economists to come in lower than the last readings, which could weigh on the dollar. On the other hand, should December’s Employment report imply that the labour market remains tight, we may see the dollar gaining.

GBP – BoE dilemma

The pound is about to end the week lower against the EUR, yet stronger against JPY and USD. On a monetary level, we note that BoE officials continue to appear hawkish. It should be noted that comments of BoE policymakers tended to contradict market sentiment as the market expects the bank to delay any rate cuts until May and then proceed with six rate cuts in total. Such market expectations seem to be exaggerated in our view at the current stage. Yet the pound’s downward trajectory could be attributed also to this week’s financial releases. In particular, the CPI rates for the UK came in lower than expected at 3.9% yoy, versus the expected 4.3% yoy. As such, with inflationary pressures in the UK economy appearing to be easing, the pressure on the BoE to maintain the interest rates at their current levels, could be weakened, thus potentially leading to downward pressure on the pound. On a macro level, we note the contraction of the US GDP rate for Q3, which intensifies our worries for the outlook of the UK economy. For next week, we also note that UK markets will be closed for the Christmas Holiday and we may see fundamentals leading the pound given the absence of high-impact financial releases stemming from the UK in the first week of January.

JPY – BoJ remains on hold

JPY is about to end the week in the reds against the EUR and the pound, yet remains relatively unchanged against the weakening USD in a sign of broader weakness. Following last week’s report by Bloomberg, which claimed that BOJ officials see little need to drastically abandon their negative interest rate in the December BOJ meeting, it appeared to have been spot on. The BoJ despite remaining on hold by keeping rates at -0.10% as was widely expected, appeared to contradict the market’s expectations for some hawkish hints, by unanimously voting to stand pat. In

particular, Governor Ueda implied that the ultra-loose monetary policy settings are to remain in place, keeping its forward guidance practically intact. In addition, the bank’s accompanying statement, tended to highlight the ultra-loose monetary policies, supportive role to the Japanese economy and implied that it still is not convinced that the CPI rate will exceed its 2% yoy target in a stable manner, which appeared dovish. It should be noted that the slowdown of November’s CPI rates tended to corroborate BoJ’s narrative. We see the case for JPY to continue weakening on a monetary policy level, given that the interest rate differential outlook with other central banks may continue to play an adverse role for the Yen.

EUR – ECB remains hawkish

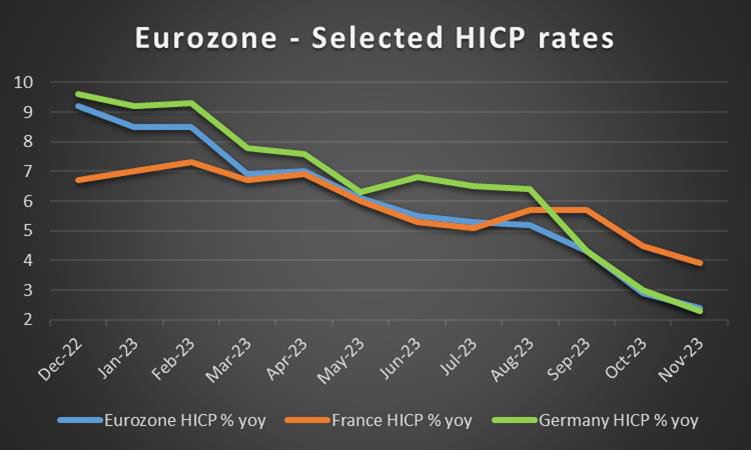

The common currency is about to end the week in the greens against the USD and GBP and the Yen in a sign of general strength. On a monetary level, we note that the hawkish sentiment, since last week appears to have been re-iterated by ECB Vice President De Guindo’s on Thursday having stated that it’s still too early for to cut rates. As such, should the hawkish sentiment be repeated by other bank officials, we may see the EUR gaining. Although, in our opinion, we may see the ECB maintaining a more hawkish approach compared to its counterparts, given the complexity of the Euro area and its member states, who may be experiencing divergences in inflationary pressures in their domestic economies. However, on a macro level, the slowdown of HICP rates for November in the Euro Area was verified, with HICP on a yoy level slowing from 2.9% to 2.4% implying easing inflationary pressures, fuelling the market’s expectations for early and extensive rate cuts by the ECB. Therefore, should the preliminary HICP rates for December, due out in the first week of January continue to indicate easing inflationary pressures they could weigh on the EUR while should inflationary pressures prove to be persistent we may see the EUR gaining, as it could allow the ECB to maintain rates higher for longer.

AUD – RBA interest rate decision due out at the beginning of the new year

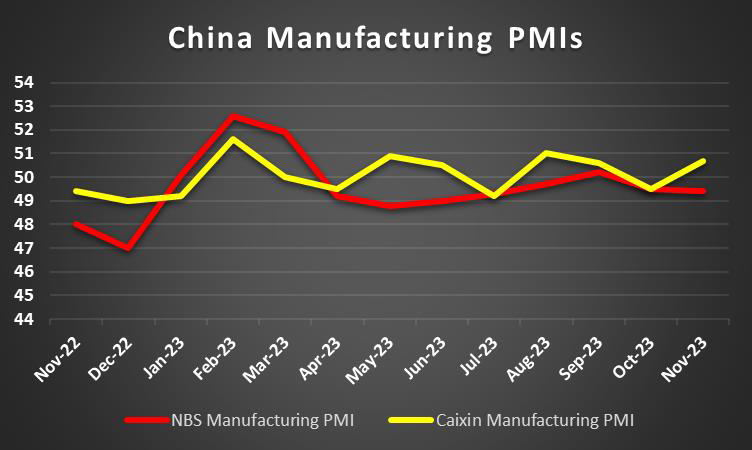

AUD is about to end the week in the greens against the USD for a second week in a row. On a monetary front, we note that RBA’s interest rate decision, with market participants widely anticipating the bank to remain on hold, as AUD OIS currently implying a 97% probability for such a scenario to materialize. In the bank’s December meeting minutes which were released on Tuesday, it was revealed that the bank had debated the scenario of remaining on hold, or potentially hiking. As such with the possibility of a hike still on the table, we may have seen the Aussie gaining, during the week, which we anticipate may continue up until the bank’s interest rate decision, as no noticeable financial releases are due out for Australia before the end of the year. On a fundamental level, we note that China’s NBS and Caixin Manufacturing PMI figures for December are due out. We maintain our concerns about China’s economic resiliency and as such, should they come in lower than expected, implying possibly another contraction of economic activity we may see the Aussie weakening and vice versa.

CAD – BoC hints at potential rate hikes in the future

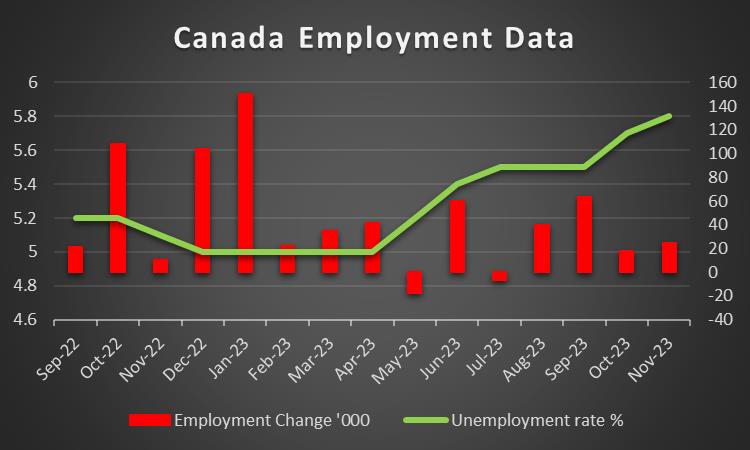

The Loonie is about to continue its winning streak against the USD for a second week in a row. On a monetary level, BoC Governor Macklem last Friday, stated that “we are certainly feeling more confident that monetary policy is working” when referring to combating inflation, yet he also pointed out that the bank is not there yet. Moreover, the BoC’s December deliberation minutes, stated that “the expected decline in inflation could stall… or new developments could lead to renewed inflationary pressures”. These two scenarios posed by the bank, in addition to BoC Governor Macklem’s comments, could be perceived as hawkish and as such could support the Loonie. On a fundamental level, we note that oil prices over the week are on track to end higher for the week. Should oil prices continue to rise, we may see higher oil prices supporting the Looney. On a macroeconomic level, Canada’s CPI rates for November came in higher than expected, implying persistent inflationary pressures and as such, supported the Loonie. Moreover, Canada’s GDP rates are due to be released later on today and could shake the CAD.

General Comment

Overall we expect market activity in the coming week to be muted, as we enter the Christmas Holiday season, with minimal financial releases expected. However, the risks for elevated volatility remain, as a few market participants could impact the market, given the lack of activity during the Christmas period. Moreover, we expect volatility to pick up with the new year, with a high number of high-impact financial releases in the first week of January and we highlight particularly the US Employment Report for December. In regards to

US stock markets, we saw the bulls maintain their lead, with all three major indexes reaching new all-time highs. Yet we do highlight that despite the new all-time highs, all three major indexes are about to end the week relatively unchanged maybe with some slight gains since Monday, implying a continuance of the positive market sentiment. We also note that the US bonds in particular the 5-Year and 10-Year moved lower once again. Lastly, we note that Reuters is reporting that Angola is preparing to leave OPEC, a move which could upset the oil cartel’s power dynamics heading into next year and as such, could lead to higher volatility in the oil markets.

Si vous avez des questions d'ordre général ou des commentaires concernant cet article, veuillez envoyer un email directement à notre équipe de recherche à l'adresse research_team@ironfx.com

Avertissement :

Ces informations ne doivent pas être considérées comme un conseil ou une recommandation d'investissement, mais uniquement comme une communication marketing. IronFX n'est pas responsable des données ou informations fournies par des tiers référencés, ou en lien hypertexte, dans cette communication.