As the week is about to come to an end, we open a window at what next week has instore for the markets. On Monday, we get the preliminary PMI figures for December of Australia, Japan, France, Germany, the Euro Zone as a whole, the UK and the US. Also on Monday we get Japan’s machinery orders for October, China’s urban investment, industrial output and retail sales all for November, UK’s Rightmove house prices for December and Canada’s House Starts for November. On Tuesday we get UK’s employment data for October, Germany’s Ifo and ZEW indicators for December, the US retail sales, Canada’s inflation data and the US industrial output all for November. On Wednesday we get Japan’s trade data and chain store sales, UK’s CPI and Eurozone’s HICP rates, all being for November, New Zealand’s GDP rate for Q3 and the highlight of the week, the Fed’s interest rate decision. On Thursday on the monetary front we get the interest rate decisions of BoJ, Riksbank, Norgesbank, CNB and BoE, which come from Japan, Sweden, Norway the Czech Republic and UK respectively. As for financial releases, we get the Germany’s forward looking GFK consumer sentiment for January, France’s overall business climate for December, UK’s CBI distributive trades for December, the final US GDP rate for Q3, the US weekly initial jobless claims figure and the US Philly Fed Business index for December, while from New Zealand we get November’s trade data. Finally on Friday, China’s PBOC is to release its interest rate decision and we note the release of Japan’s November CPI rates, UK’s retail sales for November, the US PCE rates also for November, Canada’s retail sales for October, the Eurozone’s preliminary consumer confidence for December and the final US University of Michigan consumer sentiment for December.

Fed’s interest rate decision in focus

The USD is about to end the week in the greens against its counterparts, recovering losses of the past two weeks.

On a fundamental level, we note for the USD the market worries for the possibility of Trump imposing tariffs on US imports once inaugurated. Should such worries amplify, we may see the USD gaining further.

On a monetary policy level, we highlight the release of the Fed’s interest rate decision, next Wednesday. The bank is expected to cut rates by 25 basis points and pause rate cuts in its next meeting. Hence we place substantial attention on the bank’s forward guidance which is to be included in the accompanying statement and Fed Chairman Powell’s press conference later on. Also the bank’s macroeconomic projections and new dot plot are to affect the market’s reaction. Should we see the bank show even more hesitation for more rate cuts, thus signaling a further slowdown of its rate cutting path we may see the USD getting some support.

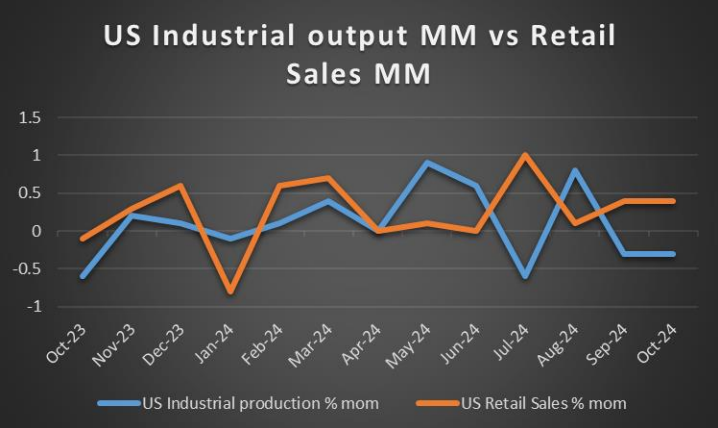

On a macroeconomic level, we get from the US, November’s retail sales and industrial output growth rates for November which are to provide more clues about economic activity in both the demand and supply sectors of the US economy. Yet the next big test for the USD after the release of the Fed’s interest rate decision and the final GDP rate for Q3, is expected to be the release of the PCE rates for November on Friday. Should the rates accelerate showing a persistence of inflationary pressures in the US economy, we may see the USD getting additional support.

Analyst’s Opinion

Overall we see all three main categories of fundamentals supporting the greenback at the current stage. Trump’s tariff threats, the market expectations for the Fed to slow its rate cutting path and the resilience of the US economy along with the persistence of inflationary pressures in the USD economy, all align towards pushing the USD higher.

GBP – BoE to delay any rate cuts

The pound lost ground against the USD this week, while gained against the JPY and seems to remain relatively unchanged against the EUR, in a sign that it allowed other currencies to have the initiative.

On a fundamental level we note the trade relationships of the UK with the US and the EU as key. The UK seems to be able to avoid Trump-tariffs for its exports in the US, or get to suffer a possibly lower tariff rate than the EU. On the other hand, the uncertainty generated by Trump getting into office, tends to push the EU with the UK closer together on a trading level. Both the possible avoidance of US tariffs on UK products and an improvement of the EU-UK trade relationship, tend to be supportive for the pound on a fundamental level.

On a monetary level, we highlight BoE’s interest rate decision next Thursday. The bank is expected to remain on hold and resume rate cuts in its February meeting. Should the bank’s forward guidance set the market’s expectations in doubt by being more hawkish in its forward guidance, we may see the pound getting some support and vice versa.

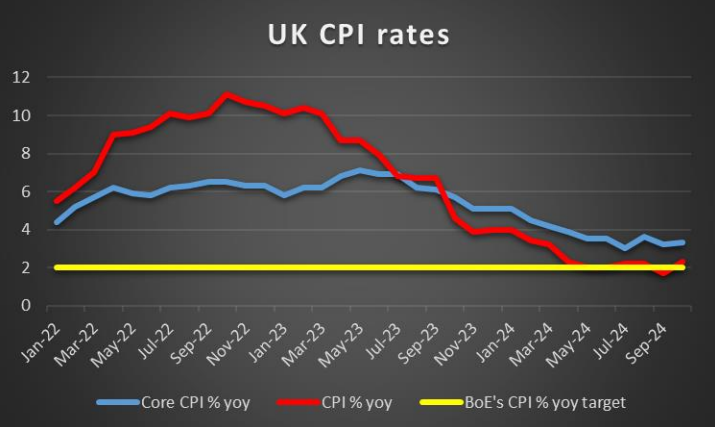

On a macroeconomic level, we would like to note the release of UK’s employment data on Tuesday and a possible tighter employment market than expected could provide support for the pound, yet the highlight is expected to be the release of the November CPI rates for Wednesday. Should the headline rate continue to accelerate on a year on year level, we may see the pound being supported. The last financial data which could stir the pound would be November’s retail sales on Friday and a possibly acceleration of the rate showing growth for the retail sector once again could support the sterling.

Analyst’s Opinion

Despite the support for the pound on a monetary level, we still have some doubts for politics and macroeconomic data, especially the latter. Yet for the time being the absence of adverse fundamentals tends to allow the pound to float.

JPY – BoJ to remain on hold?

JPY seems about to end the week in the reds against the USD,EUR and GBP in a sign of a wider weakness.

For JPY traders we highlight next week on a monetary level the release of BoJ’s interest rate decision next Thursday. JPY OIS currently imply a probability of 76.6% for the bank to remain on hold and proceed with a 25 basis points rate hike in its January meeting. Local media highlighted yesterday that BoJ officials are leaning towards keeping rates unchanged next week. Nevertheless we still see the risks related to the decision as tilted to the upside and a possible surprise rate hike could provide asymmetric support for the Yen. Yet should the bank remain on hold as expected, it would be kicking the can down the road, with the chances of a rate hike occurring in its next meeting being increased. Hence in such a scenario we would place considerable weight on the bank’s forward guidance. Should the bank signal the possibility of a rate hike in the January meeting, we may see JPY getting some moderated support, while an absence of such signals in the bank’s accompanying statement could weigh on JPY considerably.

On a fundamental level, we note the intentions of the Japanese Government to raise key taxes in 2026 to fund defence budget expansions. Also the safe haven qualities of the JPY should not be underestimated.

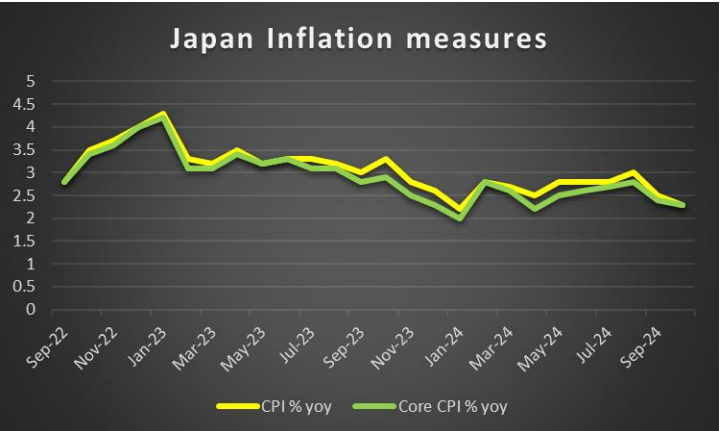

On a macro level, we note the preliminary December PMI figures on Monday and November’s trade data on Wednesday, while the highlight is expected to be November’s CPI rates on Friday and a possible acceleration of the CPI rates may support JPY as it could enhance the market’s hawkish expectations and vice versa.

Analyst’s opinion

Unless we see a surprise deriving from BoJ’s interest rate decision, we may see the Yen continuing to be in the retreat, maybe in a more moderated manner.

EUR – Focus turns towards December preliminary PMI figures

For the week the common currency seems to be losing ground against the greenback, is gaining against the Yen and remains relatively stable against the sterling.

On a monetary level, we highlight ECB’s to cut rates by 25 basis points and signal its readiness for more easing to come. The decision tended to be more or less expected, given that economic activity in the Euro Zone is faltering.

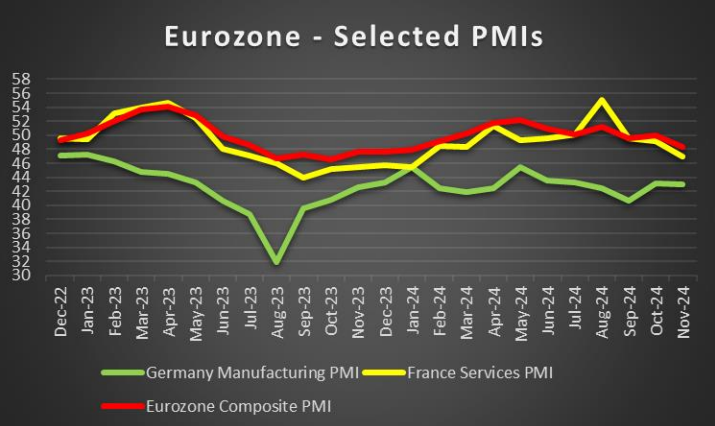

Hence on a macroeconomic level, we highlight the release of December’s preliminary PMI figures on Monday. Should the indicators show further contraction of economic activity in the Euro Zone, we may see the release weighing on the common currency. We focus our attention on Germany’s manufacturing sector and on second note France’s services sector, while Euro Zone’s composite PMI figure is to provide a rounder view.

Euro Zone’s fundamentals may be weighing on the single currency as ECB President Lagarde highlighted the risks deriving from political uncertainty and the possibility of Trump imposing tariffs on European products. On a fundamental level, overall political uncertainty is still present as premature elections were called for in February and in France, French President Macron hasn’t appointed a new Prime Minister as these lines are written. The sentiment seems to be pessimistic about the outlook of the Zone and especially in germany. Factories and business are closing and a recession may be on the horizon. Hence Germany’s IfO and ZEW indicators for December on Tuesday and Wednesday may prove to be important and if they fail market expectations may weigh on the EUR.

Analyst’s opinion

Overall we see fundamentals weighing on the common currency as he ECB is prepared to cut rates further, there is political uncertainty in France and Germany and macroeconomic indicators are not so favorable. In Macroeconomics we recognise that inflation is on the retreat despite some acceleration ahead of the Christmas festivities, yet our worries tend to focus around economic activity and growth which seems to be faltering.

AUD – RBA remained on hold with a dovish twist

The Aussie seems to be losing ground against the USD.

On a monetary level we note that RBA released its interest rate decision last Tuesday, remaining on hold as was widely expected. The bank in its altered its wording to include “Recent data on inflation and economic conditions are still consistent with these forecasts, and the board is gaining some confidence that inflation is moving sustainably towards target.” The change highlights a turn in the bank’s expectations towards the dovish side which ultimately may be opening a door to incoming rate cuts.

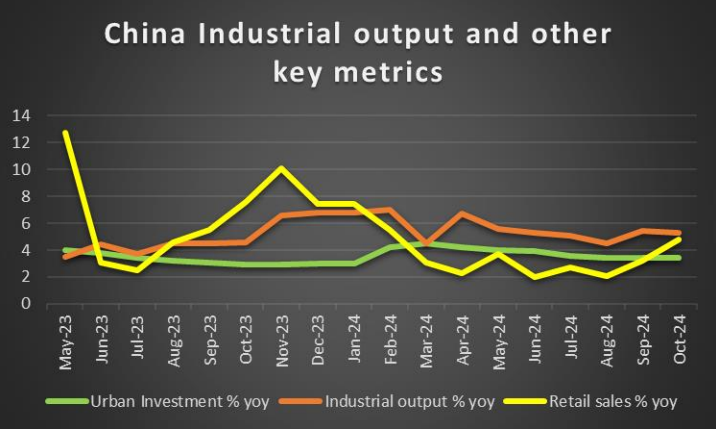

Please note that economic activity is easing in Australia while uncertainty rises with Trump entering the White house and threatening to impose tariffs on China, Australia’s biggest trading partner. On a fundamental level, our focus remain on China given the lack of evidence of a confident recovery for the Chinese economy. Yet PBoC is from now on expected to maintain an “appropriately loose” monetary policy and the Chinese government a more proactive fiscal policy. Hence we highlight on Monday from China, the release of November’s Urban Investments, industrial output and retail sales and on Friday PBOC’s interest rate decision.

On a macroeconomic level, the Aussie got some support on Thursday from the hotter than expected November employment data. In the coming week, the calendar for Aussie traders is relatively empty maybe with the exception of the December preliminary PMI figures on Monday, hence we expect fundamentals to lead the Aussie.

Analyst’s opinion

Focus of Aussie traders is expected to be on China in the coming week, as a main factor of concern given the close Sino-Australian ties. Overall we do not see fundamentals favoring the Aussie, given the lack of a confident recovery of the Chinese economy and RBA’s dovish tilt. Also we highlight the market sentiment as a factor that could influence the Aussie’s direction, given that AUD is considered a riskier asset as a commodity currency.

CAD – Canada’s November CPI rates in focus

The CAD continued weakening for a third week in a row against the USD.

On a monetary level, BoC’s tended to provide some support for the Loonie on Wednesday. The bank delivered a 50 basis points rate cut, yet in his press conference BoC governor Macklem stated that “with the policy rate now substantially lower, we anticipate a more gradual approach to monetary policy if the economy evolves broadly as expected” signalling an easing in the bank’s rate cutting path. The comment was the element supporting the Loonie at the release.

Other than that, we also highlight the bank’s worries for Trump’s intentions to slap tariffs on Canadian products imported in the US. The bank’s worries seem to reflect also the market’s worries, which on a fundamental level tend to weigh on the Loonie. Oil prices for the time being seem not to play a key role in the Loonie’s direction, yet should oil prices get more support, we may see them supporting the Loonie as well.

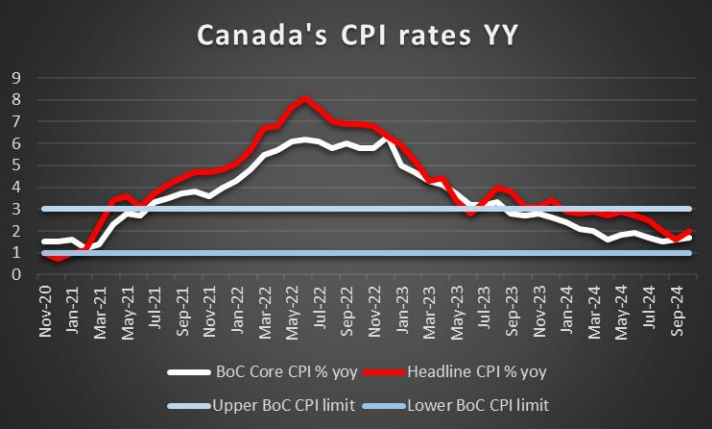

On a macroeconomic level, we highlight next week the release of Canada’s CPI rates for November next Tuesday. Should the rates continue to accelerate on a core and headline level, implying some persistence of inflationary pressures in the Canadian economy, we may see the Loonie getting some support as it could moderate BoC’s dovishness somewhat. Other than that, we may see Canada’s October retail sales next Friday stirring interest among Loonie traders.

Analyst’s opinion

We tend to remain bearish for the CAD in the coming week, given the uncertainty surrounding the Loonie at a fundamental level. Trump’s tariff threat yet may be countered by BoC’s intentions to ease its rate cutting path. A possible risk off mood of the market may also weigh on the CAD as could a possible drop of oil prices. Other than that we consider as a highlight for CAD traders in the coming week the release of the November CPI rates.

General Comment

As an epilogue we see the case for the Fed’s interest rate decision dominating the market’s interest until mid-week, at which point the USD may relent some of the initiative in the FX market. Overall, we expect the FX market trading mix in the coming week to remain relatively mixed, with some nice opportunities. As for US stockmarkets, we may see some cautiousness taking over, which may weigh on US stockmarkets, especially should the Fed show some hesitation in cutting rates further. Overall fundamentals are to lead US stockmarkets as after next week, we enter the Christmas week and interest may ease. As for gold’s price we note that its negative correlation with the USD seems to have been interrupted in the past few days. The Fed’s interest rate decision once again may interrupt the flow of gold’s price, while on a deeper fundamental level, China’s central bank seems to have rejuvenated its interest in gold prices which could have a bullish effect on the precious metal’s price.

Si vous avez des questions d'ordre général ou des commentaires concernant cet article, veuillez envoyer un email directement à notre équipe de recherche à l'adresse research_team@ironfx.com

Avertissement :

Ces informations ne doivent pas être considérées comme un conseil ou une recommandation d'investissement, mais uniquement comme une communication marketing. IronFX n'est pas responsable des données ou informations fournies par des tiers référencés, ou en lien hypertexte, dans cette communication.